Michael Vi

Tencent (OTCPK:TCEHY) shares traded up 1.5-2.0% after the Chinese language tech big reported This fall and FY 2023 outcomes. Though income got here in considerably decrease than anticipated, earnings surged 23% YoY, comfortably beating consensus. As well as, Tencent shocked markets positively by revealing a $12.8 billion inventory buyback program (anticipated to be up 100% YoY), in addition to a 40% leap in dividend funds. Personally, I see the ramp up in distributions as a serious bull sign, as I’ve beforehand voiced unfavorable commentary on Tencent’s “unappealing shareholder distributions, which certainly are below levels that would justify investing in such a risky equity asset”. Contemplating up to date valuation metrics, most notably a decrease danger requirement for the fairness, I now estimate the intrinsic worth of Tencent to be round $49 per share. I improve the inventory to a “Buy” suggestion.

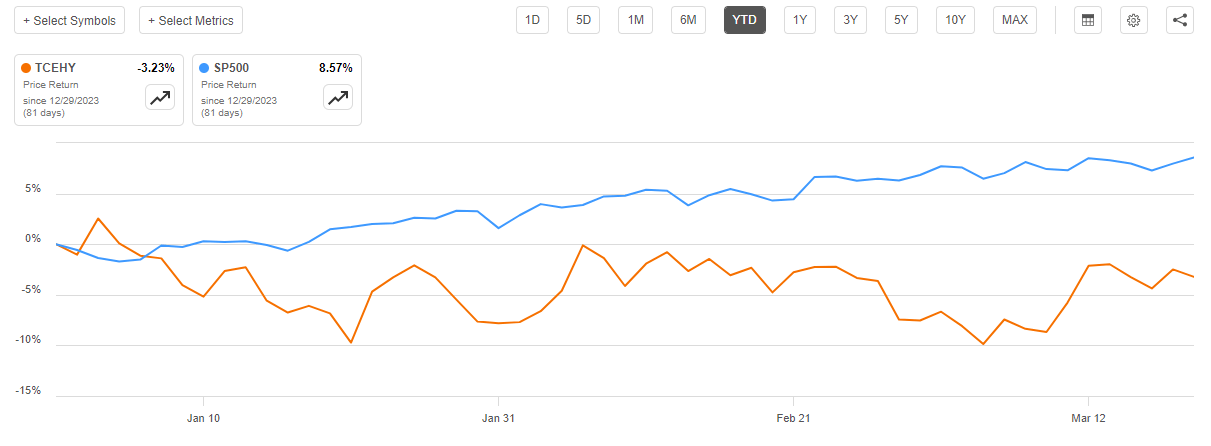

For context: Tencent inventory has grossly outperformed the broader U.S. inventory market YTD. Because the begin of the 12 months, TCEHY shares are down about 3%, in comparison with a achieve of just about 9% for the S&P 500 (SP500)

