alvarez

Notice: I previously coated Cool Firm (NYSE:CLCO) in February 2024. I mentioned the corporate’s strengths: its fleet with TF-DE/XDF engines (plus two new builds geared up with ME-GA engines), engaging dividend yield, cheap valuation, and strong funds. CLCO will profit from changing LNG carriers powered by steam generators and rising LNG demand globally. I gave CLCO a powerful purchase ranking, contemplating its deserves. In as we speak’s notice, I’ll evaluation the final outcomes for 2023 and 4Q23 reported on the finish of February, the CLCO stability sheet, and the corporate’s valuation.

Fleet

CLCO has 11 LNG carriers; two extra might be delivered in 2H24. Seven ships have 160,000 – 162,000 cbm capability, and 4 have 170,000 – 174,000 cbm capability. Two CLCO vessels are geared up with the final technology of two-stroke engines appropriate for LNG carriers, X-DF. The remaining 9 have triple-fuel diesel-electric, TFDE, energy crops.

For instance the significance of propulsion for LNG carriers, I added a quote from my article on Flex LNG (FLNG), by which I elaborated on the assorted kinds of propulsion.

Till early 2000, steam generators had been the one viable answer to propel LNG ships. Between 2002 and 2012, Twin Gas Diesel Electrical (DFDE) propulsion crops gained traction. They’re similar to cruise ship set up – a couple of four-stroke diesel engines coupled with alternators generate electrical energy for electrical motors that drive the ship propeller. They will run on HFO, MGO, or BOG. That’s why generally they’re known as TFDE. BOG means boiling of fuel. It’s the losses occurring in the course of the storage of LNG. Because of the exterior warmth, some slight evaporation happens within the cargo, equal to 0.10%-0.15% per day. BOG is reliquefied and used as a gas for the primary engines.

XDF and MEGI have turn out to be extra prevalent within the final decade because of decrease development and upkeep prices. XDF means low-pressure dual-fuel diesel engine. It’s an old-school two-stroke engine that runs on BOG, HFO, and MGO. MEGI (mechanically operated, electronically managed fuel injection) is a extra refined model of XDF. The distinction is within the injection stress of BOG. MEGA engines are the latest modification of MEGI, representing 41% of the whole orders. MEGA/MEGI engines emit 40% much less Nitrogen oxide (NOx emissions) than the engines operating on HFO. Greenhouse emissions are additionally decrease (by 22%) in comparison with HFO energy crops.

The typical age of CLCO’s fleet is 8.4 years. CLCO manages 16 different vessels, eight of that are FSRU (Floating, Storage, and Regassification Models).

LNG carriers rating the very best order e book in comparison with different ship segments, 51%. At first look, this truth makes the LNG theme unvisitable. Nevertheless, the satan is hidden within the particulars. As identified, the decisive issue is the propulsion plant. ME-GA/ME-GI/X-DF powered ships will substitute the out of date steam propulsion vessels. Then again, there’s an ever-growing demand for LNG.

