Imagesrouges/iStock by way of Getty Pictures

Bonds and fixed-income securities have develop into way more in style investments these previous few years, as Federal Reserve hikes have led to a lot increased yields. Bonds and bond funds range, with completely different traits together with maturities and credit score danger. On this article, I will be evaluating short-term and long-term bonds, how their dividends, returns, and danger, evaluate.

Yield Comparability

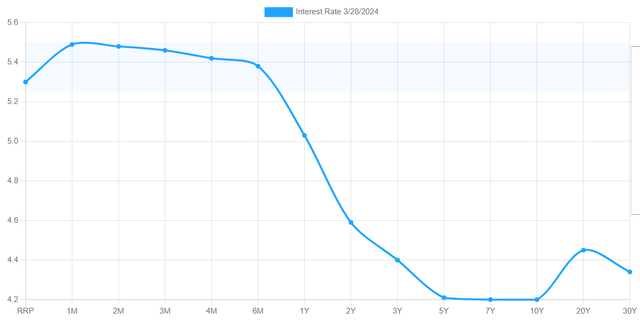

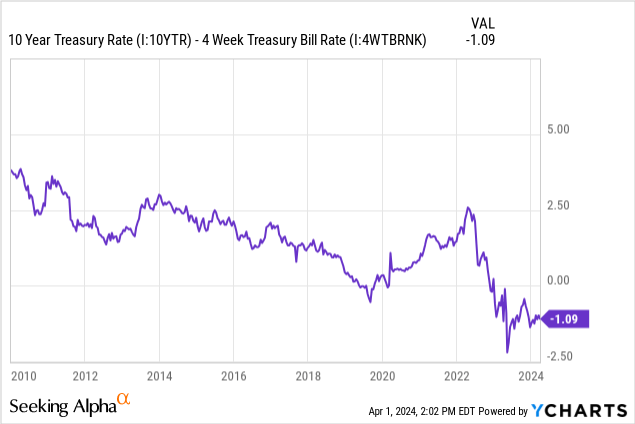

Quick-term bonds at present yield greater than long-term bonds, holding credit score high quality fixed, and with a couple of exceptions. For instance, short-term treasuries are likely to yield lower than long-term treasuries, with a pair exceptions within the curve.

U.S. Treasury Yield Curve

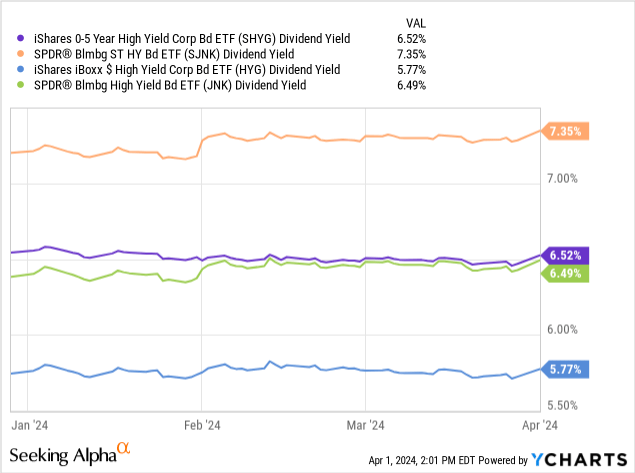

As one other instance, benchmark short-term high-yield company bond ETFs yield greater than broader high-yield ETFs. There are some exceptions right here, nevertheless.

The above is a major benefit of short-term bonds, a minimum of proper now.

Generally, long-term bonds are likely to yield greater than short-term bonds, as compensation for his or her added rate of interest danger, and as a consequence of tying up investor capital for longer. For instance, 10y treasuries have yielded greater than t-bills throughout a lot of the previous decade.

Present situations are an exception to the long-term pattern, and are unlikely to persist for lengthy, because the Federal Reserve will seemingly minimize charges within the coming months.

