no_limit_pictures/E+ by way of Getty Pictures

In at present’s market, it may be troublesome to go looking via the noise surrounding “growth” corporations. Practically each “growth” concept you examine at present is predicated round synthetic intelligence, which is an area presently fraught with uncertainty and hypothesis. Nevertheless, there are different areas to look to search out rising corporations, and wanting within the medical know-how house, I got here throughout Encourage Medical Techniques (NYSE:INSP), a quickly rising, early-stage firm bordering on profitability.

I imagine Encourage’s inventory is a long-term ‘buy’ for varied basic causes, and I imagine there are some upcoming catalysts that may push the inventory greater within the close to time period. I’ll define who Encourage is, how they function, and why I imagine the inventory isn’t being priced accurately by the market.

What’s Encourage Medical Techniques?

Encourage Medical Techniques is a medical know-how firm specializing in a machine that improves the lives of these with Obstructive Sleep Apnea. Encourage’s machine stimulates the hypoglossal nerve, shifting the tongue out of the best way to permit the affected person to breathe.

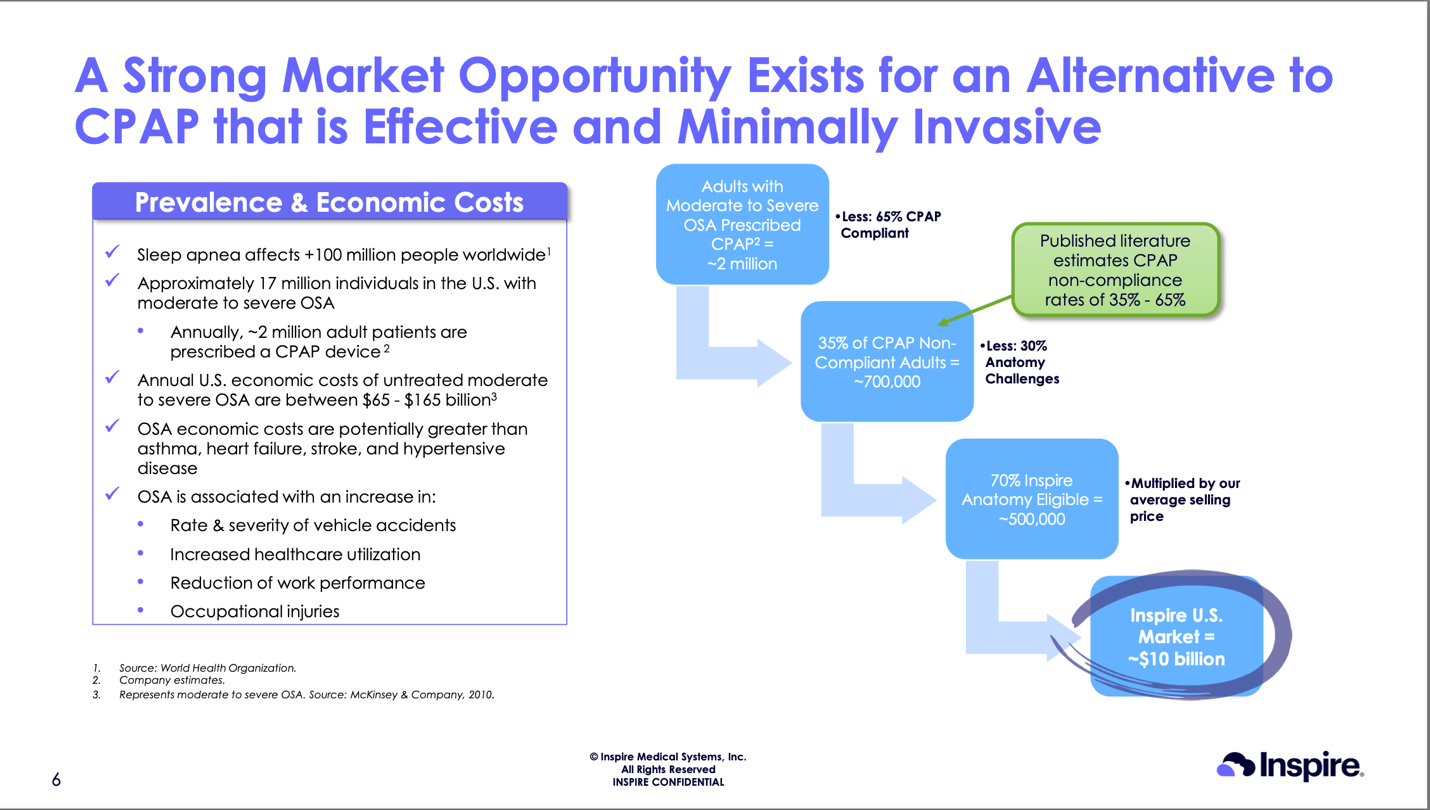

Obstructive Sleep Apnea, or OSA, is outlined as a situation the place the affected person’s respiratory is interrupted for not less than ten seconds throughout sleep, 5 or extra occasions per hour. OSA is a debilitating situation that, in line with Encourage’s most up-to-date firm presentation, doubles the danger of stroke and sudden cardiac demise, and will increase the danger for cardiovascular mortality by 5 occasions. Based on Prime-ranked Hospital within the Nation the Mayo Clinic, most people with OSA are obese, male, and have a household historical past of OSA. Encourage states that sleep apnea impacts over 100 million folks all through the world, together with about 17 million within the U.S. which have what’s outlined as moderate-to-severe OSA. The prices of untreated OSA might be as a lot as $165 billion, which, in line with Encourage, is doubtlessly greater than the financial prices of bronchial asthma, coronary heart failure, stroke, and hypertensive illness.

