ligora/iStock through Getty Photographs

Introduction

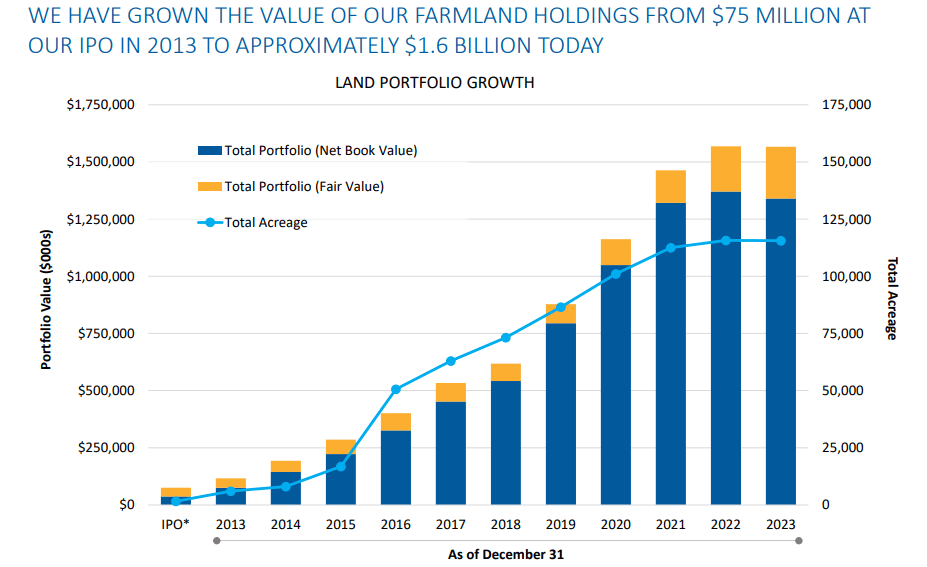

As defined in a previous article, the enterprise mannequin of Gladstone Land (NASDAQ:LAND) may be very simple: the REIT owns farmland and leases it to farmers. It’s not uncovered to profitable or disappointing harvests aside from the impression it has on the tenants. On the finish of 2023, Gladstone Land owned virtually 112,000 acres throughout 168 farms in 15 states. I’m nonetheless very within the REIT’s most well-liked shares and I’m significantly intrigued by the worth proposition of LANDM because the securities both get known as by the tip of January 2026, or the popular dividend yield jumps to in extra of 8%.

The REIT stays FFO optimistic

I’m clearly primarily within the REIT’s capacity to generate a positive FFO and AFFO. Not as a result of I’m eager on going lengthy the frequent shares however primarily as a result of I need to make certain the popular dividends are nonetheless well-covered.

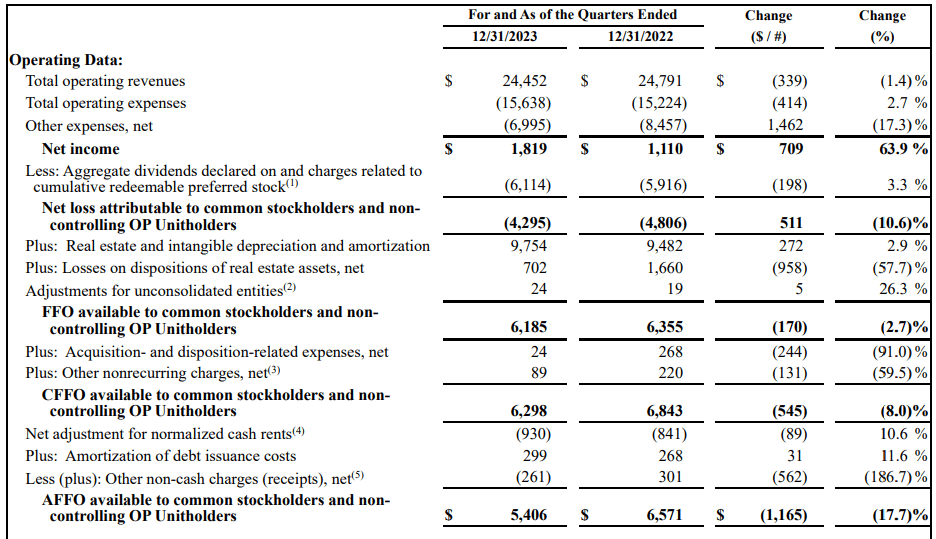

Trying on the This autumn outcomes beneath, you’ll be able to see there was a internet lack of $4.3M leading to a $6.2M FFO after including again the depreciation costs and the loss on the sale of belongings. The AFFO for the ultimate quarter of the yr was $5.4M which, primarily based on the share depend of 35.8M shares through the quarter, represented an AFFO of $0.15 per share. That was adequate to cowl the distributions of $0.139 per share.

