Editor’s notice: Looking for Alpha is proud to welcome Bullish Insights as a brand new contributor. It is simple to develop into a Looking for Alpha contributor and earn cash in your finest funding concepts. Lively contributors additionally get free entry to SA Premium. Click here to find out more »

Khanchit Khirisutchalual

Funding Thesis

In at this time’s dynamic market panorama, one firm stands out as a compelling funding alternative to me, FinVolution Group (NYSE:FINV). With a confirmed observe file of progress, strong monetary efficiency after itemizing, and a strategic imaginative and prescient poised for “Local Focus, Global Outlook”, FINV represents a stable purchase alternative. Be a part of me in exploring the potential of FINV as we delve into an in depth evaluation of why this inventory may drive important worth for traders in the long term.

Firm Overview

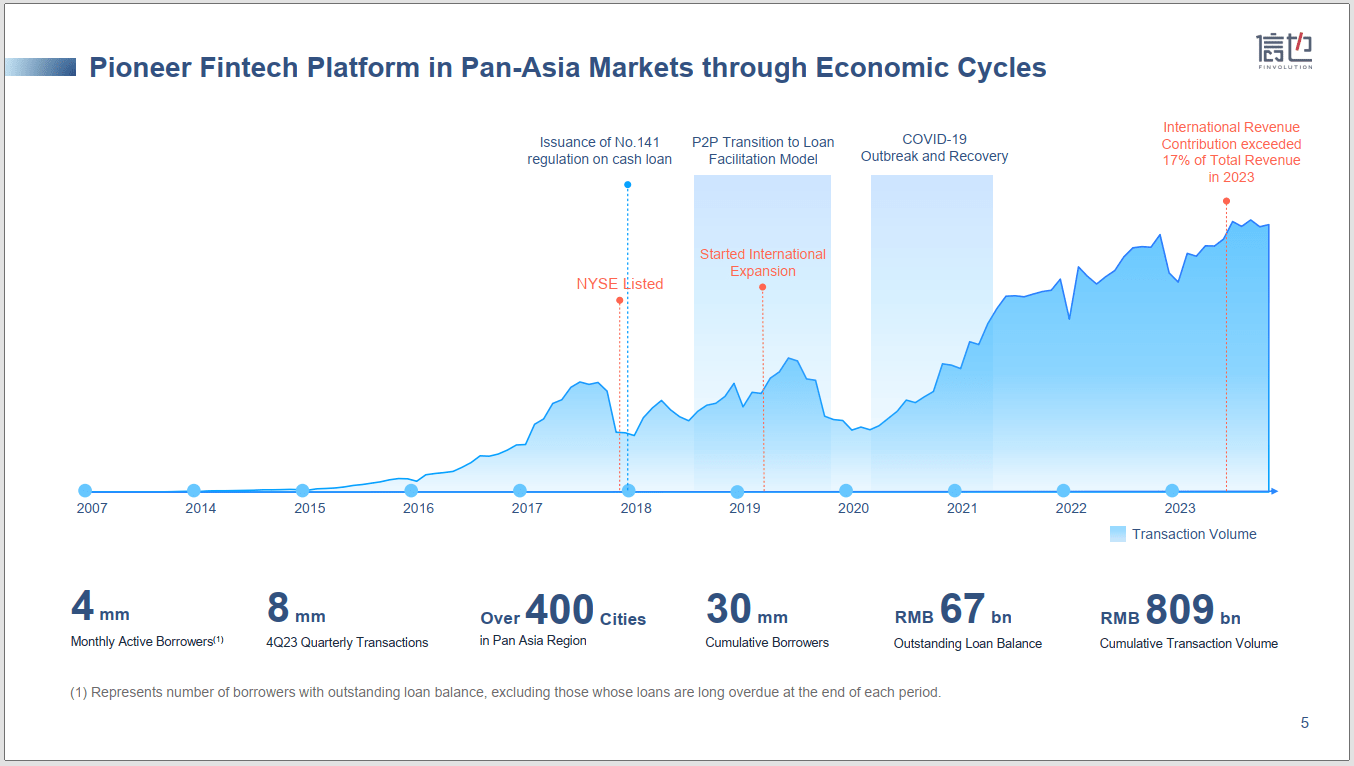

FINV, established in China in 2007, is a pioneer in China’s P2P {industry}. In 2017, they had been listed on the NYSE after a decade of operation. Nevertheless, shortly after their itemizing, they confronted regulatory stress as a result of so-called No. 141 regulation on money loans in China, which prohibited direct lending from China P2P gamers to debtors.

For my part, tightened regulation benefited FINV. Throughout this course of, quite a few small-to-medium gamers ceased the sport, and FINV along with the opposite 3 gamers survived and have become the foremost gamers within the client finance {industry}, particularly Qifu Expertise (QFIN) and LexinFintech (LX), whereas Lufax (LU) is specializing in the SME lending enterprise.