Encourage Firm Presentation – IR

The Encourage system is implanted in sufferers via a comparatively easy and easy process that lasts about 60-90 minutes. Two small incisions are made, one under the jaw and one other within the higher proper chest. The primary incision permits for placement of the stimulation lead round a part of the hypoglossal nerve, which can finally stimulate the tongue to maneuver ahead, clearing the affected person’s airway and permitting them to breathe. The chest incision permits for placement of the neurostimulator and the strain sensing lead. The battery for the Encourage system is housed within the neurostimulator and lasts round 11 years, so because the firm remains to be in its early phases, neurostimulator alternative procedures are at a minimal. In any case three components of the system are implanted, the system is examined and the incisions are closed. (All the process data could be discovered on Encourage’s web site and their 10-K).

After therapeutic for a few month, sufferers obtain their distant controls for his or her Encourage system from their physician. Though, in line with Encourage’s 10-Okay, the manufacturing facility settings are used for many sufferers, the system could be custom-made to ship totally different ranges of stimulation for every affected person. Sufferers will merely activate their machine with their remotes every evening, and the system even has a 30-minute delay to permit sufferers to go to sleep naturally. Encourage VI, which is presently being conceived, might have sleep detection capabilities, theoretically eradicating the necessity to begin the system with the distant.

As you’ll be able to see by their company presentation, Encourage believes there’s a $10 billion annual alternative for them to deal with sufferers with OSA. Present remedy for OSA is primarily steady optimistic airway strain, or CPAP. CPAP machines are thought of the very best remedy for OSA, producing optimistic outcomes when sufferers are compliant. Sadly, CPAP machines are cumbersome, uncomfortable, and solely 35-65% of sufferers prescribed CPAP machines truly use them as prescribed. This non-compliance leaves a query that Encourage has been capable of reply: Is there a greater manner?

