Paul Bradbury

As we speak I’d like to debate a distinct segment software program firm that went public again in 2021. This firm has a robust founder-led CEO and has been rising income and clientele lately. The corporate’s inventory worth is up over 12% YTD and is up practically 40% year-over-year.

Nevertheless, that is nonetheless an unprofitable firm, one which hasn’t carried out a lot for shareholders but because the inventory remains to be down since going public.

The corporate is Procore Applied sciences, Inc. Let’s dig into the corporate to see if this enterprise can proceed to develop and supply returns to shareholders in years to return.

The Firm

Procore Applied sciences (NYSE:PCOR) was based again in 2002 by Craig “Tooey” Courtemanche. On the time Courtemanche was working in Silicon Valley however had a home being in-built Santa Barbara. Courtemanche was having varied points surrounding the communication of the job with the quite a few events concerned and so Courtemanche created a method during which all these events might talk with each other extra successfully and thus Procore was born.

The corporate’s mission is straightforward, “To connect everyone in construction on a global platform.” Procore is the chief in offering cloud-based building administration software program. The development trade is a posh one with many key gamers relying on the job or job at hand. Procore’s know-how helps join these concerned in a building job comparable to house owners, normal and specialty contractors, architects, and engineers so duties might be accomplished in a well timed and environment friendly style.

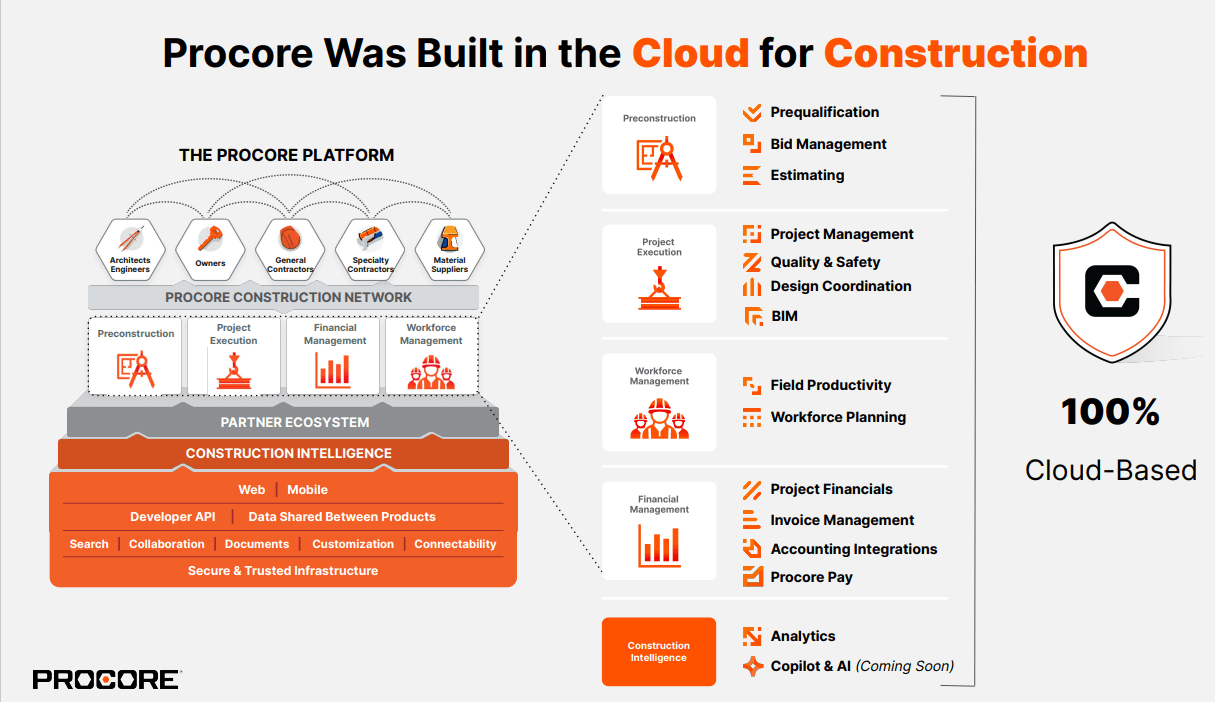

The beneath graphic illustrates Procore’s providing as the corporate’s software program has 5 totally different product classes, Preconstruction, Challenge Execution, Workforce Administration, Monetary Administration and Building Intelligence:

Investor Presentation

The Building Intelligence product is not out but, however Procore will make the most of Microsoft’s Copilot for AI capabilities comparable to making a digital assistant.

