farakos

Introduction

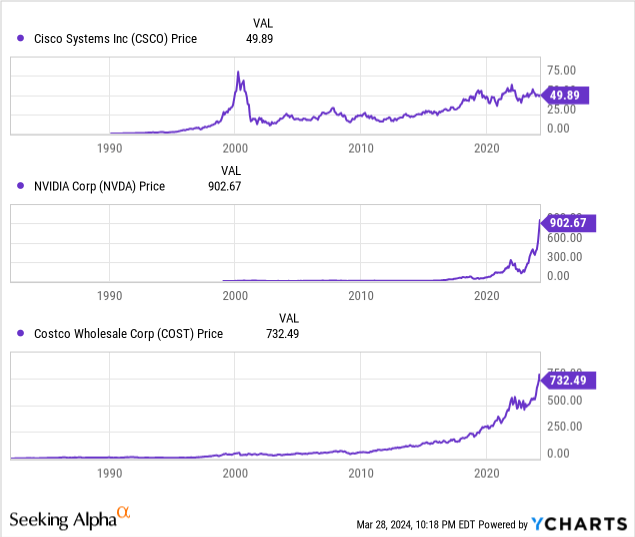

Amid parabolic inventory strikes within the know-how sector, the murmurs of an AI bubble are rising louder and louder; nonetheless, nosebleed inventory valuations are usually not restricted to the Nvidias of the world. Costco Wholesale Company (NASDAQ:COST), a mature retail large, is up ~50% during the last 12 months, constructing on high of a parabolic rally in its inventory through the liquidity bubble of 2020-21.

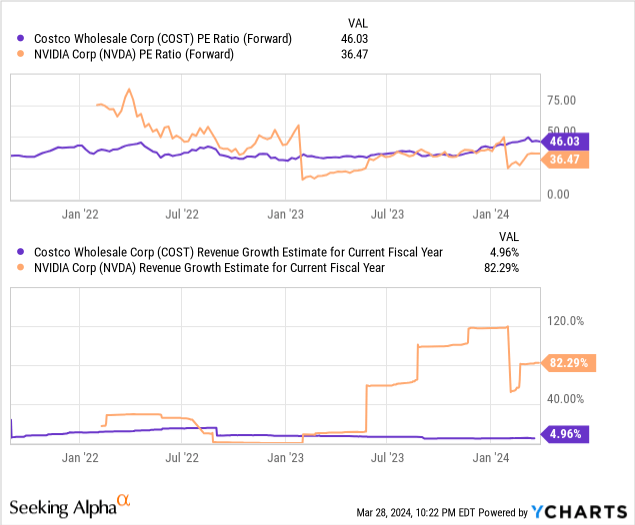

Primarily based on worth motion, Nvidia [of 2023-24] and Cisco [of 2000] look eerily related. That mentioned, for my part, Costco’s parabolic ascent is even scarier. Regardless of rising its high line at a mid-single-digit charge, Costco presently boasts an exorbitant ahead P/E a number of of ~46x. To place this valuation in perspective, Nvidia trades at a ahead P/E a number of of ~36x and is rising manner, manner sooner than Costco.

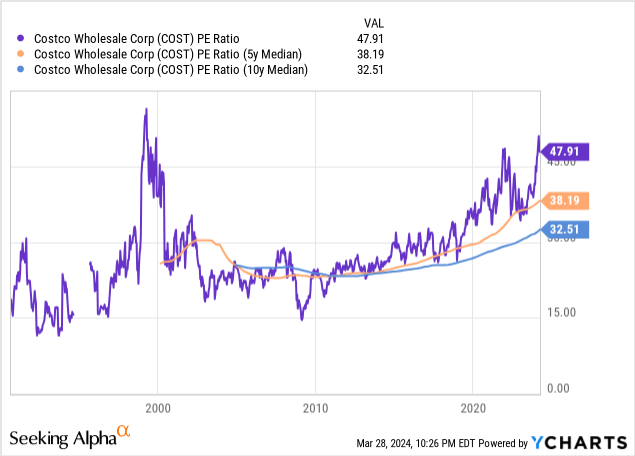

Alright, evaluating Costco to Nvidia might be unfair, however evaluating Costco to itself is truthful recreation! As you’ll be able to see under, Costco is buying and selling nicely above its historic median P/E ratios, and we’re getting fairly near the 1999 peak valuation for COST inventory.

Whereas we might or will not be in a synthetic intelligence bubble, Costco actually seems to be bubblicious. Let’s carry out a reverse DCF evaluation on COST inventory to see what Mr. Market is presently pricing into the retail large!