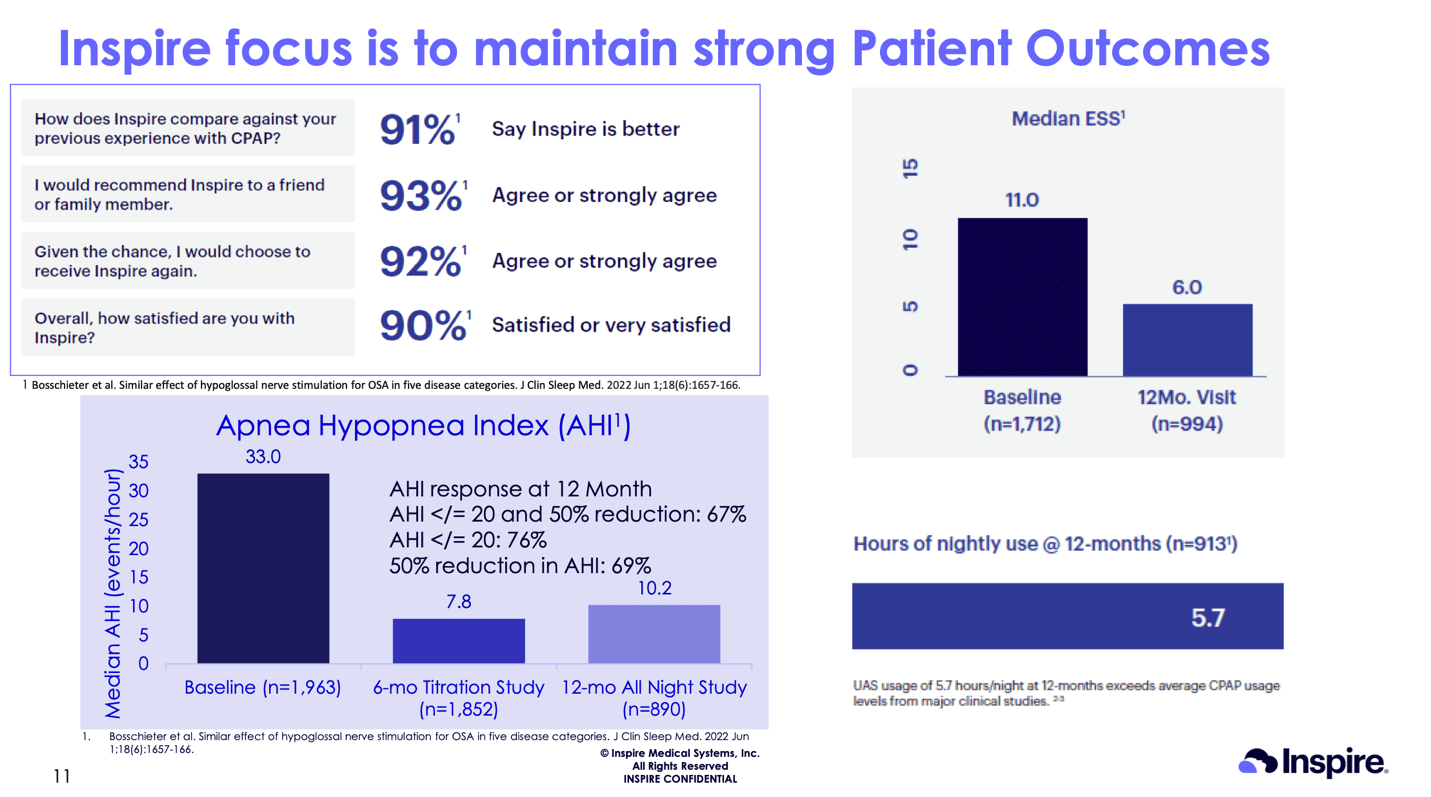

Encourage sufferers report outcomes much like CPAP, in line with the corporate, whereas reporting that 91% of sufferers say their expertise with Encourage is healthier than their expertise with CPAP.

