Eetum/iStock through Getty Photographs

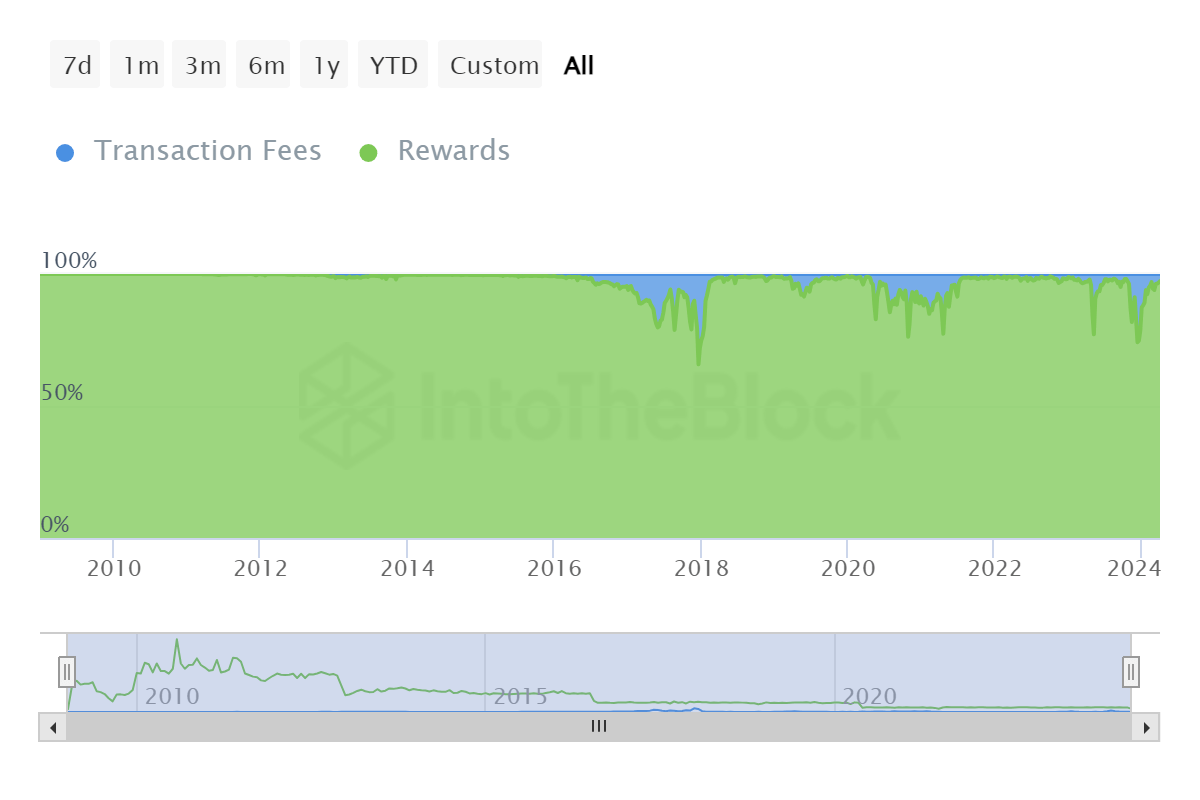

After I last covered Marathon Digital (NASDAQ:MARA) for Searching for Alpha in December, the Bitcoin (BTC-USD) community was experiencing a dramatic surge in transaction charges as a proportion of whole block reward. The potential long run stickiness of transaction charges can be vastly helpful to BTC miners like Marathon as a result of it might decrease the affect of emission halvings – the following of which is roughly two weeks away as of article submission.

Miner reward distribution (IntoTheBlock)

Within the months since that article, transaction charges have didn’t reside as much as the thrill from This fall 2023. Whereas we may theoretically see transaction charges transfer again up sooner or later, I believe the extra BTC that flows into the spot ETFs the much less seemingly that final result could finally be. Thus, I am offering an replace. We’ll take a look at the corporate’s ahead steerage from its latest report, Q1-24 manufacturing knowledge, and assess whether or not or not MARA is a basic purchase at a $5 billion valuation.