Reverse DCF Train For Costco Inventory

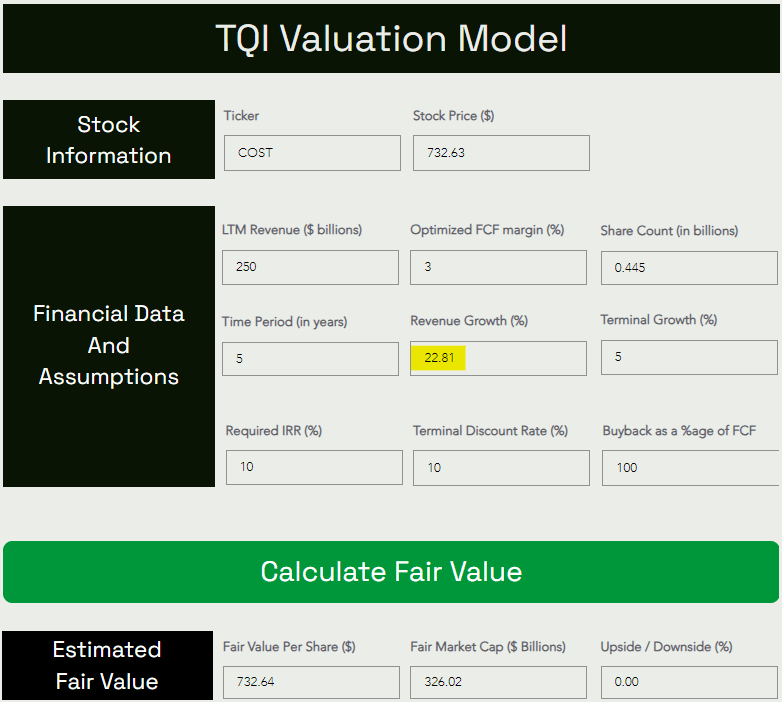

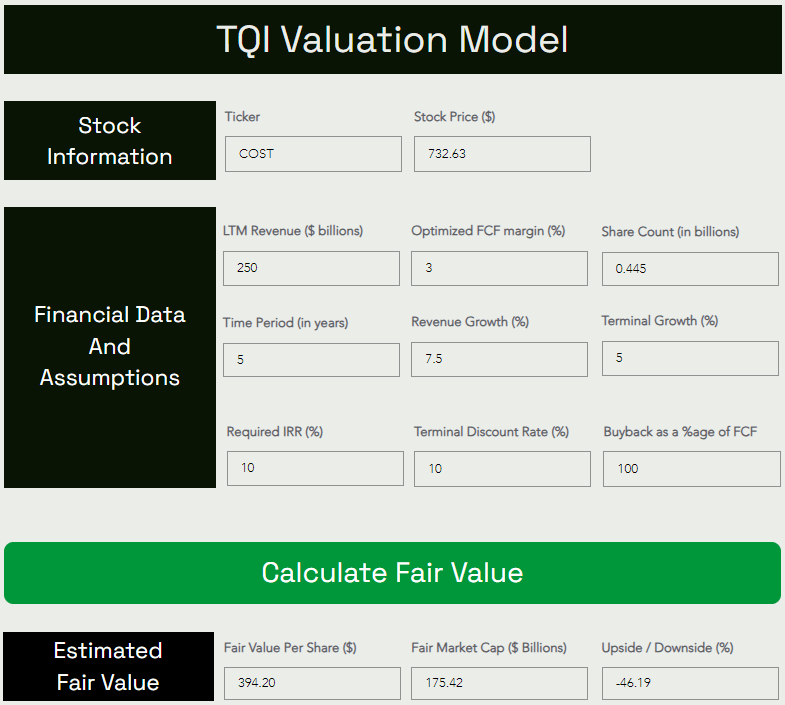

For this reverse DCF train, we have now used a 5-year modeling interval and beneficiant assumptions for steady-state free money stream margin [+3%] and terminal development charge [+5%]. Whereas these mannequin assumptions are fairly simple, please be happy to share your ideas or issues within the feedback part under.

TQI Valuation Mannequin (TQIG.org)

Primarily based on its present inventory worth of ~$732 per share, Mr. Market is presently pricing in a 5-year CAGR income development charge of ~23% into Costco’s inventory!

Does The Implied Progress Make Sense?

Given Costco’s mid-single-digit development charges, the market pricing in ~5x sooner development into COST inventory for the subsequent 5 years is solely ridiculous. Sure, Costco is a serial development compounder; nonetheless, such pricing is a tell-tale signal of irrational exuberance within the inventory market.