Encourage IR

Encourage Firm Overview

An awesome resolution for an costly and life-altering downside is nothing with out the right administration and philosophy driving the corporate ahead. Encourage is run by President and CEO Tim Herbert. Based on a 2023 article from Investor’s Enterprise Day by day, Herbert has been with Encourage because the starting, initially engaged on the know-how when it was being developed at Medtronic. Based on the identical article, he labored for the Medtronic workforce growing Encourage’s remedy since 1998. Medtronic was about to scrap their plans for growing the know-how, however as a substitute, Herbert took the reins, and the corporate was spun off in 2007.

Encourage has come a good distance since then, lately surpassing the 60,000th implant milestone in 2023. Revenues have grown from $16.4 million in 2016 to $624.8 million in 2023. The corporate, as of March 30, 2024, has a market capitalization of $6.35 billion. Encourage went public in Could of 2018, for an IPO value of $16 per share. The corporate closed that day at $24.98 and is presently buying and selling at round $214. In 2022, the corporate provided an extra 1,000,000 shares of widespread inventory to the general public markets and used the proceeds to repay all their excellent debt.

Encourage, underneath Herbert’s management, has turn into a compelling inventory to personal and a real ‘growth’ firm, regularly rising revenues at a speedy price whereas protecting prices down considerably. The corporate lately reported a worthwhile 4Q23 and initiatives a worthwhile second half of 2024. The corporate’s enterprise mannequin is easy: deal with the affected person and their outcomes. Herbert constantly talks about specializing in affected person outcomes because the primary precedence, which can enable the corporate to develop and develop at a wholesome price.

Encourage generates their income from the sale and supply of their system, primarily in the US. Whereas worldwide gross sales are rising, the principle driver of progress at present is elevated U.S. market publicity. The corporate has 1,180 ‘centers’ offering the Encourage implant to their sufferers. These facilities (together with hospitals and outpatient surgical procedure facilities) are important to the expansion of the corporate, as they’re constantly including new facilities and ‘maturing’ facilities they’ve already added up to now few years. Income progress primarily comes from ‘maturing’ these facilities, which principally means getting the present facilities to implant extra programs into extra sufferers. Consider it as “same-store sales” versus gross sales generated from newly opened shops, to steal some retail terminology.

Encourage has persistently operated with a excessive gross margin, as the principle “cost of goods sold” merchandise is the manufacturing expense for the Encourage system. The machine isn’t very massive, barely bigger than 1 / 4, and the distant given to sufferers to activate the system each evening doesn’t require important manufacturing bills. Encourage’s gross margin in 2023 was 84.5%, a rise from 2022.

The principle prices for Encourage come from locations you’d count on in a quickly rising medical know-how firm: Analysis & Improvement Bills (R&D) and Promoting, Common and Administrative Expense (SG&A).

R&D bills for Encourage elevated 69.8% in 2023 from the earlier 12 months, totaling simply over $116 million. The numerous improve in R&D comes from the event of the subsequent era system, Encourage V, in addition to the event of the SleepSync platform, which drastically enhances the affected person and doctor expertise with the Encourage system.

SG&A bills elevated 40.9% in 2023 from 2022 to $452 million. Naturally, an organization like Encourage not solely wants to advertise their system to sufferers and suppliers, however it additionally wants to teach sufferers and practice suppliers to extend gross sales and acceptance of the remedy as an answer for OSA. The corporate launched a brand new web site in December of 2023 (Inspire Sleep Apnea Innovation – Obstructive Sleep Apnea Treatment) which is designed to raised educate potential sufferers. As for as suppliers go, Encourage not solely wants to teach sleep clinicians, however additionally they want to coach Ear, Nostril, and Throat docs (ENT) who truly implant the system into sufferers.

ENT coaching is significant to Encourage’s improvement and essential to how shortly the remedy can turn into extra broadly accepted. At the moment, a few of Encourage’s most “productive” ENTs are inside 2 to three years out of fellowship, in line with UBS. Rightly so, Encourage is specializing in these graduating and early-career ENTs to attempt to get them to make use of Encourage’s system for extra of their sufferers. As the corporate continues to teach, practice, and acquire acceptance with extra ENTs, the process ought to turn into extra broadly used, which ought to result in a gentle improve in gross sales.

