Michael M. Santiago

Thesis

In my previous article (launched in Q3 2023, which have been launched on October 13) that lined JPMorgan Chase & Co. (NYSE:JPM), I assigned a robust purchase score citing that its estimated truthful worth was round $314.74, an 85% upside from the inventory worth on the time of $170.1. The inventory worth is round $196.6, which signifies that the inventory has elevated by 15.57% since my earlier article.

On this article, I’ll replace my mannequin on JPMorgan with the knowledge from Q4 2023, launched on January 12. After concluding the valuation course of, I arrived at an estimated truthful worth per share of $237.41, which is a 20.7% upside from the present inventory worth of $196.6. Moreover, the mannequin suggests a future worth of $407.06, which means 17.8% annual returns all through 2029.

Overview

Progress plan

JPMorgan announced on February 6 that they’d open round 500 new branches by 2027. This in fact represents a danger and a possibility. The chance is to get deposits from individuals who weren’t close to a JPMorgan Chase department. This growth is generally centered on low-income areas and rural communities. The danger is that if not sufficient individuals (or companies) put their cash into JPMorgan, this is able to imply that a part of these 500 new branches might be unprofitable.

How does JPMorgan evaluate towards friends?

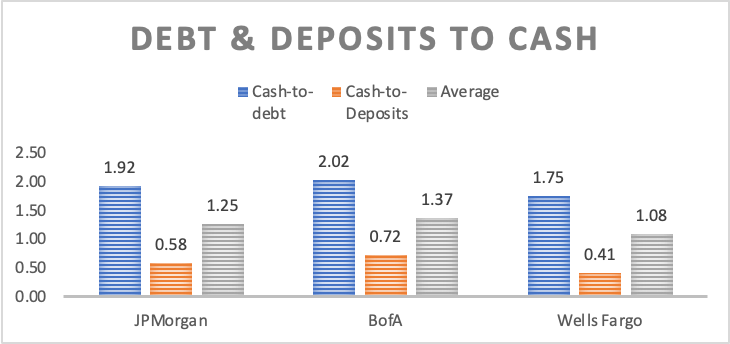

Of the massive three banks, JPMorgan is the second most stable since its whole money reserves can cowl round 58% of deposits and 1.92 occasions its whole debt. Nonetheless, Financial institution of America Company (BAC) can cowl 72% of deposits with its money reserves and a pair of.02 occasions its whole debt. For that purpose, BofA scores higher than JPMorgan.

Writer’s Calculations

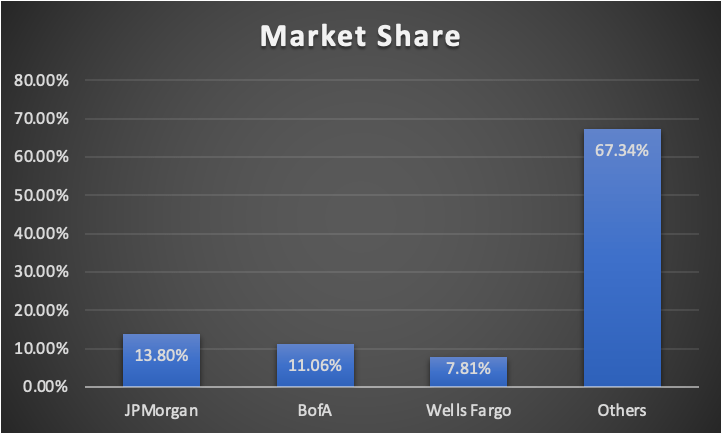

If we divided the whole deposits of every of those banks by the whole quantity of deposits within the US banking system (which is around $17.4 trillion) we will deduct that JPMorgan’s market share is round 13.80% which is barely larger than BofA’s 11.06%. Wells Fargo is available in third by holding round 7.81% of deposits. Nonetheless, this means that the three banking giants have (in concept) a number of room to develop.