SeekingAlpha

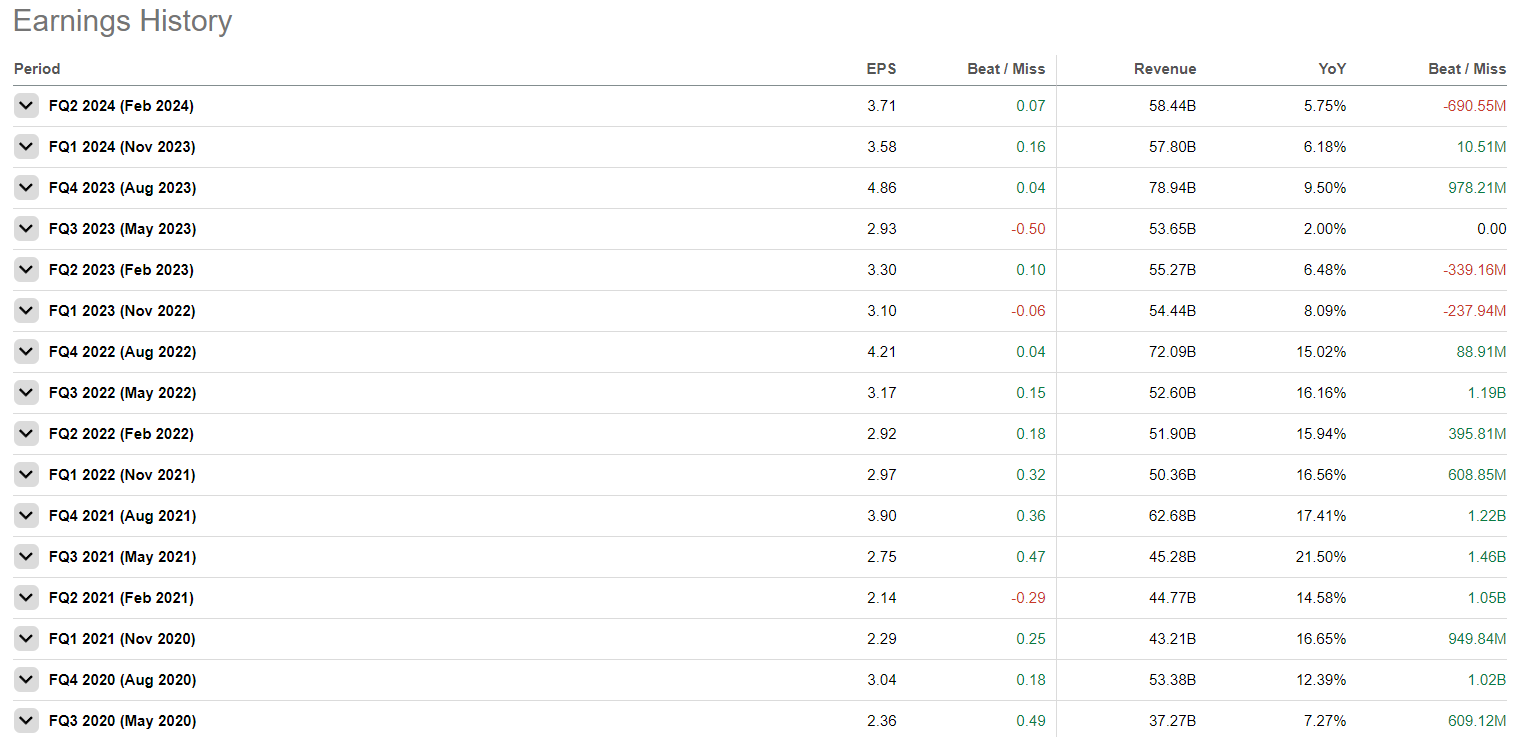

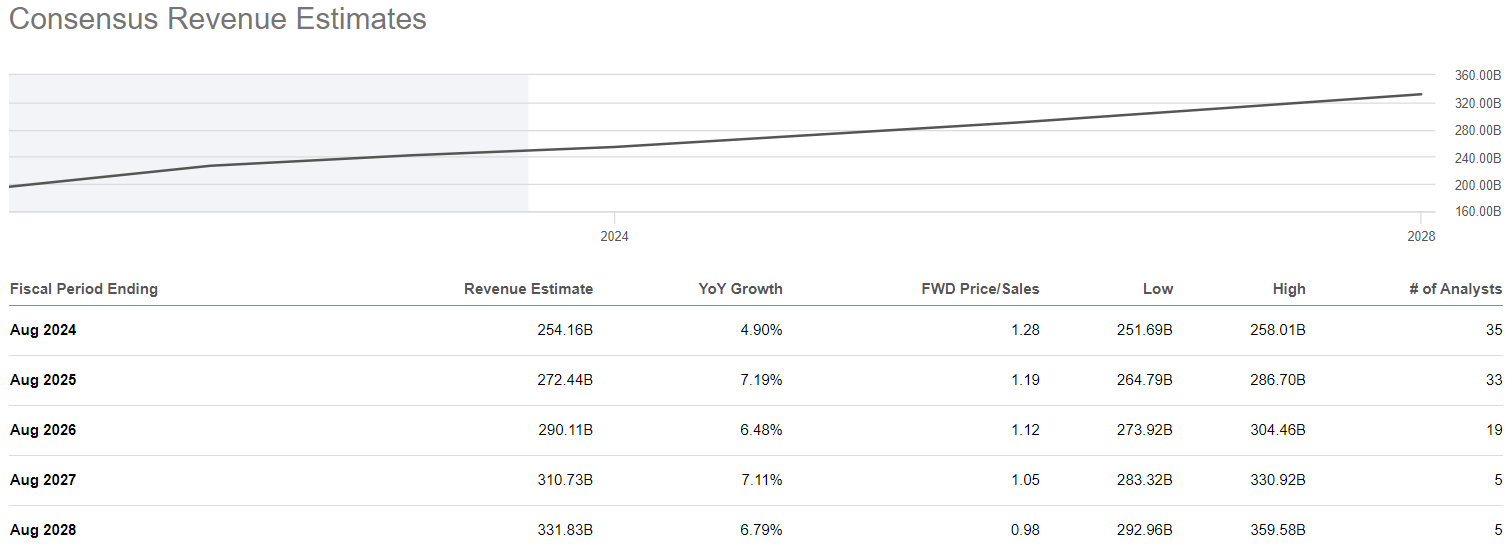

After recording wholesome double-digit top-line development through the inflationary wave in 2020-22, Costco has seen its development charges gradual again all the way down to mid-single digits over latest quarters. And, in line with consensus road estimates, Costco is projected to compound gross sales development at 6-7% per 12 months for the subsequent 5 years.

SeekingAlpha

In QQQ: Prepare for Turbulence, I highlighted the position of considerable liquidity within the ongoing meltdown in monetary markets. If liquidity dries up, Costco’s inventory may wrestle large time, as investor expectations constructed into the inventory are fully out of contact with enterprise actuality. Costco is a mature (slow-growing) retailer priced for hypergrowth.

Allow us to now have a look at a extra cheap valuation for Costco:

Costco Truthful Worth And Anticipated Return

Contemplating Costco’s footprint growth plans of 25-30 golf equipment per 12 months and comparable retailer gross sales development of 3-5% per 12 months, I consider Costco can ship 6-9% CAGR gross sales development over the subsequent 5 years. Whereas our development assumption is barely larger than road estimates, I feel a 7.5% CAGR gross sales development assumption is cheap.