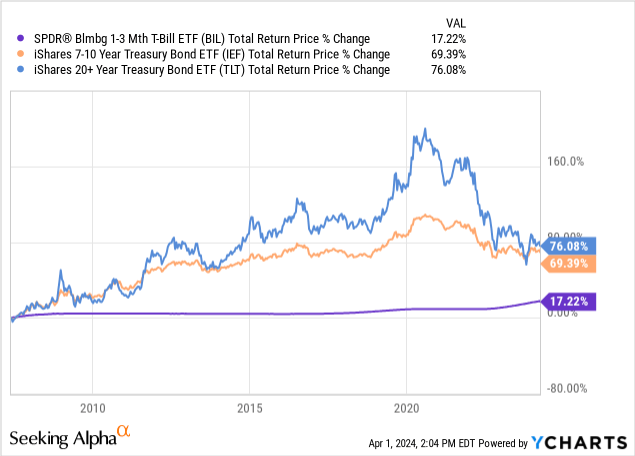

As a result of above, long-term bonds are likely to outperform short-term bonds. That is the case for t-bills, medium-term treasuries, and long-term treasuries, for the previous 20 years or so.

However, as short-term bonds do yield greater than long-term bonds proper now, short-term bonds stay a powerful funding alternative proper now. I might personally choose short-term over long-term bonds these days, though extra dovish traders would possibly disagree.

Though the above appears a bit apparent or redundant, I do not suppose it’s. Generally, short-term bonds yield a lot lower than long-term bonds. That’s not the case proper now, and I feel that’s an extremely necessary truth for traders to think about, and an necessary benefit of short-term bonds. T-bills haven’t supplied aggressive yields in over a decade, so these are way more enticing investments now than previously.

Capital Good points Comparability

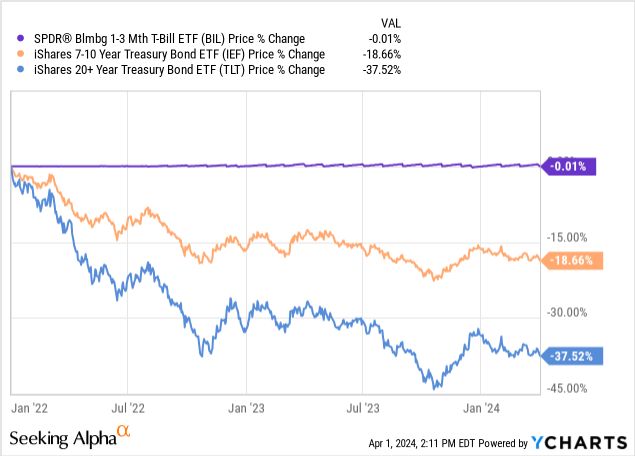

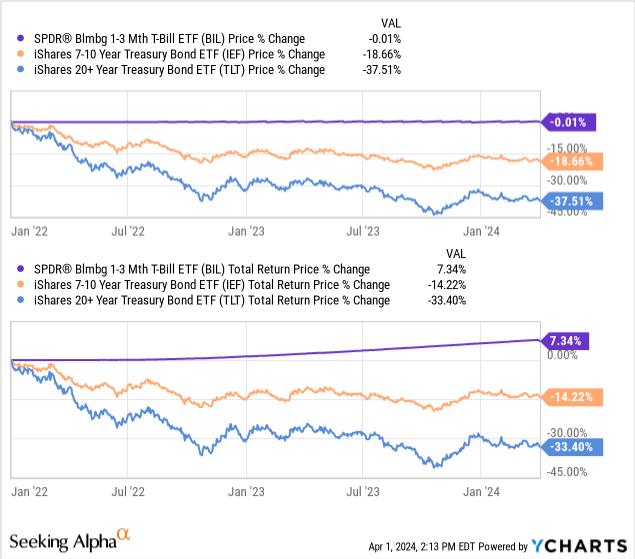

Generally, bonds are revenue automobiles, so potential capital positive factors are low. Proper now, the state of affairs is a bit completely different. Prior Federal Reserve hikes led to decrease bond costs, as traders offered off their older, lower-yielding bonds to purchase newer, higher-yielding options. Quick-term securities weren’t all that impacted, as these have (principally) matured by now, and as a consequence of their decrease length. Lengthy-term securities noticed a lot increased losses, as a consequence of increased promoting strain / length.

