SDI Productions/E+ through Getty Photographs Hutchmed emblem (Hutchmed)

Funding Thesis

After we began to cowl HUTCHMED (China) Restricted (NASDAQ:HCM) again in February of 2023, it was primarily based on our curiosity to diversify our portfolio with the inclusion of shares in a pharmaceutical, medical, or healthcare firm.

Our introduction to HCM got here all by way of our curiosity in CK Hutchison Holdings in Hong Kong (OTCPK:CKHUY), the conglomerate that holds about 38% of the shares in HCM.

Simply as a reminder, HCM is a small however world biopharmaceutical firm creating high-quality, novel oncology and immunology drug candidates for sufferers internationally. Their market capitalization is about $3 billion.

In our earlier article in December final yr, we upgraded HCM from a Maintain to a Purchase on expectations of the corporate lastly beginning to flip worthwhile.

With the corporate’s 2023 monetary outcomes out, we’ll look at if the thesis continues to be legitimate.

2023 FY Monetary Outcomes

Allow us to begin with their high line.

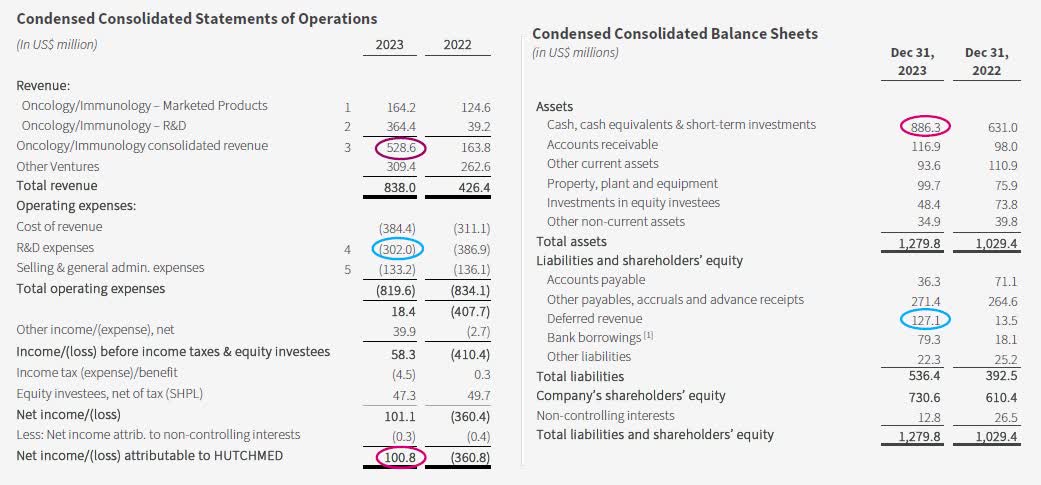

Their whole income doubled from final yr’s $ 426 million to $838 million in 2023. This massive leap can to some extent be defined by the $280 million that they obtained final yr from their associate Takeda (TAK), which has been granted unique advertising rights globally, aside from China, for the most cancers drug FRUZAQLA.

It was constructive to see how rapidly Takeda was in a position to ramp up gross sales of FRUZAQLA within the U.S. Upon receiving the FDA approval in October final yr, Takeda achieved $15 million in gross sales within the final 7 weeks of 2023 after the FDA approval was granted.

Administration has given guidance for their 2024 oncology gross sales to be within the $300 million to $400 million vary, pushed by a 30% to 50% progress goal for marketed product income.

On the underside line, HCM did handle to ship a revenue of $100.8 million, which works out to an EPS of $0.12

Restructuring of their U.S. business operation, prioritizing R&D investments, and tightly controlling working bills contributed to the constructive end in 2023.

Hutchmed P&L and Steadiness Sheet (Hutchmed FY 2023 monetary outcomes presentation)

It’s good to see that HCM had a powerful money place, as of the top of 2023 with over $880 million in money.

A part of that may be defined by the $400 million that Takeda is paying in royalty. The steadiness to be paid by Takeda over the following 3 years is $120 million.

However, gross sales from current merchandise and cheap expectations from their pipeline are the explanation the administration is assured that they are going to be worthwhile on their very own from 2025 onwards with none additional royalty funds or injection of fairness.

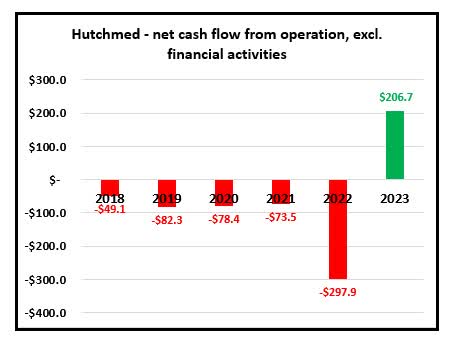

We’ve analyzed the money circulation, excluding finance, during the last six years.

Hutchmed money circulation going from destructive to constructive (Hutchmed Annual Reviews)

Financial institution borrowing was solely $79.3 million on the finish of final yr, and at an rate of interest that’s decrease than what they’re getting on their short-term deposits.

Lastly, we need to consider if there may very well be dividends to shareholders in a few years. To do that analysis, we have now turned to the Hong Kong inventory market. the place HCM additionally has a list and checked out what their friends in the identical trade are paying.

