Wirestock/iStock Editorial by way of Getty Pictures

Funding thesis

Brembo (OTCPK:BRBOF, OTCPK:BRBOY) is an Italian firm, recognized all over the world for the manufacturing of cutting-edge braking techniques.

Within the automotive parts sector (dominated by large corporations with monumental vary of merchandise) Brembo gained its management place by specializing in its area of interest, boasting robust technological edge and clever advertising methods. Whereas its sector typically fails to excite buyers because of its cyclical nature and modest revenue margins, Brembo stands out as a promising funding alternative, with development (historic and potential) larger than opponents.

My funding thesis is centered on the transition section that Brembo is experiencing, characterised by vital manufacturing and technological investments; I count on these tasks to drive necessary income development and to draw market consideration on the corporate over completion. Whereas the complete affect of those initiatives will not be felt till 2025 and past, the present interval for my part represents a chance to an “early entry” within the firm, permitting buyers to use all the corporate’s future development. Within the meantime, Brembo’s robust monetary place and enticing dividend yield can nonetheless ship good returns.

In abstract, Brembo’s management market place and ongoing investments make it a gorgeous selection for buyers looking for development within the automotive sector, with the added potential of changing into a really attention-grabbing dividend payer sooner or later.

Enterprise macro-analysis

Brembo’s enterprise mannequin is so simple as it’s efficient: a powerful give attention to a single equipment amongst all these current in a car, and the continual search of utmost high quality. This mission is supported by the corporate’s lengthy historical past in braking manufacturing and continuous investments in R&D, which assure a deep know-how and cutting-edge applied sciences, on the very prime of the sector.