Moreover, Procore has additionally just lately launched Procore Pay which is able to improve the corporate’s monetary suite. On the corporate’s newest earnings call, though it’s nonetheless very early into the launch, Courtemanche said, “…We are excited about payments and the early feedback has been very positive. It’s important to note that we are the only solution in the market that connect estimating to contracts to compliance documents to invoices to payment workflows, all on a single platform.”

Moat and Alternative

Procore believes they’ve a big alternative as the development trade is “one of the oldest, largest, and least digitized industries” as said by the corporate of their most up-to-date 10K filing. The trade is fragmented and might be fairly specialised particularly areas.

Building remains to be an enormous trade as Procore said on a latest investor presentation, $11 trillion was spent on international building in 2020 and it’s estimated that quantity will climb to $15 trillion by 2030. Moreover, in 2017 13% of United State GDP got here from the development trade and seven% of the worldwide workforce got here from the development trade.

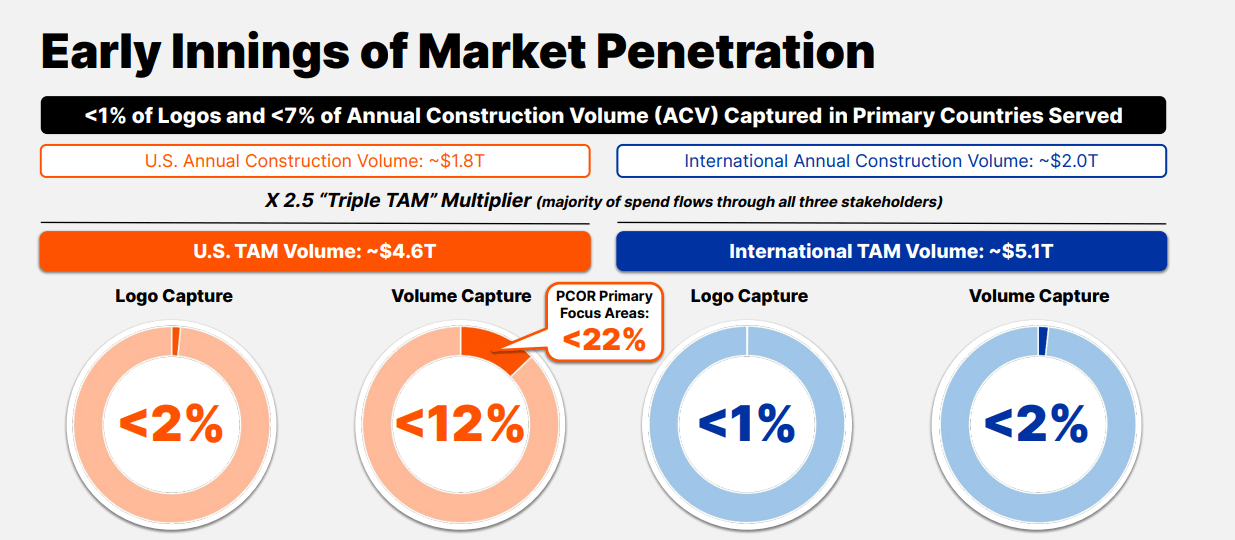

As proven below, Procore believes they’ve a home alternative of roughly $1.8 trillion and a world alternative of roughly $2 trillion:

Investor Presentation

As famous on the corporate’s latest 10K, key rivals embody, Oracle (ORCL), Autodesk (ADSK), and Trimble (TRMB). Whereas these are some severe gamers within the know-how area, Procore appears to be chief on this market, and I do imagine Procore has a moat. As I used to be researching the highest software program for building industries Procore was regularly the highest software program listed. Procore even reveals their scores on their website which illustrates how a lot firms like their software program.