So far as Encourage’s stability sheet, it’s atypical of a quickly rising firm. As talked about earlier, the corporate used their 2022 secondary providing to repay their excellent debt. Whole liabilities complete solely about $104 million. Present property embrace over $185 million of money, in addition to over $274 million of short-term investments, primarily short-term U.S. Treasuries. The corporate has a pristine stability sheet which ought to assist it climate any turbulence it faces.

Potential Challenges and Catalysts

Talking of turbulence, a fast have a look at INSP’s chart would present the inventory has fallen drastically from its high-water mark of $330 in July of 2023. The first trigger for this fall has been the hype and prominence of GLP-1 medicines. GLP-1 medicines are used for diabetes and weight reduction. GLP-1 medicines embrace Ozempic, Trulicity, and Mounjaro. GLP-1 medicines have been seen as miracle medicine for these attempting to drop some weight, however they’re additionally believed to have potential advantages for a lot of different folks, together with these with OSA. Merely put, GLP-1s have been touted as potential remedies for these affected by OSA, which, if true, can be unhealthy information for Encourage.

The true information reveals, nevertheless, that proof to help this declare is restricted. Encourage’s administration has even gone as far as to say GLP-1s might INCREASE Encourage’s affected person base, as Encourage can’t deal with sufferers with a BMI (physique mass index) over 40. Serving to folks with BMIs over 40 who are suffering from OSA decrease that quantity will help them qualify for the Encourage process after they beforehand would’ve been ineligible (offered their kind of OSA is tongue-based collapse and never full concentric collapse). Many individuals with very excessive BMIs have full concentric collapse, which Encourage can’t deal with in any case. These sufferers would most definitely profit from GLP-1s, however it is a separate affected person group than these that may obtain Encourage.

A key upcoming occasion for Encourage, and plenty of different corporations, is the discharge of the SURMOUNT-OSA trial from Eli Lilly (LLY). The outcomes of this trial ought to be launched between the tip of March and Could, and can deal with how tirzepatide, Eli Lilly’s GLP-1 remedy, impacts these with OSA, particularly those that can’t or is not going to tolerate PAP remedy. JP Morgan’s analysts imagine that this trial will present that GLP-1s don’t match the efficacy of Encourage’s remedy, and extra sufferers are more likely to fall into Encourage’s affected person base than out of it, primarily because of the decreasing of sufferers’ BMIs. Ought to this be true, the latest weak point in Encourage’s inventory value might current a really fascinating shopping for alternative.

Encourage does have some competitors on this house, though not who chances are you’ll suppose. Encourage particularly states they don’t imagine they immediately compete with PAP units, as Encourage is simply really useful for many who can’t or is not going to tolerate PAP remedies. Encourage is the ONLY neurostimulation remedy for moderate-to-severe OSA authorized by the FDA within the US. In different nations nevertheless, corporations like LivaNova and Nyxoah are conducting trials of their units. Nyxoah is conducting trials to doubtlessly turn into authorized by the FDA for treating sufferers within the US, however their know-how is totally different, and the corporate remains to be very small with 2023 income totaling 4.3 million euros. I’m not dismissing this doubtlessly disruptive competitor due to their measurement, however in a healthcare business just like the US, crucial a part of changing into a broadly accepted remedy is physician schooling and coaching, a spot Encourage is specializing in closely to fight this potential competitor.

Valuation

As for valuation, Encourage might look to many like an costly inventory, presently buying and selling at over 10-times 2023 gross sales. Usually, a inventory at 10x gross sales can be deemed fully-priced in my eyes and I might promptly flip in the direction of extra “affordable” and “reasonably-priced” corporations. Nevertheless, Encourage is an organization whose progress and up to date profitability can greater than justify buying and selling at over 10x gross sales. Additionally, the market has proven, earlier than GLP-1 disruption, the willingness to place a good greater a number of on the inventory.