This fall-23 Efficiency

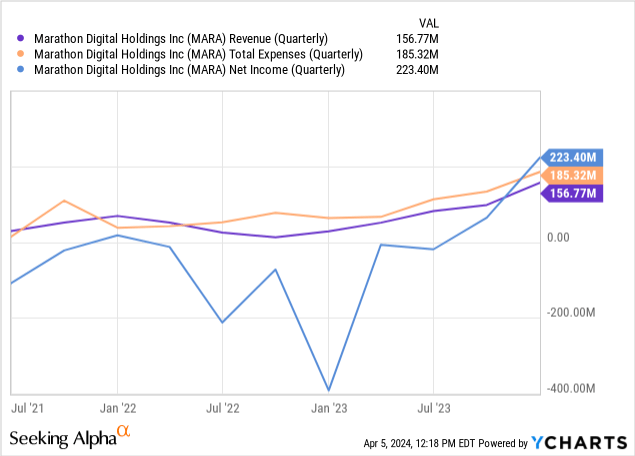

Within the final quarter for 2023, Marathon Digital recorded $156.8 million in quarterly income versus $185.3 million in whole bills. What seemingly jumps off the web page is the monstrous constructive quarterly internet revenue determine of over $200 million. How may this be with bills exceeding gross sales? CFO Salman Khan on the final convention name:

Had the corporate not early adopted the brand new FASB fair-value accounting guidelines, our internet revenue attributable to widespread stockholders for the fourth quarter of 2023 would have been a internet lack of $5 million or lack of $0.02 per diluted share. And internet revenue of $33 million or $0.17 per diluted share for the 12 months ended December thirty first, 2023.

For the complete 12 months, MARA produced 12,853 BTC and grew its Bitcoin treasury stack by 2,942 BTC 12 months over 12 months. From a price of manufacturing standpoint, there was a notable transfer increased in MARA’s breakeven worth for This fall based mostly alone estimates. However trailing twelve months, the corporate’s manufacturing prices have been really significantly better than most different gamers within the trade.

| Q1-23 | Q2-23 | Q3-23 | This fall-23 | TTM | |

|---|---|---|---|---|---|

| Value of Revenues | $33,400,000 | $55,200,000 | $59,600,000 | $75,100,000 | $223,300,000 |

| Adjusted Opex | $21,600,000 | $42,800,000 | $53,900,000 | $110,300,000 | $228,600,000 |

| BTC Mined | 2,195 | 2,926 | 3,490 | 4,242 | 12,853 |

| Breakeven Worth | $25,057 | $33,493 | $32,521 | $43,706 | $35,159 |

Sources: Searching for Alpha, Marathon Digital, Creator’s calculations

I do need to point out that these breakeven figures should not meant to be taken as gospel, they’re merely an exterior estimate that may be equally utilized to the entire firms within the house to gauge effectivity amongst friends over time. If we strip out these FASB accounting modifications and construct an actual time breakeven Bitcoin worth for MARA that mixes value of income, SG&A, and Depreciation/Amortization after which divide that determine by the quantity of BTC the corporate produces every quarter, we get a $43.7k breakeven BTC worth for Marathon Digital in This fall and a $35.1k BTC worth for the complete 12 months 2023.