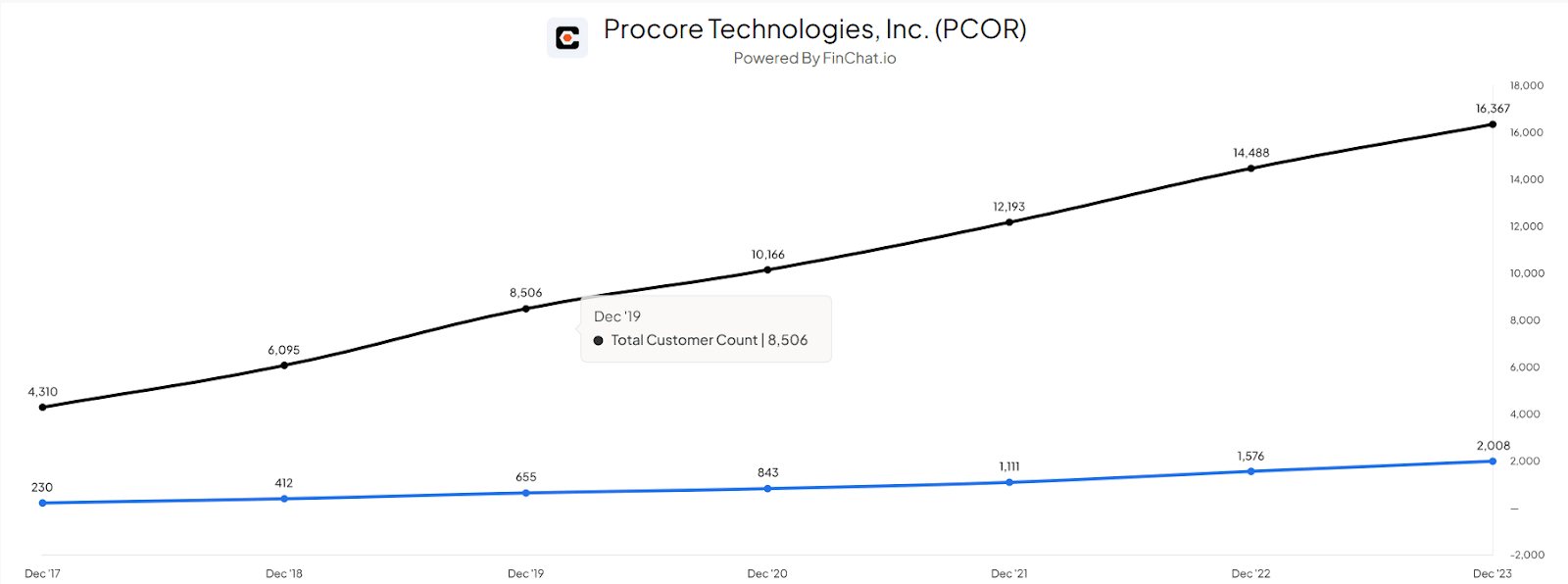

The purpose is additional illustrated with this graphic I pulled from Finchat.io. Procore has steadily been rising their variety of clients (as proven by the black line) and the variety of clients with annual recurring income of 100K or extra (as proven by the blue line) is growing as properly:

Finchat.io

Additionally as Courtemanche famous on the corporate’s newest earnings call, Procore’s internet retention price is at 114% which reveals the energy of the software program. Presently, I do suppose Procore appears to be market chief and their know-how has given them a aggressive benefit.

Administration

As famous above, Craig “Tooey” Courtemanche is the Founder, President and CEO of Procore.

Howard Fu is the corporate’s present CFO. Fu has labored at Procore since 2021. He came visiting from DocuSign the place he was a key a part of the group’s finance workforce. Fu has additionally labored at Salesforce as properly.

