Editor’s observe: Searching for Alpha is proud to welcome Claudiu Florin as a brand new contributor. It is easy to change into a Searching for Alpha contributor and earn cash on your greatest funding concepts. Energetic contributors additionally get free entry to SA Premium. Click here to find out more »

Phynart Studio

Funding Thesis

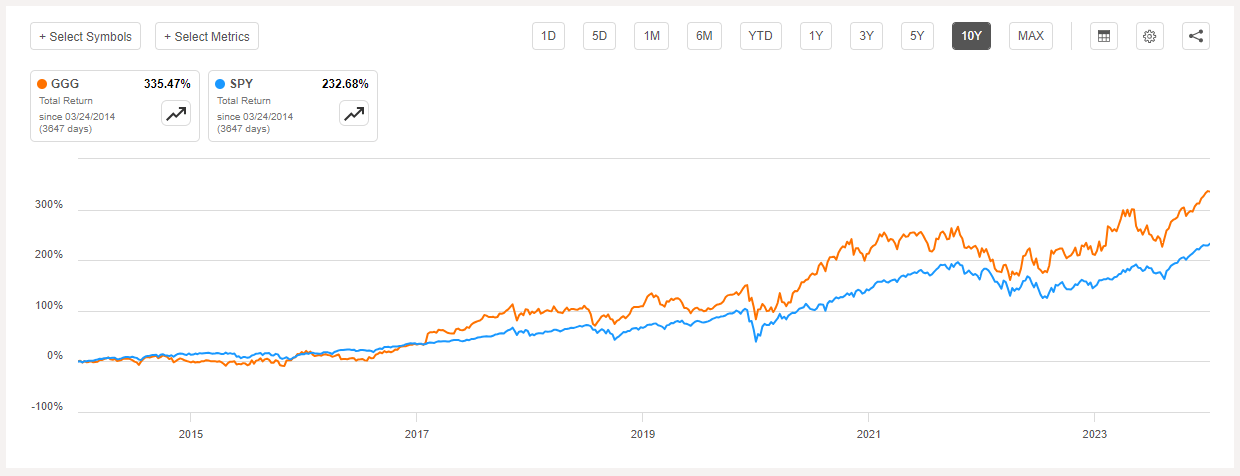

Graco (NYSE:GGG) is at all-time highs, and although the dividend yield supplied by this firm has been and nonetheless may be very low, as a result of worth appreciation, GGG has an annualized complete return during the last 10 years (~12.85%) that’s considerably above the S&P500 index (~8.78%).

For my part, the dividend is secure, given the mixture of a comparatively small payout from free money stream and a clear stability sheet. Ought to there be a reversion to honest worth, the corporate might nonetheless present a complete return above the market, contemplating its strong monetary standing and its standing as one of many business leaders.

On this article, we’ll see the place I consider GGG must be buying and selling near its honest worth, aiming to spend money on a superb firm at a superb worth. Given the present valuations, I am ranking the inventory as a maintain and I am going to clarify why in direction of the top.

Graco’s Efficiency in opposition to SPY (Searching for Alpha)

Enterprise Segments

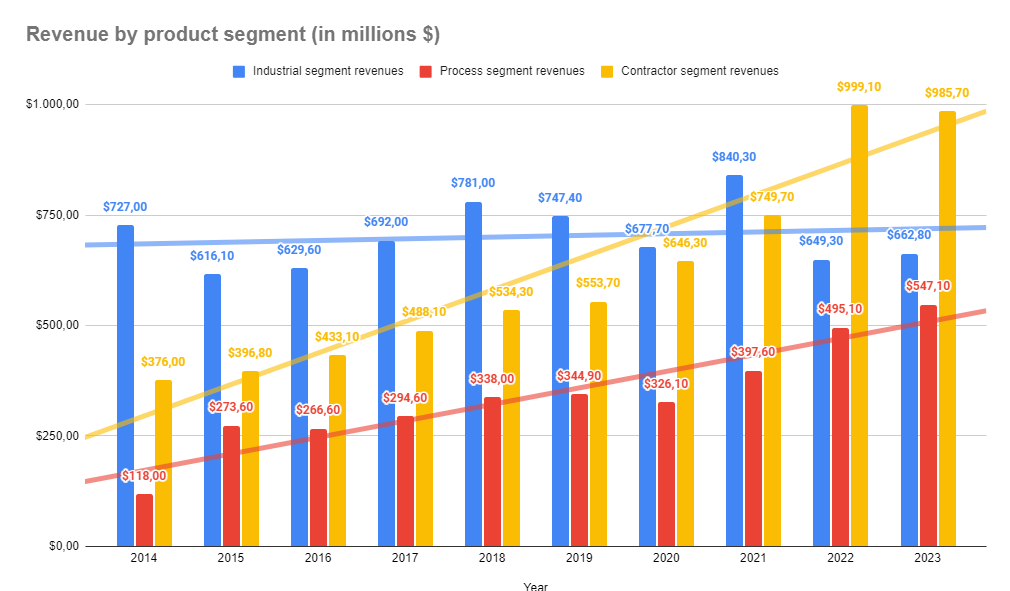

Graco’s operations are break up into three key segments: Contractor, Industrial, and Course of. Let’s take a more in-depth have a look at how these segments contribute to the corporate’s income and progress:

Contractor

Encompasses all merchandise associated to portray, insulation, adorning, or spraying processes, appropriate for each common clients, and for professionals or tradespeople who use them in numerous industries, the commonest being development and renovations inside houses and new or rehabilitated buildings.

Graco continually strives to signal contracts with an rising variety of distributors to facilitate the mediation between the corporate and the top buyer. This section is a very powerful each by way of the income generated, $985M in 2023, representing 45% of complete gross sales, and from the attitude of progress during the last 5 years, CAGR over 13%.

Industrial

Contains merchandise, gear, and methods utilized by industrial purchasers within the portray course of of assorted elements and elements, usually used inside the meeting of autos within the automotive, aviation, railway, maritime industries, and in addition within the technique of wooden portray. This whole section contributes 30% to annual revenues, in response to 2023 figures, amounting to $662M, and is split into two divisions: Industrial & Powder.

