Sashkinw/iStock by way of Getty Photos

Proudly owning shares is like being a passive proprietor of companies, and like for many enterprise homeowners, the payback interval is usually a top-of-mind concern. In spite of everything, getting your a reimbursement after which some is the rationale for why you’d begin a enterprise within the first place.

With the entire completely different channels on YouTube peddling “passive income” schemes like merchandising machines (which everyone knows just isn’t passive), one could also be fooled into considering that passive earnings requires work, when in truth these facet hustles require loads of time and labor.

The fantastic thing about proudly owning shares is that you’ve an expert administration crew in place to deal with the hassles of operating a enterprise in your behalf, and in the event that they pay you in return, then it turns into a really passive supply of earnings.

This brings me to Ares Capital (NASDAQ:ARCC), which I final covered in December final yr, highlighting its observe document of worth creation and well-covered dividend. Whereas ARCC hasn’t given a lot in manner of capital returns, altering in worth by simply +0.3% since my final piece, it is the dividends that make ARCC worthwhile, contributing to a 5.2% complete return.

On this article, I present key updates on ARCC together with its portfolio well being and working metrics, and focus on why ARCC stays a high quality alternative for top earnings, so let’s get began!

Why ARCC?

Ares Capital is the most important BDC by asset dimension, and is externally managed by a number one different asset supervisor, Ares Administration (ARES), which at the moment has $419 billion in belongings underneath administration of which $285 billion is expounded to credit score investments. Accessing ARES provides ARCC a line of sight into the credit score panorama and a helpful deal pipeline.

