TBE

What does typically come to your thoughts first, when individuals point out luxurious items?

I’d anticipate individuals to consider seaside entrance villas, yachts, sport vehicles, however definitely vogue, watches and costly cosmetics make the highest of the listing.

Moët Hennessy Louis Vuitton (OTCPK:LVMHF), Hermès Worldwide S.A. (OTCPK:HESAY) and Estée Lauder Firms (EL) are all corporations which typically characterize the posh phase, however not all of those corporations are created equal.

Not solely LVMH is certainly one of my largest funding positions, however it’s been my common go-to inventory during the last decade throughout market pullbacks, because of its heritage model portfolio, loyalty of shoppers because of their items unreplaceable exclusivity and being 48% owned by Arnault household with a major “skin in the game”.

The corporate has change into epitome of luxurious with €418 billion market cap, putting it as 2nd most helpful firm in Europe.

Though the corporate has been buying and selling at low-cost valuation couple months in the past when I’ve last covered the corporate, within the face of overblown fears of slowing gross sales within the luxurious phase. Since then the inventory skilled a exceptional restoration, which pushed the valuation into the other way, a stretched valuation.

Whereas I’m definitely not promoting any of my shares, sitting on a double-digit features, let me present you why I counsel warning, regardless of the corporate being the most effective companies to personal.

Enterprise Replace

Once I converse with fellow buyers, one of the frequent arguments I hear is that investing in discretionary companies is a “fool’s errand” because the enterprise tends to be very cyclical, pushed by the state of the underlying financial system and disposable earnings of customers.

In principle this is sensible, the very first thing that customers typically lower spending on in periods of financial contraction is discretionary bills corresponding to clothes, vehicles and journey.

The place I are inclined to differ with others, is that for my part, LVMH being a luxurious items conglomerate, specializing in rich customers is considerably extra resilient to the financial swings because of the buyer loyalty, exclusivity and pricing energy, which enabled the corporate to common natural progress of 9.1% during the last 35 years.

LVMH’s goal customers are individuals aged 18 to 54, with a considerable annual earnings of a minimum of $75,000. Whereas the earnings might not appear rather a lot in lots of western international locations, needless to say the corporate’s largest market is Asia.

Regardless of the resilience of its enterprise and earnings, the corporate’s inventory value has witnessed a very good quantity of volatility as of late, falling from it is all-time-high of €905 for its native shares in April 2023, right down to €620 in January 2024 amidst industry-wide fears of slowing gross sales progress.

But once more, LVMH has defied odds and delivered earnings above expectations for full-year 2023 and the inventory swiftly recovered, buying and selling now for over €830. In case you have capitalized on the overblow fears, you’ll be sitting on a 30% achieve in just some months.

One of many the explanation why LVMH retains delivering and rewarding its shareholders year-after-year is as a result of the corporate, which is 48% owned by the Arnault household, has a really shareholder oriented mindset and owns well-recognized and legacy manufacturers corresponding to:

- Louis Vuitton

- Christian Dior

- TAG Heuer

- Veuve Clicquot

- Bvlgari

- Tiffany & Co.

… all which characterize sought-after standing image and exclusivity.

Going ahead, it is affordable to anticipate that the posh items {industry} will witness a point of normalization after couple years of 20%+ natural gross sales progress, which was partially induced by the unfastened financial coverage and extreme financial savings of customers.

The management of LVMH nicely acknowledged this reality as throughout H1 2023 the expansion has been 17%, partially impacted by the loosening of COVID restriction, particularly in Asia. The H2 has already skilled a normalization of progress at about 10%, which is one thing we must be anticipating going ahead.

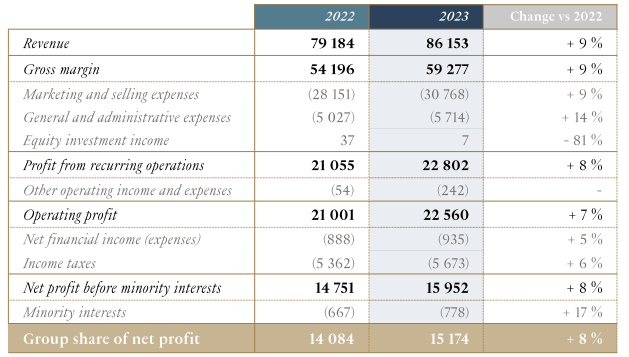

Last year has been successful for LVMH because the gross sales have elevated from €79 billion in 2022 to €86.2 billion. This represents roughly 13% natural progress, nicely above the historic common, nonetheless, the gross sales had been negatively impacted by the FX improvement, dropping to 9% progress on currency-adjusted-basis.