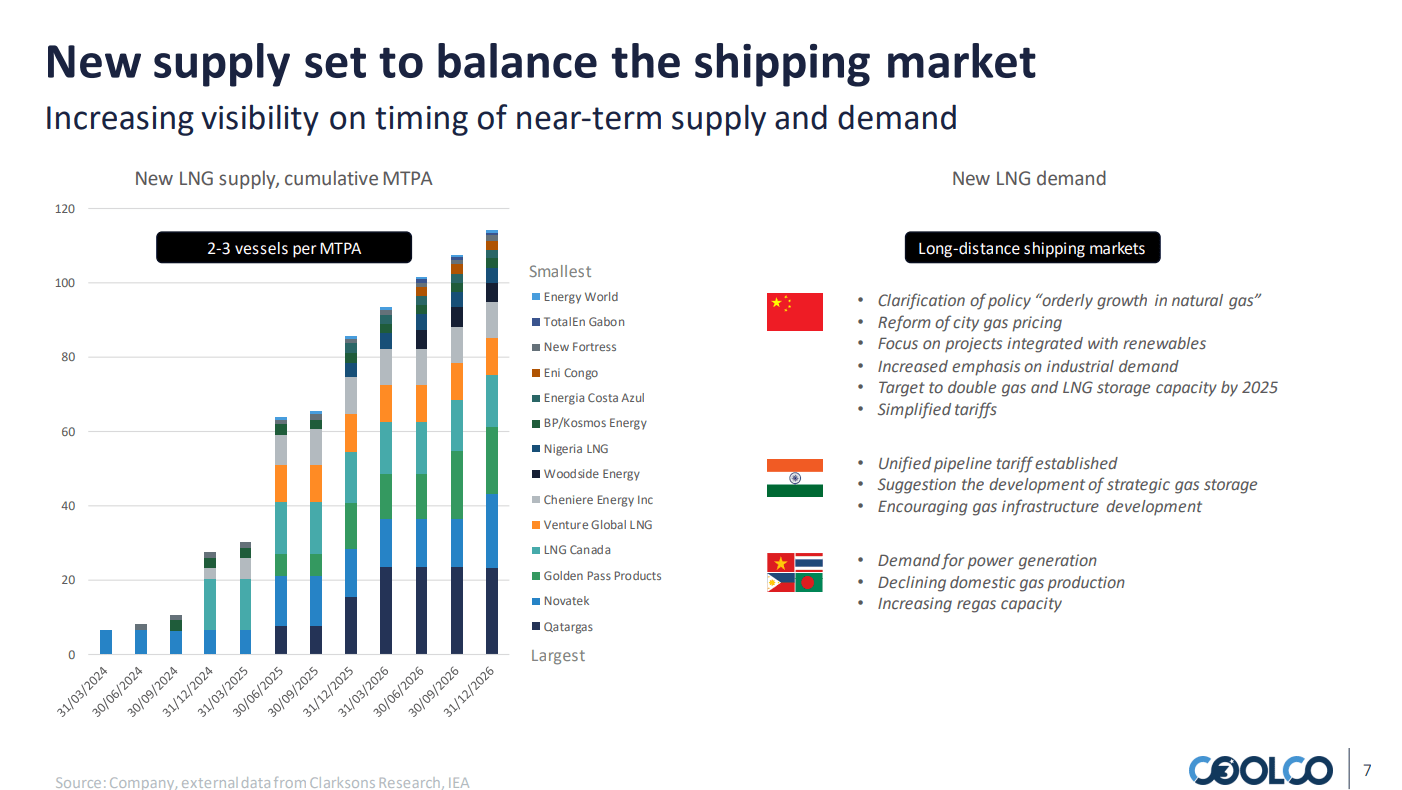

From 2024 till 2026, the LG provide will develop by 110 MTPA (million tonnes every year). Each MTPA requires 2-3 new LNG vessels. The left graph under from the 4Q23 presentation illustrates the corporate’s cumulative LNG provide for 2024-2026.

CLCO 4Q23 presentation

The most important drivers are India and China. Each closely spend money on LNG infrastructure with the long-term purpose of decreasing reliance on coal energy crops. Furthermore, Bangladesh, Vietnam, the Philippines, and Thailand are additionally getting extra concerned in LNG investments.

CLCO expects two new vessels (Kool Tiger and Kool Panther) to be delivered in 2H24. The corporate plans to make use of them on long-term contracts. The 2 incoming ships are designed with ME-GA engines. In 4Q23, CLCO closed a gross sales and leaseback settlement with Huaxia Financials to finance Tiger and Panther. The bareboat constitution is at a hard and fast charge for ten years, and the lease settlement comes with an implied curiosity of 6%.