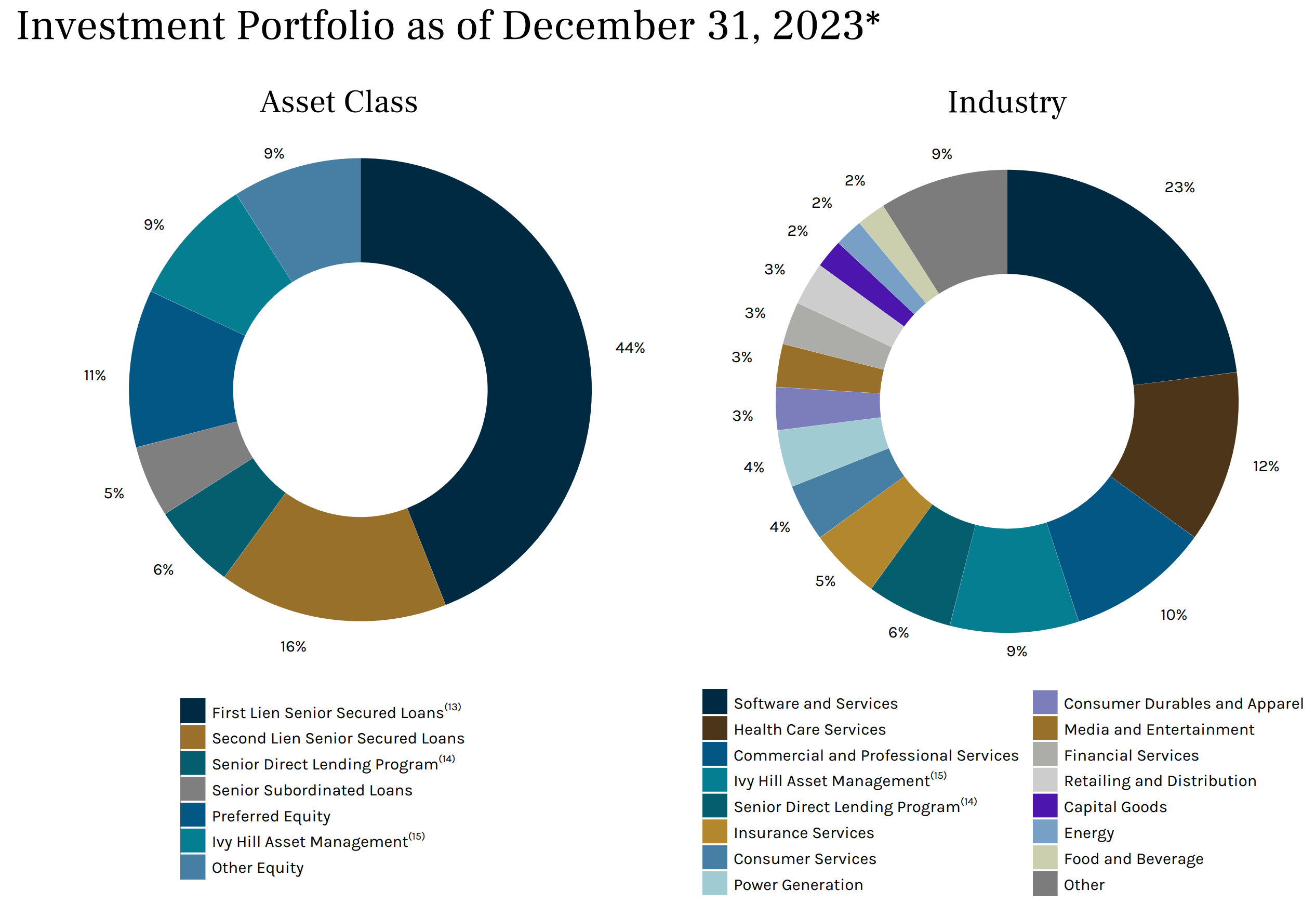

ARCC’s personal portfolio consists of $22.9 billion in investments at honest worth unfold throughout 505 portfolio corporations. Most of its investments (round 69%) are within the type of secured loans together with first lien (44%), second lien (16%) and a 9% funding in Ivy Hill Asset Administration, a related-party entity that invests primarily in secured debt. As proven under, ARCC invests primarily in development and defensive industries with Software program/Companies, Healthcare, and Skilled Companies, which make up almost half (45%) of the overall portfolio.

Investor Presentation

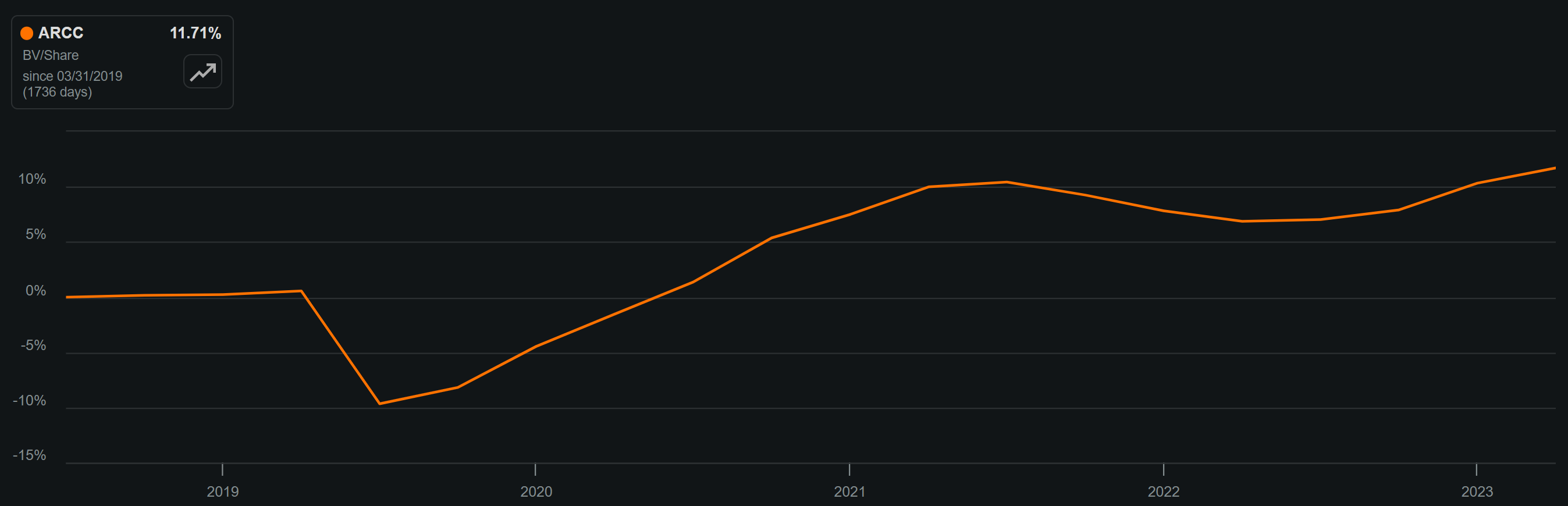

Importantly, ARCC has carried out a reasonably good job of preserving and rising its NAV per share over the previous 5 years and it was one of many few BDCs to truly develop its portfolio throughout 2020 when the pandemic hit. As proven under, ARCC’s e book worth per share now sits meaningfully greater than the place it was pre-2020, and has grown by 11.7% over the previous 5 years.

