Monty Rakusen

By Ewa Manthey

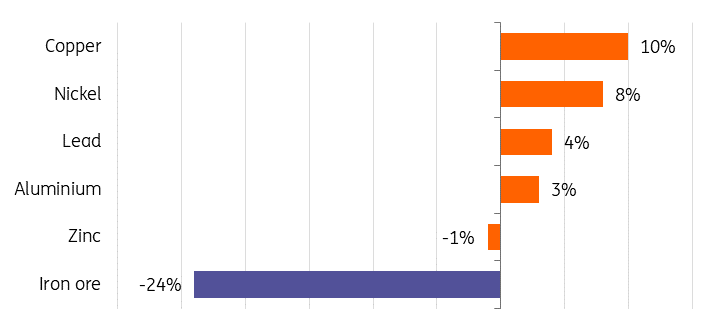

YTD metals efficiency %

Supply: LME, SGX, ING Analysis

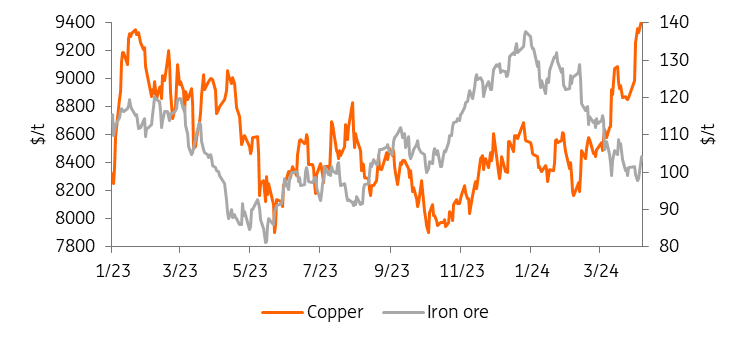

Copper and iron ore costs are diverging

Costs of copper and iron ore diverging rapidly with copper costs surging above $9,000/t, whereas iron ore is buying and selling nearer to the $100/t degree. China’s issues over the continuing property disaster have weighed on the iron ore market, whereas copper advantages from rising demand for electrical automobiles (EVs) and renewable power.

Whereas conventional demand drivers, reminiscent of property and development, face headwinds, demand from the inexperienced power sector continues to develop, and iron ore doesn’t profit from that.

Copper rallies as iron ore slumps

Supply: LME, SGX, ING Analysis

This divergence is more likely to deepen as China’s economic system undergoes a major transition in the direction of ‘high-quality progress’ and Beijing pursues new progress drivers in sectors together with clear power and high-tech manufacturing. The property sector makes the majority of metal demand however to this point there have been little indicators of huge fiscal stimulus by Beijing within the development and property sectors. It seems extra centered on the ‘new three’ progress drivers: EVs, batteries, and photo voltaic panels.

Copper is utilized in every part from EVs to wind generators and energy grids. In EVs, copper is a key part utilized in electrical motors, batteries and wiring, in addition to charging stations. Copper has no substitute for its use in EVs, wind, and photo voltaic power, and its enchantment to traders as a key inexperienced steel will proceed to help increased costs over the following few years.

Final yr, rising demand for renewables and EVs in China already offset the hunch from the extra conventional sectors just like the property market, and we anticipate this shift in demand drivers to proceed this yr.

The surge in copper costs has additionally been pushed by sudden provide constraints, particularly the closure of Canada’s First Quantum (OTCPK:FQVLF, FM:CA) mine in Panama. The Cobre Panama copper mine was one of many world’s largest sources of copper, accounting for round 1.5% of worldwide copper output.

Iron ore slumps on disappointing demand

Iron ore has bought off greater than 20% this yr, with costs dropping beneath $100/t to their lowest since August. The basics are deteriorating; metal demand in China continues to disappoint, and the gloom within the nation’s property sector drags on. Though China’s total manufacturing exercise rebounded in March, its metal trade PMI remained in contraction territory.

China’s metal trade PMI dives additional into contractionary territory

Supply: NBS, ING Analysis

As for China’s property slowdown, the nation’s new residence begins – the most important metal demand driver – fell sharply in 2023, down by greater than 20%. This could proceed to suppress metal demand this yr. Property makes up most of China’s metal demand. Futures for reinforcement bars, a key development product, not too long ago hit the bottom degree in Shanghai since 2020, signalling the nation’s property disaster is dragging on.

The federal government has to this point held off delivering a sufficiently big stimulus bundle to revive China’s ailing property sector. The same old enhance in development exercise within the spring has additionally did not materialise, and iron ore and metal inventories are climbing.

