bjdlzx

I assume most of my readers are accustomed to Western Midstream Companions LP (NYSE:WES). For others briefly, WES is a midstream operator with pure fuel gathering, working, and transporting as its main enterprise. Two different companies are oil and NGL transporting; and gathering and disposal of produced water. Please check with different sources for a extra detailed firm description.

Occidental Petroleum (OXY) owns ~49% of WES together with its restricted and basic companion stakes mixed and controls WES as a result of latter. For OXY, WES was part of the Anadarko acquisition in 2019. Michael Ure, previously with OXY, has been WES CEO because the acquisition. OXY can also be WES’s important buyer.

WES appears enticing with a ahead tax-deferred yield of ~10%, investment-grade credit standing, and sure capital appreciation over the subsequent 2-3 years. On this publish, we are going to examine this chance. All numbers, besides per share, are in thousands and thousands.

Chronology

The final decade of February was eventful for WES.

- On Feb 20, Reuters reported that OXY is exploring a sale of WES to slash its debt. Enterprise Merchandise (EPD), Williams (WMB), Kinder Morgan (KMI), and personal fairness are reportedly .

- In a while the identical day, WES issued a press release stating that

Western Midstream Companions, LP is conscious of latest information protection indicating that WES is working in the direction of a gross sales course of. WES has not launched a gross sales course of nor has it engaged bankers or different advisors with a view towards doing so. We’re conscious, as has been publicly said, that Occidental Petroleum Company (“Oxy”) has expressed curiosity in divesting belongings. We can not converse to the composition of the belongings Oxy might search to divest, and any questions concerning Oxy’s possession curiosity in WES needs to be directed to Oxy.

- On Feb 21, WES reported its This fall 2023 and full yr with an earnings name the subsequent day. Apart from the outcomes and forecast, WES made two necessary bulletins associated to 2024. Specifically, the corporate had executed agreements to promote $790M of non-core belongings, and its quarterly per share distribution might be elevated from $0.575 for This fall 2023 (payable in Q1 2024) to $0.875 for Q1 2024 (payable in Q2 2024). On Feb 22, the models jumped to $33.60 vs. $30.18 the day prior to this.

- After the fast run-up, Raymond James and Citi downgraded WES to impartial with a goal worth of $34. On the time of writing, WES is buying and selling at ~$35

Valuations

Typical MLP buyers are yield-seekers. However whereas the distribution jumped 52% in February, the models didn’t observe in sync and added solely ~15%. Buyers doubt that the introduced distribution is sustainable (Raymond James formulated it straight) and suspect {that a} leap in distributions is a ploy by OXY to pump WES models earlier than promoting the corporate.

Administration was not shy to point that WES was low cost even earlier than the distribution hike.

