Vertigo3d

DISCLAIMER: This word is meant for US recipients solely and, particularly, will not be directed at, nor meant to be relied upon by any UK recipients. Any data or evaluation on this word will not be a suggestion to promote or the solicitation of an supply to purchase any securities. Nothing on this word is meant to be funding recommendation and nor ought to it’s relied upon to make funding choices. Cestrian Capital Analysis, Inc., its workers, brokers or associates, together with the writer of this word, or associated individuals, could have a place in any shares, safety, or monetary instrument referenced on this word. Any opinions, analyses, or chances expressed on this word are these of the writer as of the word’s date of publication and are topic to vary with out discover. Corporations referenced on this word or their workers or associates could also be prospects of Cestrian Capital Analysis, Inc. Cestrian Capital Analysis, Inc. values each its independence and transparency and doesn’t imagine that this presents a fabric potential battle of curiosity or impacts the content material of its analysis or publications.

Nonetheless Too A lot Wetware And Too A lot Stuff

Righto. Salesforce (NYSE:CRM). Right here goes.

Your writer right here is outdated and remembers the 2004 Salesforce IPO. And a really thrilling factor it was too. Veterans of the pre-IPO Salesforce.com (because it was then recognized, as a result of the very addition of dot-com was as soon as price a couple of {dollars} on the share worth!) will let you know that deferred income accounting was a royal headache to elucidate to the SEC, that recruiting gross sales executives from perpetual license-driven rivals was powerful as a result of these fats ole license gross sales paid for some tremendous jolly boys’ outings to Maui and such, and that if you began speaking to folks usually about multi-tenanted database safety fashions, their eyes glazed over proper earlier than they discovered one thing extra attention-grabbing to do proper over there within the room subsequent door. It was, in brief, Onerous Work as the brand new child on the block with a product method that No person Favored and a set of fee plans that No person Favored and a set of accounting rules that No person Acquainted With GAAP Earlier than SOP97-2 Favored.

Regardless of which the factor mooned.

CRM vs SPY vs QQQ, Whole Return Since CRM IPO (Ycharts.com)

Salesforce although is now not the enfant horrible of enterprise software program; it is now extra cuddly grandpa on the skin with nonetheless a glint of veteran metal beneath the cardigan. The corporate has, with a minimum of some justification, begun trumpeting its AI credentials (however bear in mind even AT&T (T) is an AI inventory nowadays as a result of, you understand, AI means extra datacomm and all). However the query is, is the identify in its dotage, or does it nonetheless have a little bit spring in its step and a glint in its eye?