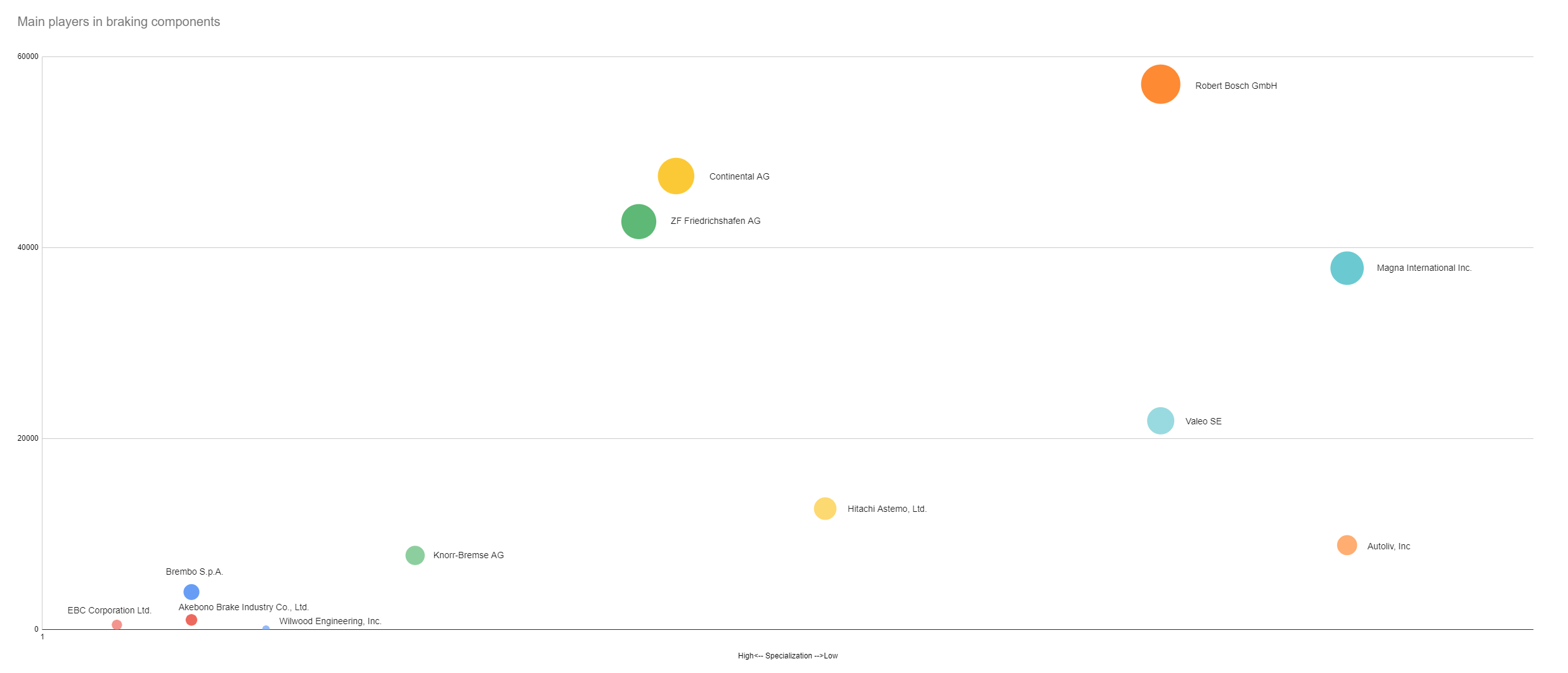

Brembo can then make the most of its robust model: Whereas the most important opponents within the trade are large conglomerates that always prioritize volumes over branding of their merchandise, direct opponents centered on braking techniques are considerably smaller in dimension (typically not even publicly traded), which subsequently lack the visibility and advertising effort Brembo might afford.

Gamers within the braking trade, by Income (Y) and Specialization (X); on the X axis, extra on the best means much less give attention to braking (Graph by the Writer)

This mix ensures Brembo an undisputed management place in its market area of interest, particularly within the premium and sport cars sectors.

The corporate’s market management is especially evident on the earth of motorsports, the place it monopolizes main international competitions:

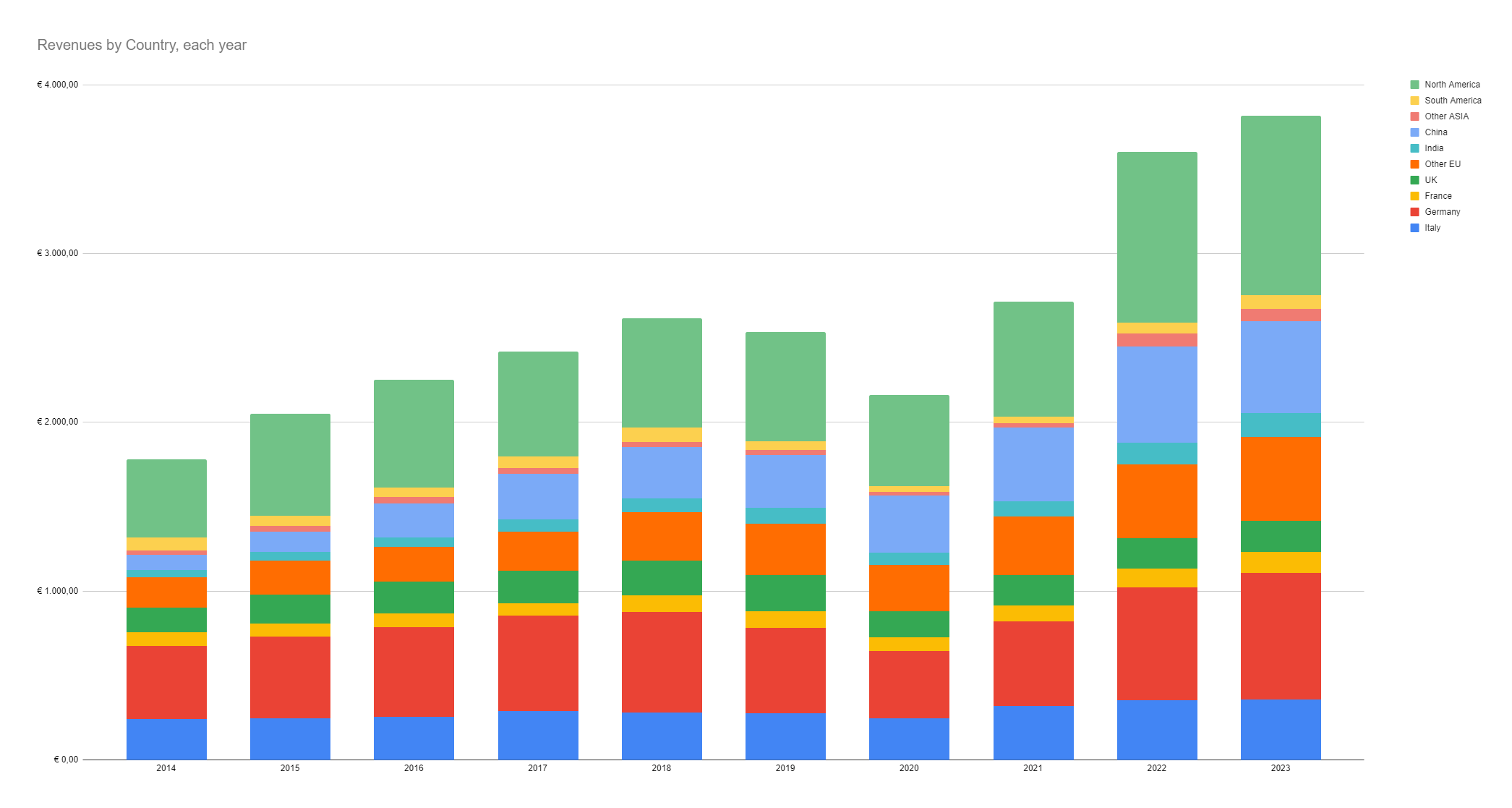

Lastly, Brembo’s international diversification technique (each when it comes to gross sales and manufacturing) has traditionally confirmed efficient in mitigating the cyclical slowdowns of single markets, and on the similar time introduced the corporate’s manufacturing geographically nearer to that of its prospects.

Whole Income by geography (Knowledge from Brembo FY report, graph by the Writer)

Monetary

Let’s check out the monetary historical past of Brembo

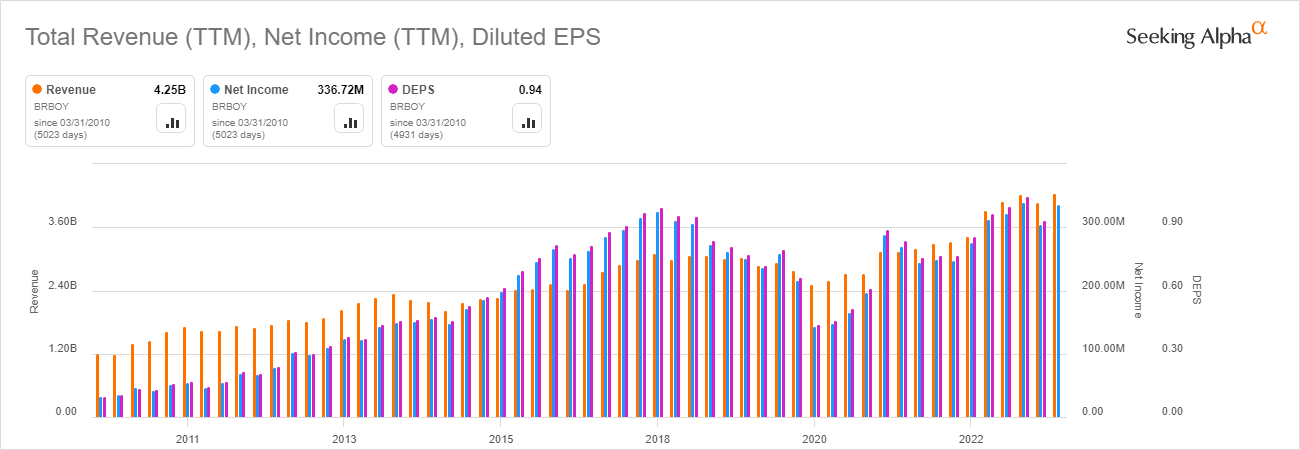

Brembo’s primary monetary numbers (Knowledge and graph by Looking for Alpha)

Ranging from 2010 (roughly after the 2008 disaster years) Brembo noticed its revenues rising by roughly 350%, with some ups and downs brought on by the cyclicality of its enterprise. It is value to spotlight that even throughout recession phases the corporate managed to stay worthwhile (constructive web revenue): this latter issue has contributed to the constant development (or a minimum of upkeep) of dividends.