ARCC Guide Worth Per Share (Searching for Alpha)

This contains the newest This fall’23 outcomes launched on February seventh, which confirmed that NAV/share grew by a decent 5% YoY (1.3% development sequentially) to $19.24 together with document core EPS of $2.37 for the complete yr 2023, representing 17% development from $2.02 in 2022. This enabled ARCC to develop its dividend by 10% in 2023, and the present annual dividend charge of $1.92 implies that it is amply coated by a 123% Core EPS-to-Dividend protection ratio.

One of many drivers behind ARCC’s greater Core EPS is greater rates of interest, as 69% of ARCC’s complete portfolio is within the type of floating charge debt. This contributed to the 90 foundation factors YoY enhance in weighted common yield on income-producing belongings to 12.5% on the finish of 2023.

ARCC’s positive aspects over the previous 12 reported months had been pushed not solely by greater rates of interest, but additionally by the continued pullback in lending from banks, a development that started for the reason that Nice Recession in 2008. That is mirrored by substantial market share positive aspects by ARCC and by 90% of leveraged buyouts being accomplished by direct lenders moderately than banks in 2023. Throughout 2023, ARCC’s portfolio grew by $1.1 billion, with the majority of the expansion ($945 million) occurring in This fall, as deal exercise picked throughout the BDC business after a slowdown earlier within the yr.