TQI Valuation Mannequin (TQIG.org)

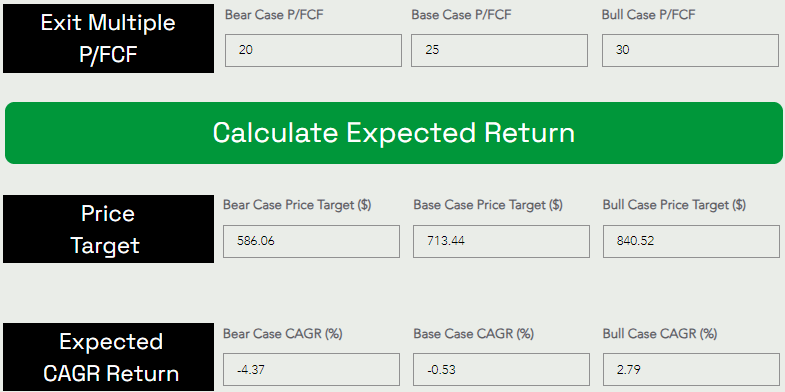

As you’ll be able to see above, Costco’s truthful worth is ~$394 per share, which suggests a draw back of roughly 46% from present ranges. Assuming a considerably beneficiant P/FCF exit a number of of ~25x, we get to a 5-year worth goal of ~$713 per share, which suggests a CAGR return of -0.53%.

TQI Valuation Mannequin (TQIG.org)

At present ranges, Costco inventory appears like lifeless cash for the subsequent 5 years. With COST’s base case anticipated CAGR falling nicely wanting my funding hurdle charge (of 15% per 12 months) and long-term market (SPY) returns (of 8%-10% per 12 months), I charge COST inventory a “Sell” at $732.63 per share.

With animal spirits operating wild within the inventory market, making a “Sell” name on a successful inventory like Costco is tough. Nevertheless, the unbelievable rally in COST has rendered the inventory lifeless cash for the subsequent 5 years. Bear in mind, no person ever misplaced cash taking a revenue!

Key Takeaway: I charge Costco a “Sell” within the mid-$700s.

Thanks for studying, and blissful investing! Please share any questions, ideas, and/or issues within the feedback part under or DM me.