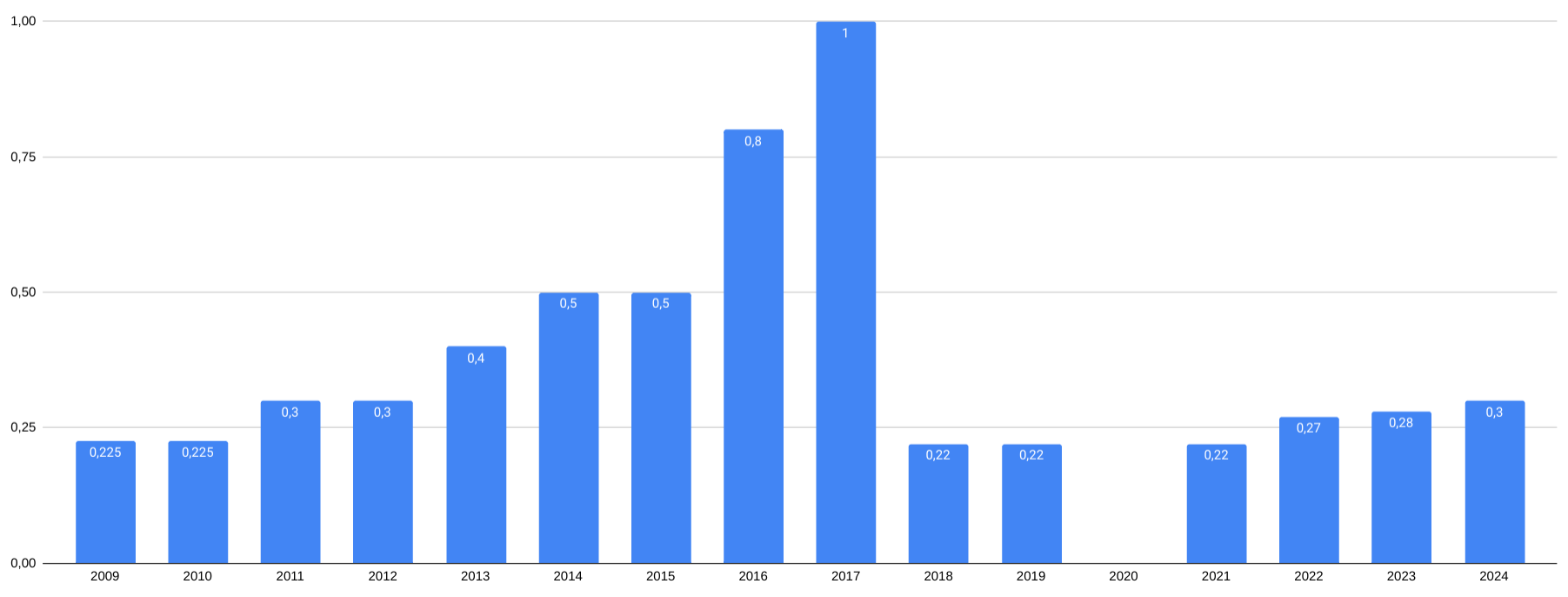

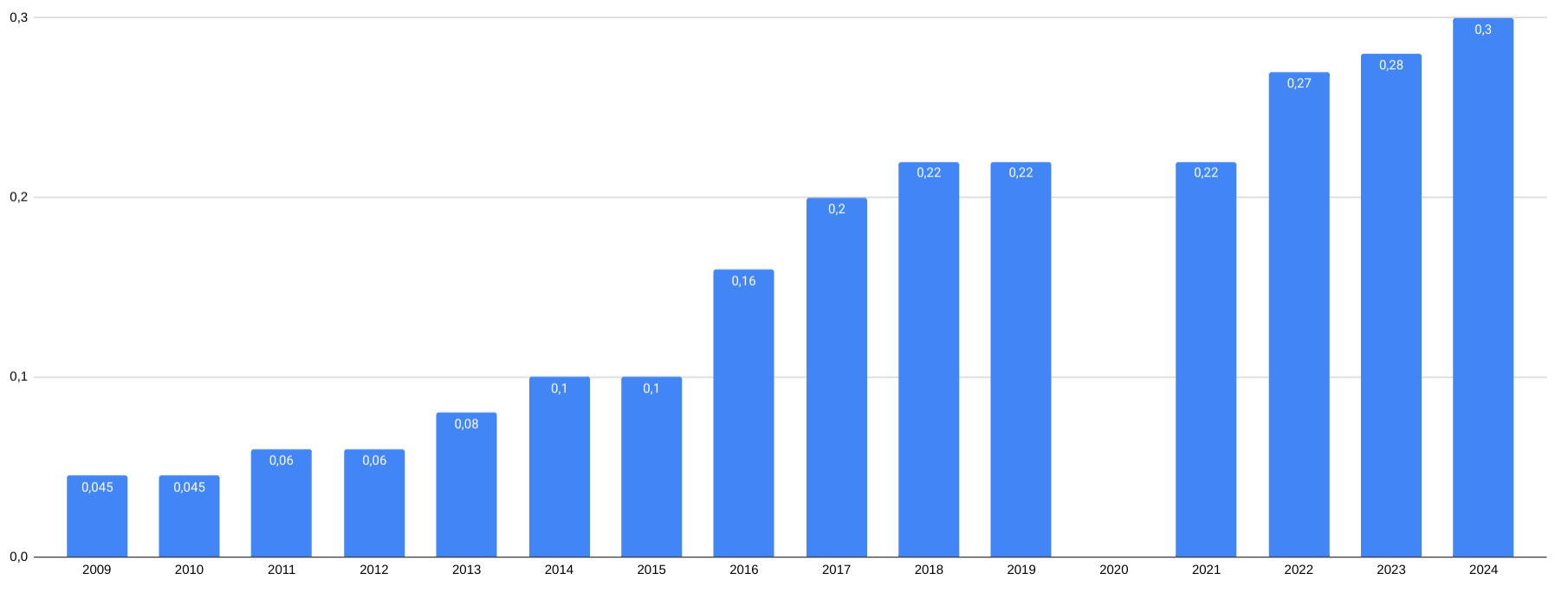

Brembo yearly dividend per share (Knowledge from Brembo FY report, graph by the Writer)

Brembo yearly dividend per share (adjusted earlier than 2017 for 1-for-5 cut up) (Knowledge from Brembo FY report, graph by the Writer)

From these graphs, we are able to see the historical past of the corporate’s dividend-per-share, which grew with a median 13% YoY share from 2009 (adjusted after 2017 1-for-5 cut up), with a single drawdown in 2020 for the Covid scenario.