Gladstone Land Investor Relations

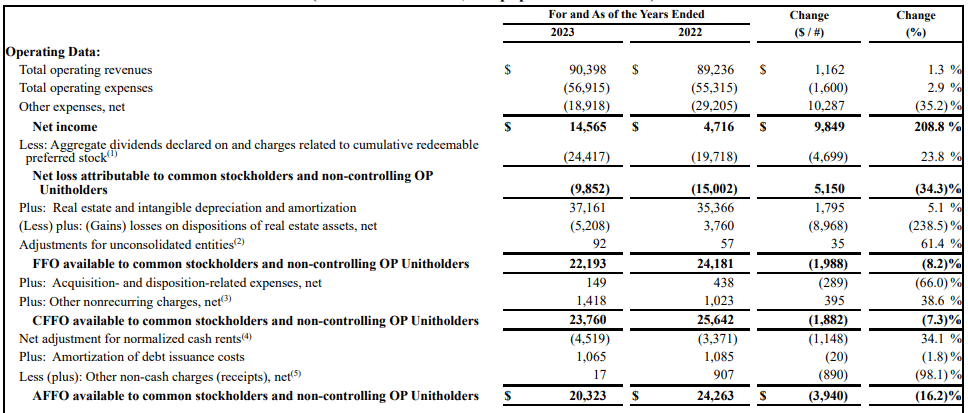

Trying on the full-year outcomes beneath, you see the AFFO got here in at $20.3M for a results of slightly below $0.57 per share. Whereas this implies the distributions of $0.554 per share had been nonetheless lined, the payout ratio elevated to a comparatively uncomfortably excessive 97%.

Gladstone Land Investor Relations

That truly is a reasonably weak efficiency contemplating Gladstone Land paid a decrease curiosity expense in comparison with the earlier yr. Whereas that’s actually robust for the frequent unitholders, I’m primarily trying on the outcomes from the angle of a most well-liked shareholder. And though the protection ratio of the popular dividends decreased, the REIT nonetheless generated roughly $45M in AFFO earlier than most well-liked dividends and the virtually $25M in most well-liked dividends represented a payout ratio of roughly 55%. That’s a bit on the excessive facet in comparison with what I like (I typically favor to see payout ratios beneath 20%) however I like Gladstone Land’s substantial land financial institution which actually gives a superb asset protection ratio.

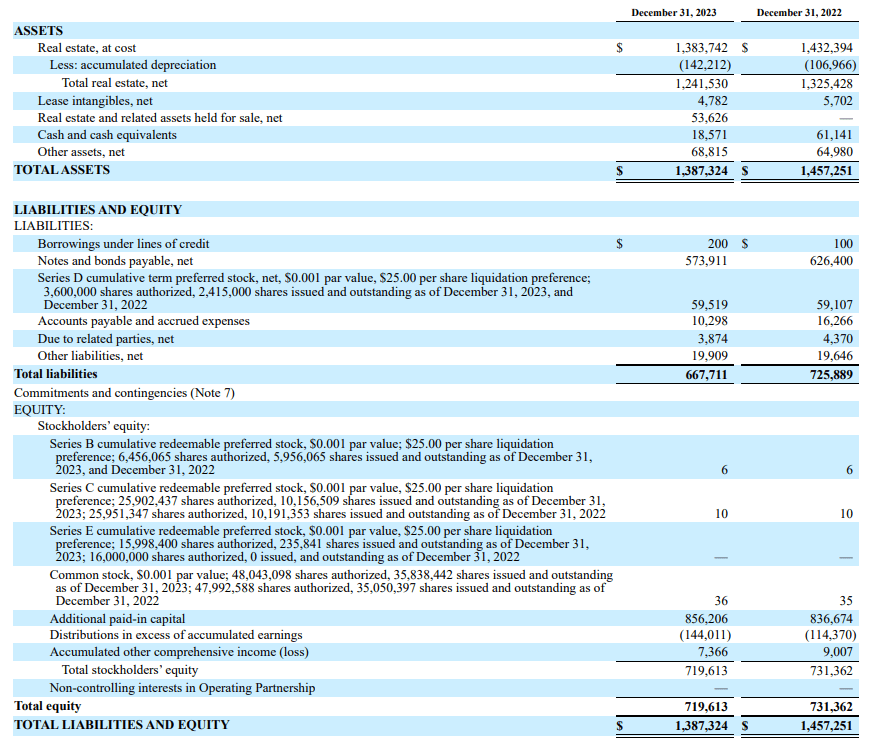

As you’ll be able to see beneath, The balance sheet contains $1.39B in assets, backed by $720M in fairness. Of that $720M, about $410M is represented by most well-liked fairness as there are roughly 16.35 million most well-liked shares excellent. It’s vital to see the Sequence D most well-liked shares (which I’ll talk about in additional element later) are listed as a legal responsibility on the stability sheet as a result of obligatory name date.

Gladstone Land Investor Relations

Within the worst case situation, if Gladstone Land elects to not name these most well-liked shares, they may transfer again to the fairness stack, leading to a complete fairness of roughly $780M of which roughly $470M is represented by most well-liked fairness.