For the full-year the working margin got here in at 26.4% mainly remaining flat YoY. What’s extra vital thought, is that the corporate as soon as once more demonstrated its pricing energy by retaining identical margins, regardless of the Advertising and marketing and Promoting Bills rising 9% on a YoY foundation.

FY23 P&L (LVMH IR)

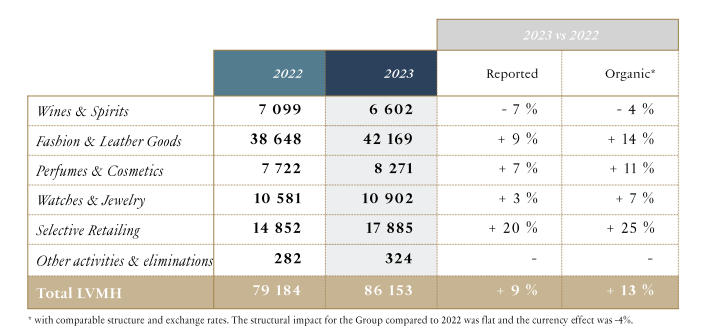

By way of the business breakdown, Vogue & Leather-based Items is by far the biggest phase or “Maison”, representing near 49% of the corporate’s gross sales. It is of utmost significance that this phase retains rising at a double-digit fee, which was nicely demonstrated final yr because the phase achieved 14% progress on an natural foundation.

Different key enterprise segments:

- Selective Retailing: 25% natural progress pushed by robust efficiency of Sephora which nicely exceeded expectations

- Watches & Jewellery: 7% natural progress due to robust dynamics

- Perfumes & Cosmetics: 11% natural progress pushed by glorious outcomes of J’adore fragrance. Sauvage fragrance is probably the most offered fragrance for a 3rd consecutive yr, worldwide.

The sore within the eye of the corporate’s outcomes has been the Wines & Spirits maison, which has been dragging down the efficiency all through the entire 2023. The rationale for the 4% decline is the robust comparability in opposition to earlier yr. But, Champagne gross sales had been up for the yr, whereas Cognac gross sales had been dragging the phase because of weak consumption in US and China.

Section Breakdown (LVMH IR)

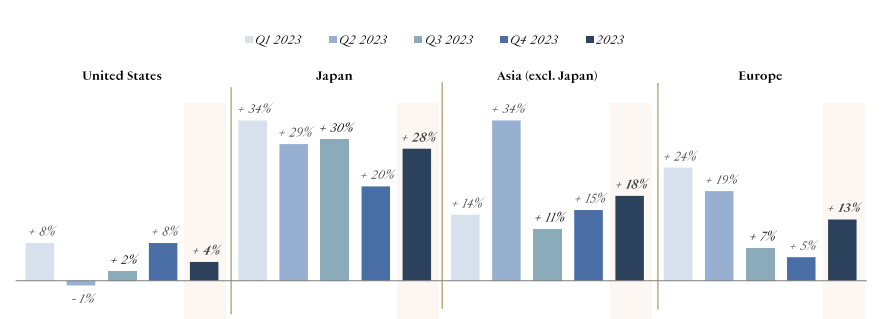

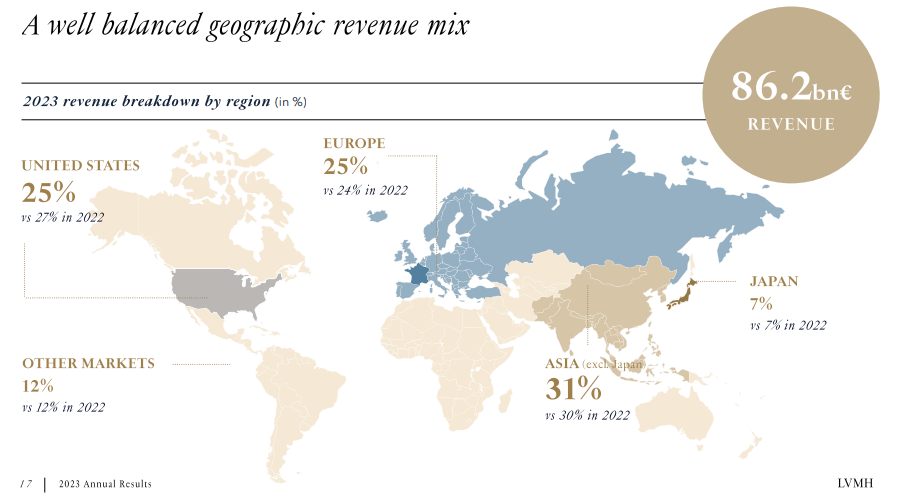

By way of the geographical progress, Japan has remained the quickest rising area throughout the yr, attaining 28%, nonetheless the weakening of Japanese yen in opposition to Euro was one of many components why the corporate was hit by €700 million adverse FX affect.