For instance, evaluate costs for benchmark t-bill, medium and long-term treasuries since early 2022, when the Fed began to hike.

As a result of above, longer-term bonds have a lot higher potential capital positive factors than short-term bonds proper now. For positive factors to materialize, traders should both watch for bonds to mature, which might take many years for long-term bonds, or for getting strain to extend, which ought to happen if the Federal Reserve hikes charges aggressively. Slower, more methodical rate hikes may not essentially result in higher bond prices, however.

Complete Returns Comparability

Bonds are revenue automobiles, so long-term returns are nearly solely composed of, and depending on, dividend yields. As long-term bonds typically yield greater than short-term bonds, their long-term returns are increased.

Then again, as short-term bonds at present yield greater than long-term bonds, I feel there’s a very sturdy argument to be made that short-term bonds will outperform within the coming months. This has been the case these previous few years, however principally as a consequence of decrease bond costs, not the dividends themselves (these did assist although).

Total, I might count on long-term bonds to outperform short-term bonds long-term, however by a lot lower than common.

Credit score Threat Comparability

Bond maturities don’t instantly, or essentially, affect credit score danger or annual default charges. Quick-term securities will be high-quality, suppose t-bills, or low-quality, suppose short-term high-yield bonds. Identical with long-term securities. However, there are a number of necessary developments or caveats to this.

Lengthy-term securities have a tendency to be high-quality holdings, as typically solely high-quality issuers are able to issuing long-term debt at affordable costs. Some high quality issuers deal with long-term debt to lock-in charges as properly. There are a lot of exceptions to this, however the developments are actual, and do affect bond markets. For instance, evaluate the maturity and length of the biggest investment-grade and high-yield bond ETFs:

Fund Filings – Desk by Writer

Evaluating maturity dates for investment-grade and high-yield bonds reveals an analogous sample, with a higher proportion of investment-grade bonds having maturities of +5 years than high-yield bonds.

S&P – Desk by Writer

Quick-term investment-grade securities are arguably safer than comparable securities of longer maturities, as protected, high quality corporations nearly by no means go bankrupt in a brief period of time. Apple (AAPL) cannot conceivably go bankrupt subsequent month, not with a $162B war chest. It might, maybe, go bankrupt in a few years, assuming gross sales plummet and the corporate begins hemorrhaging money.

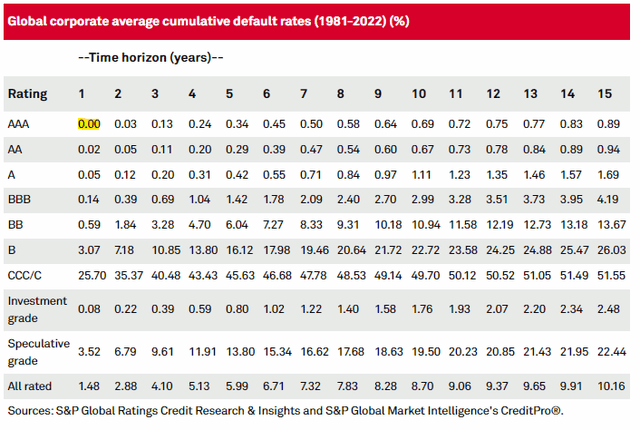

Default charges information reveals the identical, with AAA-rated bonds having a 0.00% default charge in a 1y time horizon, rising to 0.69% on the 10y mark. AAA-rated bonds do generally go bankrupt, however the course of successfully all the time takes a couple of yr. Default charges for bonds with different credit score scores reveals an analogous sample.

S&P

For my part, and contemplating the above, I feel it might be truthful to say that short-term bonds are considerably safer than long-term bonds, maintaining credit score scores fixed. On common the alternative is true, as long-term bonds are typically of upper high quality than short-term bonds. I would not personally draw any vital conclusions from these points, however the evaluation was warranted regardless.