In search of Alpha

Tencent’s This fall Misses On Income, However Beats On Revenue Expectations

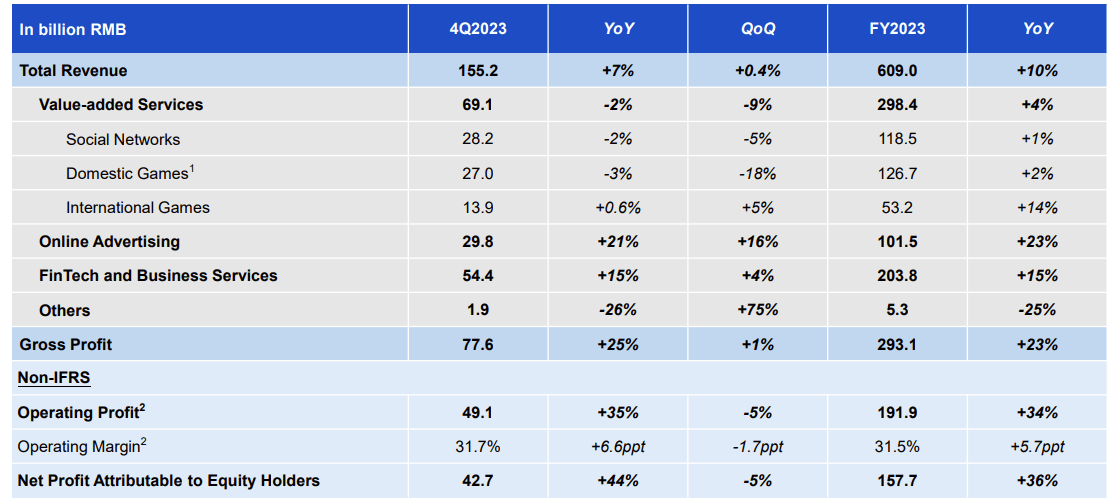

Tencent’s Q4 2023 upset expectations on topline, however shocked to the upside on revenue: Through the interval from September by means of the tip of December, the Chinese language expertise big reported a 7% year-over-year development in income, attaining RMB 155.2 billion in gross sales. This was barely under the analyst expectations, which had anticipated revenues of roughly RMB 157.4 billion, based on information compiled by Refinitv.

With regard to profitability, it’s notable to level out that Tencent’s gross revenue surged 25% year-over-year, to RMB 77.6 billion. In that context, Tencent administration identified that all through 2023, the corporate had been pushing to develop high-quality income streams, whereas phasing out the lower-quality ones. Furthermore, Tencent highlighted the accretive impression of value-added income on platforms for which prices have already been incurred in earlier intervals (akin to investments). Total, Tencent expects that the corporate’s “commitment to cost discipline” could have ongoing optimistic impact sooner or later.

The corporate’s working revenue margin for the fourth quarter was 31.7%, up 660 foundation factors in contrast tot he identical interval one 12 months earlier. By way of greenback worth, after taxes, Tencent’s non-GAAP internet revenue was reported at RMB 42.7 billion, a surge of 44% in comparison with This fall in 2022.