Writer’s Calculations

Business outlook

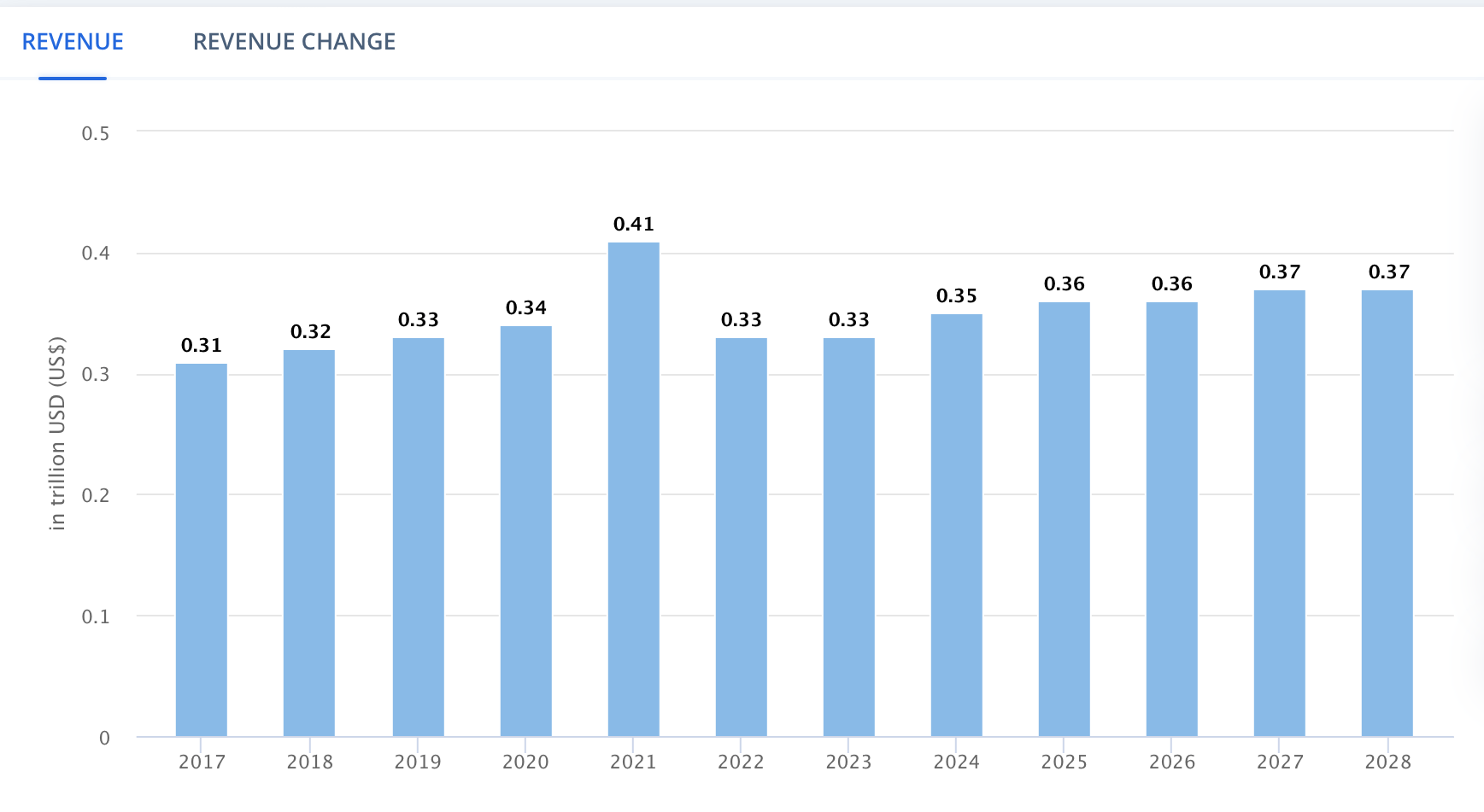

The US Traditional Banking Market, which incorporates retail banking and business banking, is anticipated to develop at a 1.44% annual tempo all through 2028. In the meantime, the global investment banking income is anticipated to develop at a CAGR of 1.4% all through the identical interval. In these two markets, the addressable market (by way of income) stands at $1.03T.