Curiosity Charge Threat Comparability

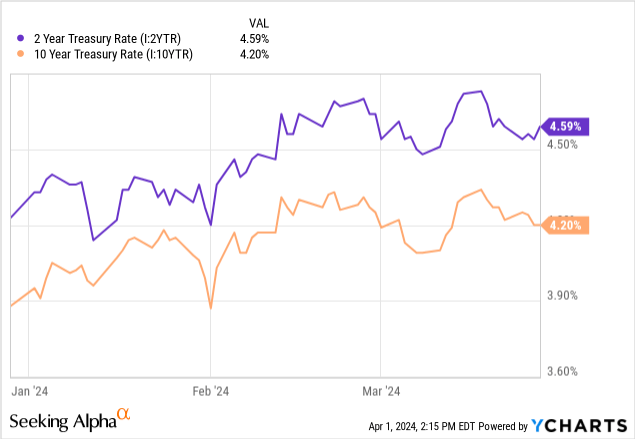

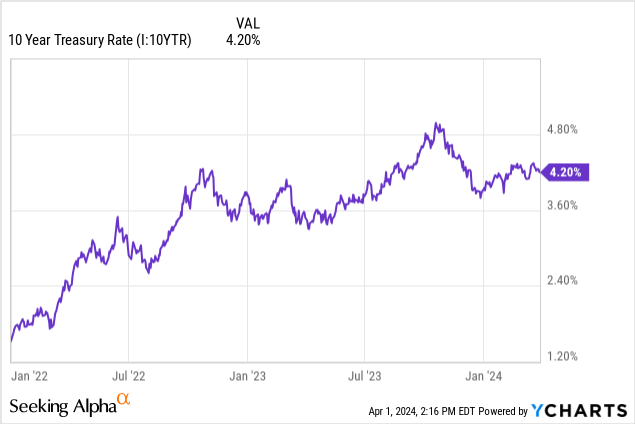

Most bonds have mounted charges from issuance till maturity. Purchase a 2y treasury immediately, and you will obtain 4.6% in curiosity yearly for 2 years. Purchase a 10y treasury immediately, and you will obtain 4.2% in curiosity yearly for ten years. Rates of interest on treasuries as a complete would possibly change, however the rate of interest on the person treasury you acquire will stay the identical from issuance till maturity.

Importantly, rates of interest on newly-issued treasuries and bonds do change on a regular basis, and the affect is a bit completely different relying on the bond’s maturity.

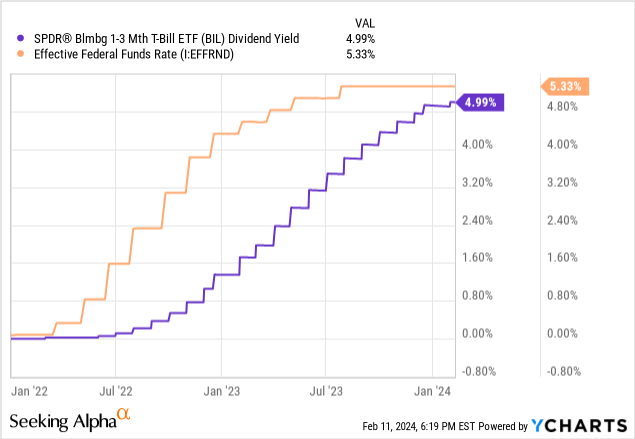

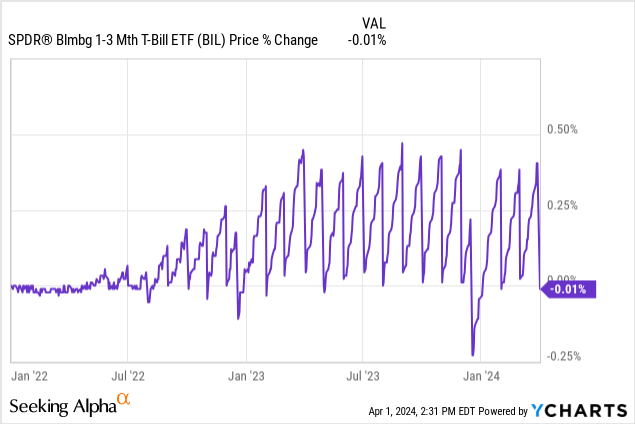

Buyers in short-term bonds are likely to see sturdy, swift adjustments to their dividends and yields when rates of interest change. Buyers in t-bills should typically wait solely a month or two earlier than their t-bills are rolled over, and charge adjustments to take impact. Buyers within the SPDR Bloomberg 1-3 Month T-Invoice ETF (NYSEARCA: BIL) have seen their yields rise from 0.0% in early 2022 to five.0% as of immediately, broadly in-line with Fed hikes.