Tencent This fall reporting

Larger Shareholder Distributions Favorably Change The Fairness Story For Traders

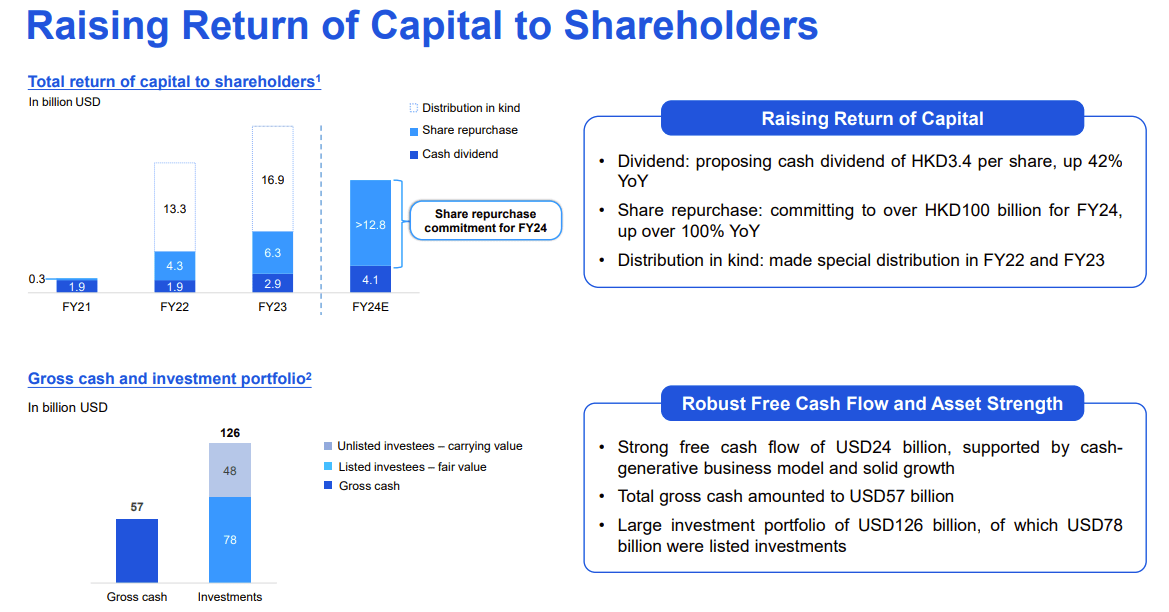

Reflecting on Tencent’s newest outcomes, a serious optimistic investor spotlight within the reporting is embedded within the firm’s announcement to supercharge shareholder distributions, in my view. Total, Tencent intends to considerably enhance its inventory repurchase program to a minimal of $12.8 billion in 2024, doubling from related buybacks in 2023. On high of this, Tencent additionally instructed plans to extend the annual dividend to fairness buyers by 40% YoY in comparison with 2022, distributing near $4.1 billion over the subsequent 12 months.

Assuming Tencent strikes on the announcement and certainly distributes $16.9 billion to buyers in 2024, I level out that the corporate’s fairness yield is poised to pattern round 5% (referencing a market capitalization of $339 billion as of twentieth March 2024).

Tencent This fall reporting

Discussing the uplift in shareholder distributions, I spotlight that Tencent cleared a serious hurdle that stored me from investing within the firm’s inventory. In truth, in late 2023 I argued:

I’m cautious to argue that Tencent inventory presents itself as a discount. One main subject that I’m seeing with Tencent shares pertains to the corporate’s unappealing shareholder distributions, which actually are under ranges that will justify investing in such a dangerous fairness asset. For the trailing twelve months, Tencent has distributed about $6.2 billion in type of share buybacks and 1.2 billion in type of dividends, partially offset by -$3.4 billion dilution for share based mostly compensation, bringing the online fairness payout to about $4 billion solely. In comparison with a $375 billion market capitalization, the payout is kind of unattractive, at ~1% yield.

Admittedly, the truth that Tencent supercharges shareholder distribution not solely displays a optimistic thesis worth, however probably additionally a unfavorable thesis on development: When an organization returns important capital to shareholders by means of dividends or share buybacks, it could point out that the corporate has extra cash than it could successfully reinvest in its personal enterprise. This may be seen as an indication that there are few development alternatives obtainable, or that the corporate can not discover investments with enticing returns. However the proof on the unfavorable development thesis should but to be seen. For reference, buyers ought to notice that main U.S. firms like Google (GOOG) (GOOGL), Apple (AAPL), and Microsoft (MSFT) have been distributing anyplace between 50-100% of FCF to shareholders for nearly a decade, and the businesses nonetheless handle to materialize enticing natural development for buyers. That mentioned, total, I feel the shareholder distributions are a serious optimistic sign for buyers.

Valuation Replace: Decrease Goal Worth

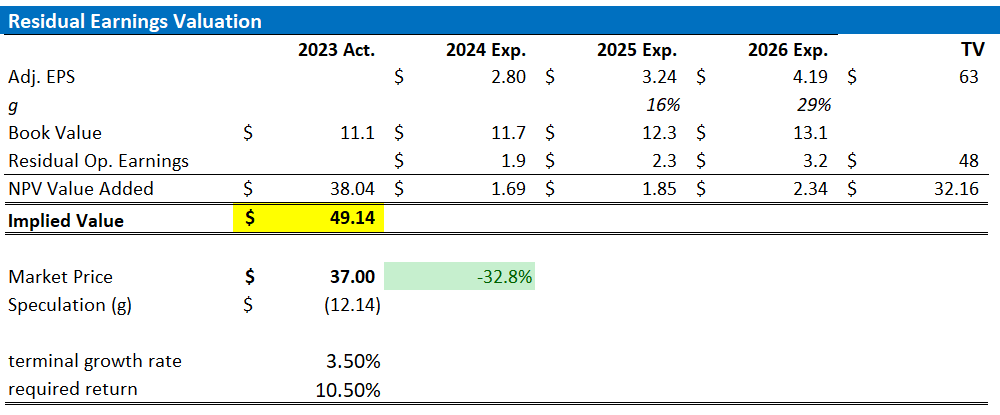

I replace my EPS projections for the Chinese language Tech big to align my estimates with analyst consensus revision over the previous 3 months, based on information collected by Refinitiv: I now anchor on EPS equal to $2.8 for FY 2023, vs $2.5 estimated beforehand. Furthermore, I alter my EPS enter for 2024 and 2025, to $3.24 and $4.19, respectively.

