PorAbove: Crew discuss is okay, however as all the time, the buck stops on the desk of the CEO on main strategic selections. Klaus Vedfelt

If there’s one palpable actuality that buyers can depend on in valuing shares within the sector right now, it is the sure failure up to now of the band aids that high managements have utilized to the sickness of the media sector: True believers who purchase the c-suite mantra that advert help, bundling and value chopping will finally show to ship the fats earnings of early sector promise. Skepticism nonetheless prevails amongst many buyers, and for good purpose.

Let’s stipulate first that we goal these inquiries to administration because of what we consider might have lengthy been lacking in too many quarterly earnings name transcripts now we have adopted.

What each investor must know that wants readability

I start with illuminating witticism from golden age film gangster/soldier of fortune actor George Raft (1901-1980). The nice film icon ended his profession as a greeter at a Havana on line casino pre-Castro. In 1957 a reporter chanced upon him on the bar slamming bourbons between internet hosting classes.

It’s instructive.

Reporter: George, you made tens of millions. What occurred to your cash all these years?

Raft: I spent it on girls, playing and liquor… and wasted all the remainder.

It appears to me that as of now, you are spending money and time on indulgences which in impact kick the cans down the highway till such occasions as they might discover a new pathway that restores shareholder worth at a quicker tempo.

For openers – managements appear to have clung to the identical recipe for higher outcomes that seem like previous wine in new bottles. Buyers are owed extra. CEOs consider of their fixes — it is to be hoped. However many buyers will not be satisfied but by takeaways from earnings transcript Q&As.

The RXs provided we see: Shave manufacturing prices on IP, increase streaming costs, go to advert supported, make films “our viewers will love,” pray for a staunching of rampant twine chopping, put money into parks, deep dive into digital, bundle, re-bundle, purchase and promote content material, hold prices down.

All that is the equal of Raft telling the reporter that his tens of millions had been joyfully spent having a great time and to hell with prudence. Hypnotizing oneself that the nostrums introduced have up to now shared with buyers will likely be purchased as viable however appear to be dead-end streets. That is as a result of they appear to supply usual usual Captain Apparent sort of options.

Contented fan sector shares proceed to cheer lead. That’s effective and anticipated. Our ideas listed here are with those that might differ. They could be quite a few and inclined to agree. They deserve extra. A few of them will present up on the Peltz aspect of the proxy vote. Win or lose, it’s a barometer.

Our modest proposal: Acknowledge the reality: Components of DIS, WBD and PARA are undoubtedly value greater than the entire.

In the present day’s media giants are very like the Austro-Hungarian Empire pre-World Struggle I. An enormous, range of multi-lingual cultures and ethnicities that now not imply a lot in a modified world. They appear like empires which have misplaced no matter purpose it could have needed to exist to start with. Whereas media conglomerates right now have associated companies inside their portfolios, they fail the check of true synergy if it doesn’t present up in a stronger restoration of share costs. The belief {that a} buyer for one vertical is routinely one for one more lengthy longer applies with such a proliferation of decisions.

Managements want to significantly worth its enterprise items and both spin off or promote the components, use the money windfall to massively scale back debt and apply to constructing worth into the remaining verticals. And make a dedication to maintain dividends as a key precedence for shareholders to keep up shareholder worth.

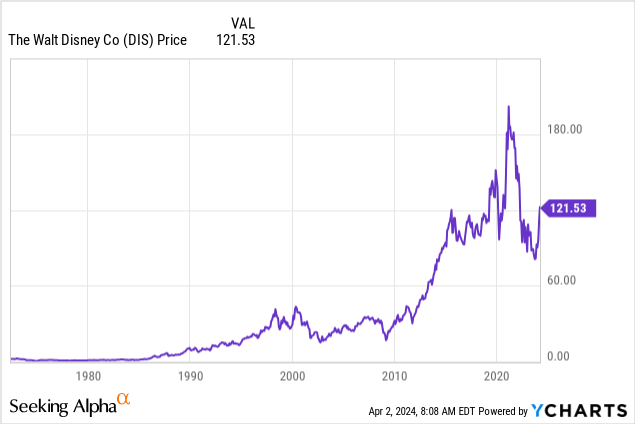

Disney: Questions for CEO Iger

How might revolving door successor Robert Chapek have lived as much as the gushing glows of the press releases on his appointment? After which swiftly change into the poster baby of widespread company ills? How was he vetted and what impressed the board about him? What does this inform us in regards to the succession planning course of at DIS?

How does ESPN and ESPNBet match with The Little Mermaid, Disney parks, Mickey Mouse t-shirts, odd cable websites and the ABC networks servicing low price range residual viewers as contrasted by streamer funds month-to-month?

