da-kuk

Funding thesis

Opera (NASDAQ:OPRA) continues to point out first rate monetary efficiency because of its strategic initiatives and progress prospects. Nevertheless, since our preliminary protection, OPRA’s inventory value has risen and present upside isn’t that engaging, so we’re downgrading the inventory’s standing to HOLD.

This fall FY 2023 earnings assessment and income outlook

The corporate reported 4Q 2023 outcomes, which have been higher than our expectations.

- Income amounted to $113 mln (+17.4% YoY) towards our forecast of $113.2 mln, which was according to our expectations.

- GAAP EBITDA totaled $24.9 mln (+21% YoY), exceeding our estimate of $21.5 mln because of decrease advertising and marketing and personnel bills.

- Non-GAAP EBITDA (excluding dilution) was $27.8 mln (+21.9% YoY), 20% above our steering of $23.1 mln owing to a smaller base determine and a better proportion of worker share-based compensation.

The corporate reveals excessive income and EBITDA progress charges, pushed by elevated product penetration and buyer LTV (primarily because of the transition to GX):

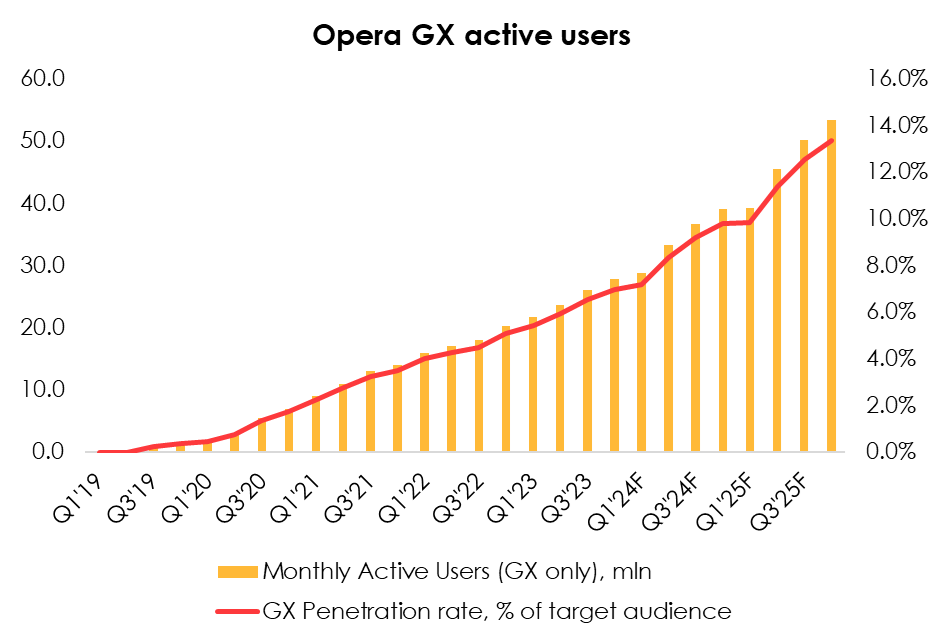

- The variety of lively customers (MAU) totaled 307.1 mln (-1.9% YoY), which was barely under our estimate of 308.9 mln (-1.8% YoY) because of slower buyer absorption by the Opera GX product. However, the expansion fee of browser customers stays robust: +40.7% YoY, 39.1 mln.

- The distinction within the variety of customers was offset by greater ARPU, which totaled $1.20/month (+21.8% YoY), barely exceeding our forecast of $1.19/month.

Regardless of a slowdown within the variety of lively customers, GX nonetheless has a low penetration fee relative to its target market, which is, in keeping with our calculations, about 7.0%. We consider that by the top of 2025 OPRA will be capable of enhance the penetration fee as much as 13%, virtually doubling its GX variety of customers.