Course of

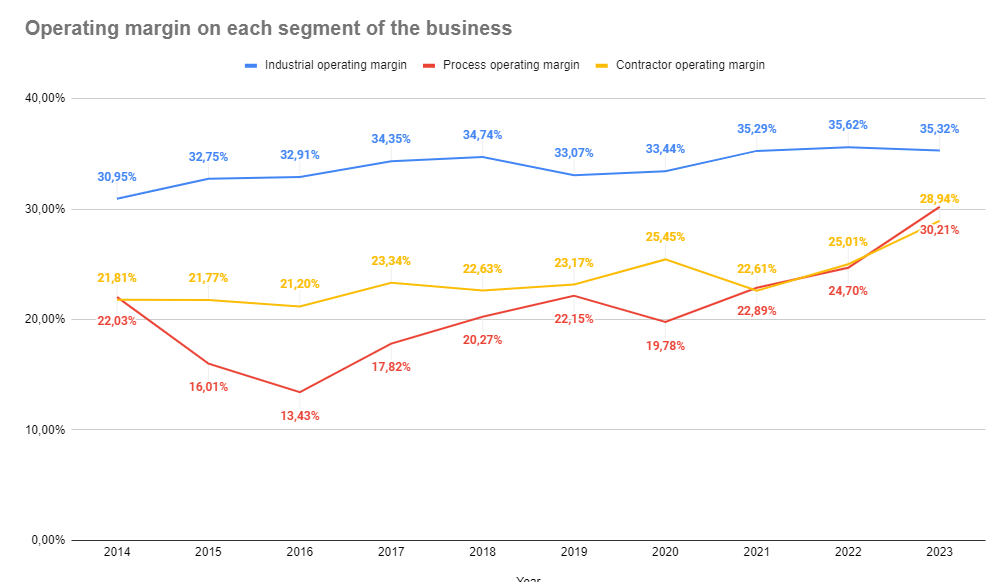

Contains a wide range of pumps, meters, valves, and equipment. Though it gives the smallest share of complete income, with $547M in 2023, representing 25%, all the section exhibits a robust upward development each by way of receipts and operational margin, which exceeded 30%, pushed by gross sales progress outpacing operational prices lately. This section can be divided into two divisions: Course of & Lubrication.

Graco’s Income by Enterprise Section (Creator’s personal Spreadsheet – Graco’s 10K)

Graco’s Op Margin by Enterprise Section (Creator’s personal Spreadsheet – Graco’s 10K)

The unfavorable efficiency of the Industrial section is as a result of firm administration’s resolution to switch foam-based merchandise, used for insulation or overlaying numerous surfaces, from the Industrial to the Contractor section. This resolution led to a 33% improve in income for the Contractor section in 2022 in comparison with 2021.

Geographical Presence

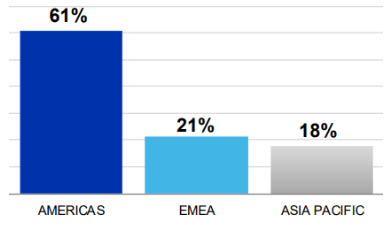

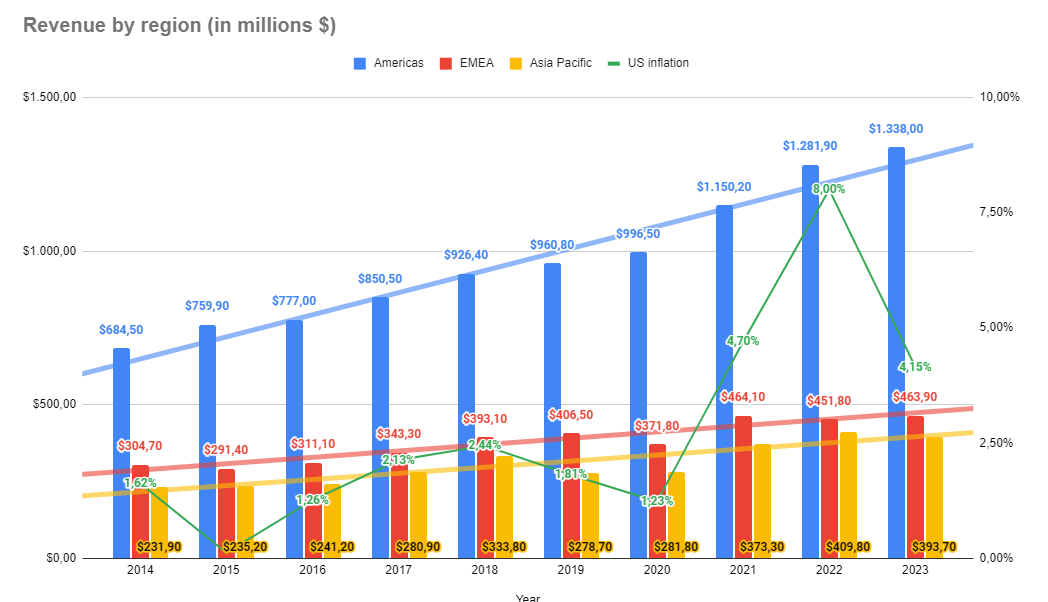

Graco is a enterprise with clients in over 100 nations, divided into three main areas:

Americas

Contains all three areas of the American continent (North, Central, and South), being the territory that contributes probably the most to annual revenues, with over $1.3 billion in 2023, representing ~61%. Nevertheless, of this complete, the USA offered over $1.1 billion, indicating it’s by far the primary marketplace for this enterprise.

EMEA

Encompasses Europe, the Center East, and Africa, with Graco incomes revenues of $463 million in 2023, accounting for ~21%. This area has had the bottom common progress during the last 5 years, particularly 3.95%, as a result of weak marketplace for new housing and constructing development, in addition to financial and geopolitical instabilities.

Asia Pacific

The one area that reported decrease revenues in 2023 in comparison with 2022, particularly a lower of -4%, attributable to unfavourable financial situations in China, and the influence of forex trade charges, given the constant appreciation of the dollar against the yuan. In complete, the area contributed $393 million to the revenues in 2023, representing the remaining ~18%.