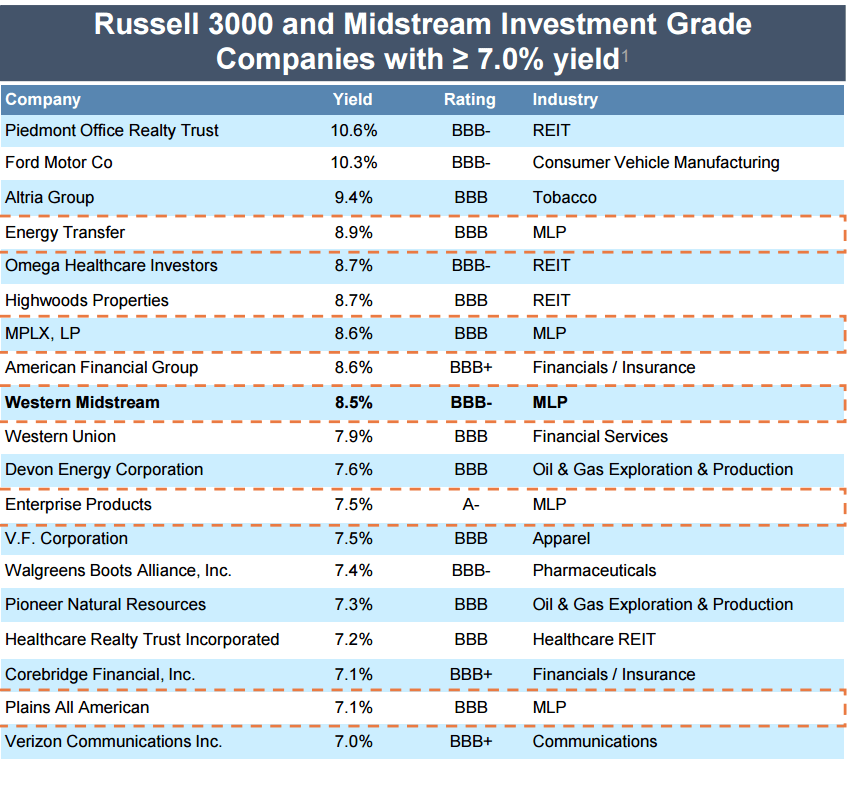

Firm

On the slide, WES is listed with its TTM distributions and inventory worth on 12/31/2023. With its new yield, on a ahead foundation, WES needs to be near the highest of the desk, buying and selling cheaper than different midstreams.

Allow us to verify the numbers crucial for WES.

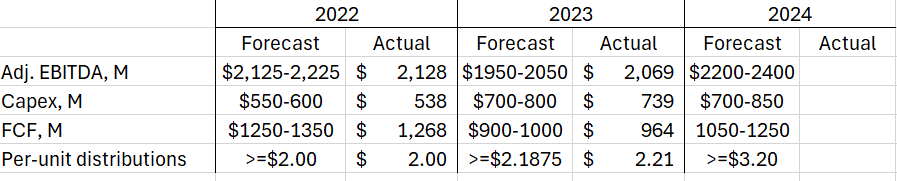

Creator, firm

In contrast to different midstream MLPs, WES emphasizes its FCF (as a substitute of distributable money) roughly equal to money stream from operations much less curiosity and all Capex, each progress and upkeep. WES is dedicated to returning all FCF to unitholders, principally by means of distributions. However during the last a number of years, the corporate additionally commonly and considerably purchased again its models.

WES raises its Base distributions at any time when FCF justifies it completely with none quarterly cyclicality. So a hike can occur each quarter (as in 2021) or solely in Q1 (as in 2022).

If some FCF stays left after Base distributions and buybacks, WES pays Enhanced distributions upon the yr’s finish as occurred in 2023 (together with Enhanced distributions for 2022, WES paid out $2.49 in 2023). Importantly, each forecasted and precise distributions within the firm’s supplies (and in my desk above) check with ONLY Base distributions.

The forecast of at the very least $3.20 in 2024 consists of $0.575 paid in Q1 (for This fall 2022) and at the very least $0.875 for every of the remaining three quarters. On a ahead foundation, WES is dedicated to at the very least $3.50 in Base distributions or at the very least a ten% ahead yield.

WES additionally forecasts ~3.0 leverage in the direction of the 2024 year-end. On Dec 31, 2023, WES had $7,088 in web debt. As soon as all asset gross sales are closed (most probably in Q2), the corporate will obtain $790 in money and its web debt will turn out to be ~$6,300. Even on the low finish of the EBITDA forecast, its leverage ratio will turn out to be ~$6,300/2200~2.9. EPD has an identical leverage ratio and A- credit standing. Whereas I’m removed from evaluating the 2 firms, it signifies that additional credit score upgrades could also be within the offing for WES.

To this point, it has not been mirrored in bonds. Rated BBB- WES bonds maturing in 2048 commerce at ~6.4-6.5% YTM, whereas ET bonds with BBB ranking and the identical maturity commerce at ~5.4% YTM.

From our first slide, WES was buying and selling at an 8.5% TTM yield on the finish of 2023. Assuming the identical yield on the finish of 2024, WES needs to be buying and selling at $3.20/8.5%~$38 even ignoring the progress in credit score rankings and potential charge cuts which will make dividend yield extra enticing. A yr from now, WES needs to be buying and selling at $3.50/8.5%~$41. The latter determine signifies an annual return of ~30% consisting of ~20% in capital appreciation and ~10% yield.