From 2018 to 2019, FINV underwent a transition from its P2P mannequin to a mortgage facilitation mannequin. As a substitute of immediately lending cash to debtors, FINV now acts as an middleman between debtors and near 100 financial institutions that collaborate with FINV. They supply important companies to their collaborated monetary establishments similar to buyer acquisition, danger evaluation, customer support, and post-loan assortment, then monetary establishments present financing to correspondent debtors. Consequently, each FINV and monetary establishments share pursuits primarily based on the danger preferences of monetary establishments, so-called funding prices by FINV.

Native Focus, International Outlook Technique

It’s price noting that regardless of dealing with regulatory stress and the challenges posed by COVID-19 afterward, I feel FINV has demonstrated outstanding resilience by way of transaction quantity progress trajectory throughout these difficult intervals. Their confirmed know-how and capabilities within the on-line client finance sector have enabled them to navigate via completely different financial cycles.

Along with its increasing presence within the an increasing number of mature China market, FINV entered Indonesia in 2018 adopted by entry into the Philippines in 2020. In accordance with their disclosure materials, by the top of 2023, worldwide income contribution accounts for approximately 17% of complete income with a YoY enhance of seven%. I feel it is a good transfer to mitigate regulatory dangers and obtain sustained progress on the group degree.

Firm Historical past (FINV 4Q23 Investor Presentation)

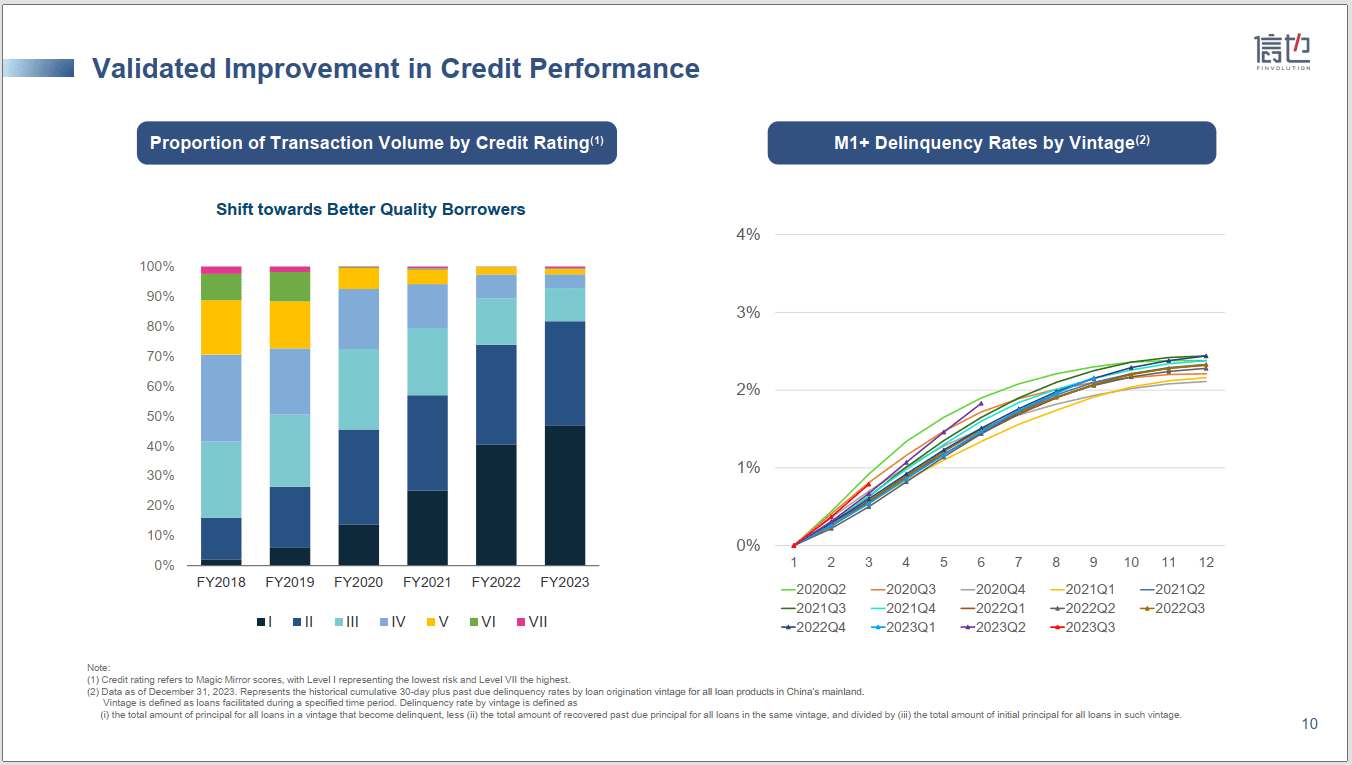

In response to the rate of interest reduce trajectory, FINV has carried out measures to manage credit score prices, mitigate price reduce affect, and keep final profitability. To boost credit score efficiency, FINV has shifted in the direction of greater high quality debtors, categorizing them from Stage I (highest high quality) to Stage VII (poorest). As of 4Q23, roughly 91%-92% of the transaction quantity is attributed to Stage I-III debtors, in comparison with nearly 40% in 2018.