Graco’s Revenues by Area (Graco’s 10K)

Graco’s Income by Area (Creator’s Personal Spreadsheet – Graco’s 10K)

Dividend

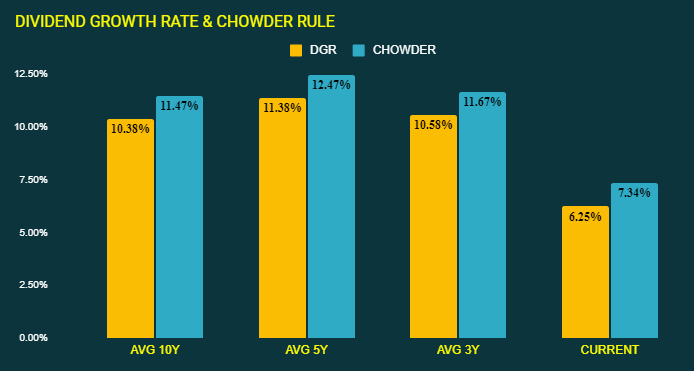

We’re a Dividend Champion, given its progress document that dates again to 1997.

Nevertheless, the present yield just isn’t very excessive, at solely ~1%, falling beneath the averages of the final three, 5, and ten years, which are not notably excessive themselves.

Regardless of the dividend progress percentages, displaying fairly excessive values, with 5 years DGR at ~11,3%, the dividend yield has been dragged down by the constant appreciation of GGG’s inventory worth, which is at an all-time excessive. This example would possibly deter traders from including this firm to their portfolio as a result of danger of “Poor Shareholders Return.”

Graco’s Chowder Rule (Creator’s Personal Spreadsheet – Searching for Alpha)

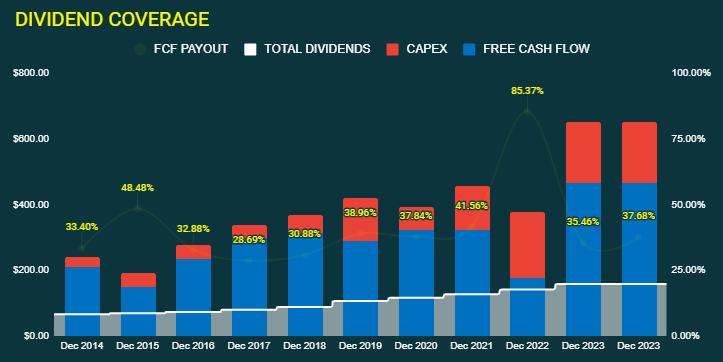

Nonetheless, for my part, the enterprise could also be appropriate for individuals who focus not on yield however on sustainability. Graco stands out as an acceptable selection due to the low percentages of Free Money Circulate it makes use of to pay dividends. Free Money Circulate Payout principally at 50% stage, this offers the corporate ample room to proceed distributing and rising dividends.

Graco’s Dividend Payout (Creator’s Personal Spreadsheet – Searching for Alpha)

Financials

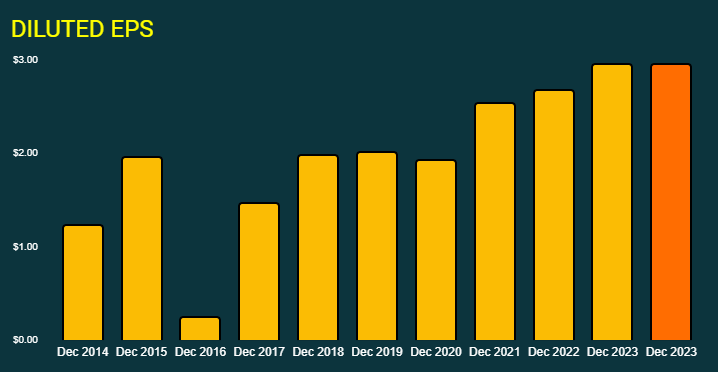

Graco’s Diluted EPS (Creator’s Personal Spreadsheet – Searching for Alpha)

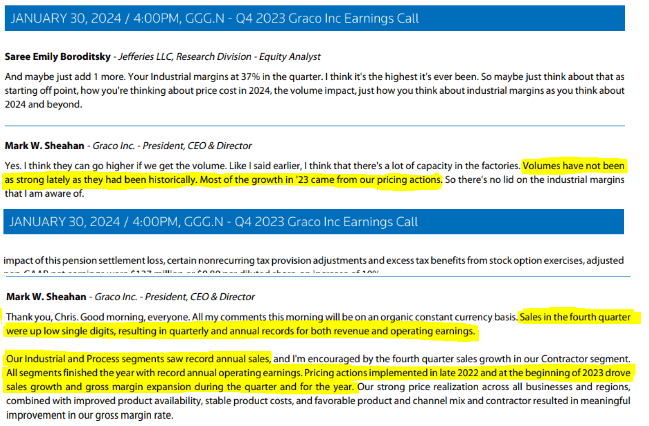

The fiscal yr 2023 got here bundled with quite a few data amongst its financials, influenced by the continual growth of the vary of apparatus and methods supplied to clients and worth will increase utilized to its merchandise, primarily through the finish of 2022 and starting of 2023. The latter cause had a extra important influence, particularly on income, a truth conveyed by Mark Sheahan, Graco’s CEO, by means of the Earnings Call for the fourth quarter and all the fiscal yr 2023.

Graco’s final Earnings Name (Graco’s Earnings Name)

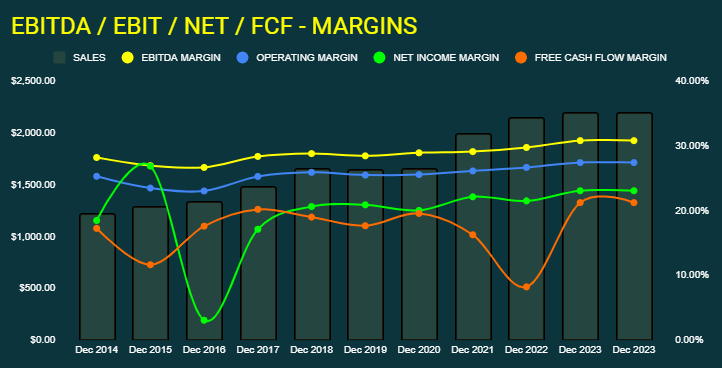

The scenario is comparable for web earnings, which surpassed the $500M mark, reaching the very best stage within the historical past of this enterprise. Identical for margins, the place most present an upward development and are on the highest values lately.

This illustrates the significance of an organization being among the many business leaders and having succesful administration to navigate inflationary intervals, with the intention of transferring the elevated manufacturing prices to the top buyer, a functionality sometimes called “Pricing Power”.