I proceed to base my valuation mannequin on – in my view – an inexpensive 3.5% terminal development price (one proportion level increased than estimated nominal international GDP development). Nevertheless, as a consequence of the capital distribution announcement, I cut back my value of fairness estimate by as a lot as 150 foundation factors, to 10.5%. Total, I nonetheless view Tencent’s danger estimate at a major premium to U.S. friends, reflecting the heightened regulatory danger overhang in China. For reference, my value of fairness estimate for Google and Microsoft are about 9% and eight.5%, respectively.

Given the changes as mentioned above, I now calculate a good implied share value for TCEHY equal to $49, seeing notable upside of about 33% in comparison with the corporate’s buying and selling value as of late March 2024.

Refinitiv; Firm Financials; Creator’s Calculations

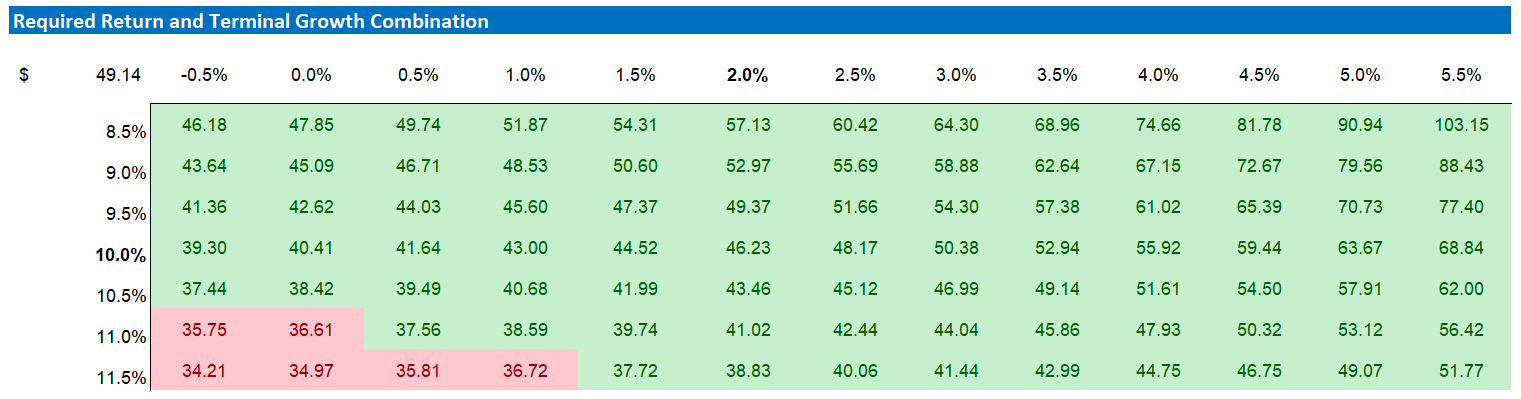

Beneath additionally the sensitivity desk, which checks totally different assumptions for value of fairness (row) in addition to terminal development price (column).

Refinitiv; Firm Financials; Creator’s Calculations

Investor Takeaway

Regardless of income falling barely in need of expectations, Tencent skilled a robust 23% YoY surge in earnings, surpassing market consensus. Furthermore, the corporate pleasantly shocked buyers by saying a $12.8 billion inventory buyback program, anticipated to double YoY, alongside a 40% enhance in dividend funds, doubtlessly reaching a 5% fairness return for FY 2024. Bearing in mind up to date valuation metrics, significantly a decreased danger evaluation for the fairness, I now estimate Tencent’s intrinsic worth to be roughly $49 per share, prompting me to improve my suggestion on the inventory to a “Buy.”

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.