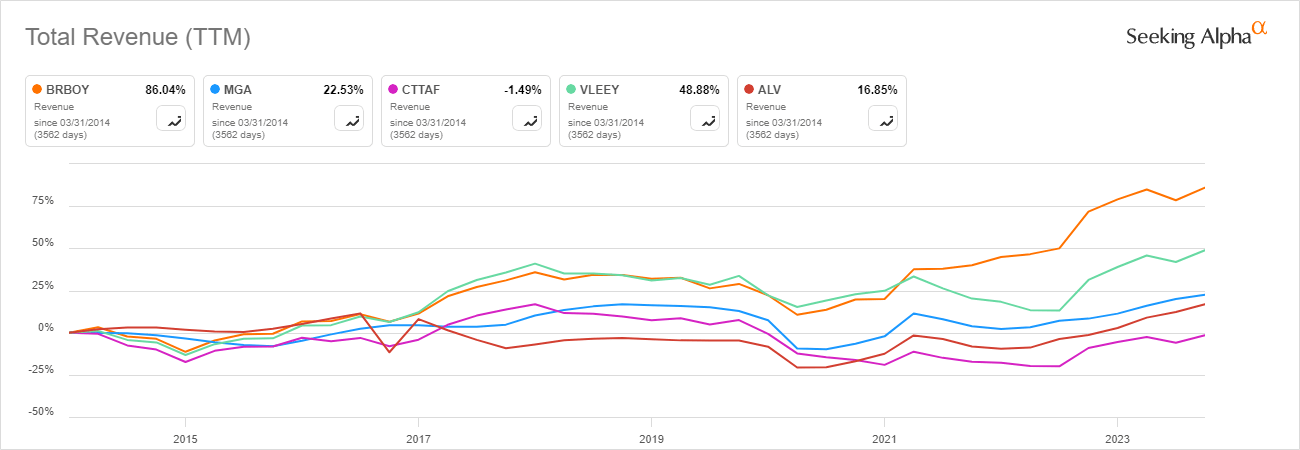

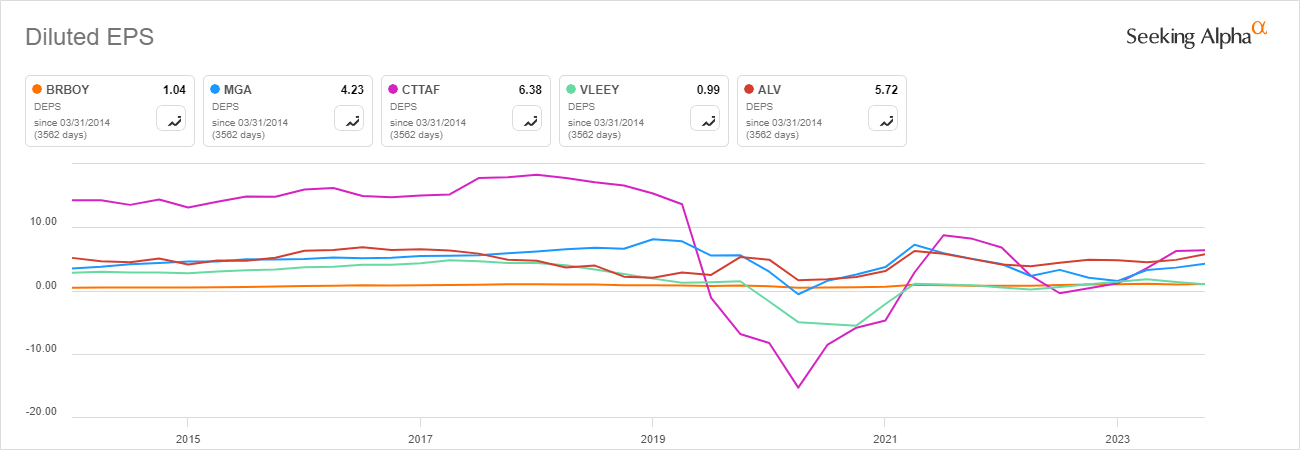

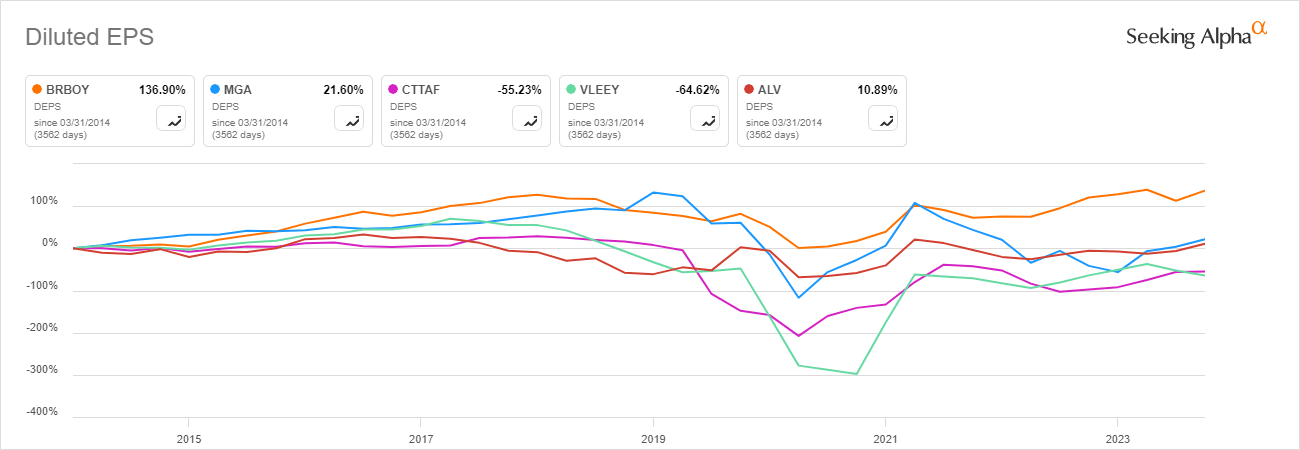

Now that we summarized the corporate previous performances, let’s attempt to make some comparability between Brembo and the “big players” of its sector: as now we have already noticed, the automotive element market is dominated by a lot of large corporations, every producing nearly all the parts we might discover in a car; in such a saturated market, earnings margins for the gamers are often lowered, as normally the first aggressive driver is worth. This, mixed with the cyclical nature of the enterprise, results in very “volatile” earnings, which for some corporations even turned destructive prior to now years.

Brembo, even when nested on this atmosphere, because of the “high-end” section, good geographical diversification and larger flexibility and effectivity because of its comparatively small dimension, exhibits extra secure financials than its bigger opponents, paired with increased development fee. The opposite “side of the coin” of this elements is the exclusion of Brembo from the huge “cheap car” sector, the place worth is extra necessary than high quality, and the place subsequently the corporate can not consider competing with the “giants” talked about above.