Knowledge by YCharts

Buyers in long-term bonds see a lot decrease, and slower, adjustments to their dividends and yields when rates of interest change. Buyers in 10y treasuries should typically wait ten years for his or her treasuries to mature, and for brand spanking new charges to take impact. Buyers who purchased 10y treasuries in early 2022 at a 1.5% yield are caught with that measly yield for ten years, no matter what the market does within the interim.

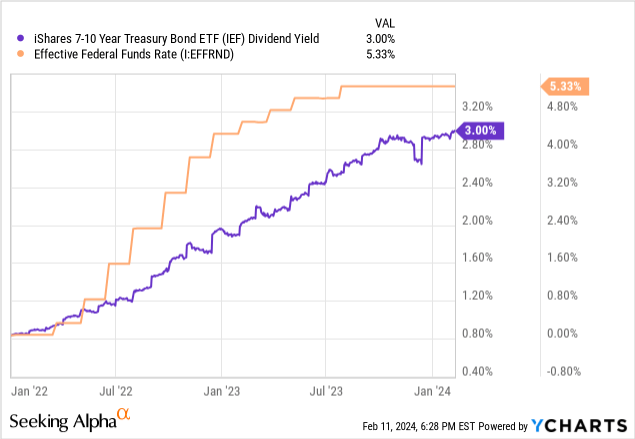

Buyers in bond funds typically see considerably extra speedy adjustments to their dividends and yields when charges change, as these nearly all the time maintain lots of / 1000’s of securities, and a minimum of a portion of those mature or get changed comparatively rapidly. For instance, traders within the iShares 7-10 Yr Treasury Bond ETF (NASDAQ: IEF) have seen their yields improve from 0.8% to three.0% in the course of the present mountain climbing cycle. Dividends have elevated, however at a a lot slower tempo than t-bills, lower than half the pace.

Knowledge by YCharts

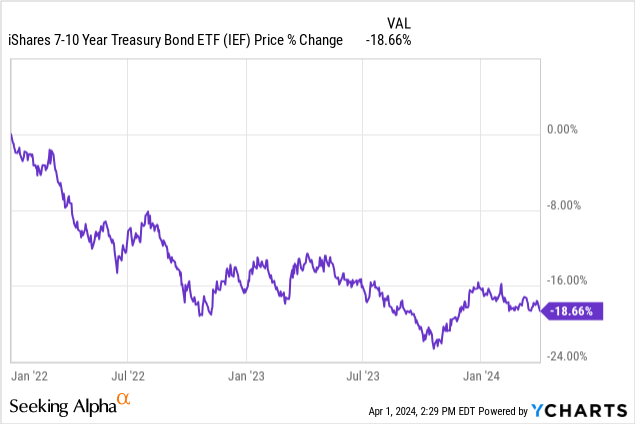

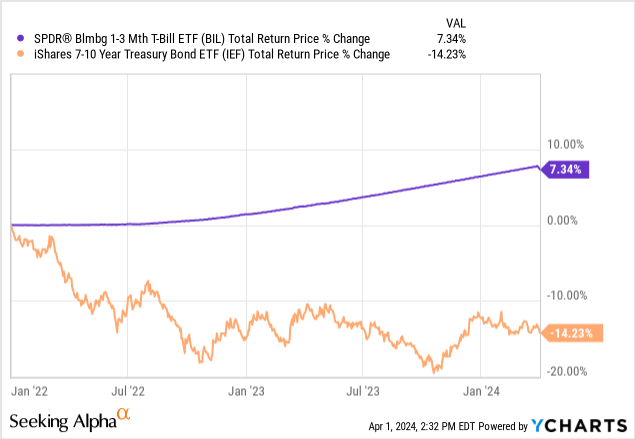

Corollary of the above is that long-term bond costs are additionally closely impacted by adjustments in charges. Buyers in 10y treasuries will shift from treasuries to t-bills if the Fed hikes, seeking increased yields. For instance, IEF’s share worth has declined by 18.7% since early 2022.