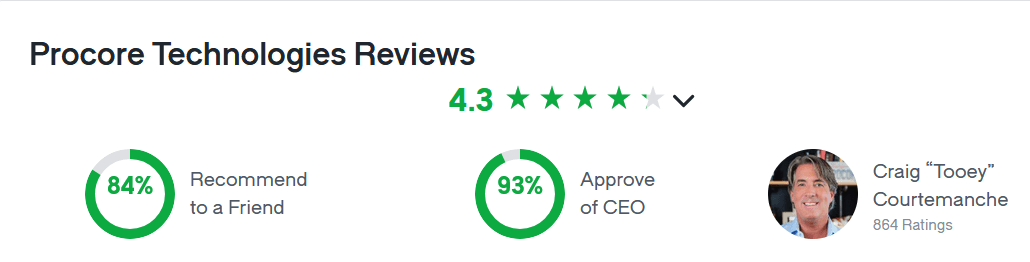

The Glassdoor scores present that Procore is a really good spot to work because it was awarded as being top-of-the-line locations to work in 2017, 2019, 2022, and 2023. Most just lately in 2024 Procore was ranked by Glassdoor as fifth finest place work to work which is kind of the accomplishment.

Beneath are the present Glassdoor reviews. Procore is seen as a superb place to work, and the workers there clearly approve of Courtemanche:

Glassdoor

As I’ve said prior to now, I’m an enormous believer in founder CEOs resulting from their propensity to give attention to the long run and I like when senior management has pores and skin within the recreation. Procore’s present 12 months proxy will come out shortly however as of the corporate’s last proxy statement Courtemanche held over 5% of the corporate’s frequent inventory which I prefer to see.

Financials

Procore has but to change into GAAP worthwhile however the firm has been making spectacular strides as you’ll be able to see beneath within the firm’s most up-to-date 10K filing:

SEC.gov

Procore delivered revenues of roughly $950 million for the newest fiscal 12 months which is a 29% enhance in comparison with the prior 12 months. Moreover, Procore’s GAAP gross margin is at a powerful 82%.

From a cash flow perspective, Procore delivered working money influx of roughly $92 million in 2023 which is way higher than $12 million of working money influx in 2022. Free money circulate for 2023 got here in at roughly $47 million.

Procore does have a strong stability sheet in addition to you see beneath:

SEC.gov

The corporate’s money stability has grown to is almost $358 million, and their present property stability can cowl all the group’s present liabilities.

Dangers

Procore lists quite a few dangers to the enterprise on their most up-to-date annual report. I’m going to debate two dangers which I imagine might harm the group.

As Courtemanche touched on within the firm’s latest earnings call, the development enterprise is cyclical and is intently related with the financial system in addition to rates of interest. Right here is an portion of Courtemanche’s opening remarks which actually replicate how Procore’s enterprise is effected by these components:

“So, I’d like to start by acknowledging that 2023 proved to be a challenging year amid a tough economic environment. Much of the commentary we shared on our last earnings call is still relevant to what we’re seeing today. 2022 and 2023 were very different years for our industry.

In 2022, our customers demonstrated optimism in their sentiment and their buying behavior. This optimism largely stemmed from the strength of our customers’ backlogs and their confidence in the future pipeline of work, however, 2023 brought a notable shift. While backlogs remain strong, sentiment shifted partially due to rapidly rising interest rates and the industry began to hedge against future work just in case.

Sentiment drove conservatism for the future and led the industry to be cautious about future volume commitments should future demand weigh in. As we all recognize, construction and our economy are cyclical.”

The US financial system has remained resilient these days however ought to the nation go right into a recession, as some predict will happen, this might harm the development trade and in flip Procore.

As famous earlier, Procore competes with a number of giant firms comparable to Oracle, Autodesk, and Trimble. Procore should proceed to innovate and create distinctive know-how so clients will stay loyal. If Procore fails to take action their place because the chief inside this area of interest software program trade would definitely be in jeopardy.