Headline Financials

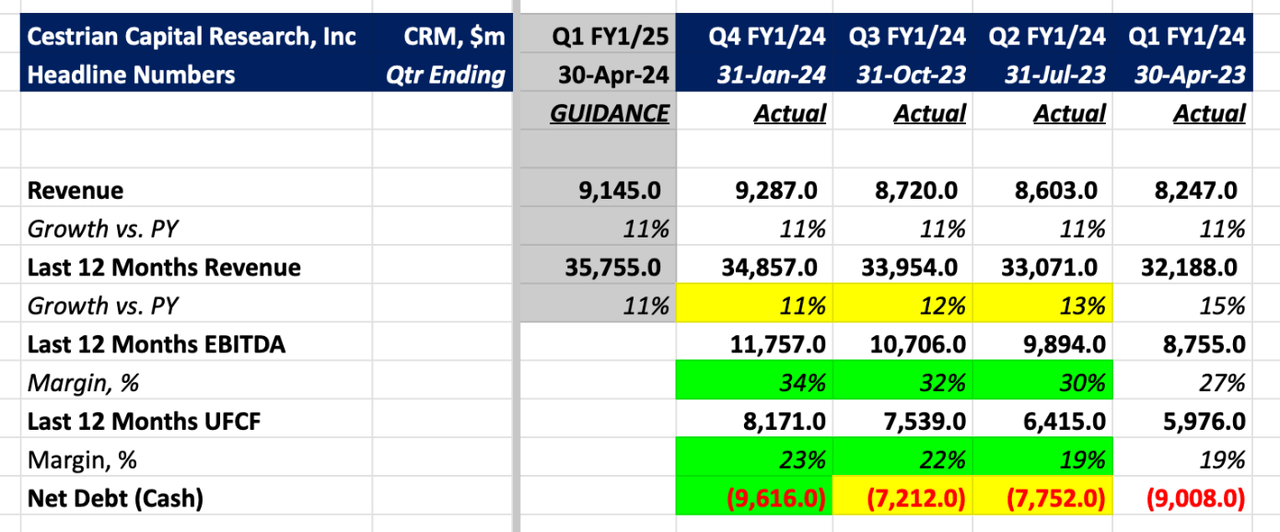

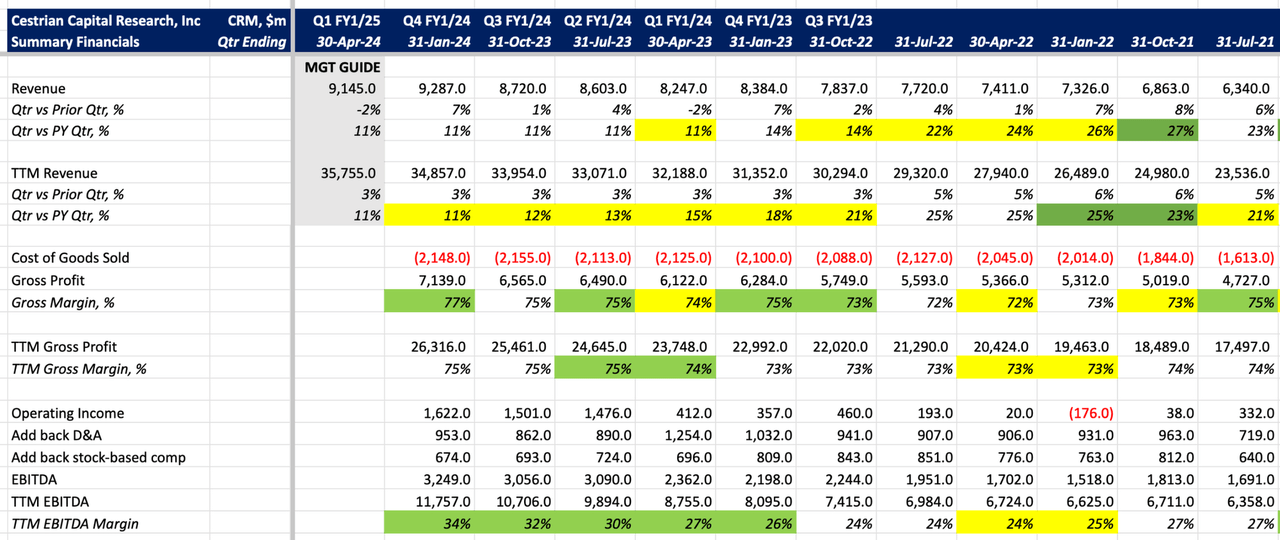

Essentially the most lately reported quarter was for 31 January 2024, this being This fall of their FY1/24. Listed here are the headlines.

CRM Abstract Financials (Firm SEC Filings, YCharts.com, Cestrian Evaluation)

Briefly:

- Income progress stays at 11% vs. earlier yr this quarter … the identical progress fee for the final three quarters … and the information for subsequent quarter is … you guessed it … 11%. That’s an uncommon stage of consistency.

- EBITDA and cashflow margins are climbing properly, however word the significant hole between them. For me, this implies I are likely to disregard EBITDA and give attention to cashflow, and people cashflow margins are fairly low for the extent of progress.

- The steadiness sheet is protected as homes, with virtually $10bn of web money now (should you deduct the worth of their long-term fairness investments, a extra cautious measure, you possibly can say there’s round $6bn web money).

My very own view on the basics is, meh. The corporate is in the course of additional restructuring – see the latest Wall Road Journal protection here – however that is nothing really main, and should you sit again, you could effectively conclude that 11% progress at 23% cashflow margins is nothing significantly particular.

You may take a look at youthful firms like CrowdStrike (CRWD) that are capable of develop at +36% on a TTM foundation while clocking in +19% TTM UFCF margins and conclude that is a greater steadiness.

CRWD Abstract Financials (Firm SEC Filings, YCharts.com, Cestrian Evaluation)

However, as everybody is aware of, fundamentals are merely one enter into the inventory worth, not even a very powerful enter. So let’s flip to evaluation of the inventory (the output materials), versus evaluation of the corporate (the enter).