Graco’s Margins (Creator’s Personal Spreadsheet – Searching for Alpha)

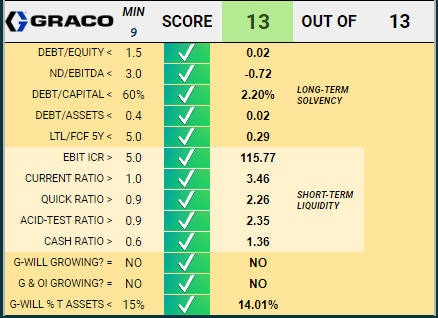

On the Stability Sheet aspect, there’s completely no situation; the corporate meets all 13 of the factors I analyse when evaluating an organization’s leverage.

Graco’s Debt (Creator’s Personal Spreadsheet – Searching for Alpha)

Within the 10K report issued for 2023, the place Graco presents the maturities of loans. Inside these, aside from these due in 2024, there aren’t any others listed.

Graco’s Debt maturities (Graco 10K)

Valuation

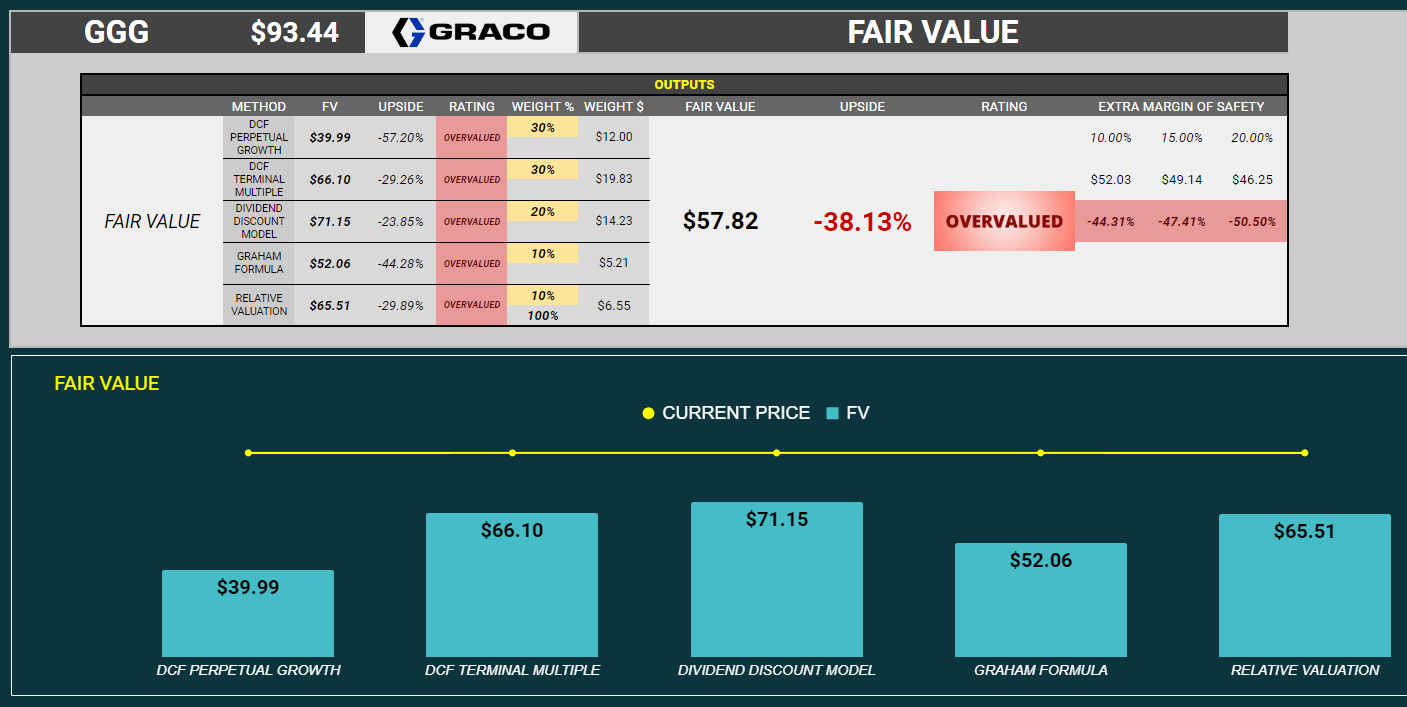

Relating to Valuation, I take advantage of 5 strategies to calculate an organization’s intrinsic worth:

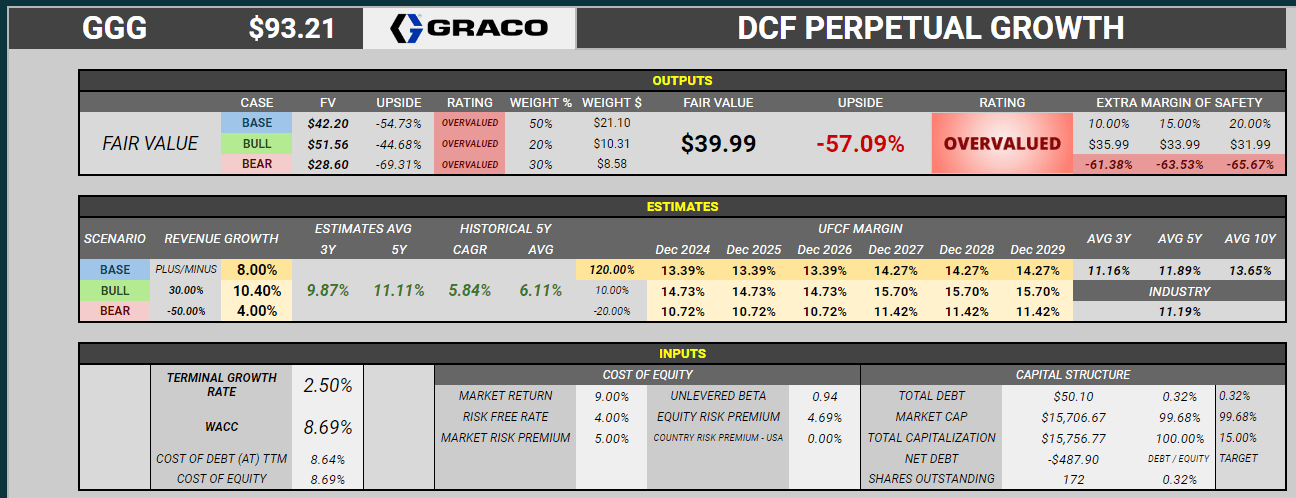

DCF Perpetual Progress – Weight 30%

Beginning with Income progress, I subsequent forecast the Unlevered Free Money Circulate Margin over the subsequent 5 years after which low cost again to the current utilizing WACC.