Encourage’s income has grown from $28.6 million in 2017 to $624.8 million in 2023, a determine representing a 67% CAGR (compound annual progress price). Income progress is slowing, with Encourage’s final two quarters displaying income progress of (solely) 40% year-over-year. In comparison with the primary two income progress figures of 2023 (Q1 displaying 84% and Q2 displaying 65%), the corporate could be forgiven in my eyes for not persevering with to almost double their gross sales yearly. Encourage initiatives income of $775 million to $785 million in 2024, which might equate to 24% – 26% progress over 2023’s determine. This moderation in progress has been priced into the inventory since July together with the troubles from GLP-1s. Additionally, as many corporations do, Encourage could also be setting the bar relatively low for themselves, working underneath the “under-promise, over-deliver” philosophy.

Whereas Encourage’s income progress begins to reasonable, the actual story turns to their profitability metrics. Gross margin continues to extend with the corporate posting a whopping 84.5% GM in 2023. Q423 was the primary quarter the corporate reported an working revenue, which is a significant accomplishment and can’t be ignored. The corporate is also projecting profitability in 2H24, even with a reasonable income progress projection in comparison with prior years.

Encourage is a lean firm with controllable bills and important working leverage. Their COGS (cost-of-goods-sold) are minimal, with the machine being comparatively easy and cheap to fabricate. As talked about beforehand, Encourage’s most important prices are associated to R&D and promoting prices, areas that present for future progress relatively than present sustainability. This reveals the energy of Encourage’s Revenue assertion. If Encourage determined they needed to be worthwhile tomorrow, they might do it. They may reduce gross sales consultant positions and cut back R&D spending and “turn on” the profitability button of the group. They don’t have any debt to pay or collectors to report back to, solely their shareholders.

Clearly, this excessive instance is unrealistic, as the corporate should proceed to develop their system to maintain it forward of rivals, and slashing gross sales representatives would stunt progress instantly. The purpose of the train is to indicate that Encourage is working from a place of energy relatively than merely attempting to maintain itself afloat. An organization working from a place of energy deserves a premium valuation, particularly one persevering with to develop gross sales whereas rising profitability.

The three-year common P/S ratio within the Medical Tools business is 5.2x. If we take Encourage’s complete finish market estimate of $10 billion (from the sooner presentation picture) and halve it (to offer us a margin of security), future annual revenues could also be someplace round $5 billion per 12 months. $5 billion of annual income occasions the 3-year common P/S ratio for the business equals a $26 billion valuation for Encourage. $26 billion divided by the quantity of excellent shares on Encourage’s 2023 Annual Report offers us a valuation of round $879 per share.

There are a few issues to consider with this valuation, however I imagine it reveals a tough estimate of what Encourage is price. First, there is no such thing as a concept as to when Encourage would attain $5 billion in annual income or if their complete market alternative estimate of $10 billion is right. If these estimates show incorrect or take too lengthy to achieve, the corporate would virtually definitely be price lower than that valuation. Nevertheless, if the corporate can attain their estimate of $10 billion or in the event that they exceed the typical P/S ratio of the business (by reaching a higher-than-average degree of profitability and progress, for instance), the corporate might be price greater than the practically $900 per share estimate at which I arrived. I may also acknowledge that this estimate is a long-term price-per-share estimate, not a 12-month value goal like most analysts undertaking. This estimate can be based mostly on a a lot less-detailed valuation course of than another buyers might use to investigate corporations, however to me, it reveals Encourage’s potential to develop into a really invaluable firm. I imagine the long-term view is suitable for this rising firm, as a short-term view might not totally admire the patient-centered, regular progress strategy. Too many occasions, corporations try to develop too quick and sacrifice buyer satisfaction and product high quality for higher quarterly earnings and enticing headlines.