Technical Evaluation

CRM inventory was really brutalized in 2022, overly so for my part. The inventory bottomed in December 2022, just some {dollars} above its late 2018 low. The restoration was equally sharp. We rated CRM at Accumulate between $138 and 166/share, reflecting the focus of institutional shopping for on the time; the inventory is now sat at round $305, having recovered from a modest selloff on earnings. So, a chance to have doubled your cash in not rather more than a yr, in a steady software program enterprise with a stable steadiness sheet. Not too shabby. This was our note back in November 2022.

CRM Notice, November 2022 (In search of Alpha, Cestrian Capital Analysis)

And now?

Nicely, this is how we see the inventory long run. You possibly can open a full web page model of this chart, here.

CRM Inventory Chart (TrendSpider.com, Cestrian Evaluation)

The inventory ought to have the ability to hit $325 with ease; we’re in a bull market and that’s solely the 100% extension of the prior Wave 1 positioned on the Wave 2 low. For now, we lengthen our Markup Zone solely to that stage.

However with a wind behind the inventory – and we predict we’re in a bull market with loads of wind in its sails but – $447 is not a foolish goal – that is the 1.618 Wave 3 extension of that prior Wave 1 positioned on the Wave 2 low. Which is a reasonably regular Wave 3 excessive. CRM could be boring for software program, however it’s excessive beta vs. the indices, as you possibly can see with one look on the chart above, so its potential to achieve 1.618 extensions is not actually in query for us. Potential, after all, isn’t any certainty; that is not my level – my level is a inventory this unstable can shock to the upside in a bull market simply as it will possibly shock to the draw back in a bear.