Buyer Cohort (FINV 4Q23 Investor Presentation)

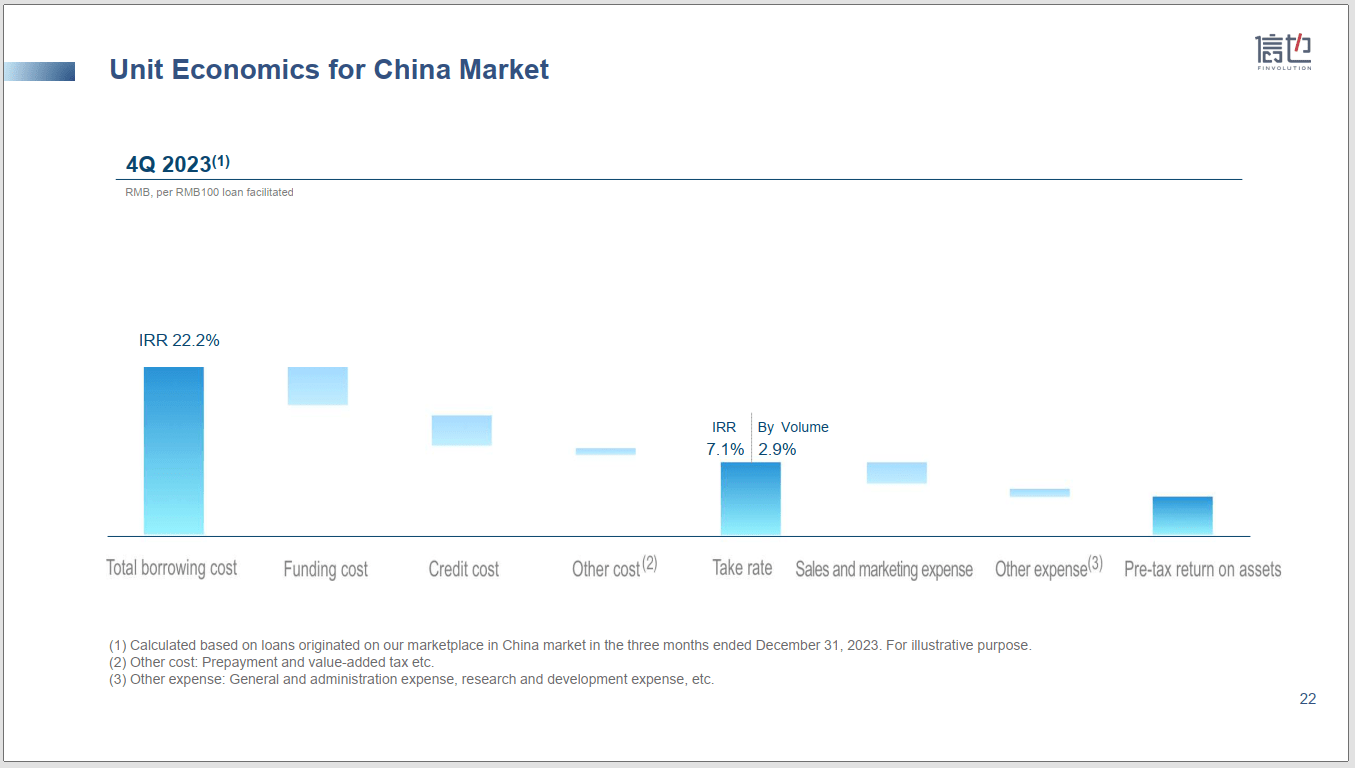

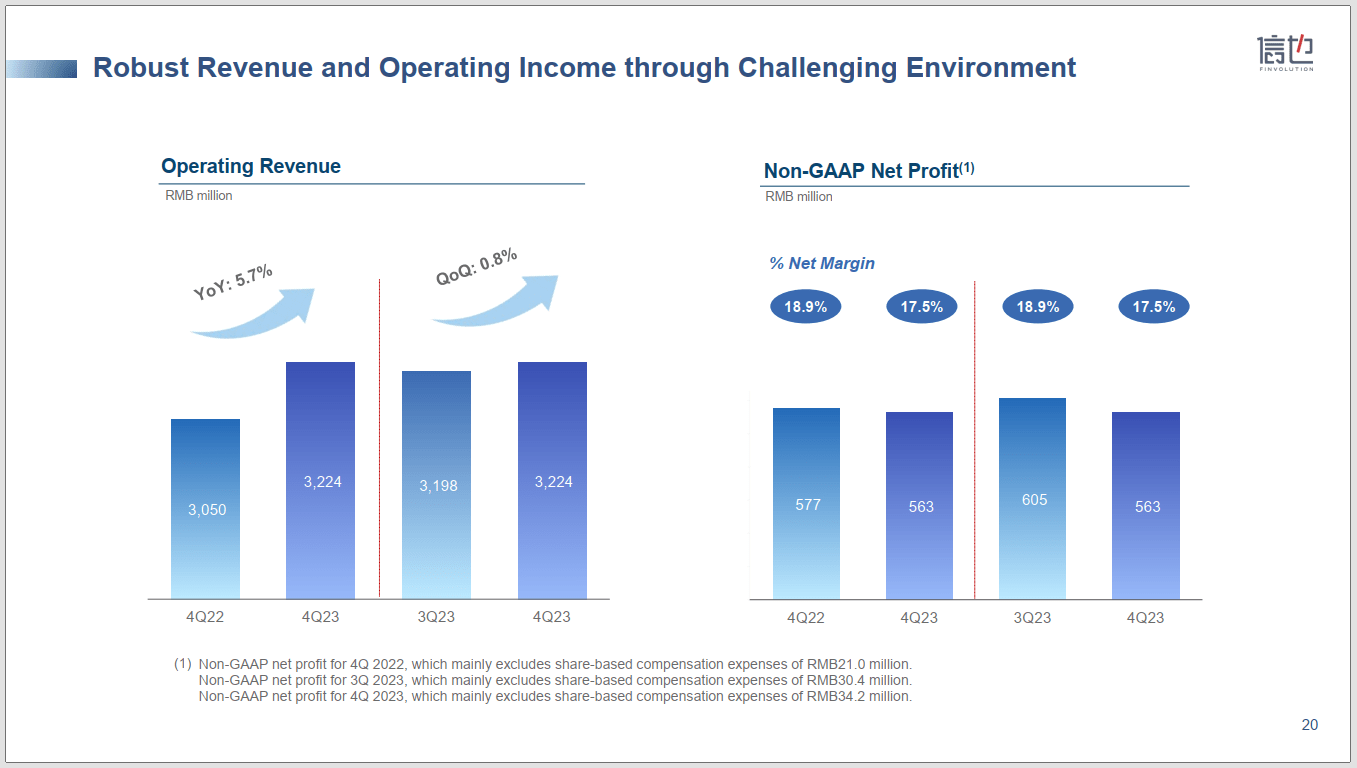

When it comes to its unit economics in China, the present rate of interest is capped at 24%, and FINV maintains an rate of interest of twenty-two.2%, which has stabilized in latest quarters. The take price is primarily calculated by deducting funding prices, as talked about earlier, together with credit score prices, generated from mortgage delinquency. Different prices similar to prepayment and value-added tax have minimal affect on the take price. As of This fall 2023, the volume-based take price decreased to 2.9% from 3.1% in Q3, I imagine this decline is principally resulting from lingering asset high quality stress in China market, aligning with {industry} friends’ explanations. Fortuitously, the upside potential lies in steadily enhancing funding prices, which have improved by 30 bps QoQ and 100 bps YoY, attributed to the preferable regulation of provide and demand between belongings and cash in China. Trying forward, FINV’s steady borrowing charges mixed with better-than-industry delinquency charges (classic delinquency at 2.5% for the latest 3 months) and enhanced funding prices allow it to attain greater take charges and ROA (round 3.6%, web revenue RMB2.4bn divided by excellent mortgage stability: RMB67.4bn) in comparison with its opponents in China.

Unit Economics (FINV 4Q23 Investor Presentation)