Asia (excl. Japan), which represents 31% of the corporate’s gross sales and is essential market, began the yr on a difficult footing because of the ongoing COVID restrictions, nonetheless the market nonetheless delivered double-digit progress each in 2023 and 2022, implying energy.

Whereas the scenario stays difficult in US market with gross sales rising solely by 4% YoY, Europe is a unique story, returning to progress of 13%, much like what the corporate has been accustomed to previously, partially due to journey.

Progress by Geography (LVMH IR)

Though LVMH doesn’t present official guidance for the following yr, over the past earnings name, Bernard Arnault, has expressed his confidence to attain round 13% natural gross sales progress in 2024, much like 2023. The expectation is that the deliberate rate of interest cuts might spur spending within the US, making it extra dynamic and returning to excessive single-digit progress.

From a private standpoint, I’m anticipating the corporate will proceed rising their top-line someplace between 10% to 12% which is somewhat “normalized” however sustainable progress going ahead.

Dangers

The potential issues which might hinder LVMH’s efficiency in 2024 are geopolitical tensions, whether or not between China and US over Taiwan or the continued army conflicts in Center East and Jap Europe, over which the corporate has no affect. These conflicts might inflict additional injury to the prosperity of world economies or probably result in transport disruptions as we’re seeing within the Purple Sea.

When investing in LVMH it is key to know that the corporate is actually international with markets like China, US, Europe and Japan all taking part in a serious position within the firm’s success. Whereas the corporate can not affect financial improvement in both of those international locations, its vital to pay attention to the slowing financial system in China, excessive rates of interest in US and Europe that are affect disposable incomes of individuals.

Geographical Dependency (LVMH IR)

Whereas operations throughout completely different economies brings its personal benefits of diversification, one other layer of complexity is the FX affect, which has value the corporate €700 million in 2023 and will additional exert strain on the corporate’s bottom-line progress within the following years.

Valuation

Though I take into account LVMH the epitome of luxurious and high quality alike, we should be aware of the valuation, as shopping for the enterprise at a proper valuation is a key to unlocking market beating returns.

Shopping for even prime quality enterprise as LVMH at elevated valuation would possibly result in years of underperformance and I’d somewhat maintain money in high-yield financial savings account, yielding 5%, somewhat than personal high quality enterprise which is able to virtually definitely underperform.

The final time I lined the corporate, throughout the pull-back induced by the overblown fears of {industry} progress normalization, I’ve rated the corporate as a “Strong Buy” and I’ve loved 20% ROI since, when accounting for the dividend.