Statista Statista

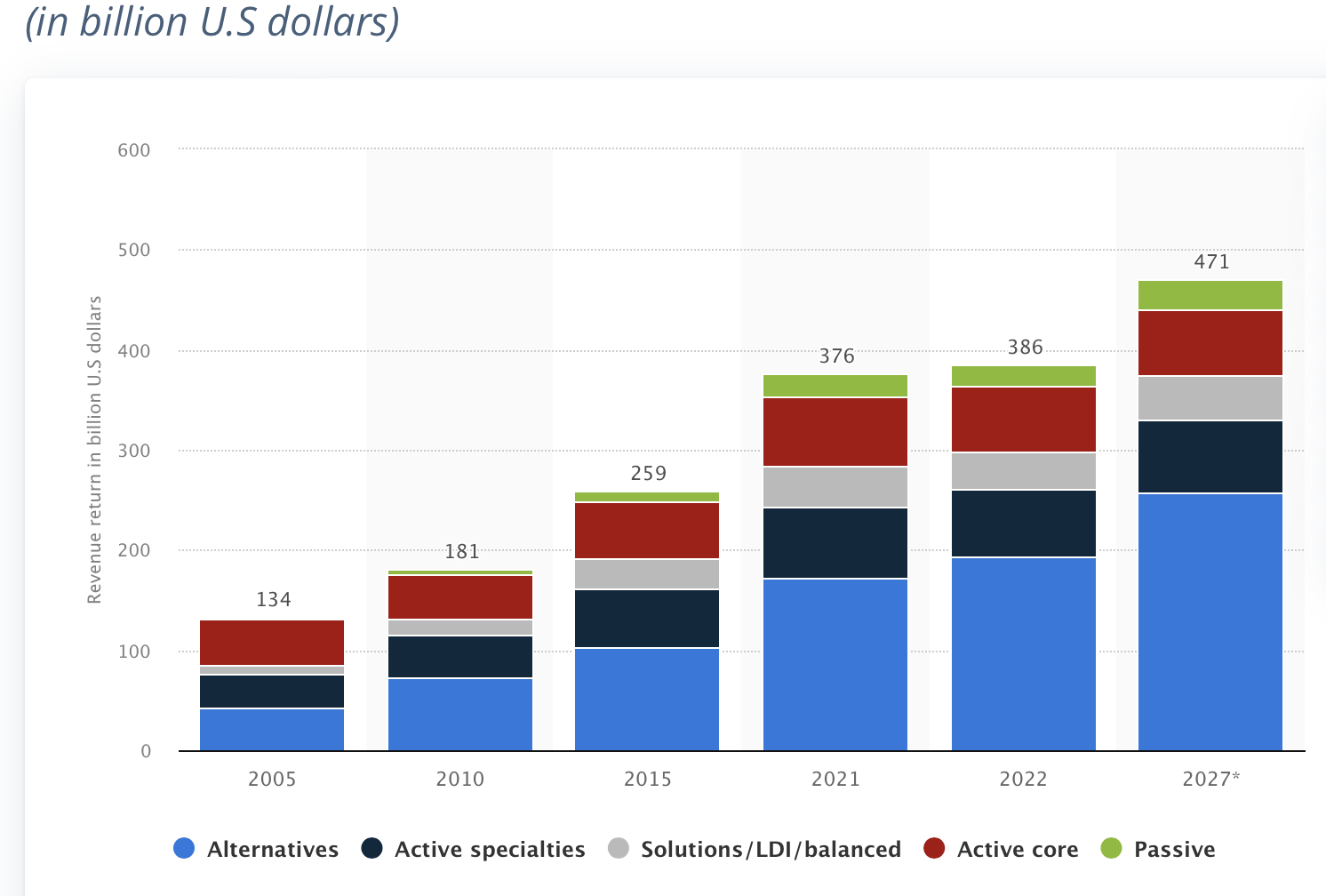

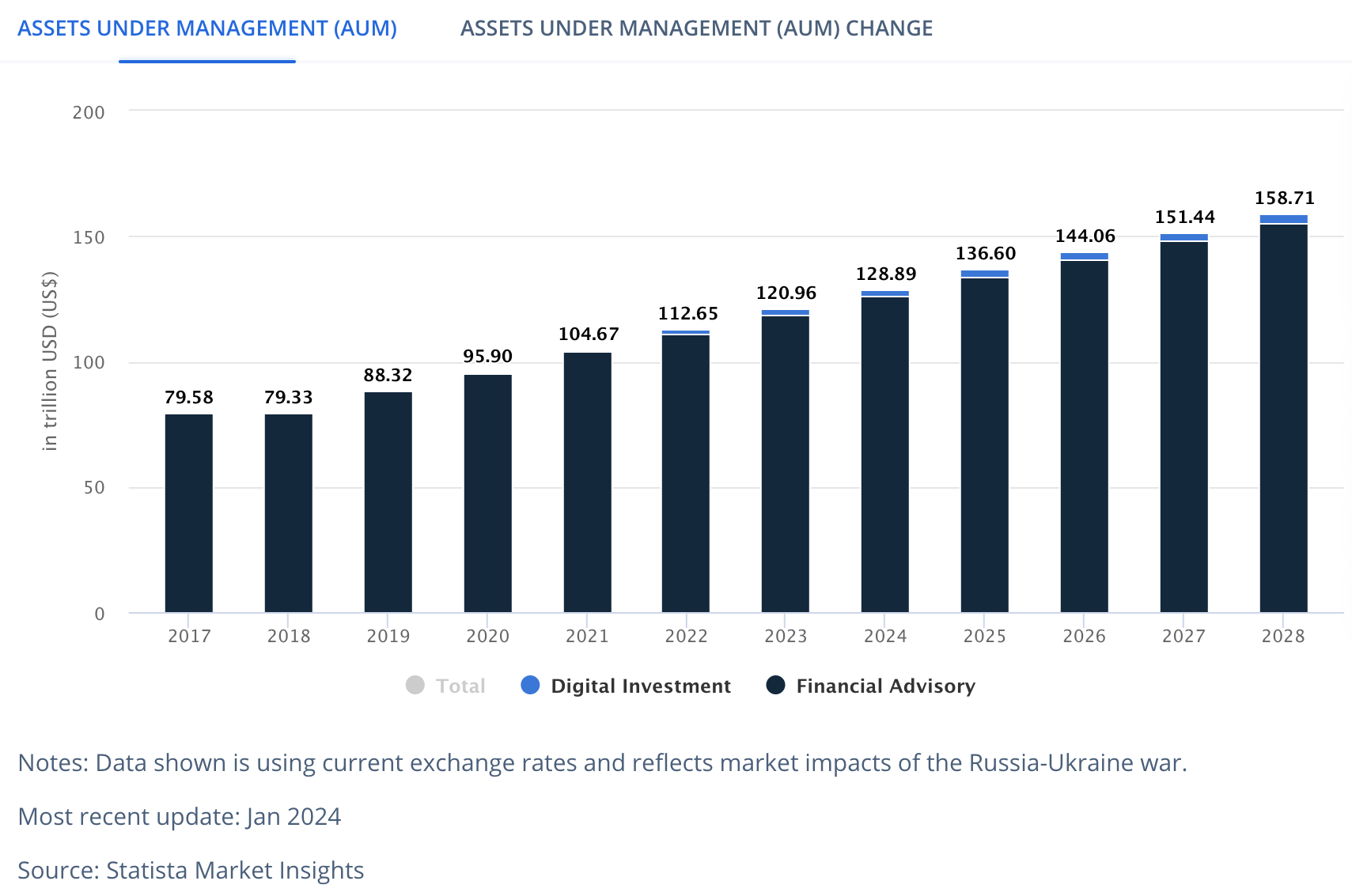

Lastly, Worldwide Asset Management and Wealth Management are anticipated to develop sooner, at a 4.40% and 5.90% annual tempo respectively. The addressable market of asset administration stands at $402.98B and within the case of wealth administration, the addressable market is $120.96T in belongings.

Statista Statista

Summing all of this up, we will deduct that JPM has an addressable market (by way of income) of round $1.43T comprising Conventional & Funding banking, and Asset Administration, and an addressable market (By way of AUM) of 120.96T in belongings in wealth administration. The addressable marketplace for 2028 is anticipated to achieve $1.56T (in income) for the primary three segments and $158.71T (in AUM) for wealth administration.

