Prykhodov

What’s Alphabet’s enterprise mannequin?

Right here is the very fact, Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) has 77% of complete income coming from the digital promoting enterprise, and 57% of complete income comes straight from the advertisements on Google Search.

Principally, Google has 91.37% market share within the world search market, and after we search the net for no matter purpose, we see the advertisements, and we click on on these advertisements. Alphabet will get paid for every click on, and for every advert that we see. That is Alphabet’s enterprise mannequin – digital advertisements.

Right here is breakdown of Alphabet’s gross sales by section:

Alphabet 10K

However extra importantly, Alphabet’s income come straight from the advertisements – the Google Providers section. In 2022 all different segments had losses, whereas in 2024 Google Cloud turned worthwhile, however accounting for lower than 2% of Google Providers income. Thus, Alphabet’s profitability is completely reliant on digital advertisements.

Alphabet 10K

Alphabet really warns of 1) slower development and a pair of) decrease margins within the 2023 10K report, the Administration Dialogue part, part “Trends in Our Business and Financial Effect”.

Customers’ behaviors and promoting proceed to shift on-line because the digital economic system evolves. The persevering with evolution of the web world has contributed to the expansion of our enterprise and our revenues since inception. We anticipate that this evolution will proceed to learn our enterprise and our revenues, though at a slower tempo than we have now skilled traditionally, particularly, after the outsized development in our promoting revenues in the course of the COVID-19 pandemic.

Customers proceed to entry our services and products utilizing various gadgets and modalities (smartphones, wearables, linked TVs, and good dwelling gadgets), which permits for brand spanking new promoting codecs which will profit our revenues however adversely have an effect on our margins. We anticipate these traits to proceed to have an effect on our revenues and put stress on our margins.

Right here is the issue, desktop search has very excessive margins, however most individuals at the moment are utilizing different modalities to go looking, which have decrease margins. As well as, Alphabet believes that the post-Covid development is unsustainable.

However right here is the larger drawback

The massive drawback with Google Search is the “annoying” advertisements – however that is how Alphabet makes cash. The latest innovation with the ChatGPT is probably an existential risk to the Alphabet’s ad-based enterprise mannequin.

Here’s what the founding father of OpenAI (ChatGPT) Sam Altman thinks concerning the advertisements:

I type of hate advertisements simply as an aesthetic selection. I feel advertisements wanted to occur on the web for a bunch of causes, to get it going, nevertheless it’s a momentary trade. The world is richer now. I like that individuals pay for ChatGPT and know that the solutions they’re getting are usually not influenced by advertisers. I’m positive there’s an advert unit that is smart for LLMs, and I’m positive there’s a technique to take part within the transaction stream in an unbiased method that’s okay to do, nevertheless it’s additionally straightforward to consider the dystopic visions of the long run the place you ask ChatGPT one thing and it says, “Oh, you should think about buying this product,” or, “You should think about going here for your vacation,” or no matter.”

ChatGPT is actually a chatbot – you ask a query and also you get a solution. And that might be a brand new method of trying to find info.

However right here is the deal – there aren’t any advertisements in ChatGPT. It looks like individuals are paying for the subscription to entry superior variations of ChatGPT, or it is free – with no advertisements.

Sam Altman doesn’t need to compete with Google Search, or to enhance Google Search, Altman needs to create a brand new method of trying to find info – advertisements free.

So, that is primarily the Google Search killer, not straight away, however ultimately. Extra exactly, that is the Google Search enterprise mannequin killer. Google can simply incorporate LLM into Search, however the issue is it can’t embrace the advertisements.

Alphabet should adapt or die

Thus, clearly, Alphabet has to adapt, it has to create a brand new enterprise mannequin. Apparently, Alphabet plans to charge subscription for the superior AI Search, however apparently it nonetheless plans to ship the advertisements – even for the premium model. That is not going to work if the rivals provide ad-free AI search.

Let’s take a look at the primary competitor in Search – Microsoft (MSFT), which at the moment has a 3% market share in search with Bing. Microsoft invested in OpenAI and included ChatGPT in Search because the Copilot.

Microsoft sells productiveness instruments, and it will probably provide Copilot as one of many instruments. It is a new method of incorporating Search (as info gathering) with the analytics (Excel spreadsheets) and report preparation (MS Phrase). The identical precept can apply to any workload – akin to creativity and others. So, Search turns into solely the primary half – info gathering. Alphabet can attempt to copy Microsoft’s all-inclusive productiveness subscription mannequin, however it is going to be very pricey.

The purpose is Alphabet has to adapt the enterprise mannequin to be much less reliant on advertisements and extra on subscriptions. Or, alternatively attempt to compete with the Cloud providers, taking a word from Amazon (AMZN), whose solely development driver now’s AWS.

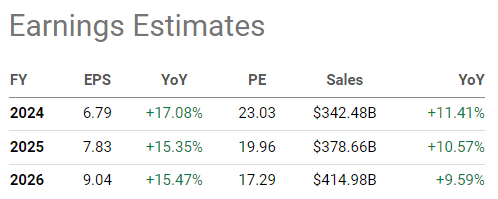

Present metrics

Alphabet is going through a critical risk and should reorganize. The present income/earnings estimates for Alphabet do not incorporate the risk from ChatGPT to Google Search advert revenues.

Even so, Alphabet is predicted to have a progressively declining development charge in revenues over the subsequent 3 years, to lower than 10% in 2026. That is according to the expansion warning within the 10K report. Earnings are anticipated to develop round 15%. However this estimate doesn’t think about the revenue margin warning from the 10K assertion (because of change in modality).

Searching for Alpha

Alphabet is at the moment overvalued with the ttm PE ratio at 26 and ttm PS ratio at 6.37, nevertheless it’s not a bubble. The ahead PE ratio is at 23, which means that earnings development expectations are usually not exuberant – confirming the 15% earnings development estimates. Meta (META) might be akin to Alphabet, as a result of it has just about all income from digital advertisements, though the enterprise mannequin could be very totally different. Meta is costlier than Alphabet based mostly on the ttm PE at 34, and barely costlier based mostly on ahead PE at 26.

Searching for Alpha

Based mostly on the present metrics, each Alphabet and Meta are overvalued, however Alphabet is cheaper than Meta – which alerts that the market is pricing slower development, and it is really destructive for Alphabet.

Implications

Alphabet is going through a critical risk to its important enterprise mannequin – Google Search. Microsoft is innovating the Search enterprise, making ChatGPT (Copilot) a part of the productiveness instruments. Thus, the Search half is bundled with different productiveness instruments and offered as a subscription.

Alphabet acknowledges this risk and it is engaged on the adjustment (Gemini). Nevertheless, within the meantime, the danger of holding Alphabet inventory is simply too excessive. Thus, my ranking for Alphabet is a Promote.

The chance to this bearish thesis is as follows:

- The AI rules, just like the EU AI Act, might cease the progress of Gen AI, which may gain advantage the normal ad-based Search mannequin, though this could not be a constructive for the broad tech sector, and thus Alphabet inventory.

- Clearly, Alphabet might adapt and alter rapidly to the brand new surroundings and transition to the brand new enterprise mannequin with none vital destructive impact on earnings.