These details are clearly seen in these few graphs:

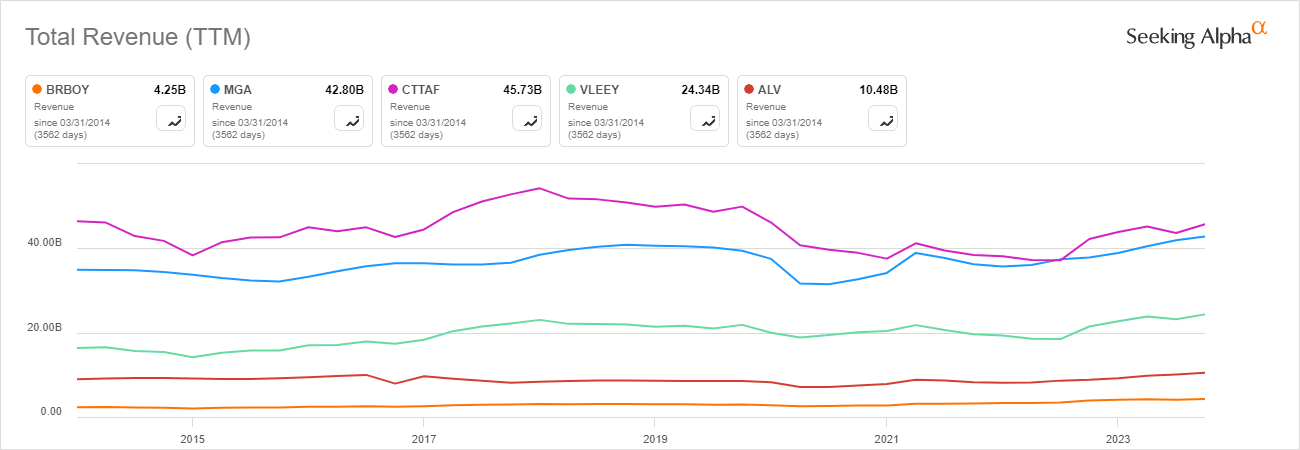

TTM Whole income (linear) for Brembo and primary opponents (Knowledge and graph by Looking for Alpha) TTM Whole income development (share) for Brembo and primary opponents (Knowledge and graph by Looking for Alpha) EPS development (linear) for Brembo and primary opponents (Knowledge and graph by Looking for Alpha) EPS development (share) for Brembo and primary opponents (Knowledge and graph by Looking for Alpha)

Ranging from the primary graph, we are able to see that Brembo is a a lot smaller firm by income than opponents, however on the similar time had an even bigger development fee within the final years.

In the identical approach, we are able to see how at the moment it has a decrease EPS by absolute worth, however how over the past years it had a gradual development which outperformed the opponents.

Progress drivers (Highway to 2025)

On this part, the very core of my thesis, I need to spotlight the details which make Brembo a gorgeous selection for the long run.

The corporate has vital and difficult investments underway, with many of those tasks anticipated to be accomplished by mid-to-late 2025; these investments are each “traditional” will increase of manufacturing capability and extra “disruptive” launches of latest applied sciences, as nicely a major company reform: upon completion of those tasks I count on a rise of volumes and (possibly much more necessary) market curiosity on the corporate.

I’ll summarize among the most noteworthy tasks, many of those info (and plenty of extra) are from 2022 FY conference transcript and 2023 FY convention transcript.

New manufacturing vegetation: Mexico, Poland, China, Thailand

Mexico: Brembo’s funding in Mexico goals to double manufacturing capability within the Nation. The works are already completed, and the primary manufacturing started within the second half of 2023. Is predicted to enter full manufacturing in 2024, with an affect of 100 million/12 months on revenues when at full-speed.

Poland: Brembo plans to open a brand new forged iron foundry in Poland, which ought to change into the corporate’s most modern and technological. The primary pour is scheduled for the primary half of 2025.

China: Brembo plans to double its manufacturing capability additionally in China, with manufacturing anticipated to start out within the second half of 2025. Though no indication on revenues affect has been offered from the corporate, I keep in mind that China at the moment represents roughly 14% of the corporate’s revenues.

Thailand: Brembo plans to open a brand new manufacturing facility in Thailand centered on brakes for the motorbike section, with manufacturing anticipated to start out within the first half of 2025. The manufacturing facility will probably be strategically positioned close to the key motorbike producers for the ASEAN market, in a brand new Nation for the corporate.