Present State and Ahead Steerage

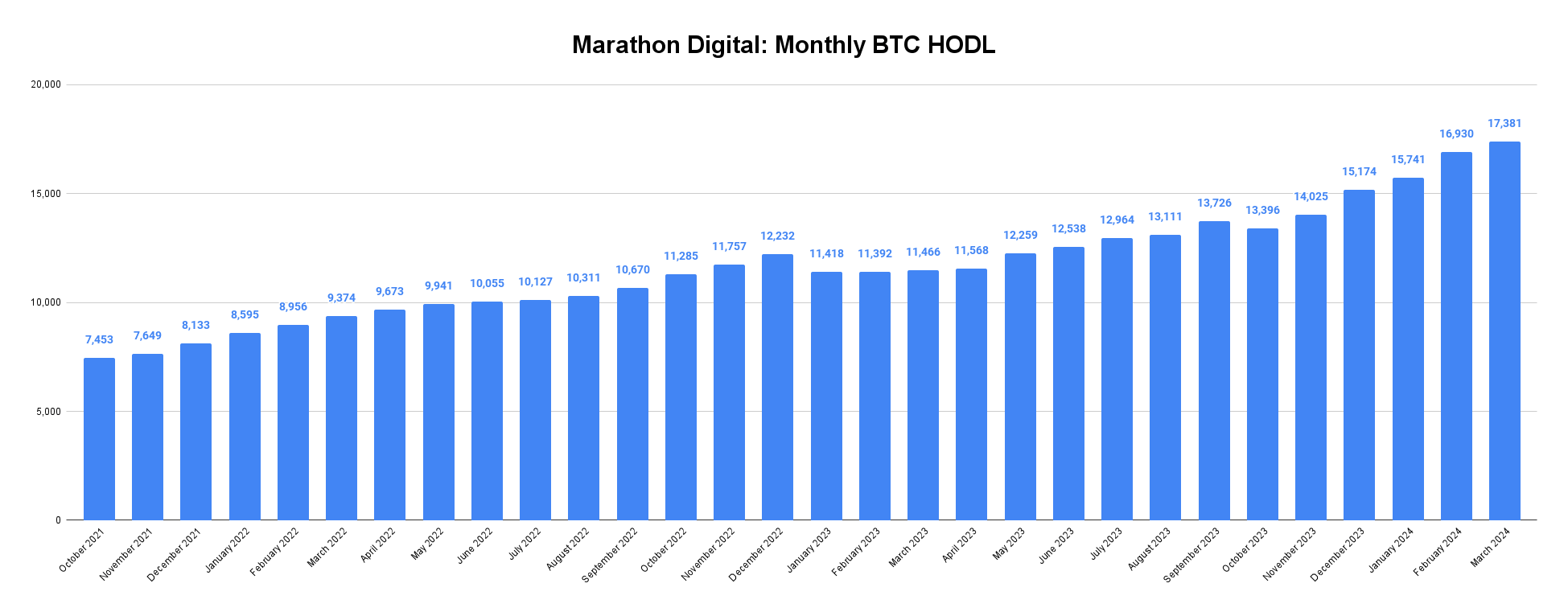

Creator’s chart (Marathon Digital)

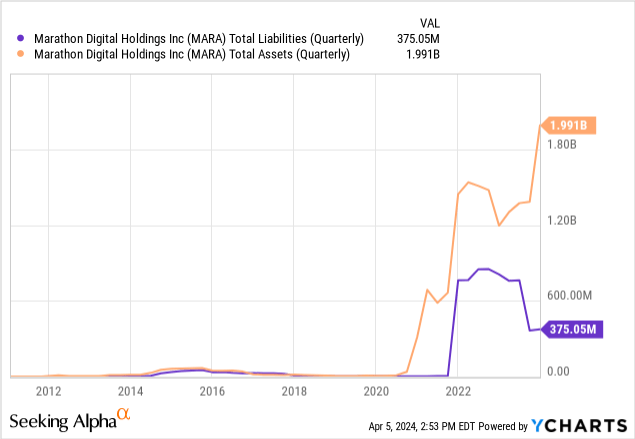

As of finish of March, Marathon Digital has 17,381 BTC on the stability sheet. At a coin worth of $68k, MARA has almost $1.2 billion in liquidity from BTC alone. The corporate is in a significantly better monetary place than it was a 12 months in the past following the depths of crypto winter. During the last a number of quarters, Marathon Digital has accomplished a pleasant job rising belongings whereas additionally reducing debt:

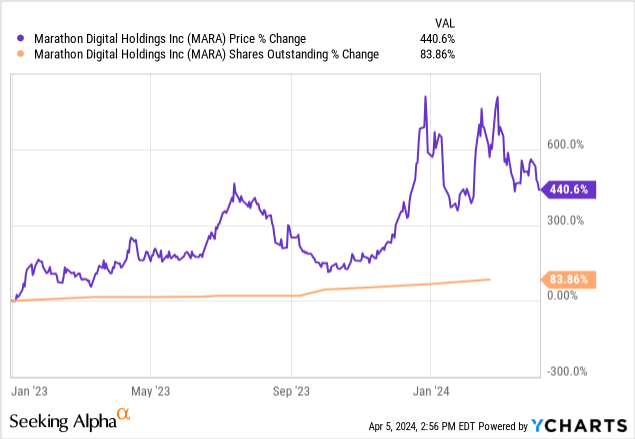

A lot of this asset development has come on the expense of shareholder dilution, however with the value of MARA shares up over 400% for the reason that finish of 2022, anybody who purchased the capitulation in December of that 12 months has considerably outpaced the dilution since that point:

On the convention name, CEO Fred Thiel talked about simply how totally different the setup is for miners at this time in comparison with a 12 months in the past when BTC was buying and selling underneath $25k per coin and the corporate had extra debt than liquidity:

We’ve $1 billion of liquidity on our stability sheet and have lowered debt by over $411 million, whereas saving our shareholders $100 billion within the course of, leading to internet debt of $331 million.

What Marathon has pulled off relating to the stability sheet is admittedly spectacular. Thiel went on to say the corporate plans to take management of about half the of their whole hash fee and we’re already seeing a few of these dominos falling with Marathon recently agreeing to purchase Utilized Digital’s (APLD) knowledge middle in Backyard Metropolis, Texas for $87 million. MARA has traditionally used APLD for Bitcoin mining internet hosting companies. Based on Marathon, this deal will scale back mining value at that website by 20%.

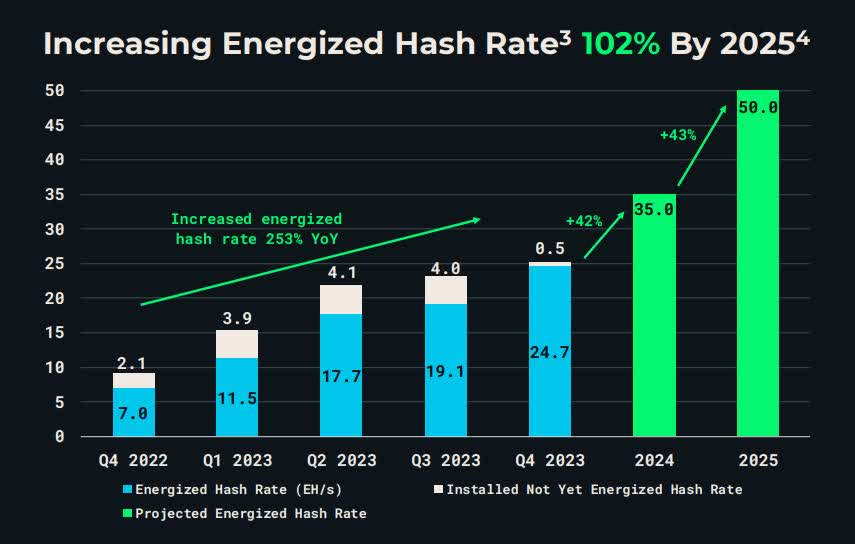

Investor Deck, Slide 3 (Marathon Progress)

Wanting forward, Marathon Digital is eying substantial exahash development by way of the rest of this 12 months and into 2025. 35 EH/s by the top of this 12 months can be 42% development from the top of 2023. 50 EH/s by 2025 can be roughly double the 12 months finish stage. Thiel talked about that it will likely be attainable for this timeline to be accelerated if alternatives to take action manifest; which is probably going a reference to post-halving consolidation that figures to occur when weak mining outfits faucet out and switch off machines.