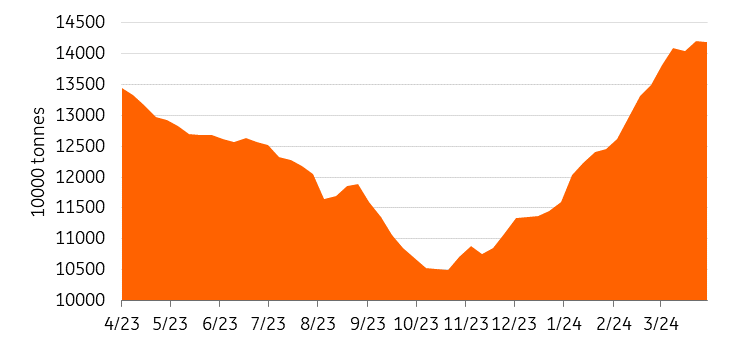

Iron ore inventories in China surge

Supply: Steelhome, ING Analysis

Iron ore inventories in China surged 24% within the first quarter – the most important three-month enhance in share phrases since 2014. China’s iron ore port stock is a key indicator that displays the provision and demand steadiness, in addition to the protection web and imbalance between the iron ore provide and the metal mill demand. With the seasonal uptick in demand not but materialising, the drawdown in shares is likely to be delayed. We consider excessive iron ore availability in China will proceed to place stress on costs.

The China Iron & Metal Affiliation not too long ago referred to as on home metal mills to “reduce production intensity” because the property downturn and slowdown within the infrastructure sector delay metal demand restoration.

Draw back dangers are more likely to prevail within the close to time period for iron ore costs amid subdued metal demand. China will proceed to drive iron ore costs going ahead, and the provision and demand steadiness will largely rely on China’s metal demand outlook. An additional increase for China’s property sector will probably be essential in supporting demand. We see costs averaging $100/t in Q2 with a 2024 common of $106/t.

Copper rallies on tightening provide

This hunch in iron ore costs contrasts with copper, which is buying and selling at its highest for the reason that center of 2022, up 10% to this point this yr, fuelled by provide dangers and bettering demand prospects for metals used within the inexperienced power transition.

The primary catalyst for copper’s rally is the sudden tightening within the world mine provide, most notably First Quantum’s mine in Panama, which has eliminated round 4000,000 tonnes of the steel from the world’s annual provide. As well as, Anglo American (OTCQX:NGLOY, OTCQX:AAUKF) stated it was reducing output by 200,000 tonnes. And Codelco, the world’s largest copper producer, is struggling to get well from the bottom output in 1 / 4 of a century.

Most not too long ago, Ivanhoe Mines (IVN:CA, OTCQX:IVPAF) reported a 6.5% quarterly drop in output on the Kamoa-Kakula mining advanced within the Democratic Republic of Congo.

Copper smelters in China have pledged to curb output in response to a tightening copper ore market and following a collapse in spot therapy and refining fees to document lows. Spot fees in China plunged to $2.30/t final week, based on weekly information from Fastmarkets. They’re now down greater than 95% for the reason that starting of the yr.

The drop in therapy fees displays not solely the tightening concentrates market but additionally the fast enlargement in copper smelter capacities in China. China’s strategic want for copper has pushed this enlargement as demand from the inexperienced power sector continues to develop. Final yr, China’s manufacturing of refined copper surged 13.5% year-on-year to 12.99 million tonnes, based on information from the Nationwide Bureau of Statistics (NBS).

The worldwide refined copper market was anticipated to be pretty balanced this yr, however the shortfall in mine provide now signifies that the market is more likely to be in a deficit. The extent of this deficit may also rely on the scope of Chinese language smelters’ manufacturing curbs and the way rapidly Chinese language copper demand will choose up within the second quarter, which is seasonally the strongest for copper demand.

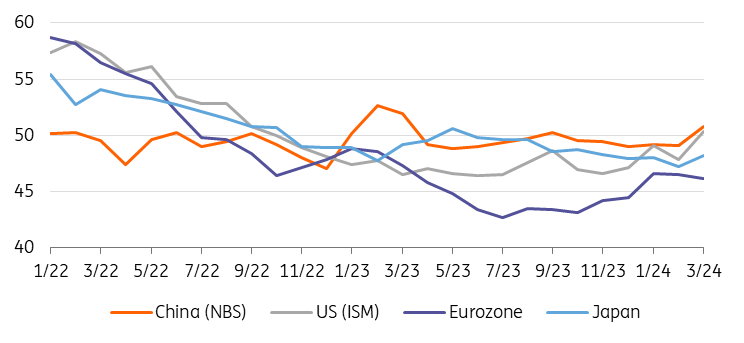

Hopes for a world restoration in demand this yr are additionally supporting copper, with manufacturing exercise selecting up globally. In China, the official manufacturing buying managers’ index expanded in March for the primary time since September.