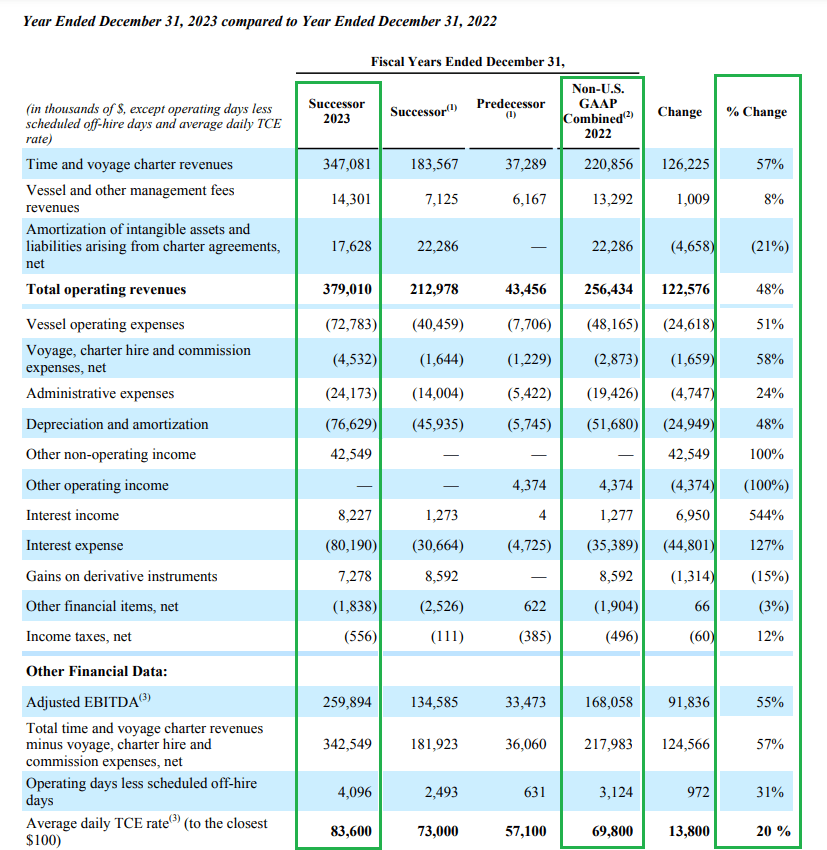

2023 outcomes dialogue

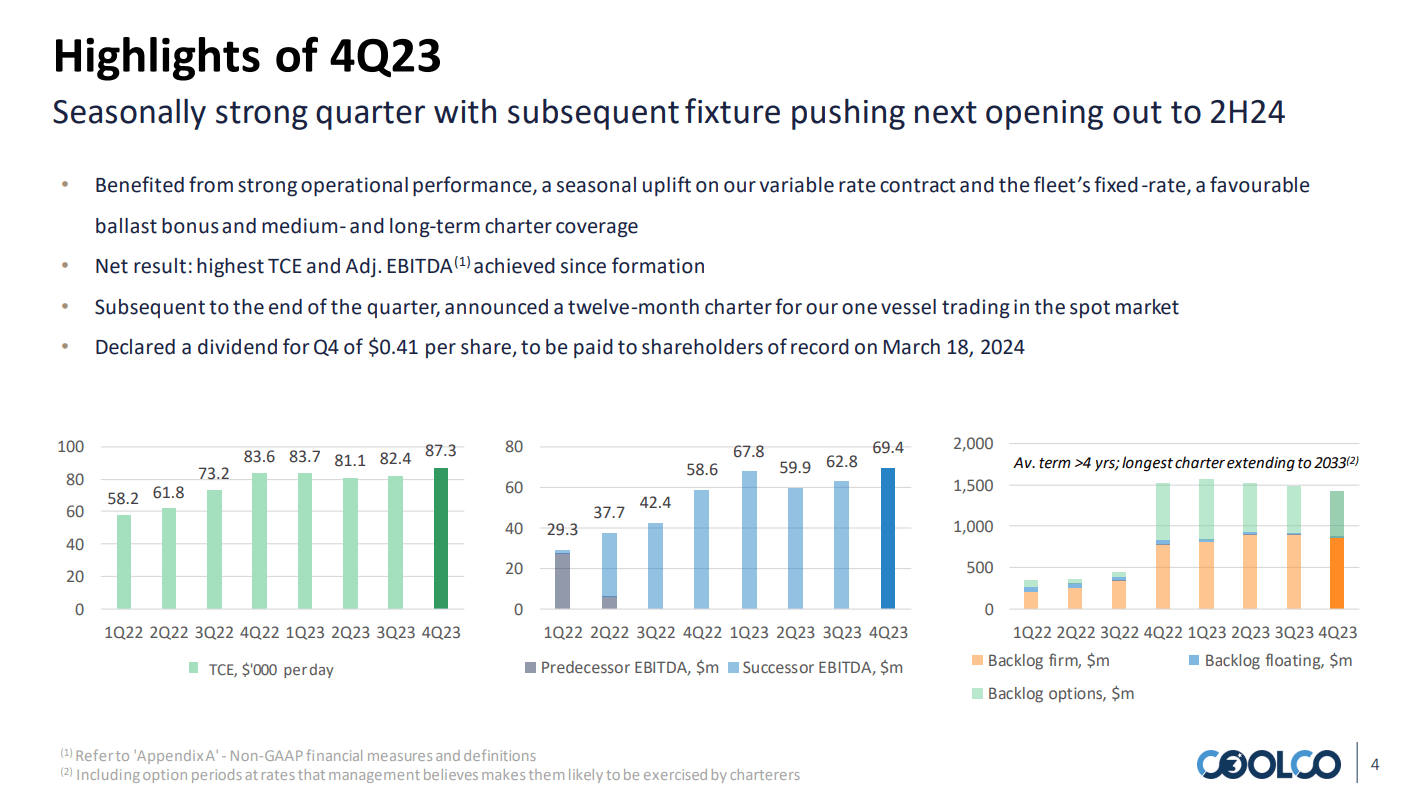

CLCO achieved sturdy operational ends in 4Q23 and FY23. The desk under presents realized TCE charges, quarterly EBITDA, and the corporate’s backlog.

CLCO presentation

CLCO employed its ships for $87,300/day in 4Q23, a report determine for the corporate. For comparability, CLCO achieved $69,800/day in 2022 TCE charges. The distinction in day charges for vessels geared up with steam generators and ships with newer generations of propulsion is price mentioning. Day by day TCE for steam turbine ships might be as little as $25,000/day. Then again, the steamers have every day OPEX like newer vessels.

For reference, Dynagas LNG reported $15,172 every day OPEX for 4Q23, whereas CLCO had $16,600/day. So, CLCO, with its up-to-date fleet, can obtain considerably higher charges at comparatively secure OPEX, leading to broader revenue margins.