Make investments Heroes

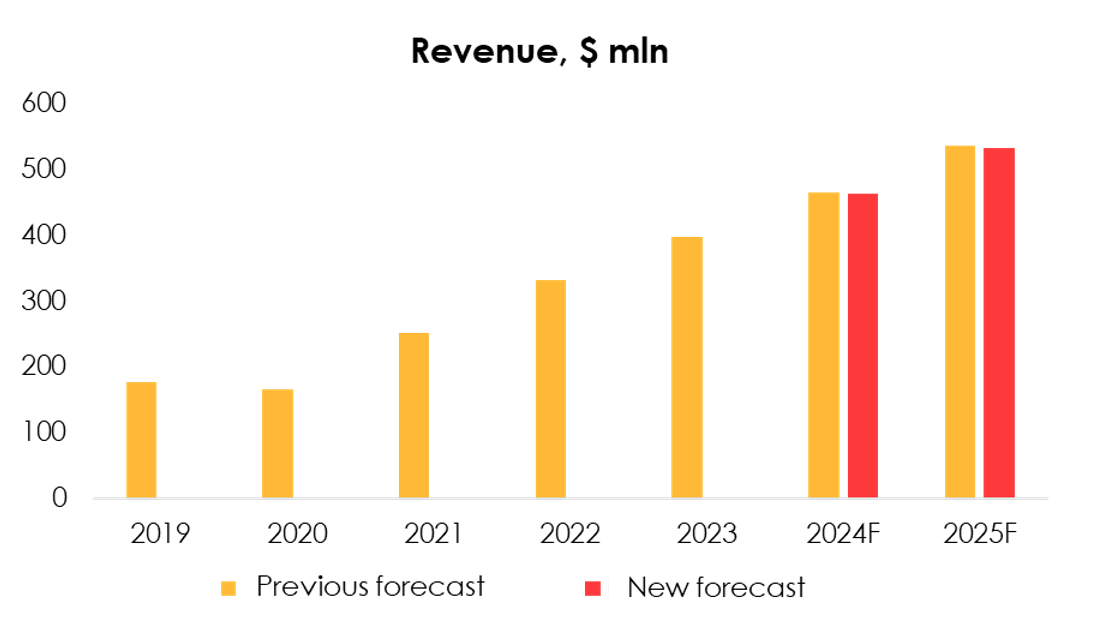

We’ve barely adjusted MAU and ARPU forecasts to replicate slower person base progress however greater ARPU progress. Thus, we now have revised downwards our income forecast from $466 mln (+17.4% YoY) to $464 mln (+16.8% YoY) for 2024 and from $536 mln (+15.2% YoY) to $532 mln (+14.7% YoY) for 2025.

Make investments Heroes

The administration expects 2024 income to be within the vary of $450-465 mln, which is according to our estimates.

Backside-line EBITDA progress was higher than anticipated

By way of working prices, the corporate reported higher numbers than our expectations because of the truth that personnel bills have been under our forecast by ~$1 mln and advertising and marketing bills by $2 mln.

Nevertheless, the share of money compensation to staff decreased over the interval because of a rise in fairness compensation. The corporate’s hiring fee is prone to stay low. We’ve downgraded our forecast for money compensation prices for 2024 from $78.5 mln (+13% YoY) to $74.4 mln (+13% YoY), however upgraded our outlook for fairness compensation to $11.1 mln (+6% YoY) from $6.3 mln (-32% YoY) and to $11.9 mln (+6% YoY) from $7.1 mln (+13% YoY) for 2025.

We’ve additionally adjusted the calculation of the corporate’s different gross bills (value of content material, stock bought and third-party platform commissions) taken under consideration seasonality, and revised downwards the forecast from $116.5 mln (+24% YoY) to $112.9 mln (+21% YoY) for 2024 and from $128.7 mln (+11% YoY) to $126.9 mln (+12.4% YoY) for 2025.