Valuation

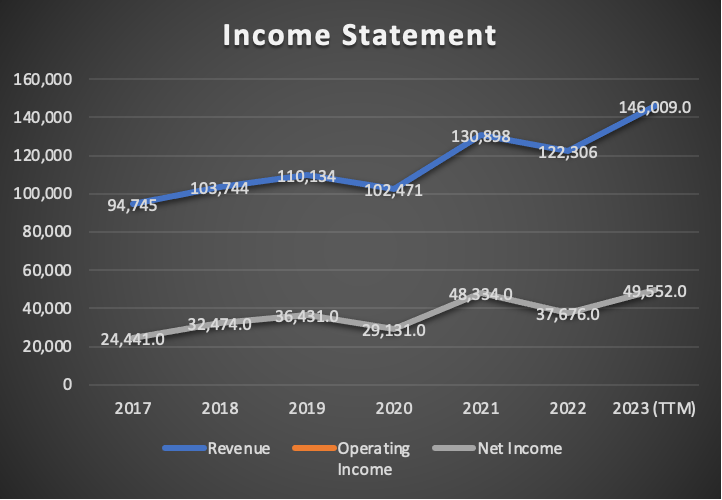

On this article, I’ll worth JPMorgan Chase utilizing a Residual Earnings Mannequin. Within the desk under you’ll be able to see all the present monetary knowledge as of This autumn 2023 that’s essential to proceed with the mannequin. Moreover, the low cost fee within the mannequin might be calculated by way of a easy CAPM mannequin.

| Desk Of Assumptions | |

| (Present knowledge) | |

| Fairness Worth | 566,340.00 |

| Debt Worth | 731,372.00 |

| Value of Debt | 2.16% |

| Tax Price | 24.34% |

| 10y Treasury | 4.222% |

| Beta | 1.10 |

| Market Return | 10.50% |

| Value of Fairness | 11.13% |

| Web Revenue | 49,552.00 |

| Curiosity | 15,803.00 |

| Tax | 12,060.00 |

| D&A | 7,512.00 |

| EBITDA | 84,927.00 |

| D&A Margin | 5.14% |

| Curiosity Expense Margin | 10.82% |

| Income | 146,009.0 |

| CAPM | |

| Threat-Free Price | 4.222% |

| Beta | 1.1 |

| Market Threat Premium | 6.228% |

| Required Price of Return | 11.073% |

Step one is to fill within the variables of working belongings, and e-book worth after which mission them all through the years. Beginning with working belongings, I’ll subtract money reserves and deposits from whole belongings. The rationale for that is that the belongings that generate money are the e-book of loans, and deposits are the working legal responsibility. The whole working belongings got here out at $70.83B. In the meantime, e-book worth stands at $327.87B. When put towards income, this yields margins of 57.92% and 224.56% which might be used to estimate these two figures all through the projection.