Manufacturing exercise is selecting up

Supply: NBS, ISM, S&P International, ING Analysis

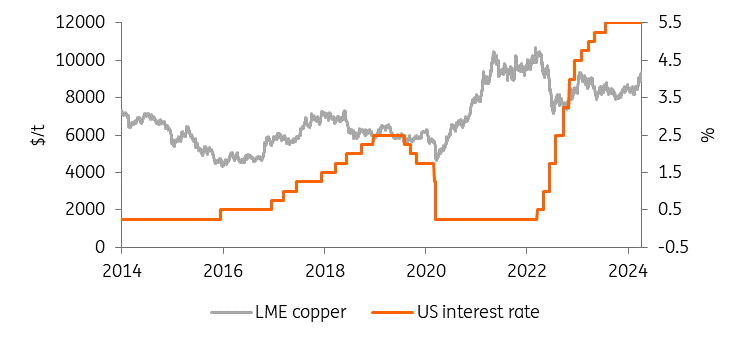

Copper costs have additionally been lifted by the nearing finish of the Federal Reserve’s rate of interest tightening cycle. Elevated charges and a stronger greenback have been a drag on industrial metals over the previous two years.

Trying additional forward, copper costs will probably be supported by a weaker US greenback on the again of Fed easing. Copper will profit from looser financial coverage, which can alleviate the monetary pressure on producers and development firms by lowering borrowing prices.

Nevertheless, with the newest US jobs information for March surged previous estimates, the prospect of a June rate cut from the Fed looks slim.

If US charges keep increased for longer, this might result in a stronger US greenback and weaker investor sentiment, which in flip would translate to decrease copper costs.

Copper ought to profit from looser financial coverage

Supply: LME, Federal Reserve, ING Analysis

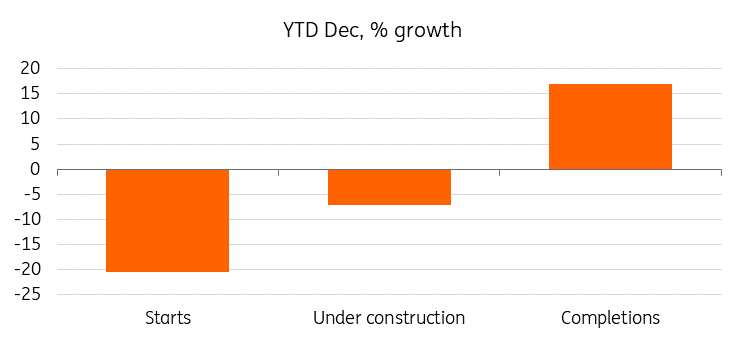

On the identical time, demand uncertainties stay. China’s property market has been a significant headwind for copper demand for the previous yr. A continued slowdown within the sector stays the primary draw back threat for the steel. Nevertheless, whereas housing begins had been down greater than 20% final yr, completions, the important thing supply of copper consumption, have been rising. This might present further help for copper costs sooner or later.

Completions are the important thing supply of copper consumption

Supply: NBS, ING Analysis

Within the brief time period, the upside to copper costs is likely to be capped by macro drivers, together with ongoing demand issues in China and lingering uncertainty over US financial coverage.

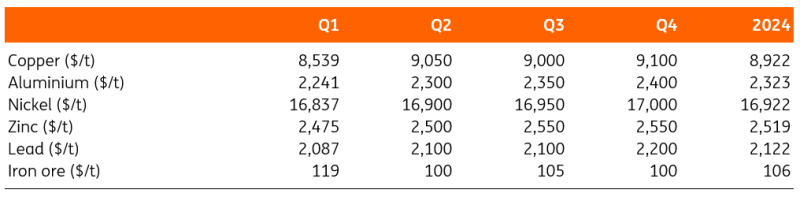

Nevertheless, micro dynamics are beginning to look extra constructive for the steel amid a tightening provide outlook. We see copper costs rising within the second quarter, which is seasonally the strongest for copper demand, to $9,050/t on common from a median of $8,539/t within the first. They might peak within the fourth quarter at $9,100/t. That stated, the market will stay unstable because it’s uncovered to macro drivers, not least from US rates of interest and Chinese language insurance policies.

ING forecast

Supply: ING Analysis