Nastco

Welcome to a different installment of our CEF Market Weekly Evaluate, the place we focus on closed-end fund (CEF) market exercise from each the bottom-up – highlighting particular person fund information and occasions – in addition to the top-down – offering an summary of the broader market. We additionally attempt to present some historic context in addition to the related themes that look to be driving markets or that buyers must be conscious of.

This replace covers the interval by way of the second week of March. You’ll want to take a look at our different weekly updates protecting the enterprise growth firm (BDC) in addition to the preferreds/child bond markets for views throughout the broader revenue house.

Market Motion

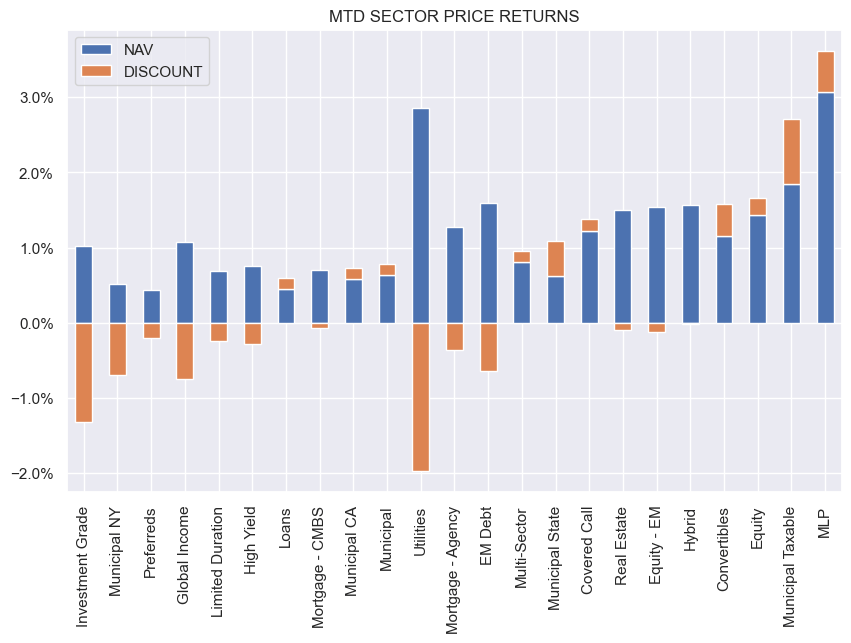

It was a superb week for CEFs with all sectors having fun with an increase in NAVs, nonetheless reductions had been blended. Largely equity-linked sectors completed within the lead.

Systematic Earnings

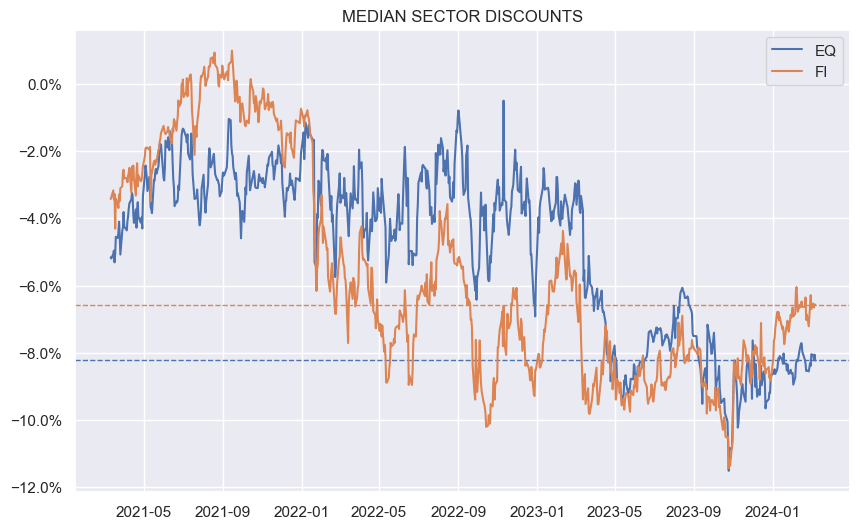

The hole between fixed-income and fairness CEF sector reductions stays. The mixture CEF low cost stays wider of its longer-term common; nonetheless, that is largely because of a handful of sectors akin to Munis and Coated Calls with the remainder of the CEF house now buying and selling round their longer-term averages.