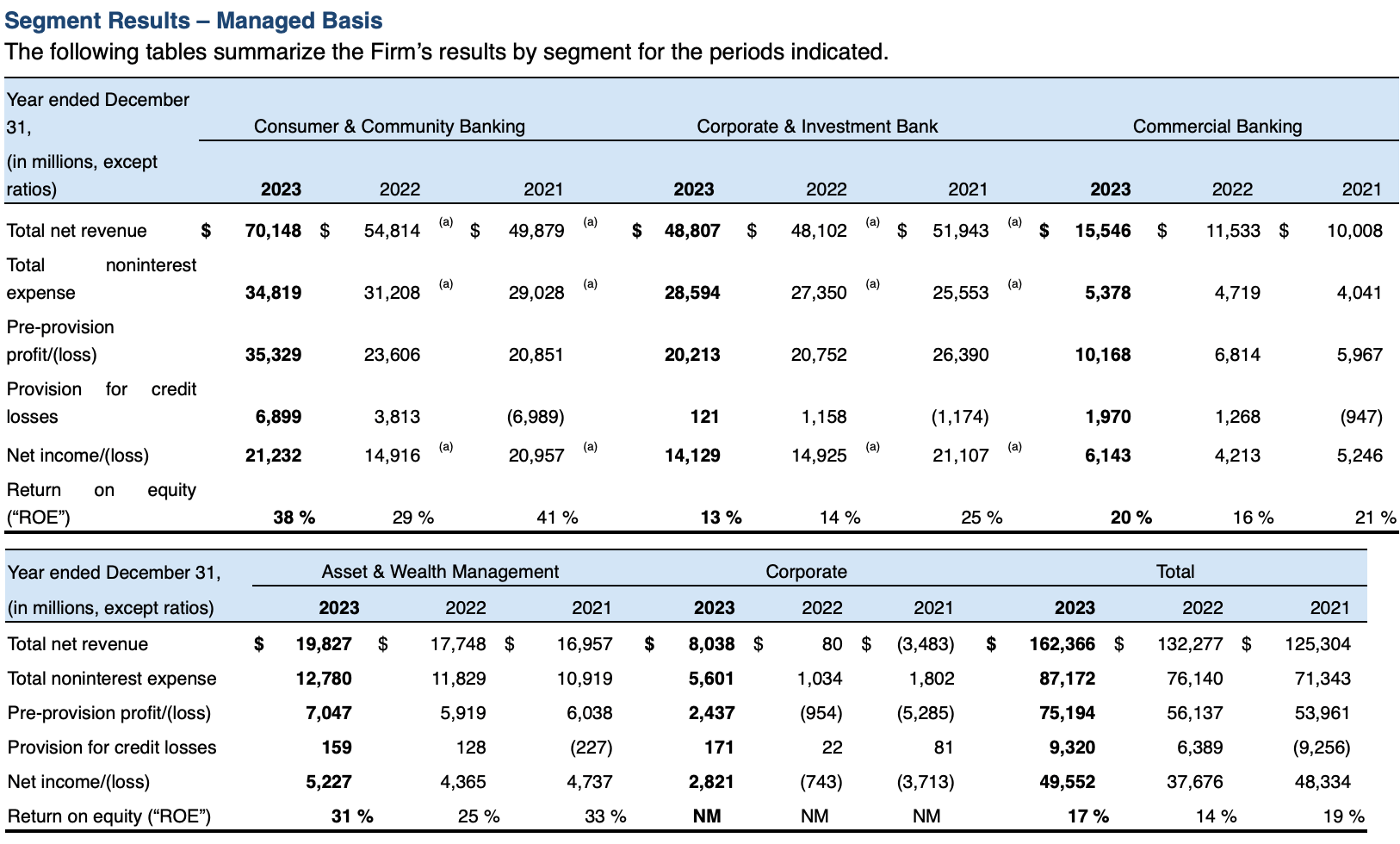

The second step is deducting how a lot every of these 500 new branches will add to income. The very first thing to notice is that these branches are strictly for shopper & group and business banking. JPMorgan shouldn’t be going to open wealth administration workplaces in a rural space, as a result of the overwhelming majority of the cash is in large cities. Due to this fact, I’ll divide the 2023 Shopper & Neighborhood banking income of $70.14B and the business banking income of $15.54B by the 4,700 estimated branches JPMorgan Chase has. This division yields a results of $14.92M and $3.30M per department respectively. Then, past 2027, the Shopper & Neighborhood, and business banking segments will develop on the estimated market fee of 1.44%.

Chase

Subsequently, the opposite segments regarding Company & Funding Financial institution and Asset & Wealth Administration will develop on the tempo of the general market, 1.40% and 5.15% respectively. The rationale for it’s because the income generated in these segments is reliant on how good JPMorgan manages belongings (within the case of wealth administration) and the way handy would JPMorgan be (within the case of funding banking).

JPMorgan This autumn 2023

Subsequent, I have to calculate internet earnings. I’ll do it by means of internet earnings margins. This may even not directly result in attempting and predict future rates of interest by the FED. For the 12 months 2024, I count on that the FED undergo with its fee cuts, which might decrease JPM’s profitability and income as a result of purchasers can pay much less curiosity. The web earnings margin right here is 29.29% as a result of in 2019-2020 the web earnings margin was decreased by 4.65% and handed from 33.08% to twenty-eight.43%.

For the 12 months 2025, I count on that decrease rates of interest will result in elevated consumption of loans which ought to cowl the decreased curiosity earnings JPM will obtain as a consequence of decreased rates of interest. The web earnings margin right here might be 33.94%, recovering the lack of 4.65%.

Subsequent, I’ll put a 31.47% internet earnings margin for 2026, which is according to the 2017-2023 TTM.