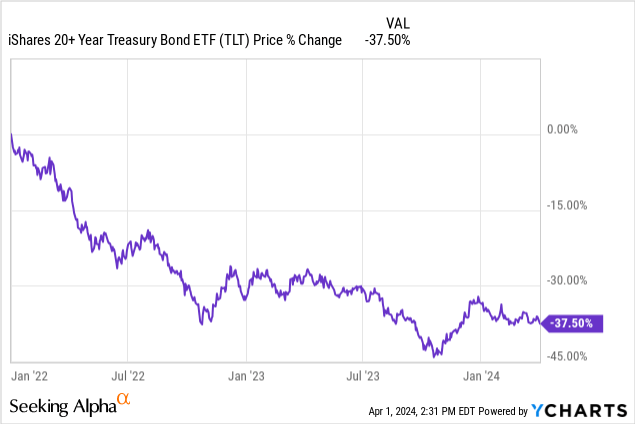

Longer-term bonds see even higher declines from the above, as they endure way more from increased charges (being caught at low yields for longer / increased length).

Quick-term bonds see a lot decrease affect, as they are often changed comparatively rapidly. BIL’s share worth has not been materially impacted by increased Fed charges, as an illustration.

Contemplating the above, short-term bonds are likely to outperform when rates of interest rise, seeing sturdy dividend development and worth stability. For instance, t-bills have outperformed treasuries since early 2022.

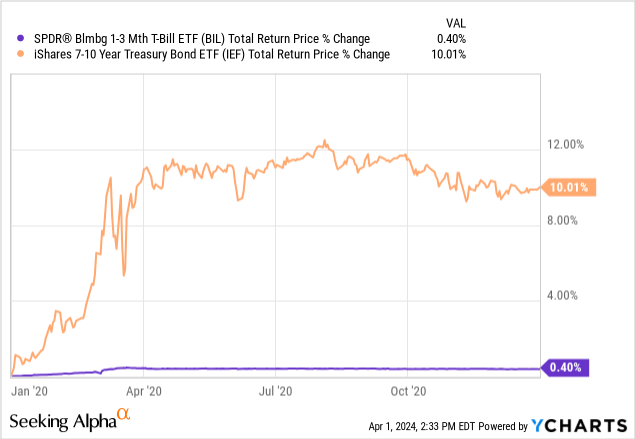

On the flipside, long-term bonds are likely to outperform when charges decline, seeing sturdy capital positive factors when this happens. For instance, treasuries outperformed t-bills throughout 2020, when the Fed slashed charges in gentle of the pandemic.

Total, long-term bonds have way more rate of interest danger than short-term bonds. This will increase total portfolio danger and volatility, an necessary unfavorable for shareholders. On the similar time, for dovish merchants increased charge danger means increased potential positive factors from decrease charges.

Reinvestment Threat / Lock-In Charges Comparability

Quick-term bonds have increased reinvestment danger, which implies that traders may not essentially have the ability to re-invest their money or roll over their funding at a charge corresponding to their present charge of return. For instance, traders in t-bills may not have the ability to roll over their securities at +5.0% within the coming months, because the Federal Reserve is more likely to minimize charges.

Lengthy-term bonds have a lot decrease reinvestment danger, as most bonds are fixed-rate, and so charges are locked-in for a number of years. Buyers in 10y treasuries, as an illustration, haven’t got to fret about rolling over their securities for ten years, a really lengthy period of time.

Reinvestment danger is a very necessary subject for retirees. Retirees specializing in t-bills would possibly see their revenue decline fairly quickly and might need to pivot to different asset lessons if charges decline. Retirees specializing in 10y treasuries solely face these points each decade.