This certainly means the cushion of $310M (complete fairness minus most well-liked fairness) is comparatively skinny however there’s greater than meets the attention right here. Though most REITs need to cope with the distinction between guide worth and truthful worth of their belongings, only a few really trouble to publish the truthful worth of the belongings. In keeping with Gladstone, the truthful worth of its farmland is roughly $1.6B which is a number of a whole bunch of tens of millions of {dollars} larger than the guide worth. That sounds practical, and subsequent to the tip of 2023, the REIT sold a farm for $66M. It initially acquired the farm for $54M seven years in the past and the appraisal worth was simply $64M.

Gladstone Land Investor Relations

This implies the security internet for the asset protection ratio is probably going considerably larger than $310M and doubtlessly even twice that, which makes the asset protection ratio of the popular shares acceptable.

I just like the time period most well-liked shares for short-term fastened earnings

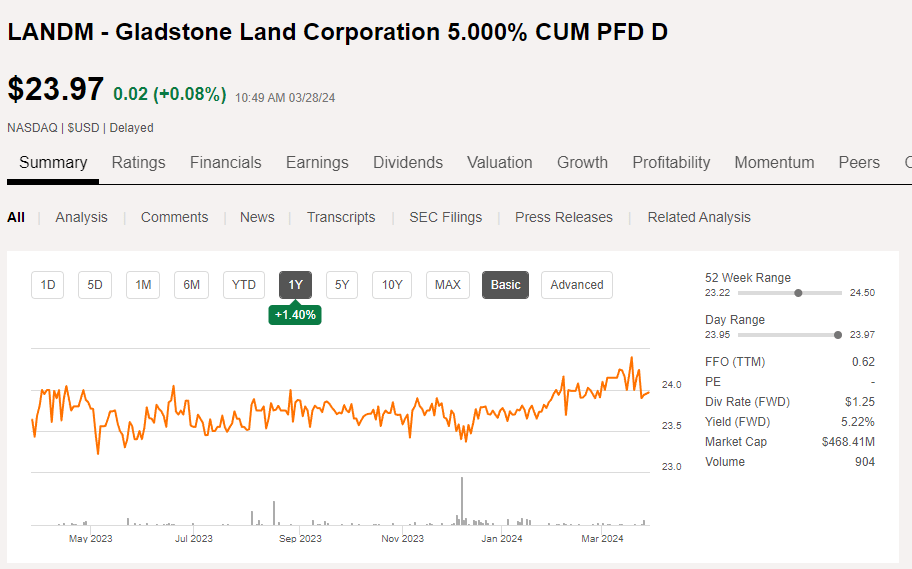

In my article final yr, I primarily centered on the Sequence D most well-liked shares that had been issued by Gladstone Land. These securities are buying and selling with (NASDAQ:LANDM) as ticker image and provide a most well-liked dividend of $1.25 per yr, payable in twelve equal month-to-month tranches. And whereas these most well-liked shares need to be redeemed by Gladstone Land by the tip of January 2026, ought to Gladstone Land fail to name these most well-liked shares, the popular dividend will enhance to $2/share per yr.

Looking for Alpha

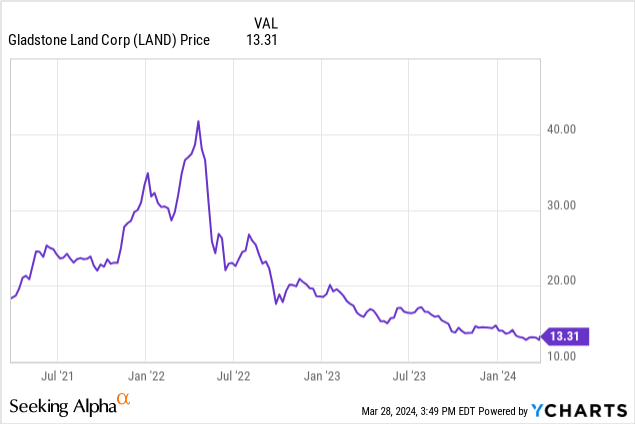

This implies there are two attainable methods to take a look at LANDM. The primary one is by assuming the securities will certainly be redeemed in January 2026, wherein case there can be a capital acquire of roughly 4.3% primarily based on the present share worth of $23.97. The yield to obligatory name is roughly 7.4% which I feel is fairly enticing for a short-term safety.

Nonetheless, the caveat certainly is the danger of Gladstone preferring to pay an 8% coupon somewhat than calling the securities. In that case, the annual most well-liked dividend of $2 would symbolize a yield of simply over 8.3% which is also a greater than acceptable compensation.

Funding thesis

Though I like farmland, I’ve no place in and no intention to provoke an extended place in Gladstone Land. I did write some put choices with a strike worth of $12.50 expiring in April & Might however I hope to not get any inventory assigned and will shut these positions forward of the expiration date.

I presently have a small lengthy place within the Sequence D most well-liked shares (LANDM) and can possible add to this place. Whereas the disappointing outcomes of Gladstone Land are primarily hurting the frequent shareholders, the popular dividends are nicely lined whereas there’s loads of junior fairness ranked junior to the popular fairness. I just like the trade-off between both getting a 7.4% annualized return over 22 months, or the popular dividend yield elevated to roughly 8.3-8.4%. I might be tremendous with each outcomes.