Valuation

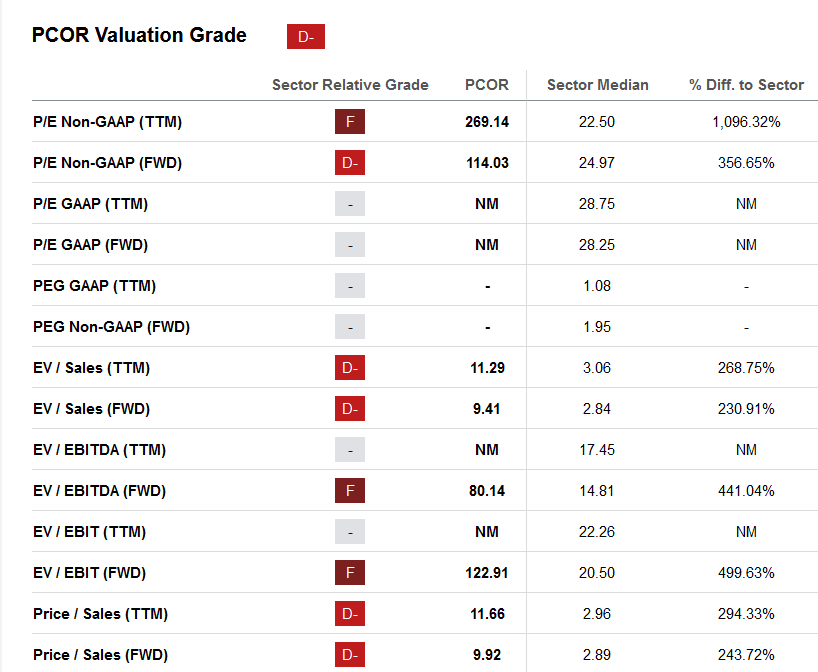

As you’ll be able to see from the beneath valuation metrics from Looking for Alpha, the general worth grade for Procore is a “D-.”

Looking for alpha

As Procore is unprofitable, I believe worth to gross sales is the most effective metric to view this group.

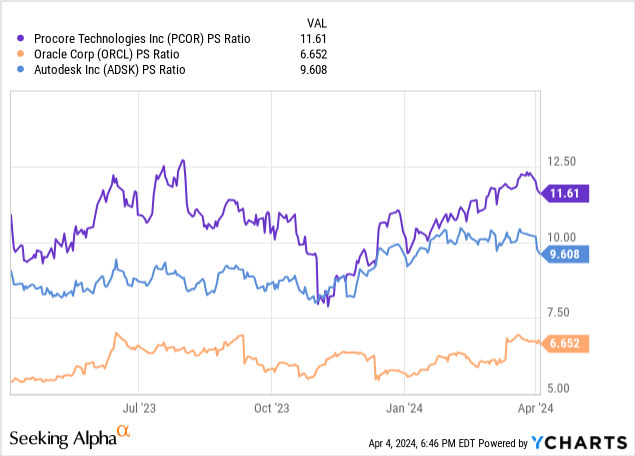

On this case, Procore does look like buying and selling at a premium in comparison with the rivals I’ve talked about above as this graphic illustrates.

Nevertheless, as Procore is the market chief, I’m prepared to pay a premium for trade chief. I might provoke a place at these ranges and would fortunately add ought to this metric drop.

Conclusion

Procore is a pacesetter inside a distinct segment market and is rising income in addition to shopper rely.

Procore has a founder-led CEO with years of expertise within the building trade and who has a substantial stake within the enterprise. Staff appear to actually approve of Courtemanche too and the working setting he and the administration workforce have created as Procore is seen as one of many high firms within the nation to work for in accordance with Glassdoor.

As the development trade isn’t as “digitalized” as different industries and is very fragmented Procore appears to a big alternative to proceed to develop so long as the corporate can proceed to ship stellar know-how and retain clientele.

I imagine Procore might be a superb alternative for long-term buyers as I believe this founder-led firm can proceed to develop within the years to return.