Based on Seeking Alpha Analysts Estimates for the upcoming three to 5 years, Income progress is anticipated to vary between 9% and 11%.

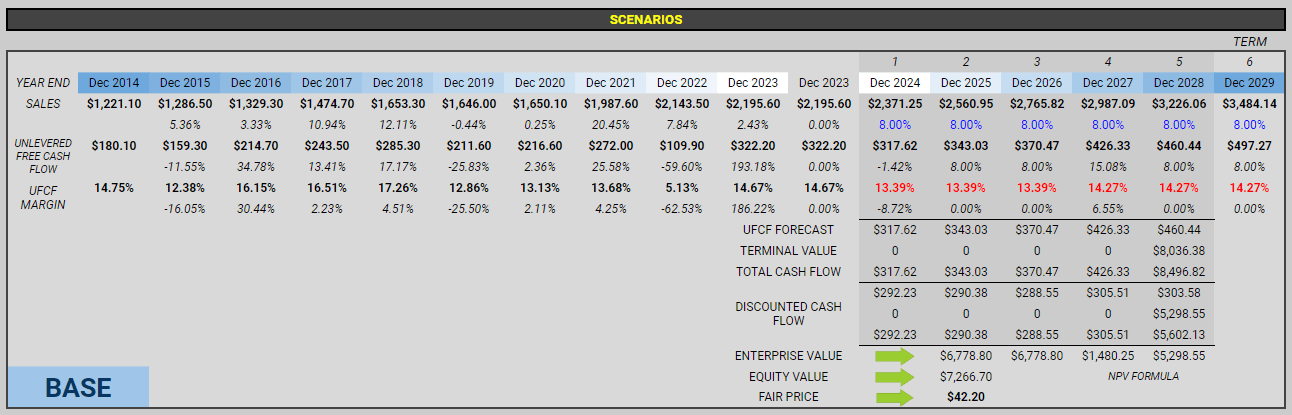

Choosing a conservative stance to make sure a better margin of security, I’ve chosen an 8% progress fee for the Base Case. Contemplating a Terminal Progress Fee of two.5% and a WACC of 8.69%, the honest worth on this state of affairs comes as much as round $42.

Graco DCF Perpetual Progress Valuation (Creator’s Personal Spreadsheet)

Assigning a 50% weight to the Base Case, a 30% weight to the Bear Case, and a 20% weight to the Bull Case, honest worth utilizing Discounted Money Circulate with Perpetual Progress comes as much as round $40.

Graco DCF Perpetual Progress Valuation (Creator’s Personal Spreadsheet)

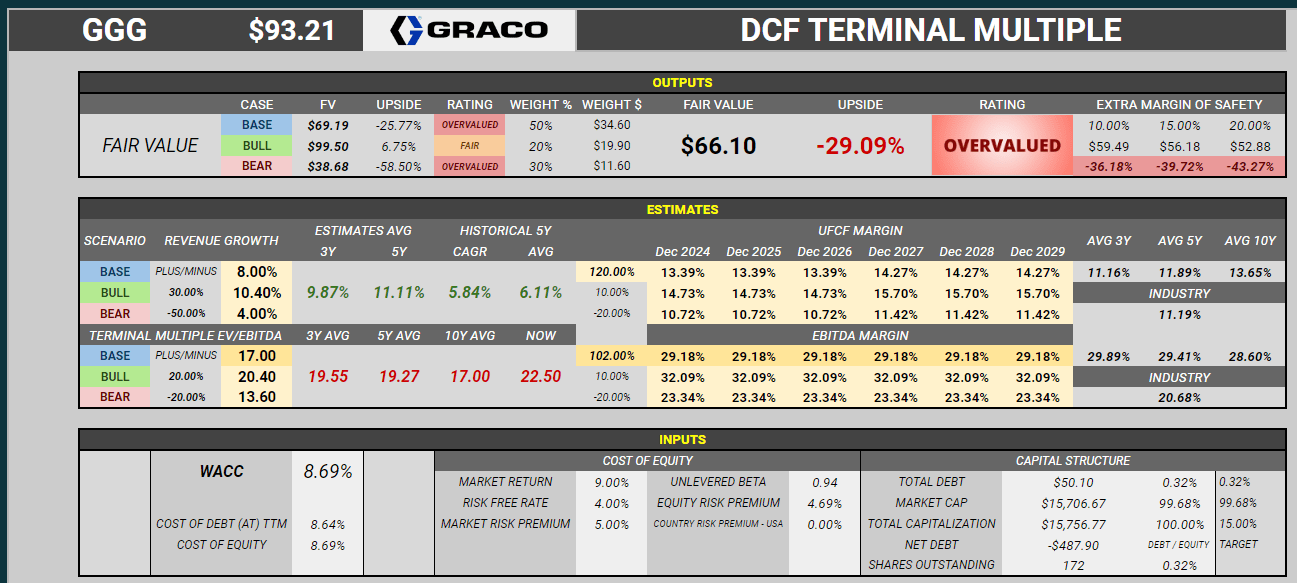

DCF Terminal A number of – Weight 30%

Identical because the earlier technique however this time I additionally venture EBITDA Margin and I apply a Terminal A number of as a substitute of Terminal Progress Fee.

Identical Income Progress, similar UFCF Margins, similar WACC, however with an EV/EBITDA Terminal A number of of 17, barely beneath Graco’s 5-year common of roughly 19 but according to the Trade Median, honest worth utilizing this technique comes as much as round $66.