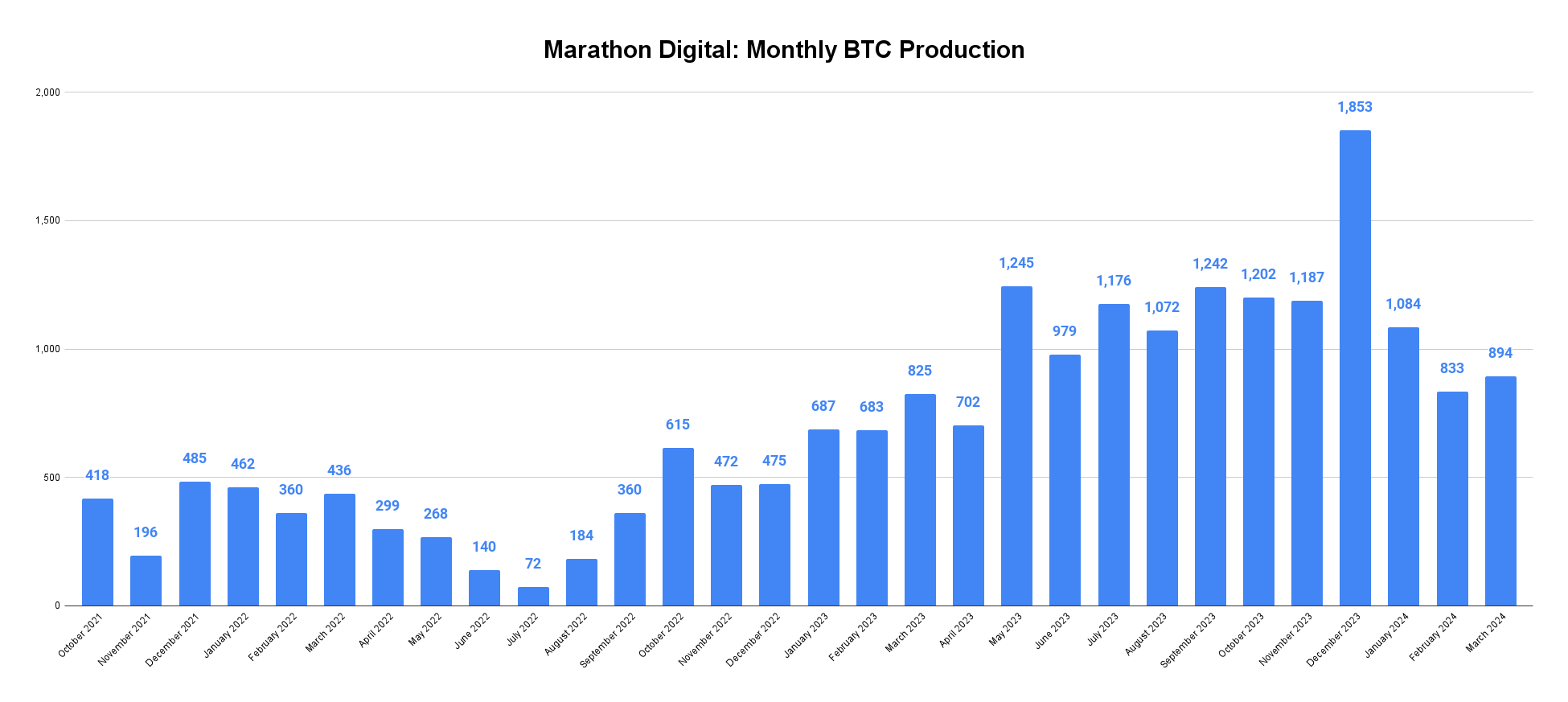

Q1 Manufacturing

Creator’s chart (Marathon Digital)