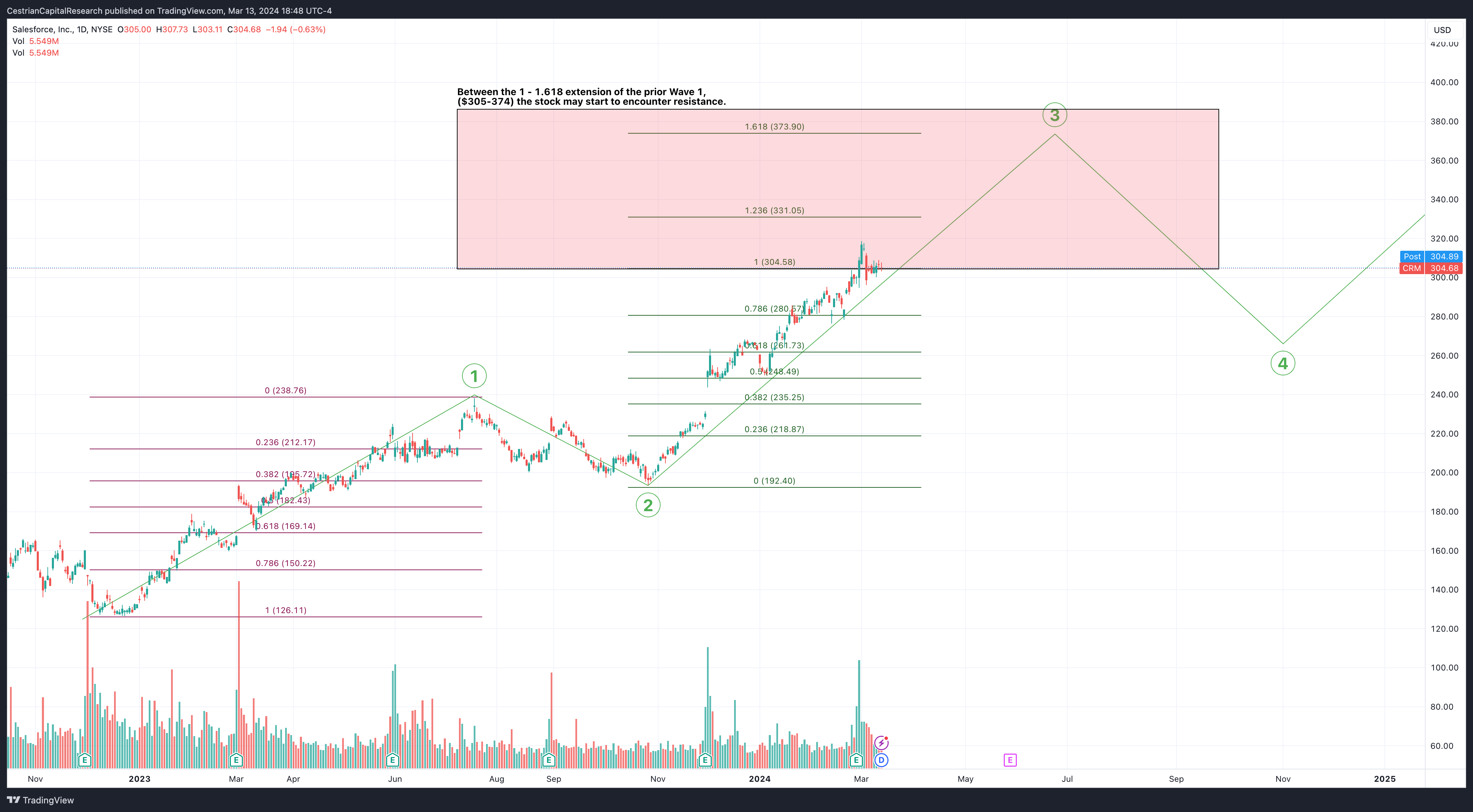

On a shorter-term foundation, the inventory has hit resistance and is in a consolidation sample proper across the 100% extension of the prior Wave 1. Once more, that is a modest extension at which to dump in a bull market, so extra upwards motion could also be anticipated. I might be stunned if the inventory climbed previous round $374 (the 1.618 extension of the prior Wave 1) earlier than a fabric retracement, however for the time being most surprises are to the upside, in order all the time one ought to let worth say what worth is and never attempt to second guess.

You possibly can open a full web page model of our shorter-term chart, here.

CRM Shorter Time period Chart (TradingView.com, Cestrian Evaluation)

Basic Evaluation

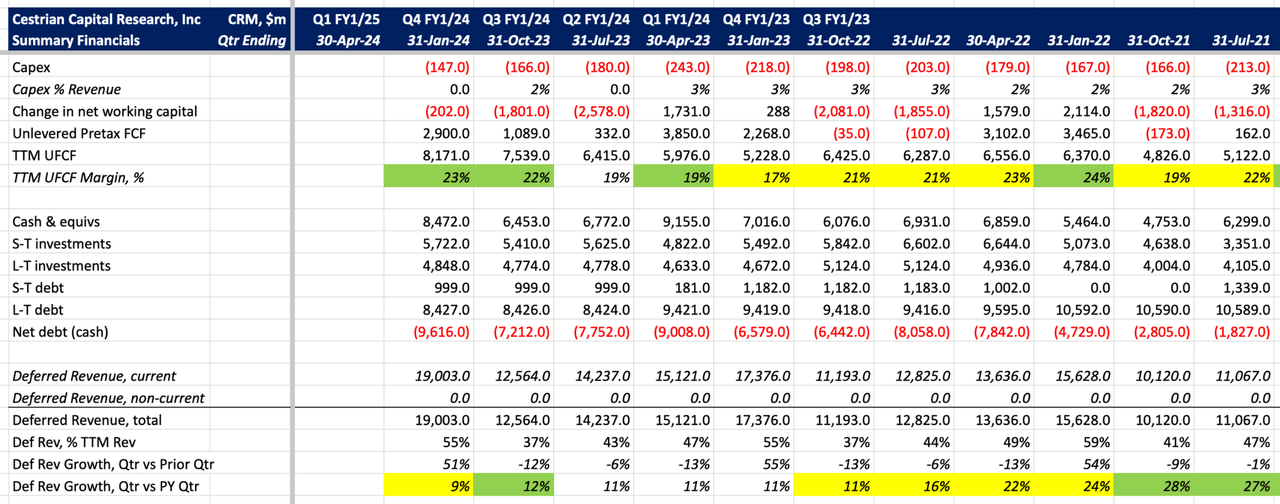

Let’s check out the detailed numbers earlier than we transfer on to valuation evaluation.