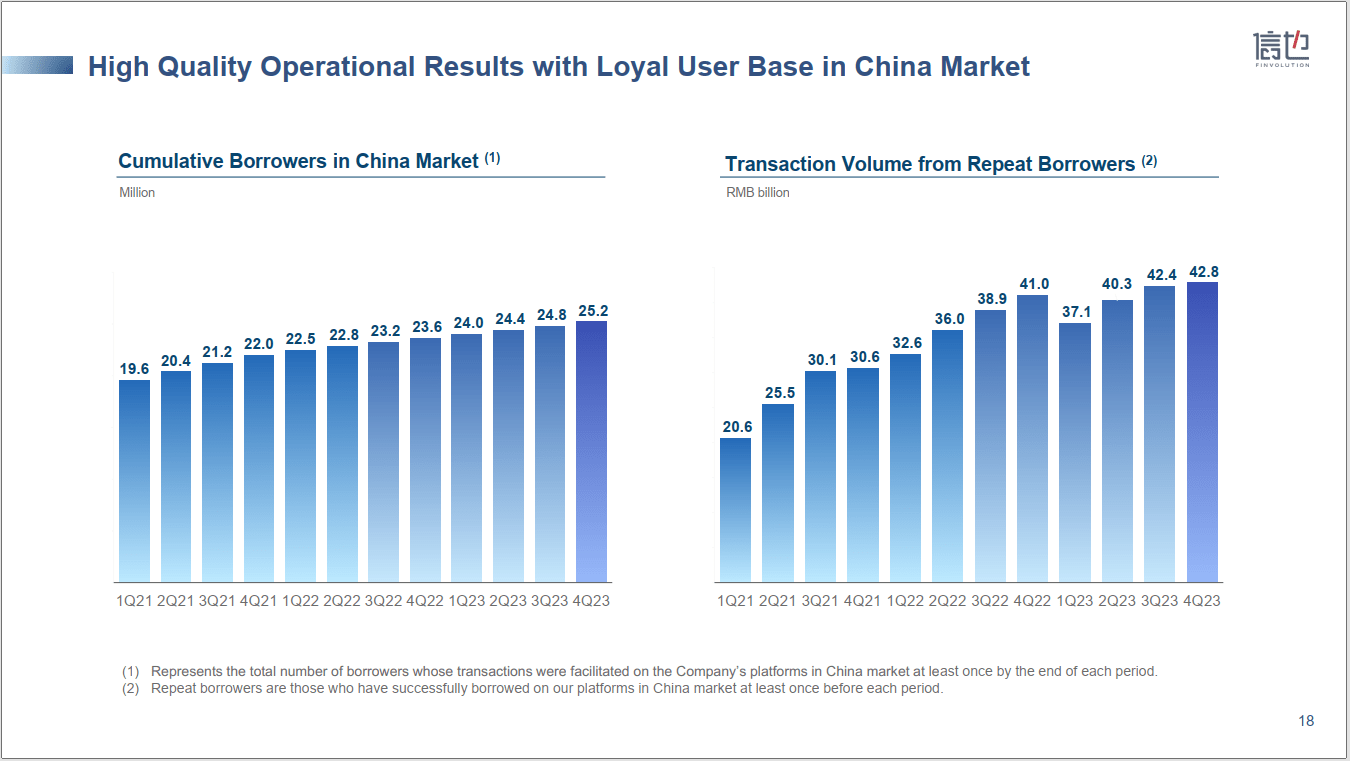

For my part, the expansion of FINV in China and worldwide markets seems strong. Notably, China market is experiencing progressive progress, whereas worldwide markets are exhibiting accelerated growth through the early levels of the P2P {industry}.

The China and worldwide markets characterize two levels of market growth for on-line client finance: one characterised by the maturity stage, and one other marked by the introduction & progress stage. In consequence, within the China market, roughly 85% of transaction volumes are pushed by repeat debtors (calculated by transaction quantity from repeat debtors RMB42.8bn/complete transaction quantity in China market RMB50.1bn).