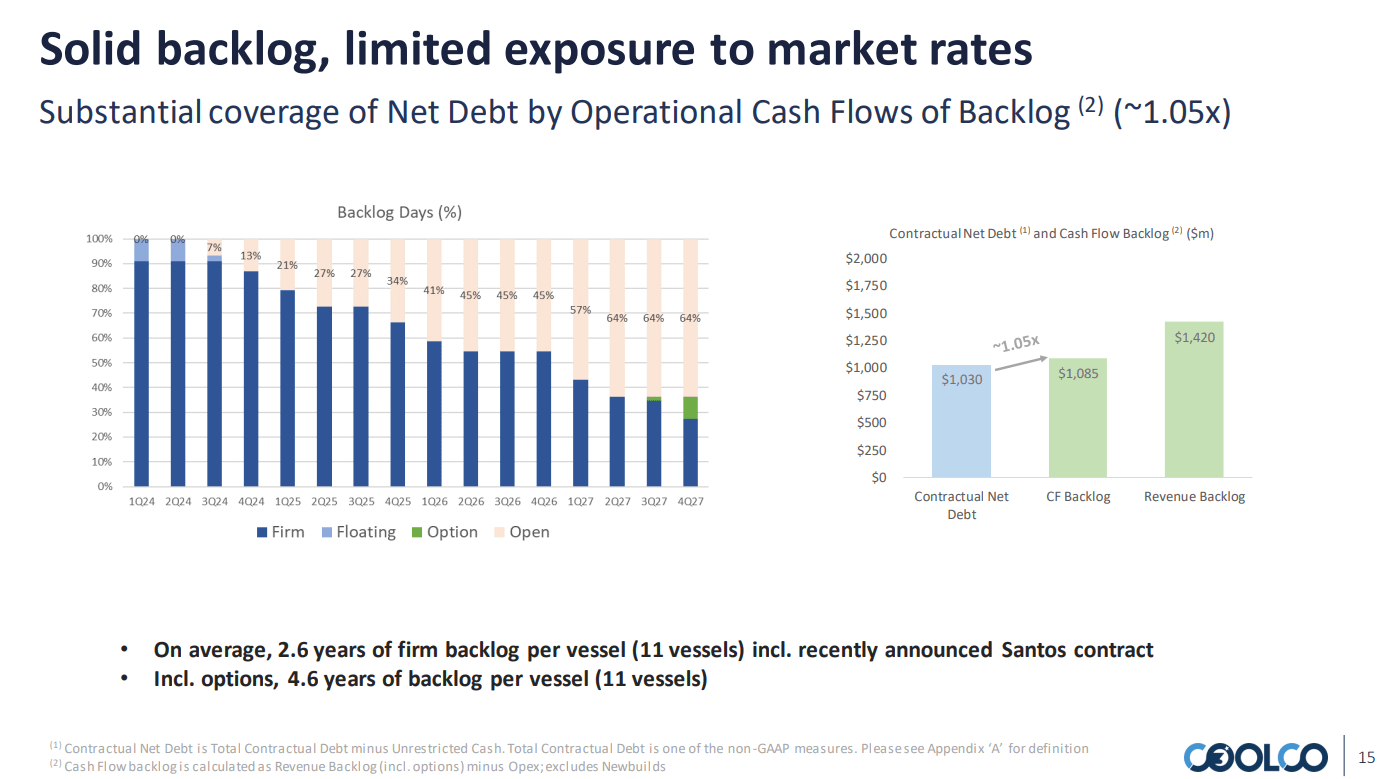

The next graph exhibits the CLCO backlog as a share of fleet days, measured in income and money move.

CLCO presentation

CLCO has a stable income backlog of $1,420 million, with a TCE of roughly $76,000/day. The typical length of the backlog per vessel is 4.6 years, together with choices. For 2024, CLCO plans dry docking for 4 of its ships, one (Kool Crystal) in 2Q24 and three (Kool Husky, Kool Frost, Kool Ice) in 3Q24.

CLCO delivered spectacular ends in 2023. The desk under represents CLCO’s monetary highlights from the 2023 report.

CLCO report

CLCO delivered $347 million in complete working revenues and $259 million in EBITDA. Stronger day charges and better variety of working days contributed to improved revenues in 2023. The CLCO technical administration section delivered 8% income development, reaching $14.3 million in 2023. Working days had been elevated by 31%, resulting in 51% YoY development in every day OPEX. Curiosity bills greater than doubled YoY from $35.3 million to $80.2 million. Larger revenues and secure working bills resulted in higher profitability. YoY CLCO delivered 55% EBITDA development and 53% working money move development. The corporate scored $3.25/share diluted EPS FY23 vs $2.31/share FY22.