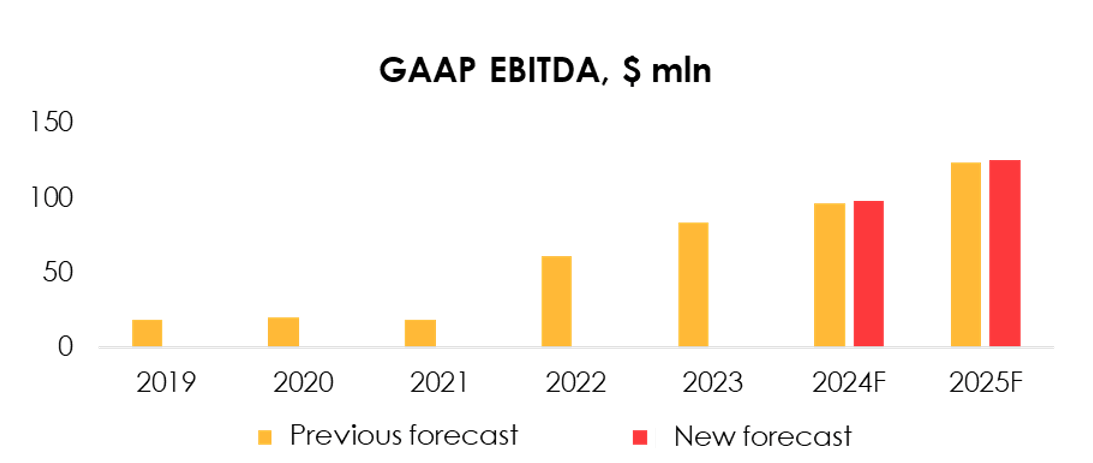

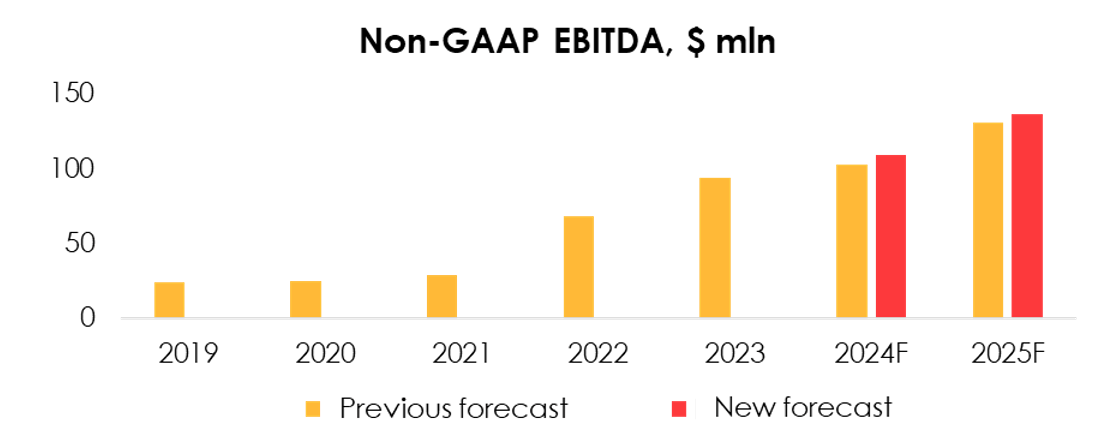

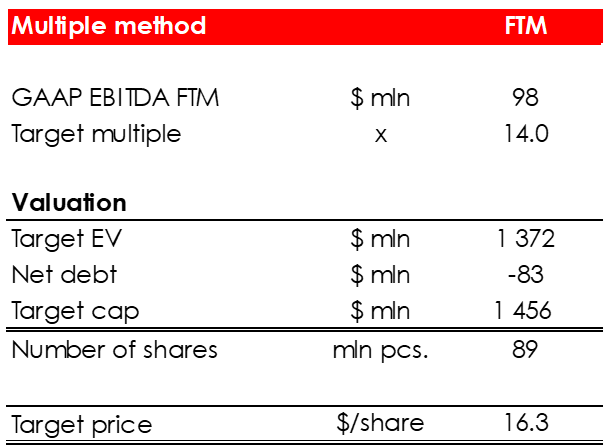

Thus, we now have revised upwards our estimate for GAAP EBITDA from $97 mln (+21% YoY) to $98 mln (+18% YoY) in 2024, and from $124 mln (+28% YoY) to $125 mln (+28% YoY) for 2025. By way of adjusted EBITDA, we now have upgraded the forecast from $103 mln (+10% YoY) to $109 mln (+17% YoY), and from $131 mln (+27% YoY) to $137 mln (+25% YoY) for 2025 given the elevated share of non-cash worker advantages.

Make investments Heroes Make investments Heroes

Valuation

For valuation functions, we use an trade EV/EBITDA a number of of 14.0x. The peer group for a number of estimates contains such corporations as Alphabet (GOOG) (GOOGL), pre-2022 Baidu (BIDU), Meta Platforms (META) and many others.

We’ve elevated our goal share value from $15.2 to $16.3 because of:

- improved EBITDA steering for 2024-2025;

- elevated internet money from $75 mln to $83 mln;

- shift in FTM valuation.

Based mostly on the brand new assumptions, we downgrade the inventory to HOLD.

Make investments Heroes

Conclusion

Regardless of the presence of great opponents reminiscent of Microsoft (MSFT) and Alphabet, Opera managed to seek out its target market and an unoccupied area of interest out there. The Opera GX product meets the calls for of recent avid gamers significantly better than its analogs, which permits the corporate to extend its person base and ARPU at a excessive fee. As well as, the corporate reveals a steady degree of profitability with out diluting shareholder capital. Nevertheless, after a post-earnings enhance, we’ve downgraded our score to HOLD.

To handle your positions, we suggest to observe Opera earnings releases.