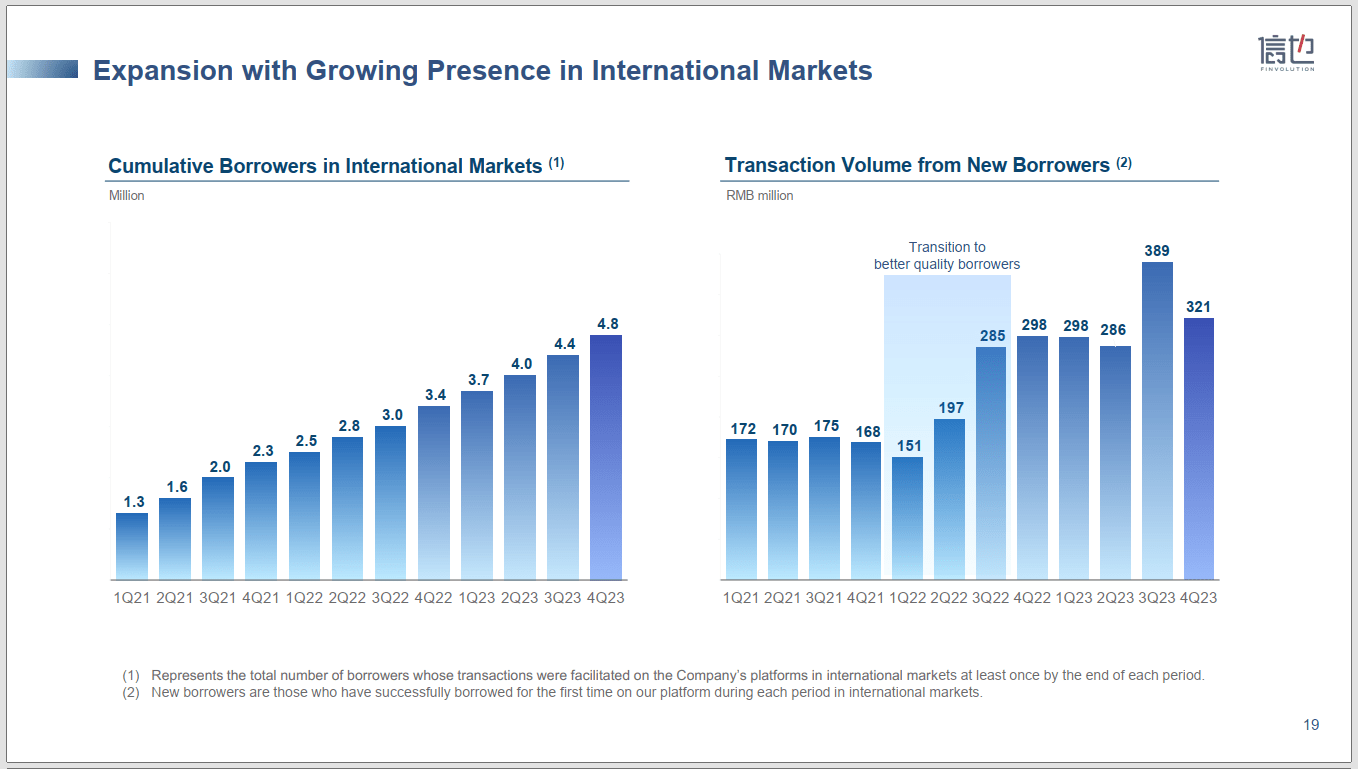

In worldwide markets, FINV is specializing in new buyer acquisition to enhance market penetration charges, its transaction quantity in 2023 elevated to RMB7.85 billion, representing an 84.7% YoY progress, whereas revenues rose to RMB2.1 billion, exhibiting an 85.9% YoY enhance and contributing 17.0% to complete web revenues.

China Market (FINV 4Q23 Investor Presentation)

The Indonesian market is at present present process its 2nd spherical of rate of interest adjustment from a each day price of 0.4% to 0.3%, following a earlier adjustment from 0.8% to 0.4% in 2021. This has resulted in FINV transitioning in the direction of higher high quality debtors, aligning with the trajectory carried out within the Chinese language market. As talked about through the earnings name, FINV expects the take price after the pricing adjustment in Indonesia’s market to be round 10%, down from 13% previous to the adjustment, I feel it’s nonetheless way more worthwhile than the China market (4Q23 take price: 2.9%). Notably, the rate of interest adjustment has led to a 20% enchancment of their credit score value and buyer acquisition prices have decreased by 8%, due to market consolidation, some small and medium-sized gamers have been unable to maintain profitability through the transition interval.

Within the Philippines market, the transaction quantity and excellent mortgage stability are increasing at a YoY progress price of over 200%. Contemplating the steady regulatory setting and strong growth within the client finance sector within the Philippines, I feel FINV’s Philippine automobile is predicted to contribute a bigger portion of transaction quantity and income to the worldwide sector going ahead.

Worldwide Markets (FINV 4Q23 Investor Presentation)

Notably, amongst main gamers within the Chinese language market, FINV stands out as the only firm dedicated to delivering a 5%-10% year-on-year transaction quantity progress, whereas different opponents are projecting zero or maybe destructive progress by 2024 (QFIN was offering 1Q24 web revenue steerage slightly than transaction quantity steerage; and LexinFintech was offering a GMV steerage, which accounted for 2.1% of transaction quantity). I feel it’s a good signal of its functionality to ship sustained progress throughout financial cycles.

Monetary Efficiency

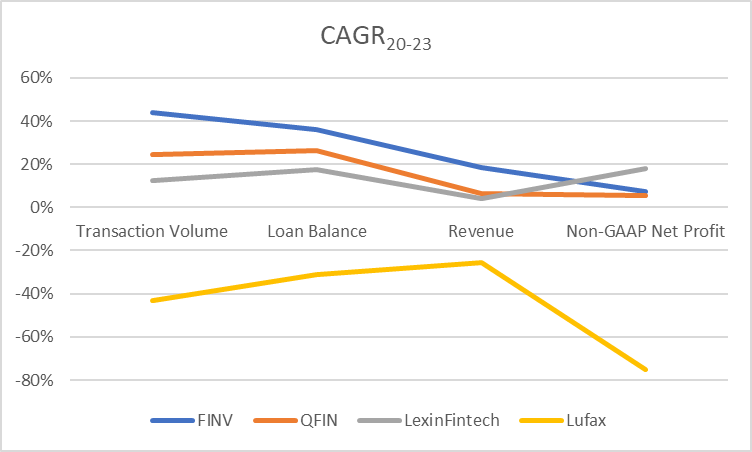

Moreover, in response to the disclosed earnings releases from 2020 to 2023, I made a CAGR comparability amongst key operational and monetary figures, FINV’s transaction quantity has been increasing at a CAGR of over 40% and its excellent mortgage stability was near 40% CAGR, surpassing its opponents. Its income has been constantly rising with a CAGR of practically 20% from 2020 to 2023, the place its main opponents are beneath 10%, together with QFIN, LX, and Lufax.

The one weaker indicator is non-GAAP web revenue. I feel it’s primarily resulting from ongoing investments in abroad markets, potential licenses, and buyer acquisition efforts in numerous international locations, together with periodic asset high quality pressures in China. The underside-line efficiency is but to be totally launched – the online revenue margin of FINV remained constant at roughly 20% with slight fluctuations, however nonetheless surpassing that of nearly all of different sectors.

Comparability with Friends (Earnings Releases throughout 2020-2023)

Trying forward, it’s anticipated that FINV’s Indonesian market will obtain profitability for your complete 12 months in 2024 by the corporate. Equally, profitability is predicted for his or her Philippines enterprise through the second half of 2024. In China’s market context, because the financial restoration continues and potential alleviation of asset high quality pressures emerges, I imagine that an enchancment above a take price of three% might be anticipated.