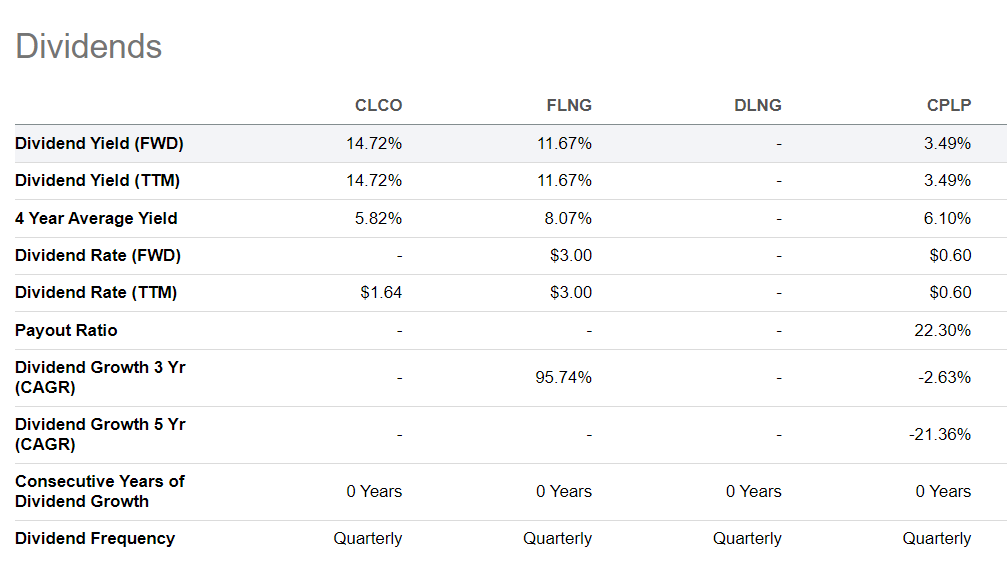

Dividends

Amongst its friends within the LNG section, FLEX LNG (FLNG), Dynagas LNG (DLNG), and Capital Product Companions (CPLP), CLCO distributes dividends with essentially the most engaging yield.

Looking for Alpha

Since October 2022, CLCO has applied its variable dividend coverage. The corporate distributes dividends based mostly on FCF after drydocking, and CAPEX allocations are calculated. For 2023, CLCO pays $1.64/share, leading to a 14.7% TTM yield and 50% payout ratio. In 2023, the corporate achieved $198 million working money move and distributed $87.5 million in dividends.