Graco DCF Terminal A number of (Creator’s Personal Spreadsheet)

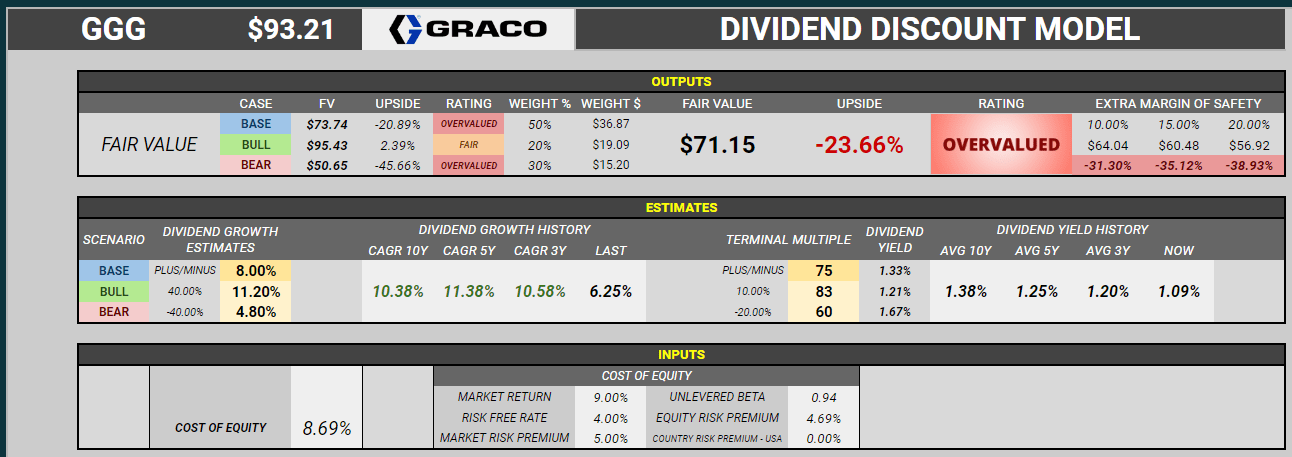

Dividend Low cost Mannequin – Weight 20%

I estimate the Dividend per Share (DPS) Progress for the subsequent 5 years, discounting these dividends again to the current utilizing the Value of Fairness, additionally in three eventualities with the identical weightings as earlier strategies. Then, I apply a terminal a number of within the type of Dividend Yield.

In Graco’s Base Case, I estimate a DPS Progress of 8.00%, primarily based on the aforementioned particulars within the Dividend Part, and a terminal a number of of 1.33% Dividend Yield, aligning with the traits during the last 10, 5, and three years. Honest worth utilizing this technique comes as much as round $71.

Graco Dividend Low cost Valuation (Creator’s Personal Spreadsheet)

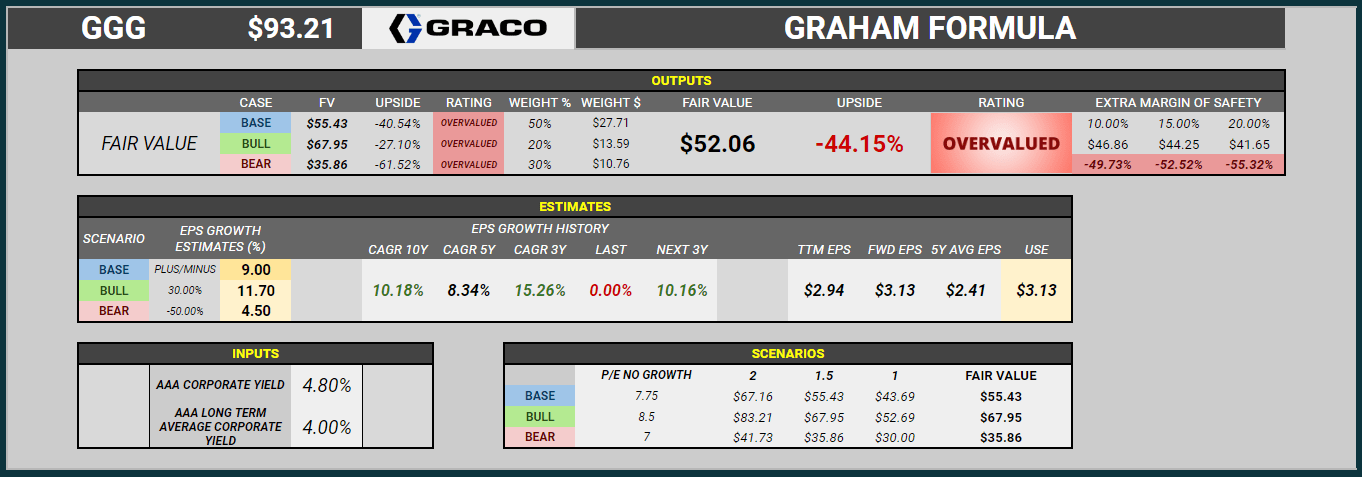

Graham Formulation – Weight 10%

Starting with an EPS of $3.13 as estimated by analysts for 2024 on Searching for Alpha, the typical progress fee for the next three years is roughly 10.16%, in response to the identical source. With the final 5 years’ EPS CAGR at round 8.34%, my estimate for the Base Case is 9.00%. Honest worth utilizing this technique comes as much as round $52.

Graco Graham Formulation Valuation (Creator’s Personal Spreadsheet)