Income and Revenue (FINV 4Q23 Investor Presentation)

Capital Return Program

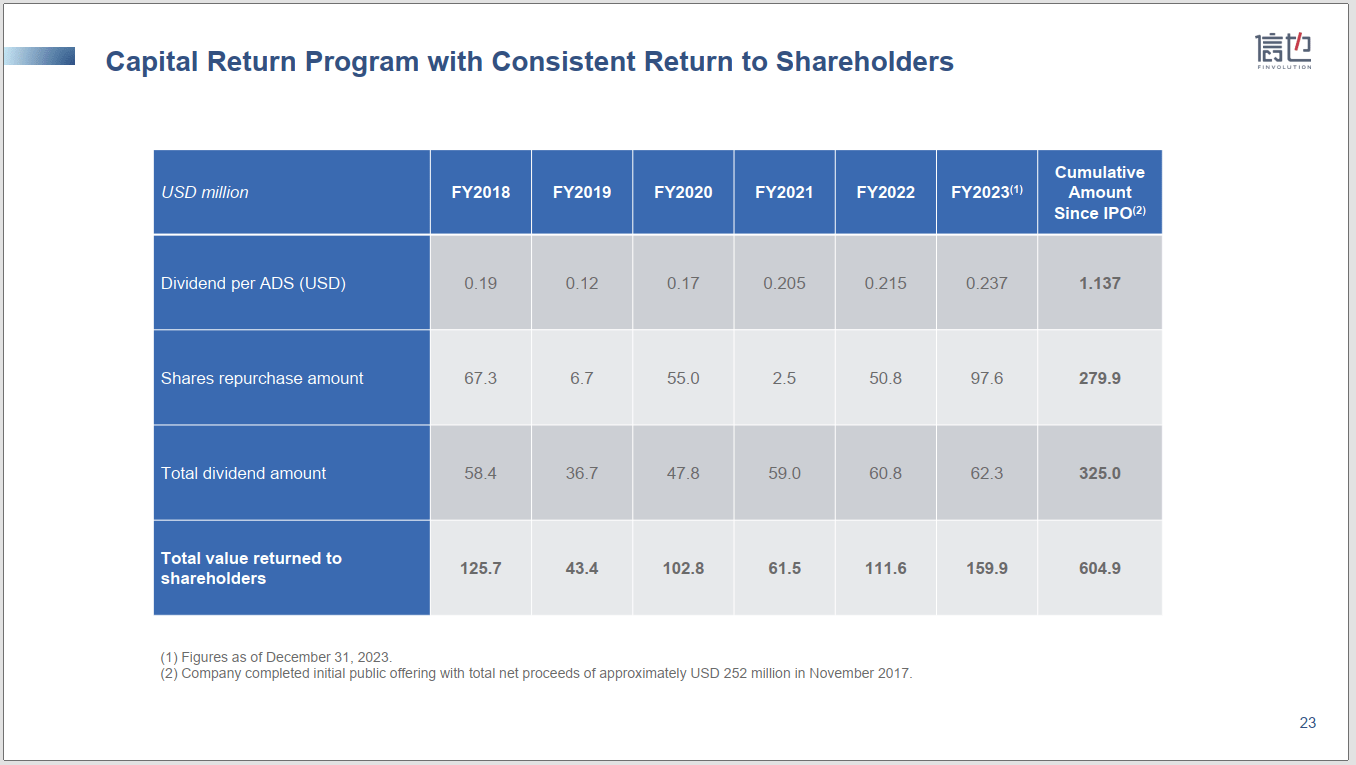

Lastly, pushed by the sustained progress in each home and worldwide markets, FINV has been enhancing shareholder worth via its capital return program, which incorporates annual dividends and share repurchases.

In accordance with the earnings launch, in 2023, FINV deployed near US$100 million to repurchase our shares and US$62 million for dividend distribution, representing 49% of web revenue for 2023 and a mixed yield of 11%. For those who have a look at the desk above, on a five-year common, dividend will increase of greater than 10% mixed with constantly rising income characterize an honest prospect for rising returns.

Capital Return (FINV 4Q23 Investor Presentation)

I feel that capital returns have been an ad-hoc matter this 12 months, and we have seen quite a few Web giants begin emphasizing shareholder returns and large dividend distributions or share repurchase packages over highlighting progress, as the standard progress story is fading. For my part, the distinction for FINV is that they’re making an attempt to stability progress in each China and worldwide markets with enhancing shareholder returns at a payout ratio, in 2023, their complete payout ratio expanded to almost 50%. In the course of the earnings name, administration said that they’re assured in sustaining a observe file (6 years of capital return) and persevering with to ship a constant enhance in dividends for shareholders (common of 10% YoY progress prior to now 5 years).

Valuation

I additionally search different sources to show my opinion on FINV’s progress momentum and functionality, primarily based on my investigations of its methods, and operational and monetary fundamentals.