EBITDA valuations are much less optimistic. On the finish of 2023, the EV/EBITDA a number of was 8.8. The identical 8.8 a number of and $2,300 mid-point forecast for 2024 EBITDA produces an EV of 8.8*2300=$20,240. With the online debt of $6,300 and 389.6 models, it corresponds to the unit worth of (20240-6300)/389.6=$36. In different phrases, based mostly on EBITDA we are able to anticipate little or no capital appreciation and our return will consist primarily of yield.

WES and OXY

The present unit worth reveals that the market considers yield a much less dependable indicator than EBITDA. And this isn’t stunning as yield is just a by-product of money flows.

Revisiting our final desk, the 2024 FCF forecast is $1050-1250 vs the $900-1000 forecast and $964 precise for 2023. It corresponds to solely 9-30% progress of FCF vs 52% progress in distributions.

At the very least $3.20 in 2024 Base distributions would require 3.20*389.6~$1250 in FCF. This is the same as the highest finish of the 2024 forecast and reveals that the final distribution hike was fairly aggressive and should have accomplished in preparations for the sale. Does it imply that the brand new distributions will not be sustainable?

My reply is unfavorable. For 2024, the danger of slashing distributions is low. Even when FCF is inadequate to cowl distributions, the corporate could have money available and a leverage of ~3.0 which may be very low for a BBB- firm. Borrowing will present more money if wanted.

I additionally assume, and that is purely speculative, that the corporate plans to realize the highest finish of its FCF forecast. The 2024 FCF forecast vary is twice greater than in 2022 or 2023 ($200 vs $100). That is unlikely unintentional. In Q2 2024, WES plans to fee its new pure fuel plant Mentone III within the Delaware Basin. The manufacturing of this plant is already offered out and money ought to begin flowing in instantly upon commissioning. The elevated forecast vary, for my part, displays the dangers related to this new huge capital mission.

Early in 2025, the corporate plans to fee one other pure fuel plant (North Loving) within the Delaware Basin. It means one other bump in money flows plus diminished Capex. On the final earnings name, Michael Ure talked about that when it comes to Capex, 2025 might seem like 2022 with $200M much less spent. So even, if WES has a slight deficit of FCF in contrast with distributions in 2024, they’re more likely to catch up in 2025 and past.

Nonetheless, the aggressiveness of the hike implies OXY involvement. Assuming OXY plans to promote WES later in 2024, it needs to be enthusiastic about growing WES valuations and pumping as a lot money as potential out of WES earlier than the sale.

What’s the potential sale worth of WES based mostly on related comps?

- WES’s asset sale in early 2024 was accomplished at 9.6x EV/EBITDA a number of.

- Late in 2023, Vitality Switch closed its Crestwood (CEQP) acquisition for about 9.6x a number of of the projected 2023 EV/EBITDA. Whereas it’s in all probability the most effective comp, Crestwood was a lot smaller and had a junk credit standing vs funding grade for WES.

Thus in acquisition, WES is anticipated to fetch at the very least a 9.6x a number of of its projected mid-point 2024 EBITDA or 9.6×2,300 ~ $22,100.

The latter determine interprets right into a share worth of (22,100-6,300)/389.6~$40 however could be barely larger.

Conclusion

If the sale of WES happens in the direction of the tip of 2024, buyers are more likely to pocket ~$5 in capital appreciation plus ~$2.60 in distributions for a complete of $7.60 or $7.60/35 ~ 22% over the 9 months.

Suppose the sale of WES doesn’t happen. In that case, buyers will hold receiving a ten% yield plus doubtless capital appreciation in a yr when WES will hike its distribution once more as a result of coming commissioning of the North Loving plant.

Each of those situations ought to hold buyers glad besides, maybe, for previous WES holders who will face vital taxes in case of acquisition for money.

There are many dangers in each situations. The obvious are materials issues with the commissioning of Mentone III and North Loving vegetation, a decrease acquisition worth for WES, operational dangers, and so forth. Nonetheless taking a place in WES appears enticing to me.