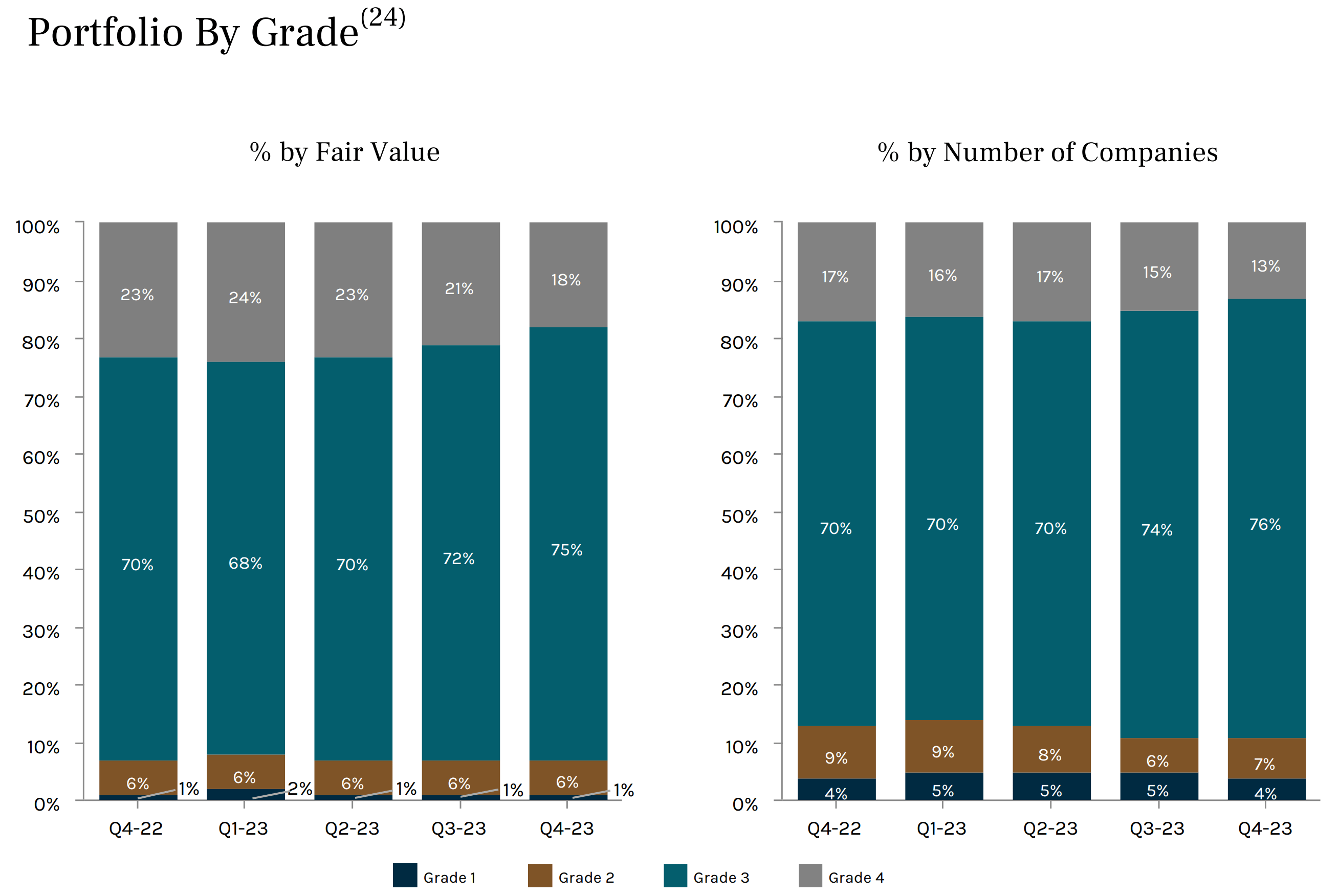

Notably, ARCC’s development and better curiosity don’t seem to have negatively impacted the standard of its underlying investments, as investments on non-accrual truly declined by 50 foundation factors YoY to 0.6% of honest worth (no change on a sequential QoQ foundation). Portfolio high quality can be supported by the proportion of ARCC’s investments at Grade 3 and 4 (on a scale from 1-4, with 4 being the very best high quality) rising by 2 proportion factors YoY to 89%, whereas the proportion of investments on the lowest Grade 1 remained secure at 4% from 2022 to 2023, as proven under.

Investor Presentation

Trying forward, ARCC is poised to proceed to experience heightened demand, because it’s moderately low leveraged with a debt-to-equity ratio of 1.07x, sitting nicely under the two.0x statutory restrict and under the 1.29x on the finish of 2022. Within the first month of Q1’24, ARCC had already made $705 million of latest funding commitments, of which 89% had been first lien senior secured loans and 94% had been floating charge, enabling it to reap the benefits of greater rates of interest. Administration famous the momentum round its enterprise over the last conference call:

In 2023 and into 2024, we have witnessed giant high-quality corporations that had been historically financed by the broadly syndicated markets turned to us to refinance their capital constructions, not as a result of they had been unable to entry the general public markets, however as a result of they most popular the steadiness that we offer via market cycles.

By leveraging the broader scale of Ares’ U.S. direct lending platform, we consider we will unlock worth for a variety of companies, whether or not they’re giant high-quality corporations looking for multibillion-dollar financings or strong-performing core middle-market corporations looking for a lender with versatile capital and the flexibility to assist development over time.

Dangers to ARCC embrace potential for decrease rates of interest because the Fed Chairman not too long ago acknowledged 3 rate cuts for this yr as being the aim. This may decrease the efficient yield on ARCC’s debt investments. Alternatively, a higher-for-longer rate of interest surroundings might hurt debtors and their potential to make funds on loans, particularly if there’s a laborious touchdown for the financial system.

Over the following few quarters, I’d search for indicators of ARCC’s potential to develop its portfolio via administration’s statements on borrower demand, as that would present an offset to probably decrease charges. As well as, I’d additionally deal with portfolio high quality as it could be best for ARCC to take care of a low non-accrual charge as described earlier. Increased non-accruals above 1.5% can be an indication that extra debtors are dealing with issues and be indicative of a higher-risk surroundings.

Turning to valuation, I proceed to seek out ARCC to be engaging on the present worth of $19.99, which equates to a price-to-book worth of 1.04x. That is truly barely cheaper than the 1.05x price-to-book worth from after I final visited the inventory on the finish of Q3, resulting from ARCC’s NAV/share development since then. That is moderately engaging, as ARCC has traded as excessive as a 17% premium to NAV over the previous 5 years, as proven under. Contemplating ARCC’s sturdy stability sheet, portfolio high quality, and heightened potential for deal exercise, I consider traders would do nicely to purchase ARCC as much as 1.1x Value-to-NAV as a conservative estimate.

ARCC Value-to-Guide (Searching for Alpha)

Investor Takeaway

Whereas some social media influencers spotlight “passive income” that isn’t actually passive, traders who know higher could do nicely to tune out that noise and layer into high-quality names like ARCC. ARCC has carried out respectably nicely in recent times, and is nicely positioned to proceed its development trajectory. With a powerful stability sheet, diversified portfolio, NAV/share development, and favorable business developments, ARCC is poised to profit from continued demand for direct lending. Whereas traders ought to regulate rates of interest and portfolio high quality, I discover the inventory engaging on the present valuation with a 9.6% yield that is nicely coated by earnings. As such, I preserve a “Purchase’ ranking on the inventory.