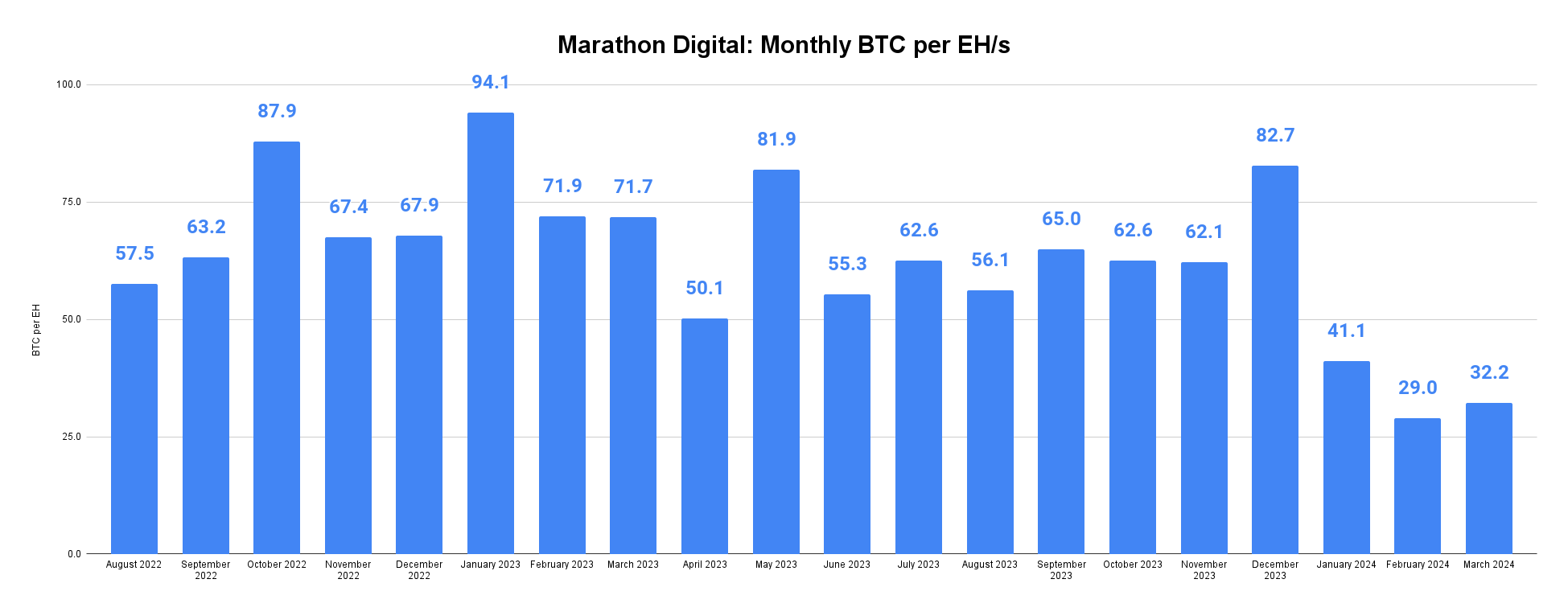

Regardless of the outstanding manufacturing metrics for many of 2023, Q1 was not notably nice for MARA each from a complete BTC mined standpoint and from an effectivity perspective. After mining no less than 1,000 BTC in 7 consecutive months between July and January, Marathon has averaged simply 864 BTC over February and March. Whereas Q1 manufacturing was up 12 months over 12 months, development has come at the long run expense of BTC per EH/s effectivity:

Creator’s chart (Marathon Digital)

Marathon’s BTC per EH/s numbers have been broadly trending down for over a 12 months and it speaks to the elemental drawback with everybody within the enterprise chasing share features from what’s a shrinking nominal BTC pie:

To name Bitcoin community international hash parabolic would in all probability be acceptable. The hope for firms like MARA is that they will develop share of world hash fee towards their friends. Thus far, the corporate has been in a position to accomplish that a number of quarters operating. However even assuming Marathon can hit its scaling aims, the block reward halving later this month is a serious long run headwind.