Systematic Earnings

Market Themes

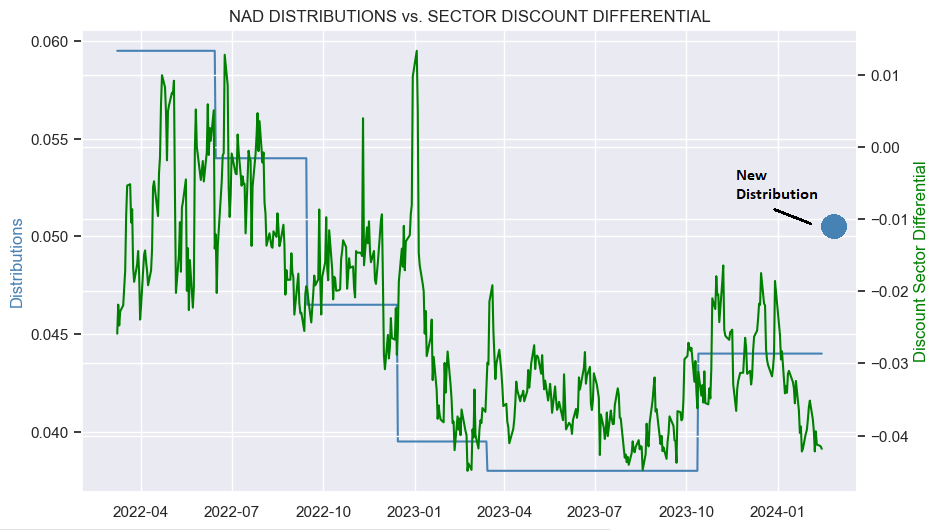

If at first you do not succeed… Nuveen is having one other go at boosting the reductions of their Muni CEFs by mountain climbing distributions. The reasoning within the press launch was the identical – to enhance market liquidity and to tighten reductions. The previous is a catch-all generic cause that managers use for something they do. And on the latter, recall that the earlier sizable hikes did not make a lot of a dent within the reductions. If something, it has been the lately broad-based market rally which has tightened Muni CEF reductions considerably.

The chart beneath exhibits that whereas the distribution has grown for NAD (blue line / dot), its relative low cost has truly widened – NAD trades at a reduction 4% wider than the sector common which is the widest degree over the previous 12 months. In different phrases, Nuveen’s transfer has failed to this point for NAD and lots of others of its funds.

Systematic Earnings

Realistically, we might have to attend for leverage prices to fall earlier than Muni CEF reductions tighten convincingly. The hike in distributions within the absence of internet revenue beneficial properties has not satisfied the market.

Market Commentary

The Virtus Convertible & Earnings 2024 Goal Time period Fund (CBH) sharply decreased its distribution. CBH is a goal time period CEF with a termination date in 2024. The press launch talked about the fund has rotated into short-term securities in anticipation of its termination. As is pretty widespread information, time period CEFs do not at all times terminate. And a supervisor like Virtus which has been busy buying current CEFs from smaller retailers (e.g. Allianz, Voya), will not be notably eager in dropping belongings and costs.

Nonetheless, a goal time period CEF construction (versus a plain time period construction) is a little more troublesome to show right into a perpetual fund as it might require a virtually complete turnover of the portfolio in addition to a shift in technique. If the fund truly terminates, it is probably this characteristic which is accountable. On this sense, goal time period CEFs usually tend to terminate than plain time period CEFs.

The PIMCO Dynamic Earnings Technique Fund (PDX) made a bunch of modifications in its distribution. First, it hiked the distribution by over 18% from $0.22 to $0.26. Then it converted from a quarterly to a month-to-month distribution. And eventually, that month-to-month distribution was hiked as effectively – from $0.0867 (the brand new $0.26 quarterly distribution / 3) to $0.1133 – by over 30%.

Internet internet the distribution was hiked by 55% and altered to a month-to-month profile. These modifications had been anticipated and mentioned in our final replace. Though the scale of the hike appears to be like giant, we’re ranging from a really low base of only a 3.8% distribution yield on NAV which brings us as much as solely 5.84% – a bit greater than half of what the corporate’s different taxable CEFs distribute. Though the distribution ought to preserve rising, we should not count on it to match the opposite taxable funds given the upper Vitality sector profile of the fund (leaving internet revenue decrease than the extra pure-play credit score funds) and its greater administration price.

Stance and Takeaways

Muni CEF reductions stay very large in each absolute and relative phrases. Managers of those funds have tried to tighten them by mountain climbing distributions. As we mentioned lately, a part of this is because of potential activist strain with Karpus, specifically, sniffing round many funds. In the end, we consider Muni CEF reductions will tighten; nonetheless, buyers might have to attend for the Fed to begin to lower the coverage fee first.

Take a look at Systematic Income and discover our Earnings Portfolios, engineered with each yield and threat administration concerns.

Use our highly effective Interactive Investor Instruments to navigate the BDC, CEF, OEF, most popular and child bond markets.

Learn our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Examine us out on a no-risk foundation – sign up for a 2-week free trial!