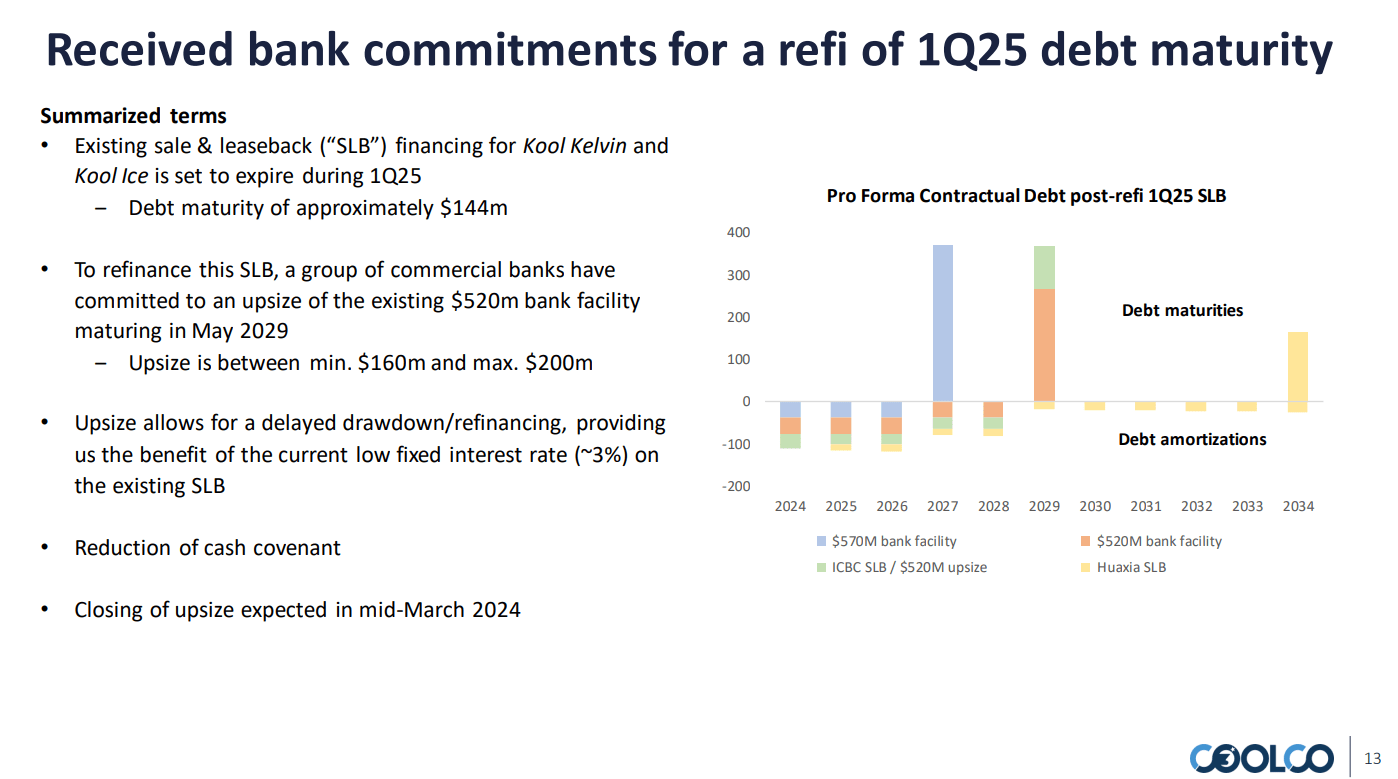

Steadiness sheet

CLCO has $133.5 million in money, $866 million in long-term debt, and $1,066 million in complete debt (together with $2.9 million in lease agreements). CLCO credit score services have rates of interest under 6%, and 85% of the debt is fastened curiosity. The corporate’s debt maturities will not be till February 2027.

CLCO 4Q23 presentation

A superb fleet resembling CLCO comes at a steep value. Nevertheless, CLCO maintains an sufficient capital construction: 132% complete debt/fairness and 60% complete liabilities/complete property. The corporate has enough liquidity to cowl its curiosity bills. In FY23, CLCO delivered $200 million in working revenue and $198 million in working money move. Over the identical yr, the corporate incurred $65.8 million in web curiosity bills.