Already Priced For Perfection?

If we take MARA’s 2024 12 months finish steerage for EH/s and calculate what we may fairly anticipate annualized income to be in a post-halving setting, we get $1.1 billion in annual income from mining at a BTC worth of $100k:

| BTC Worth | 30 Eh/s | 35 Eh/s |

|---|---|---|

| $60,000 | $587,520,000 | $685,440,000 |

| $70,000 | $685,440,000 | $799,680,000 |

| $80,000 | $783,360,000 | $913,920,000 |

| $90,000 | $881,280,000 | $1,028,160,000 |

| $100,000 | $979,200,000 | $1,142,400,000 |

| $150,000 | $1,468,800,000 | $1,713,600,000 |

| $200,000 | $1,958,400,000 | $2,284,800,000 |

| $250,000 | $2,448,000,000 | $2,856,000,000 |

Supply: Creator’s calculations

This calculation makes some assumptions on post-halving effectivity and manufacturing. Particularly, I am utilizing a trailing twelve month weighted common month-to-month EH/s of 54.4 and slicing it right down to 27.2 for my post-halving BTC per EH/s estimate. This clearly does not take a change in international hash fee or Marathon’s share of world hash into consideration. However at 30 EH/s, MARA can be mining 816 BTC post-halving. At 35 EH/s they’re at 952. Just like the breakeven worth earlier within the article, take this extra as a again of the envelope estimate somewhat than as a forecast.

In any case, this system has MARA shares already buying and selling at about 3x ahead gross sales at a $150k BTC worth – or greater than double at this time’s Bitcoin worth. The ahead P/S sector median for information tech is 2.9. This estimate additionally assumes Marathon Digital sells manufacturing after the halving and historical past is a sign that the corporate usually does not try this.