CRM Fundamentals I (Firm SEC filings, YCharts.com, Cestrian Evaluation) CRM Fundamentals II (Firm SEC filings, YCharts.com, Cestrian Evaluation)

Valuation Evaluation

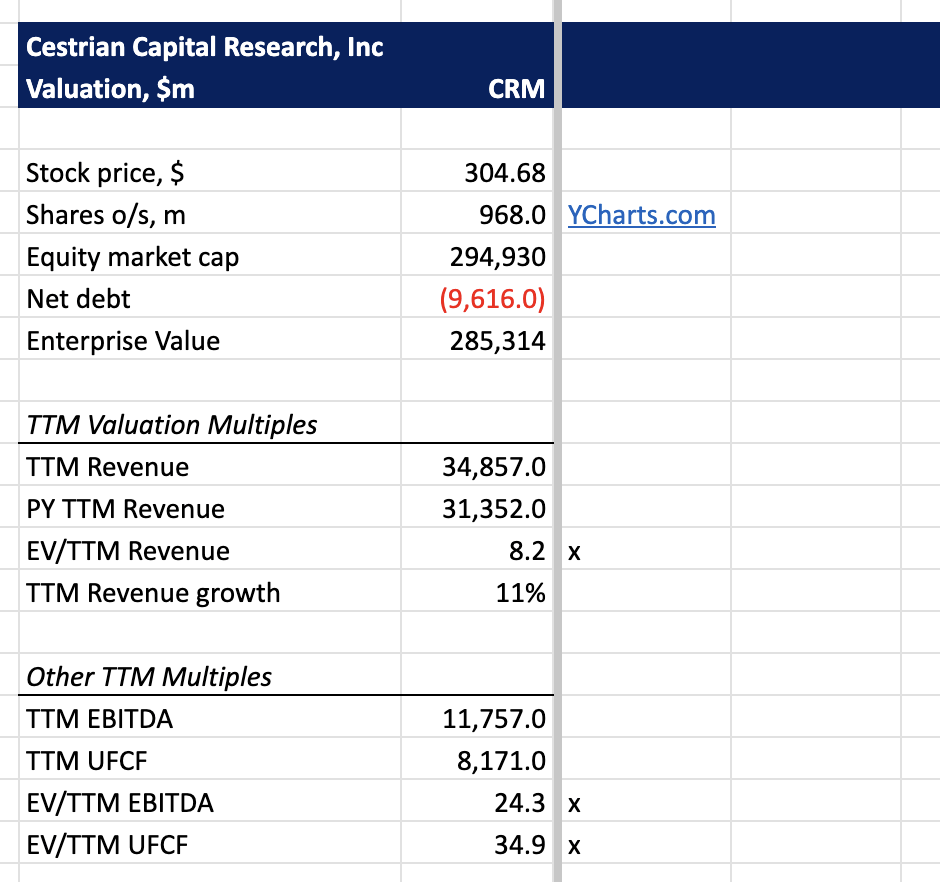

The inventory is a little bit dear for my part – nothing foolish, but when I used to be paying 35x cashflow for this factor, I might hope to see a extra aggressive restructuring plan in place in order that cashflow progress can be sooner than is at the moment the case. The present valuation although will not be a purpose to purchase or promote for my part – it isn’t near excessive lows or highs.

CRM Valuation Evaluation (Firm SEC filings, YCharts.com, Cestrian Evaluation)

Inventory Ranking

Formally talking, we fee the identify at Maintain as a result of if the market retains transferring up – which we predict it would, see our long-term take on markets here – then more than likely CRM can tag alongside, per our charts above.

Personally, although, I maintain no place within the identify as a result of I can consider different locations I would favor to have my capital put to work. On fundamentals, the corporate is neither fish nor fowl; not excessive progress, and never excessive margin both. As progress drops under 10%, which it seemingly will sooner or later, a well-managed mature software program enterprise must be clicking in 35-50% unlevered pretax free cashflow margins. CRM is reaching solely 23% TTM UFCF, which says that there’s nonetheless numerous wasted spending within the enterprise. Spending is ok if it ramps up the expansion fee, but when progress would not reply to spending, then at this stage of an organization’s lifecycle it ought to be reduce, for my part. There’s one thing of a restructuring program afoot at Salesforce however not, so far as I’m conscious, one that may ship Microsoft-style cashflow margins, and AI-washing will not ship larger progress both for my part. So, maintain, as a high-beta inventory in a bull market.

Any questions or feedback, have at it within the feedback discipline under. We learn all of them and endeavor to reply promptly.