Reinvestment danger can be a problem insofar because it makes retirement planning tough. Retirees specializing in t-bills might need points forecasting their revenue a few months into the long run. Retirees specializing in 10y treasuries have a a lot clearer thought of their revenue for the following decade.

Total Threat Comparability

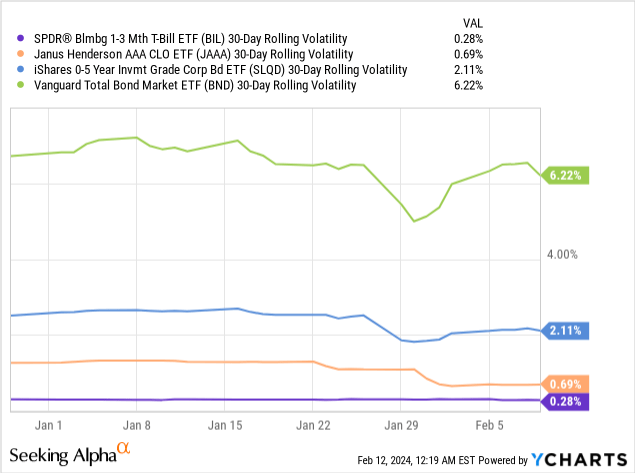

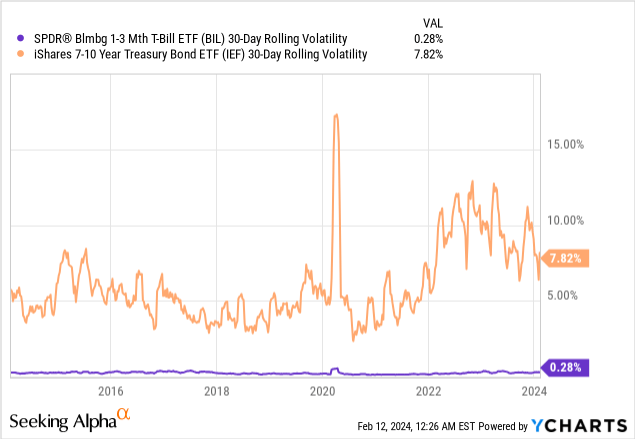

Quick-term bonds have decrease rate of interest danger than long-term bonds, which implies decrease danger and volatility on most conventional metrics. Funding-grade bonds have low credit score danger too, so short-term investment-grade bonds have the bottom volatility of all.

Knowledge by YCharts

The affect of the above is especially impactful when rates of interest are in flux, as they at present are. For instance, treasuries are all the time extra risky than t-bills, however spreads have widened since early 2022, when the Fed began to hike charges aggressively.

Knowledge by YCharts

A difficulty with the figures above is that these don’t consider reinvestment danger. For my part, the extra conventional danger and volatility metrics centered on costs do a great job at measuring a bond’s danger, which implies that short-term bonds are materially much less dangerous than long-term bonds. Some traders would possibly contemplate dividends and reinvestment danger to be extra necessary, through which case long-term bonds look much less dangerous.

Total Threat-Return Profile

Lengthy-term bonds typically have increased yields and returns than short-term bonds, though that isn’t the case proper now.

Lengthy-term bonds are typically riskier too, and extra risky. That is notably true proper now, as rates of interest are in flux.

For my part, and contemplating the above, short-term bonds have a lot stronger total risk-return profiles than long-term bonds. Quick-term bonds are a lot safer, whereas potential returns appear solely considerably decrease, with a lot of uncertainty. Underneath these situations, I want short-term bonds over long-term bonds. I’ve thought as a lot for years, and most of my top picks on this space have carried out fairly properly. Returns have been fairly sturdy YTD, however the actual check will come when the Fed begins to chop charges.

Conclusion

Quick-term and long-term bonds have many similarities and variations between them. I’ve coated among the extra salient of those on this article. Hopefully the knowledge right here was of use and curiosity to readers.

Editor’s Observe: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.