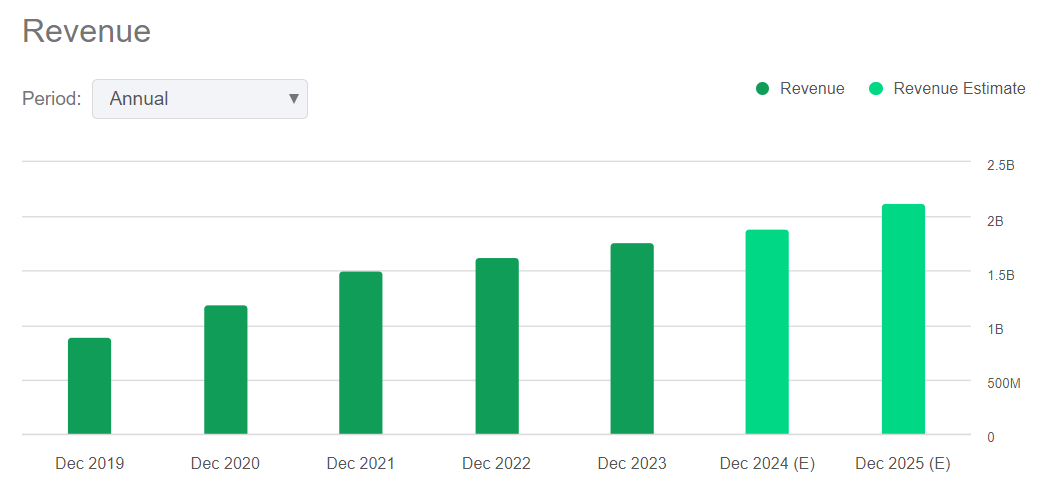

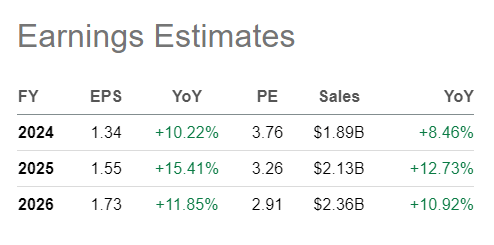

In accordance with Looking for Alpha consensus, their income is predicted to additional develop to over US$2.13B in 2025 vs US$1.77B in 2023, representing a 20% progress. And its EPS is predicted to develop at above 10%-15% YoY.

Income Estimates (Looking for Alpha) Earnings Estimates (Looking for Alpha)

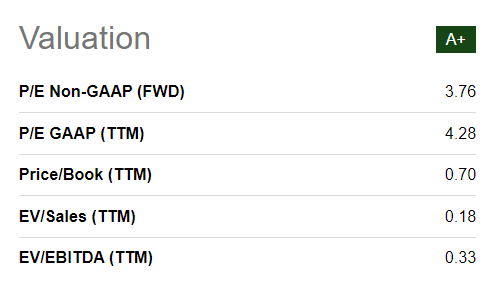

For those who have a look at FINV’s money and money equal + short-term investments as of 4Q23, which is roughly US$1.12B, nearly equal to its market cap as of 31 March 2024 (US$1.41B), and its P/B stands at 0.70, whereas P/E at 4.28, far behind its US opponents, I imagine it’s primarily resulting from geographical and political points as China ADR, however its fundamentals look wholesome and sustainable.

Valuation (Looking for Alpha)

Dangers To My Thesis

For my part, the important thing draw back dangers for this bullish alternative embody however should not restricted to:

Tightened laws in China, the place I feel a 24% annualized cap is at a low degree worldwide and there may be minimal room for additional downward adjustment to non-mortgage money loans;

Tightened laws in Indonesia, in response to OJK regulation, they do have a plan to steadily regulate the each day rate of interest to 0.3% in 2024, 0.2% in 2025, and 0.1% in 2026, the place this would possibly squeeze FINV’s profitability on this market, however as I discussed above, as Prime 3 participant available in the market, FINV advantages from market consolidation, optimized advertising value and higher credit score efficiency, which can offset the facet impact of price changes;

Tightened laws within the Philippines, it is a potential danger whereas I feel there isn’t a signal of regulatory stress within the Philippines market;

Sharp fluctuations in asset high quality/delinquency price, for a web-based lending firm, the core enterprise danger lies in asset high quality. There isn’t a historic observe file exhibiting that FINV did not handle its danger metrics and asset high quality, I feel future uncertainty lies in altering administration model, macroenvironment headwinds, gradual restoration in China’s economic system, and many others.;

Scarcity in funding assets, I feel this danger resulting from abroad growth is resource-consuming, despite the fact that FINV’s present stability sheet seems to be wholesome, it might face deficiency if it enters into a number of new international locations at one time and with out good allocation of assets;

Fiercer competitors within the international locations the place they function, this occurs within the mature China market, the place their Gross sales and Advertising and marketing bills proceed increasing from RMB1.6B in 2021 to RMB1.9B in 2023.

Conclusion

In a nutshell, for my part, FINV’s present technique of “Local Focus, Global Outlook” seems to be efficient in dishing out regulatory dangers and reaching sustained progress benefiting from the early stage of P2P growth in these rising markets. So long as they proceed glorious administration of asset high quality, I imagine the compelling progress trajectory will probably be sustained and therefore replicate a stronger capital return to shareholders.