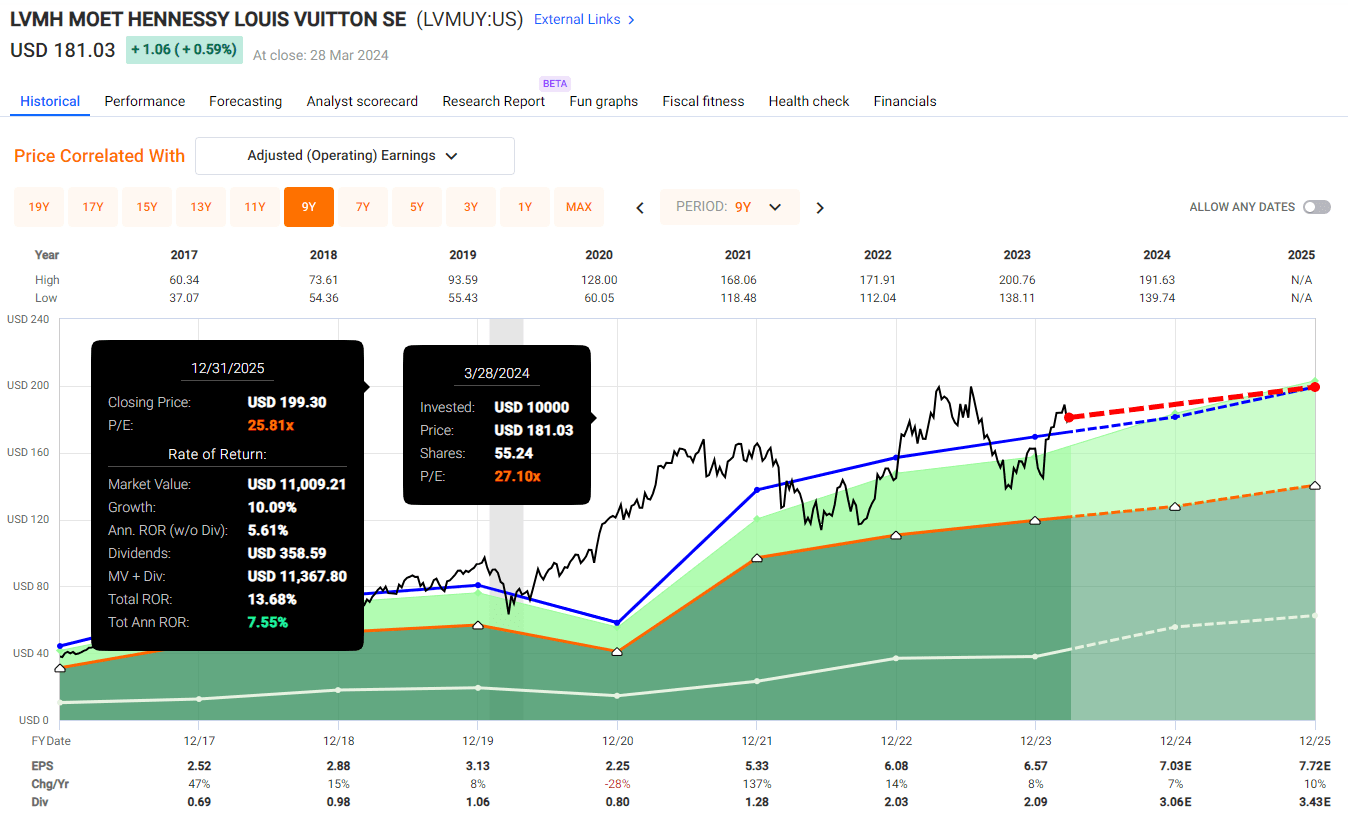

At the moment the scenario is completely different, the inventory has ran up 30% since its low in January and the corporate is at the moment buying and selling at a blended P/E ratio of 27.1x.

Once we zoom-out, since 2003 the corporate has been buying and selling on common at 23.1x its earnings with common annual EPS progress of 12.8%.

Within the meantime, LVMH has change into €418 billion juggernaut, 2nd most respected firm in Europe, and the expansion will likely be harder to return by and acquisitions might need considerably lesser impact on its bottom-line progress.

But, the expectations for the shares traded within the US is that the EPS progress will proceed at a following fee:

- 2024: $7.03E, YoY progress of seven%

- 2025: $7.72E, YoY progress of 10%

- 2026: $8.41E, YoY progress of 9%

From the analyst forecasts we are able to see that certainly a normalization of EPS progress is anticipated and the occasions of excessive double-digit progress as skilled between 2020 to 2022 are principally over, a minimum of for now.

Nonetheless, we can not disregard the standard of the corporate and its “AA-” credit standing by S&P World, which definitely deserves a premium valuation, in comparison with some opponents corresponding to:

- Compagnie Financiere Richemont SA (OTCPK:CFRHF), blended P/E of 21.5x

- Kering SA (OTCPK:PPRUF), blended P/E of 14.9x

Contemplating the anticipated EPS progress of LVMH to be round 8.5% over the following three years and its huge moat and management with important “skin in the game”, I’d anticipate the corporate’s truthful worth to be round 25x its earnings.

Assuming the expansion materializes and the valuation contracts from right now’s 27.1x its earnings to 25x, buyers might fairly anticipate returns of round 7.6% together with the dividend.

LVMH Valuation (Quick Graphs)

The anticipated return falls in need of a ten% to fifteen% minimal returns that buyers ought to goal for by inventory selecting and I’d advise warning, whereas ready for a greater entry level, therefore I’m downgrading the score to “Hold” in the intervening time solely because of the stretched valuation.

Takeaway

LVMH is an epitome of luxurious and high quality alike, being led by the Arnault household with 48% stake within the firm, driving the shareholder-friendly nature of the enterprise which has been rewarding shareholders handsomely for final twenty years.

The luxurious items {industry} is nicely resilient to financial cycles catering to wealthier people, but the expansion is normalizing in the direction of high-single digits to low-double digits, which was confirmed by the corporate’s management.

With the anticipated annual EPS progress to proceed at round 8.5% over the following three years, we have to alter the valuation expectations, which has change into stretched not too long ago after the 30% spike in share value because the January backside.

Given the standard of enterprise and its huge moat, I’d anticipate the corporate to commerce at a premium valuation of round 25x its earnings, which is nicely under right now’s blended P/E of 27.1x, implying potential overvaluation which can end in poor efficiency for buyers trying to provoke their positions at right now’s costs.

I counsel warning and to maintain the corporate on a watchlist in the intervening time, capitalizing on any pullbacks which can make the corporate engaging as soon as once more.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.