Dividend yield of different Hong Kong-listed Bio-Pharma firms (Aastock.com)

We imagine we have to see two to a few consecutive years of strong progress of 30 to 40% to compensate for the royalty earnings which can finish in 2026.

Solely then, can we look at extra intimately if natural EPS from gross sales and its free money circulation is excessive sufficient to justify a dividend to shareholders.

Proper now, it’s too early to think about.

Enterprise improvement

Though HCM has given Takeda unique rights to gross sales globally, it excludes China. There have not too long ago been some adjustments to China’s insurance policies which supplies extra help to affected person’s greater access to modern medicines. That’s constructive.

On FRUZAQLA, HCM is now ready for approval from the EU and Japan, which is predicted to happen someday later this yr. That can also be constructive, because it ought to garner additional progress in income and revenue going ahead.

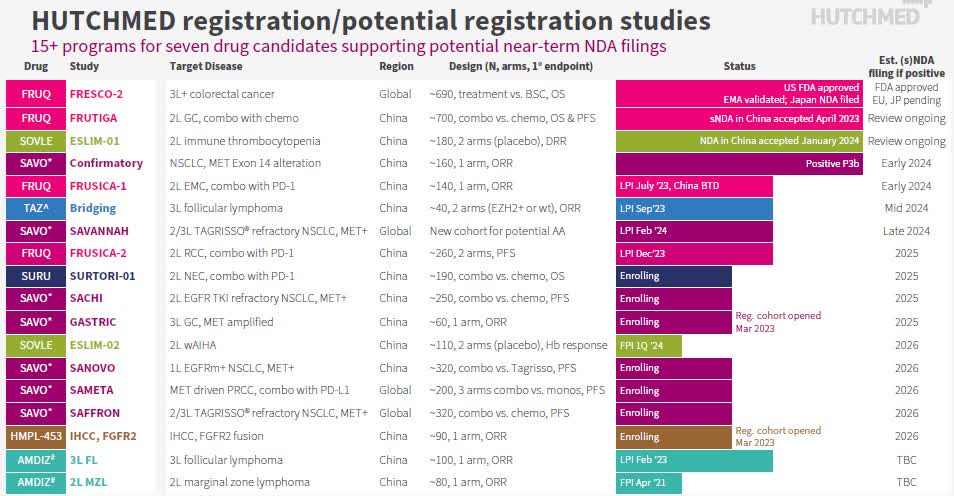

As well as, HCM does have a strong pipeline of recent merchandise with registration ongoing globally.

Hutchmed pipeline of recent merchandise (Hutchmed FY 2023 monetary consequence presentation)

Lastly, we want to report on the progress of their new manufacturing unit in Shanghai. In our article of 19th October final yr, we identified their progress technique which included the constructing of a brand new facility situated in Shanghai.

Progress goes properly, and so they have accomplished the development. With this new manufacturing unit in place, they need to be in a superb place to leverage this brand-new facility, which can give them 5 instances extra manufacturing capability. It’s anticipated to have the ability to provide from this new facility in 2025.

Dangers and conclusion

We’ve earlier said that one threat is that HCM may have little pricing energy in China for his or her medication because the pricing is negotiated and set by a authorities company. The chance is that HCM’s margin will deteriorate for merchandise bought domestically.

One other threat that we are able to consider is whether or not their important shareholders CKHUY will deal with minority shareholders properly. Our two largest e book losses in our portfolio are each managed by the Hutchison Group of firms. Maybe that’s only a coincidence.

If we look at CKHUY’s conduct up to now, they’re at all times lively in recycling capital by promoting off firms. One might due to this fact argue that a possibility might come up the place a big firm, like TAK which has a market cap of $46 billion, might doubtlessly launch a suggestion to accumulate HCM sooner or later.

We want to share Dr. Wei-Guo Su, CEO and Chief Scientific Officer’s comment to analysts through the firm’s presentation of the FY 2023 outcomes on the twenty eighth of February 2024:

And these regulatory actions will guarantee a gradual circulation of recent approvals and speed up our income and revenue progress in years to come back. We’re assured about our purpose of turning into self-sustaining by 2025 and properly positioned for accelerated progress past 2025.”

Though we did improve HCM from a Maintain to a Purchase in December final yr, the share value is down roughly 8%. It requires extra time to point out any potential signal of a better share value. It is just from subsequent yr that we imagine the expansion in earnings will likely be extra important.

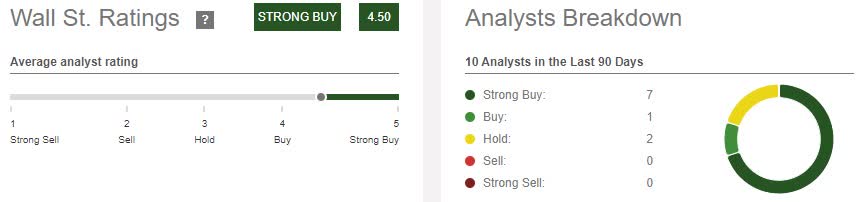

For what it’s price, in line with SA, Wall Avenue analysts have a Sturdy Purchase and there may be not one being bearish on HCM.

Wall Avenue has a powerful Purchase on HCM (SA)

We stay optimistic about HCM and preserve our stance unchanged.