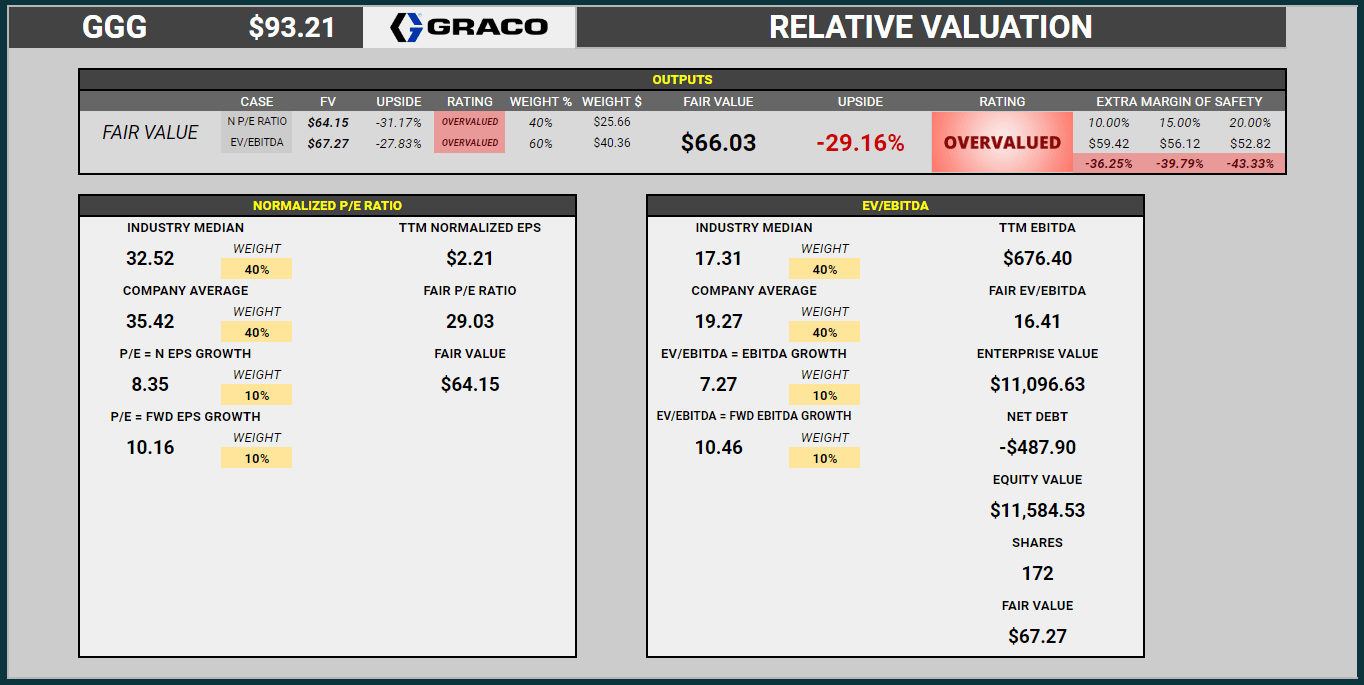

Relative Valuation – Weight 10%

I take advantage of two totally different valuation metrics right here: P/E Ratio and EV/EBITDA.

I strive then to give you honest worth a number of for every, utilizing 4 standards: Trade Median (P/E or EV/EBITDA), Firm Common for the final 5 years (P/E or EV/EBITDA), Equal the Progress of the final 5 years (Normalized EPS or EBITDA) and Equal Ahead Progress (Normalized EPS or EBITDA, with the final one coming from my EBITDA projections in DCF Terminal A number of Base Case).

On the finish I give 40% weight for P/E technique and 60% for EV/EBITDA technique as I all the time take into account P/E a much less dependable metric. Honest worth utilizing this technique comes as much as round $66.

Graco Relative Valuation (Creator’s Personal Spreadsheet)

With all of the above strategies, I take into account the honest worth for Graco to be someplace between $55 and $60.

Graco’s Valuation (Creator’s Personal Spreadsheet)

Moreover, I created a chart to see the correlation between the inventory worth and numerous metrics reminiscent of Normalized EPS, EBIT, EBITDA, Gross sales, and so on. Observing the correlation between GGG’s inventory worth and EBIT, this technique signifies a superb entry level, for my part, additionally round $60.

Graco EBIT & Value Correlation (Creator’s Personal Spreadsheet)

Important Dangers

Graco earns over 10% of its revenues from a single shopper, Sherwin-Williams, an American firm with an identical enterprise scope in that it produces, distributes, and sells paint-based merchandise, each from its personal manufacturing and bought from different entities, then resold to the top shopper. That is evident on their website, the place Graco merchandise might be discovered. Subsequently, any hostile scenario affecting this shopper might negatively influence Graco’s enterprise, particularly contemplating the extremely leveraged balance sheet of Sherwin-Williams.

Graco has come to acquire greater than half of its annual income from the USA market, making it weak to any occasion that would have an effect on the demand for its merchandise. Last clients could shift in direction of gear or methods with decrease costs, particularly in contexts the place shopper sentiment shifts in direction of spending much less, even when there’s a danger that the standard stage will not be the identical. Such selections from the American area may have a unfavorable influence on the gross sales quantity of Graco merchandise.

The first market Graco caters to, particularly the development business with a concentrate on homes and dwellings, has change into unstable. Key causes for this case in the USA embody:

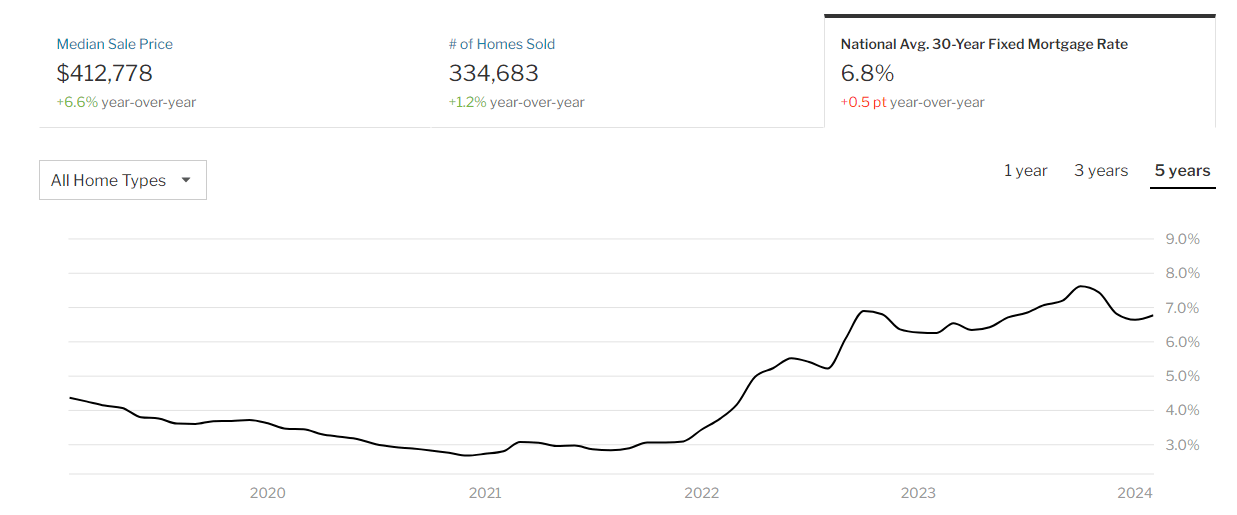

(1) Interest rates reaching a stage not seen since 2007, at 5.5%, main industrial banks to borrow from the central financial institution at increased charges, thereby providing increased charges to their purchasers. This reduces the variety of people qualifying for loans, as seen from the attitude of the typical rates of interest for 30-year loans reaching 6.8%, in comparison with 3% at first of 2021