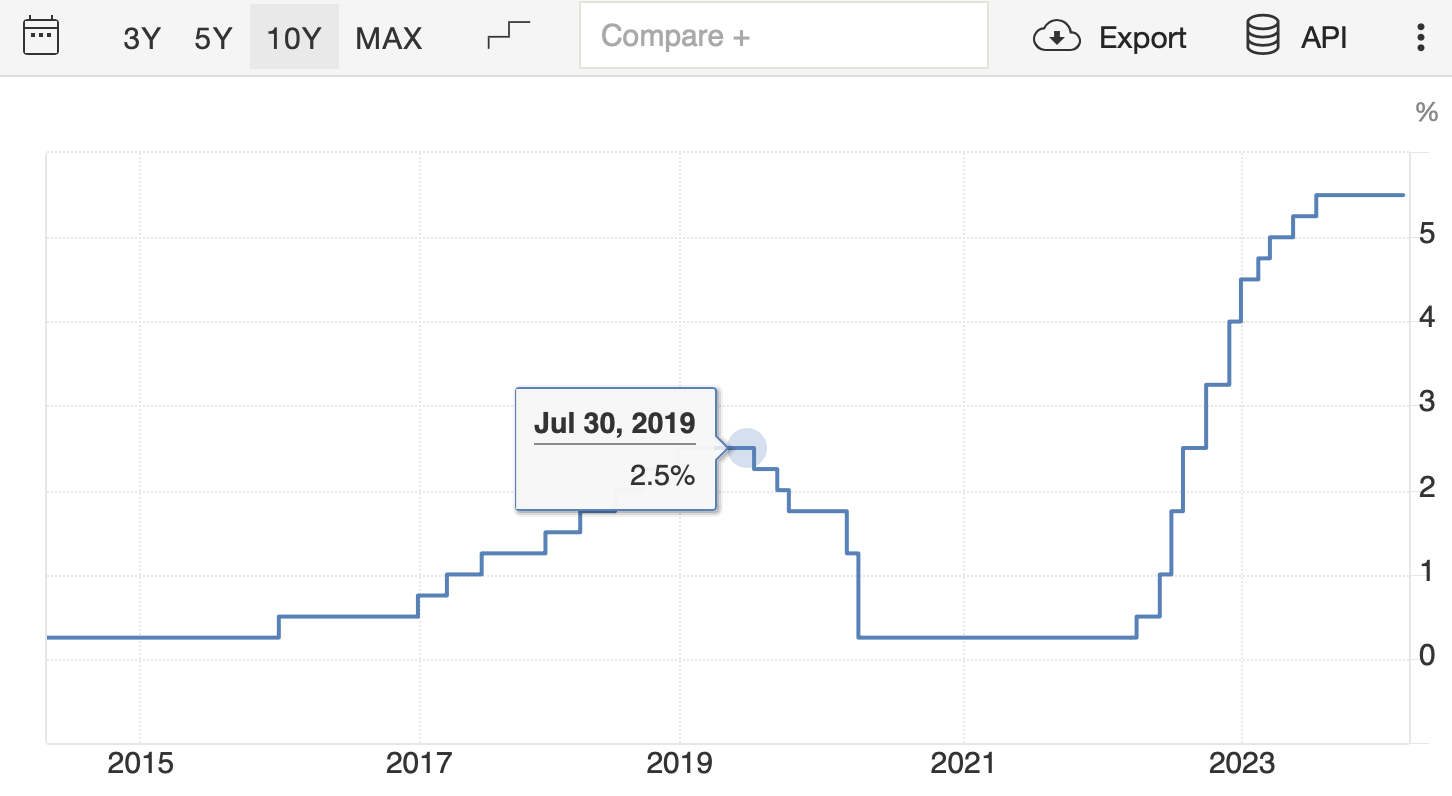

Nonetheless, now comes the true problem, when is the FED going to hike rates of interest once more? Nicely, I’ll suggest that the FED goes to hike charges by not that a lot in 2027, most likely 2.25% (one thing near what happened in 2019). The web earnings margin for this 12 months might be 36.12%, up 4.65% as JPM’s income and profitability improve as a result of larger rates of interest.

Buying and selling Economics

Moreover, due to this, I may even make income tumble by 7.27% in 2027 as a result of that is the approximate change fee in JPM’s income in 2019-2020 when the FED lowered rates of interest in 2019-2020 and when the FED elevated rates of interest in 2021-2022.

Writer’s Calculations

Then for 2028, the web earnings margin will fall to 31.47% as a result of slower consumption outpacing larger rate of interest advantages. So for 2028, the Fed ought to scale back this hypothetical 2.25% rate of interest.