Funding Thesis and Facets to Think about

I imagine Encourage inventory is a purchase at this degree, and any weak point ought to be purchased. Encourage’s inventory may be very weak to GLP-1 information in at present’s market setting, which may present nice shopping for alternatives. Encourage’s inventory was additionally pushed down after the 2023 Q3 earnings report when the corporate introduced that they had some prior authorization points with insurance coverage corporations. The inventory was severely punished by this information, although the corporate introduced they have been engaged on correcting the problem and had seen success of their decision of this difficulty. This was an overblown concern, as evidenced by the inventory’s fast restoration from the 52-week low of $123.27. The corporate has shortly mounted the problem and now, over 4 months later, the prior authorization difficulty is a forgotten occasion. This, together with the inventory’s response to GLP-1 information, is proof that the inventory is weak to massive, typically unjustified, strikes.

The inventory has comparatively low quantity in comparison with bigger and extra widespread corporations. This will likely trigger an investor to wish a stronger abdomen when weathering a few of the volatility within the inventory. The inventory is liable to bigger strikes than regular equities, so a powerful conviction is required when the inventory dives down, and humility is required when the inventory soars greater.

One other potential funding alternative for Encourage is the potential to be an acquisition goal for a bigger firm. Encourage is a fast-growing firm with principally no debt, a confirmed know-how, and competent administration, which makes it a really enticing goal for a bigger medical firm. With a market capitalization of round $6 billion, it might not be far-fetched to suppose a bigger firm might come alongside and scoop them up. It’s doubtless, nevertheless, that CEO Herbert understands this and would demand a big premium for the acquisition of his firm, particularly one he has actually constructed from the start. I might think about he would additionally wish to stay in cost as effectively, which might be a optimistic or a detrimental for the purchaser, relying on how a lot management they might need over the corporate.

Monitoring my funding thesis for Encourage will probably be important, as many alternative components can affect Encourage’s future prospects. Corporations like Nyxoah might acquire FDA approval and will probably acquire market share. GLP-1 medicines might show to be extra useful for OSA victims than I’m projecting. And clearly, with all corporations within the healthcare business, potential detrimental affected person outcomes or product recollects might sew mistrust within the Encourage implant with would-be sufferers or result in lawsuits. All of those components have to be thought of and continually evaluated and studied.

At any price, I count on Encourage to be ready for these potential challenges, in addition to others. Their patient-first strategy ought to maintain affected person outcomes at an particularly optimistic degree. The fixed improvement and enchancment of their know-how, coupled with constant and protracted affected person and physician schooling, ought to maintain them forward of rivals and solidify the market share for the Encourage machine. I additionally count on the corporate to stay financially prudent, so long as Tim Herbert is on the helm.

Conclusion

After reviewing the basics of Encourage, potential occasions that may affect the corporate (just like the SURMOUNT-OSA trial), and analyzing its future prospects, Encourage is a uncommon progress inventory with just about no debt, latest profitability, and a really manageable price construction. Encourage’s most important concern is the outcomes of their sufferers, which permits them to develop at a wholesome and sustainable tempo relatively than overreaching or reducing corners. The principle headwinds going through the corporate and the inventory are GLP-1 medicines and a slowing progress price, each of that are overblown for my part. GLP-1 medicines will most definitely show not practically as useful to OSA victims as many imagine, and the slowing progress price is sensible when the corporate is coming off such a powerful and unsustainable progress price within the first place. Additionally, GLP-1 medicines usually tend to improve the variety of Encourage sufferers than lower it, which is the other impact that many expect. The corporate is well-run and has their priorities in the best place, specializing in educating docs and sufferers as to why their system is appropriate for many who can’t or is not going to tolerate CPAP.

Although the corporate is buying and selling at over 10x 2023 Gross sales, Encourage is probably going nonetheless undervalued based mostly available on the market alternative in treating OSA and its glorious monetary place. Latest weak point has offered a doubtlessly enticing entry level, so buyers within the house might wish to discover this additional.

We want to thank Tyler Ormond for this piece.