The nationwide common 30 yr fastened fee mortgage fee(Redfin)

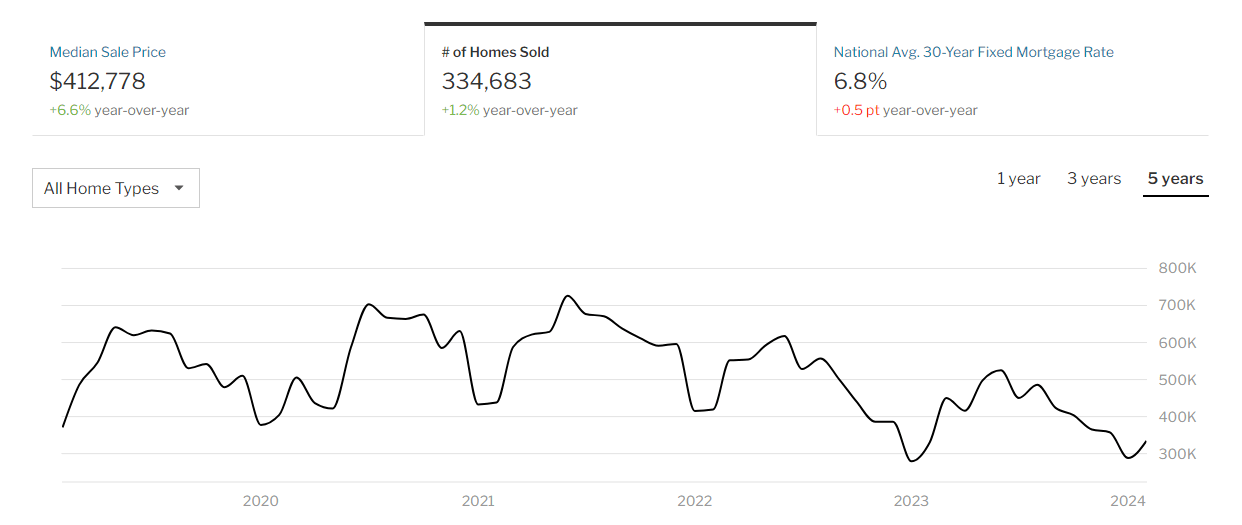

(2)The average price of homes, which, opposite to expectations and primarily based on the scenario described above, is repeatedly rising, influenced by the continued want of individuals to personal their dwelling and make money transactions by these not requiring a mortgage.

The typical worth in the USA market reached over $412K in February 2024, a 6.6% improve from the identical interval final yr. These causes, amongst many others, led to a greater than 50% lower within the variety of houses bought at first of 2024 in comparison with mid-2021, affecting firms within the business the place Graco operates, as order and gross sales volumes could enter a downward development.

Variety of houses bought(Redfin)

That is in all probability the best danger when contemplating such companies, and undoubtedly, a monetary and actual property recession akin to 2008-2009 would have important influence. Let’s check out how Graco and the GGG inventory fared throughout that interval to gauge their path within the occasion of an identical incidence. Financially, most metrics noticed constant declines, as revenues in 2009 have been 31% decrease in comparison with 2007, and web revenue for a similar years decreased by 68%.

Graco’s Financials 2005 – 2009(Graco’s 10K)

Moreover, between 2006 and 2009, the GGG inventory worth was down round -72%. Thus, occasions of this nature considerably have an effect on Graco’s enterprise, and whereas an identical recession could also be onerous to recur within the current or close to future attributable to stricter laws within the system, the market stays unstable, which means any downturn in demand will influence the quantity of merchandise and gear bought by the corporate.

Backside Line

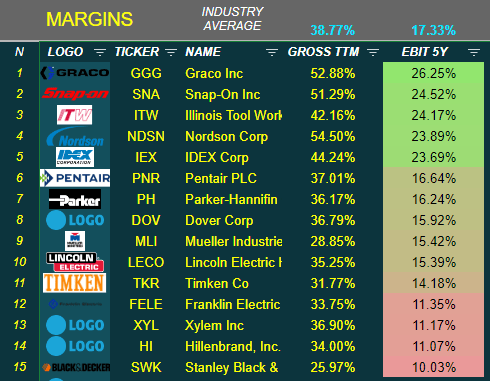

Graco is in a really advantageous place, rating among the many business leaders. We will see down beneath the gross margins for the trailing twelve months and the EBIT margin as a median of the final 5 years, with Graco main in opposition to different firms inside the business.

Graco In opposition to Rivals (Creator’s Personal Spreadsheet – Searching for Alpha)

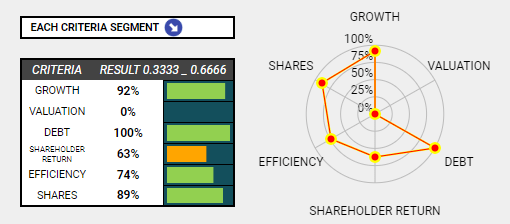

Its functionality to supply, develop, and market merchandise, methods, and gear throughout a broad vary of sectors repeatedly opens alternatives for innovation and reaching a large pool of potential clients. I take advantage of numerous standards to measure the corporate’s efficiency concerning Progress, Valuation, Debt, Shareholder Return & Shares Excellent, and the outcomes are excellent:

Graco’s Monetary Efficiency (Creator’s Personal Spreadsheet – Searching for Alpha)

Despite the fact that Graco appears to suit properly many funding portfolios, the final word and decisive issue is the inventory’s valuation.

From my viewpoint, GGG’s valuation is excessive, which personally compels me to attend on buying shares till the value falls into my comfy vary, particularly someplace below $70 at the least.

Drawing from Warren Buffett’s quote, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price,” I take into account Graco to be a beautiful firm however priced removed from honest.

Nevertheless, it would not be stunning to see the corporate buying and selling at a cheaper price, contemplating the outlined dangers. Nonetheless, if I already owned Graco shares, I positively would not promote them. The corporate performs very properly, has sturdy administration, and I personally make investments for the long run, believing it to be a mistake to promote shares strictly due to valuation. In conclusion, I give a HOLD ranking.