Lastly, in 2029, the web earnings margin will improve to 33.94% as decrease rates of interest improve consumption and demand for JPM loans improve.

| Shopper & Neighborhood Banking | Company & Funding Financial institution | Business Banking | Asset & Wealth Administration | Company | Complete | |

| 2023 | 70,148.0 | 48,807.0 | 15,546.0 | 19,827.0 | 8,033.0 | 162,361.0 |

| 2024 | 72,013.0 | 49,490.3 | 15,959.4 | 20,848.1 | 2,277.0 | 160,587.8 |

| 2025 | 73,878.0 | 50,183.2 | 16,372.8 | 21,921.8 | 2,277.0 | 164,632.7 |

| 2026 | 75,743.0 | 50,885.7 | 16,786.1 | 23,050.7 | 2,277.0 | 168,742.6 |

| 2027 | 72,101.5 | 47,186.3 | 15,979.1 | 21,374.9 | 2,277.0 | 158,918.9 |

| 2028 | 73,139.7 | 47,846.9 | 16,209.2 | 22,475.8 | 2,277.0 | 161,948.7 |

| 2029 | 74,193.0 | 48,516.8 | 16,442.7 | 23,633.3 | 2,277.0 | 165,062.7 |

| Progress Price % | 1.44% | 1.40% | 1.44% | 5.15% |

Lastly, the mannequin may even yield a future worth for FY2029, which was calculated by taking the undiscounted residual earnings after which dividing them by the whole widespread shares excellent.

Writer’s Calculations

As you’ll be able to see, the mannequin suggests a good worth for JPMorgan of round $237.41 per share, which is a 20.7% upside from the present inventory worth of $196.60. Moreover, for 2029, the mannequin suggests a inventory worth of $407.06 which interprets into an honest 17.8% annual return on prime of the present 2.35% dividend yield.

How do my estimates evaluate with the common consensus?

If I did a mannequin solely based mostly on common analysts’ estimates, I might get a good worth per share of $194.19, which signifies that there’s a 1.2% draw back from the present inventory worth of $196.6. The longer term worth that may be steered by this hypothetical mannequin could be $331.06, which factors in direction of annual returns of 11.4% all through 2029.

Within the graph under you’ll be able to see how each outcomes evaluate with one another. For FY2024, my estimates are round 2.44% larger, so it is achievable. Then the opposite facet you’ll be able to see is that for FY2027, the common consensus signifies that EPS will lower by round 17%, whereas mine factors to five.82%.

Writer’s Calculations

Now, within the desk under it is possible for you to to deduct that the trigger is expounded to internet earnings margins since my income estimates are decrease than these of the common consensus by a big margin.

Writer’s Calculations

| Common Web Revenue Margin Estimates | My Web earnings Margin Estimates % | |

| 2024 | 28.25% | 29.29% |

| 2025 | 28.35% | 33.94% |

| 2026 | 29.81% | 31.47% |

| 2027 | 26.32% | 36.12% |

| 2028 | 25.29% | 31.47% |

| 2029 | 24.30% | 33.94% |

Dangers to Thesis

The primary danger to my thesis is that JPMorgan’s plan to open 500 branches (primarily in rural areas) might go flawed due to the low inhabitants within the areas the place JPMorgan will develop. Nonetheless, it is best to be the primary, as a result of in the event that they obtain that, then different large banks won’t see it as a worthwhile enterprise to enter rural areas.

Moreover, banking is already a progress market which signifies that JPMorgan might probably develop by way of M&As nonetheless since JPMorgan is already too large, regulators will forestall it.

I feel that JPMorgan is healthier off within the banking panorama, because it has a status as a well-managed financial institution, throughout banking panics individuals would rush to place their cash in a safer financial institution, and a type of is JPMorgan.

Conclusion

In conclusion, JPMorgan continues to be a really stable monetary establishment, it could actually cowl round 58% of deposits, which is already glorious since throughout banking panics persons are extra susceptible to maneuver their cash to an enormous financial institution reminiscent of JPM.

The primary dangers embrace that the brand new 500 branches don’t obtain the anticipated efficiency and change into unprofitable. However, because the growth will goal small inhabitants facilities, being the primary there’ll assist make it unprofitable for rivals to enter the realm.

The inventory stays, in line with my estimates, very undervalued, by round 20.7%, which means that the truthful worth per share stands at 237.41. Moreover, the long run worth steered by my mannequin is round $407.06 which means 17.8% annual returns all through 2029. For these causes, I keep my “strong-buy” score on JPM.