Different Issues

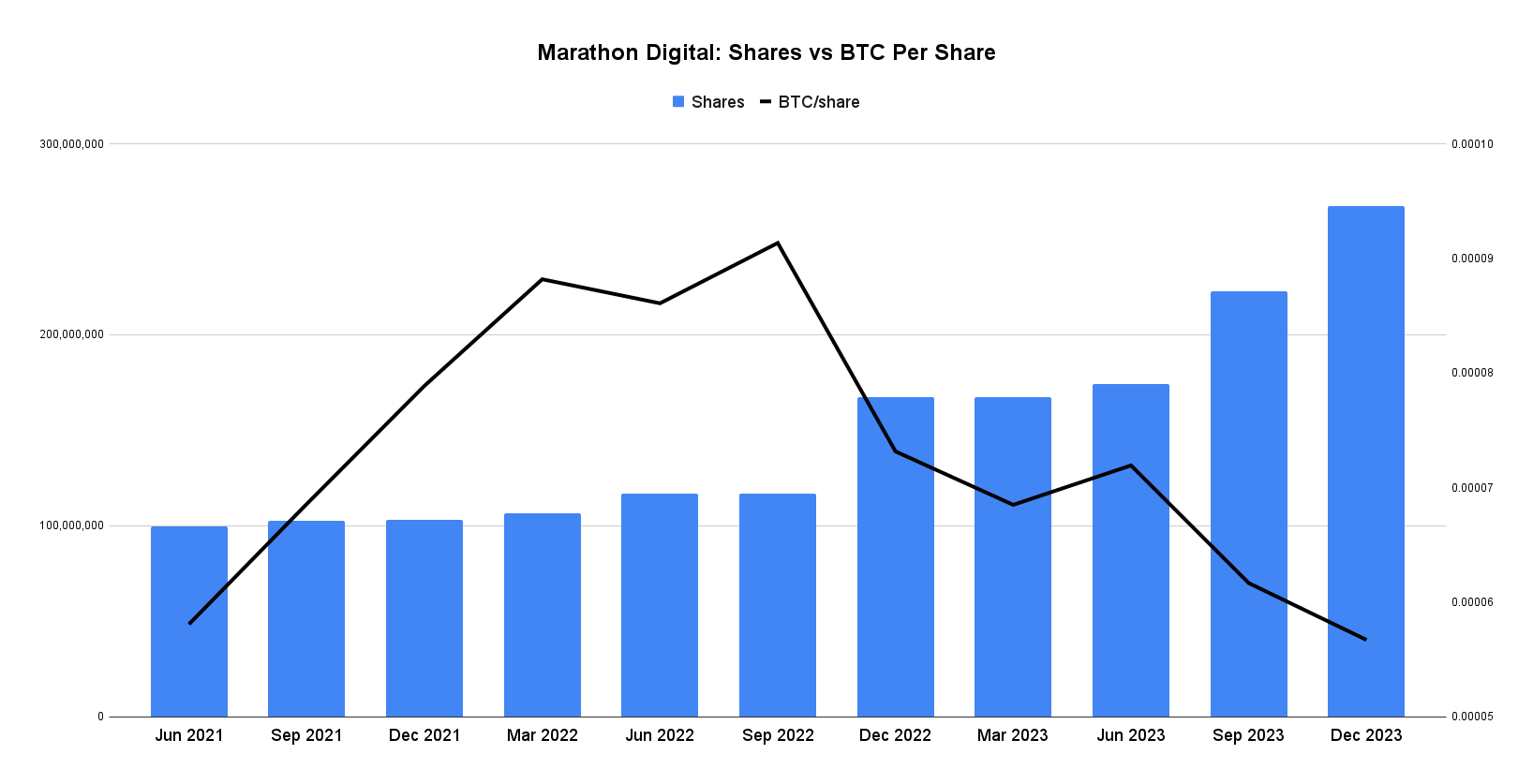

I have been writing about Bitcoin miners for Searching for Alpha for almost two years. Over that point, I have been fairly clear that I do not personally view BTC mining firms as nice long run investments. I feel they’re actually nice for merchants and for that purpose I nonetheless do maintain some MARA shares. However in the event you’re shopping for MARA for the BTC stack, you are seemingly going to proceed getting diluted over time:

Creator’s chart (Searching for Alpha, Marathon Digital)

Within the chart above, I am displaying almost a 3 12 months development in quarterly shares excellent and BTC per MARA share. During the last 5 quarters, the BTC per share for MARA shareholders has been almost reduce in half. This is not meant to say MARA is essentially a nasty BTC proxy guess as a lot because it’s simply to level out every investor ought to be aware of what their private goal is.

Investor Takeaway

In the event you’re attempting to optimize swing trades and personal firms which have BTC-denominated income streams, MARA works very properly for that. You simply should be ready for the volatility. Nonetheless, in the event you’re merely attempting to extend your publicity to BTC particularly, the newly authorised spot ETFs are in all probability a significantly better long run choice. I am personally nonetheless holding MARA shares as a result of I feel a few of the extra long run targets are literally pretty attention-grabbing; particularly wasted warmth and stranded gasoline alternatives. However these are extremely speculative at this juncture.

On the deserves of what the underlying enterprise is at this time, I feel spot ETFs are the higher method to categorical a $150k BTC thesis than MARA at $19. If transaction charges have a comeback, which may change issues for me. However the extra BTC that will get sucked up by ETF managers, the much less energetic addresses I would anticipate to see paying charges on chain.