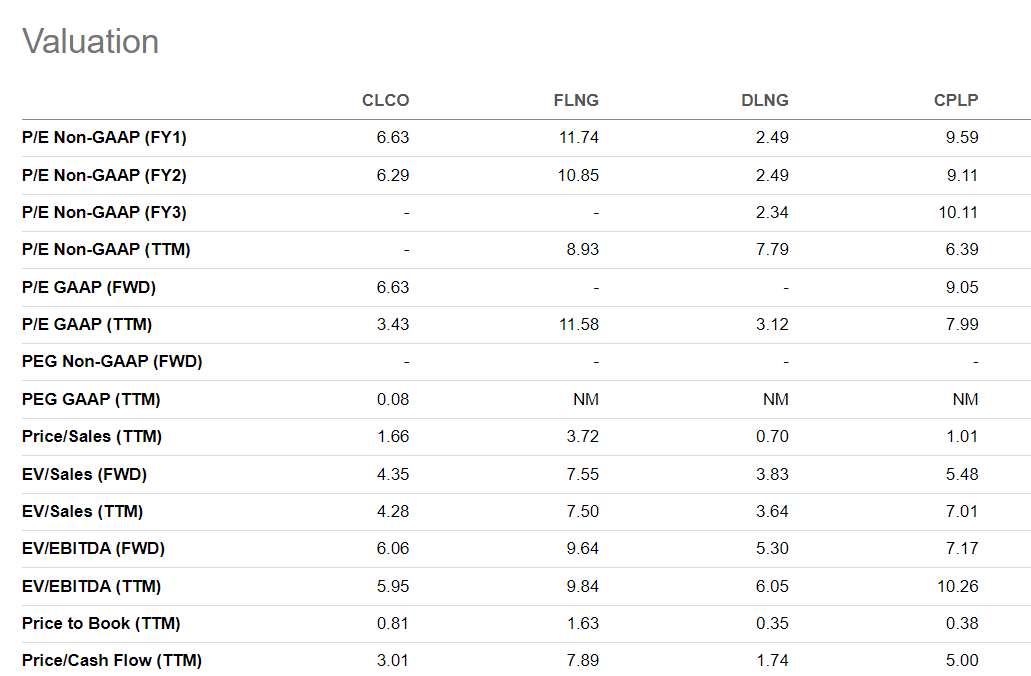

Valuation

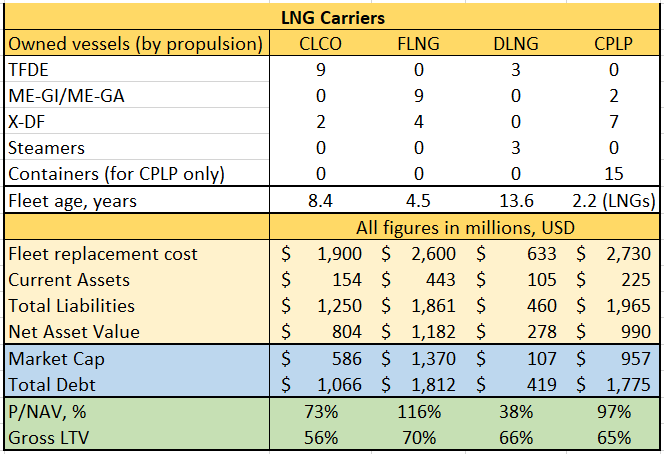

To estimate CLCO’s relative worth, I picked FLNG, DLNG, and CPLP. CPLP shouldn’t be a pure LNG play. The corporate owns 9 LNG carriers with a 174,000 cbm capability, geared up with X-DF/ME-GA propulsion. It additionally owns 15 container vessels of assorted sizes. Furthermore, CPLP ordered eleven different LNG carriers. So, it deserves to be included within the listing.

The next desk collates LNG delivery shares based mostly on fleet specs (propulsion, quantity, and age), worth (value to web asset worth), and leverage (mortgage to worth).

Writer’s knowledge

CLCO trades at 73% PNAV and has 56% LTV. I like FLNG and DLNG for various causes, although CLCO strikes the right stability between a top quality fleet, value, and leverage. The juicy dividend yields are the cherry on prime.

Since my final take, the valuations haven’t modified considerably. Then, CLCO traded at 4.15 TTM EV/Gross sales and 5.86 TTM EV/EBITDA. At as we speak’s market value, the corporate scores 4.28 EV/Gross sales and 5.95 EV/EBITDA.

Looking for Alpha

In comparison with its opponents, CLCO is comparatively undervalued. DNLG is the underside fish within the group because of its outdated fleet and publicity to Russia. FLNG and CPLP come on the highest multiples. FLNG has the youngest fleet, whereas CPLP declares its ambitions to turn out to be a number one LNG delivery firm.

Investor Takeaway

CLCO and DLNG are my favourite picks within the LNG section. Each corporations have distinct benefits over their friends. CLCO thesis comes with a couple of dangers. The prime one is the availability glut of LNG vessels.

Nevertheless, the demand for LNG transportation appears to develop at a quicker charge than the expansion of LNG vessel provide. Furthermore, we should think about the significance of propulsion. Steam turbine-equipped ships are out of date because of their inefficient propulsion crops. Within the coming years, vessels with MEGA/MEGA/XDF would be the most sought-after. Conversely, the demand for steamers will steadily decline. So, I anticipate the demand for the latest technology of LNG vessels to stay sturdy. Kool Tiger and Kool Panther will be part of CLCO’s fleet in 2H24, significantly enhancing the fleet’s high quality.

Financially, CLCO is a wholesome firm with a sturdy stability sheet and ample liquidity. The primary debt maturity within the coming years is in 2027. The opposite idiosyncratic threat is working threat, which relies upon totally on the fleet’s age. CLCO’s fleet is under ten years outdated, so its working threat because of surprising breakdown is comparatively low.

I used the volatility over the previous few weeks to purchase extra CLCO shares. A extra strong LNG demand pushed by Asia and a deficit of LNG carriers with up-to-date propulsion act as tailwinds for CLCO. The corporate is completely positioned with its high quality fleet. I give CLCO a Robust Purchase ranking.