Extra specifics on what Disney intends to spend on parks contemplating that inflation and the response to its pressures has made a visit to parks out there for largely the elite? It is now a enterprise that will depend on households to piggy financial institution their nickels and dimes over time to avoid wasting up for a as soon as in a lifetime deal with for the youngsters that would value $7,000. That’s cash as of late wanted to maintain meals on the desk, the mortgage paid, and fuel within the automobile to go to work. Will the growth embody price range sights for the plenty?

Or is the DIS parks buyer now a cash no object household, which is a significantly smaller, addressable market? So how does that sq. with a $60b capex expense forward? Spend more cash to draw a smaller viewers doesn’t seem to cross a logic check. The failure of the Star Wars resort ought to echo because it clearly made poor assumptions about pricing for households.

Debt discount strikes up to now are to be revered, in fact. However this isn’t profitable a struggle by making use of a 75% answer. The one method to win is by 100% which is to generate money by spin off or sale, scale back it and use the cash to wipe out not less than 40% to 50% of the debt in a single fell swoop, in any other case the present debt load will proceed to empty FCF that may very well be used much more effectively or so as to add shareholder worth by rising dividends or investing in new IP. Readability on this huge of an funding is so as now.

The monetary assemble of the studio in an period the place theatrical grosses might by no means get better to a pre-COVID degree is flawed. Extra films made for much less cash? Fewer films made for more cash?

We’ve not seen particular greenback values added to the enterprise by Disney’s pursuit of sure content material to the extent that advantage signaling might have its place, however it seems to not be a spot on the underside line.

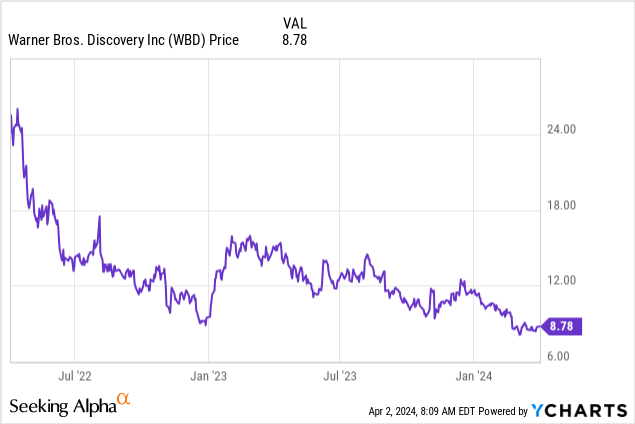

Inquiries to David Zaslav of Warner Bros. Discovery

Because of the AT&T mess, the corporate inherited too many marginal cable networks nonetheless within the portfolio. But if provided as items, they may discover viability to firms anxious to construct content material on a smaller scale.

WBD lucked out with Barbie. Congrats. However there is no Barbie manufacturing machine in operation anyplace within the leisure enterprise. We ask the identical query we did to Iger: What’s WBD’s life like tackle the studio enterprise going ahead?

Canceling product for tax loss values was a sensible transfer. Are there any extra potentialities right here of transferring product in progress into the tax loss dumper forward? Or is that technique now not out there for IP beneath improvement?

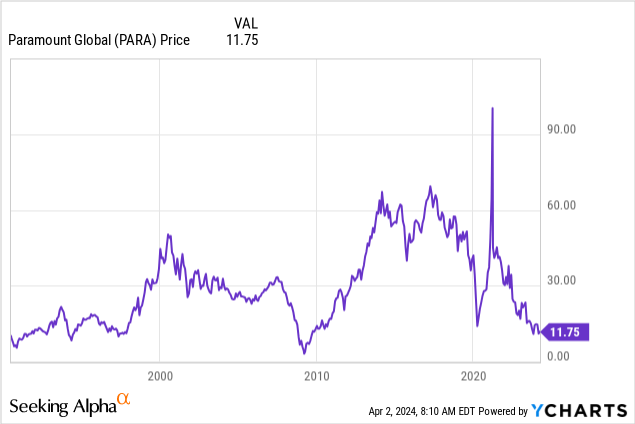

One query for Paramount’s Shari Redstone

It might seem that the corporate and its advisors have seen the very huge writing on the wall that some friends have but to see. What lies forward for PARA is a scale down or a useless finish road. Our query: What’s taking so lengthy to discover a value that matches a best-case beneath the circumstances for a deal?

Conclusion

We invite readers of this publish so as to add their questions within the feedback part beneath or problem any assumptions made on this article. We’ve tried to keep away from among the rabbit gap dives now we have seen by some analysts on the values or ills of the sector shares. Our try right here tries to respect the eye spans of readers by posing these key questions solely.

We acknowledge there are numerous questions buyers are entitled to have solutions to that don’t actually emerge in earnings calls. We’ve learn earnings transcripts of those firms for 3 years for every quarter. Our conclusion: Little or no ft is held to the fireplace throughout Q&A. That’s comprehensible provided that analysts do must behave to protect entry.

We share these questions out of observations, not judgments. These last selections lie with Mr. Market.