Sensify

SENSIFY is the following “big thing” for Brembo: the venture (about which Brembo nonetheless maintains strict confidentiality) was officially launched in 2021 and, after a protracted testing and advertising section, ought to arrive available on the market between the top of 2024 and the start of 2025. It is a refined, all-encompassing solution designed for full management of the braking system, which use state-of-art built-in sensors and AI.

It’s essential to spotlight that SENSIFY goes past merely stopping a car, it additionally contains elements associated to highway holding and car management, subsequently it’s carefully linked to the most recent autonomous driving applied sciences, the place autos should adapt to exterior circumstances of the highway and surprising occasions with out with the ability to depend on the direct intervention of the driving force.

This product represents a major step for Brembo, which ventures into a brand new “disruptive” sector: though inserted within the braking “area”, SENSIFY in truth marks the transition from the normal “mechanical” enterprise to a brand new “technological” one. This transfer might have an ideal “grip” available on the market given the doubtless increased revenue margins and on the whole the curiosity it might create from buyers.

M&A, Brembo Enterprise and the brand new Netherland workplace

This subheading would possibly seem to be a mixture of completely different subjects, nevertheless it really displays some necessary steps taken by Brembo in a single course.

As a primary step, within the second half of 2022, Brembo launched “Brembo Venture“, a enterprise capital unit aimed toward supporting and integrating promising startups and new applied sciences into the corporate. Among the many first entries into Brembo’s “area” now we have PhotonPath (photonics), Agade (exoskeletons, robotics and synthetic intelligence), Infibra Applied sciences (fiber optic sensing) and Petroceramics (carbon-ceramic supplies).

Then, within the second half of 2023, Brembo (considerably surprisingly) determined to move its registered office to the Netherlands, and accomplished the operation by the top of the 12 months. Brembo assured everybody that the fiscal headquarters will stay in Italy, an indication that this transfer was not a query of cash, however (as declared by the corporate) of guaranteeing higher governance circumstances because of the extra favorable Dutch laws. One of many primary benefits that Brembo is considering is the “strengthened voting right” offered by the brand new company kind, which provides extra voting energy to secure shareholders with consequent larger management for historic possession within the occasion of acquisitions and mergers.

General, I see all these “movements” as a consequence of Brembo’s option to “attract” and “include” within the firm know-how and applied sciences that would be the way forward for the automotive trade. These choices align with what Brembo’s CEO, Matteo Tiraboschi, stated within the FY 2022 convention name:

“We focus on developing in-house knowledge and anticipating market trends and client needs. What we can’t learn fast enough, we bring into the company from outside […] Continuous innovation, client-driven solutions, and sustainable development are key factors for Brembo’s future.”

One final attention-grabbing situation could possibly be the one across the rumor (which have been circulating for a while) a couple of potential merger with one other giant Italian firm, Pirelli, recognized for the manufacturing of tyres.

In February 2023 Brembo (which maintain round 6% of Pirelli’s capital) signed a shared voting agreement with Camfin, a significant Italian shareholder in Pirelli which holds nearly 20% of the corporate; this deal offers them a complete voting weight of 26%, second solely to the 37% held by Chinese language firm SinoChem. Though they’re solely rumors for the time being, the market may be very on this potential settlement, as a result of evident complementarity of the sectors (brakes and tyres), moreover there can be few obstacles at authorities degree since each are nationwide corporations.

EV market

This ultimate part is extra a mirrored image on the way forward for the automotive trade somewhat than an organization venture. The sector is getting ready to a significant transformation, maybe the most important it has ever seen: the spreading of electrical autos is predicted to show many conventional parts out of date, posing a problem to corporations that don’t adapt their manufacturing processes.

Brembo has a bonus, as it’s possible that braking techniques will stay an integral part sooner or later; in truth the shift to electrical autos (which are usually heavier than conventional ones) will most likely mark a rising demand for performing braking techniques that may deal with the elevated weight. Moreover, new autonomous driving applied sciences would require “intelligent” braking and traction management techniques that may want to have the ability to reply to surprising occasions with out counting on the driving force’s response, opening up new enterprise alternatives for the corporate.

Truthful worth estimates

Let’s now attempt to assign a good worth to Brembo’s shares utilizing DCF mannequin.

I want to notice that these calculations ought to at all times be thought of as a reference, somewhat than a worth goal: the true worth of the corporate will probably be, as at all times, decided by the market.

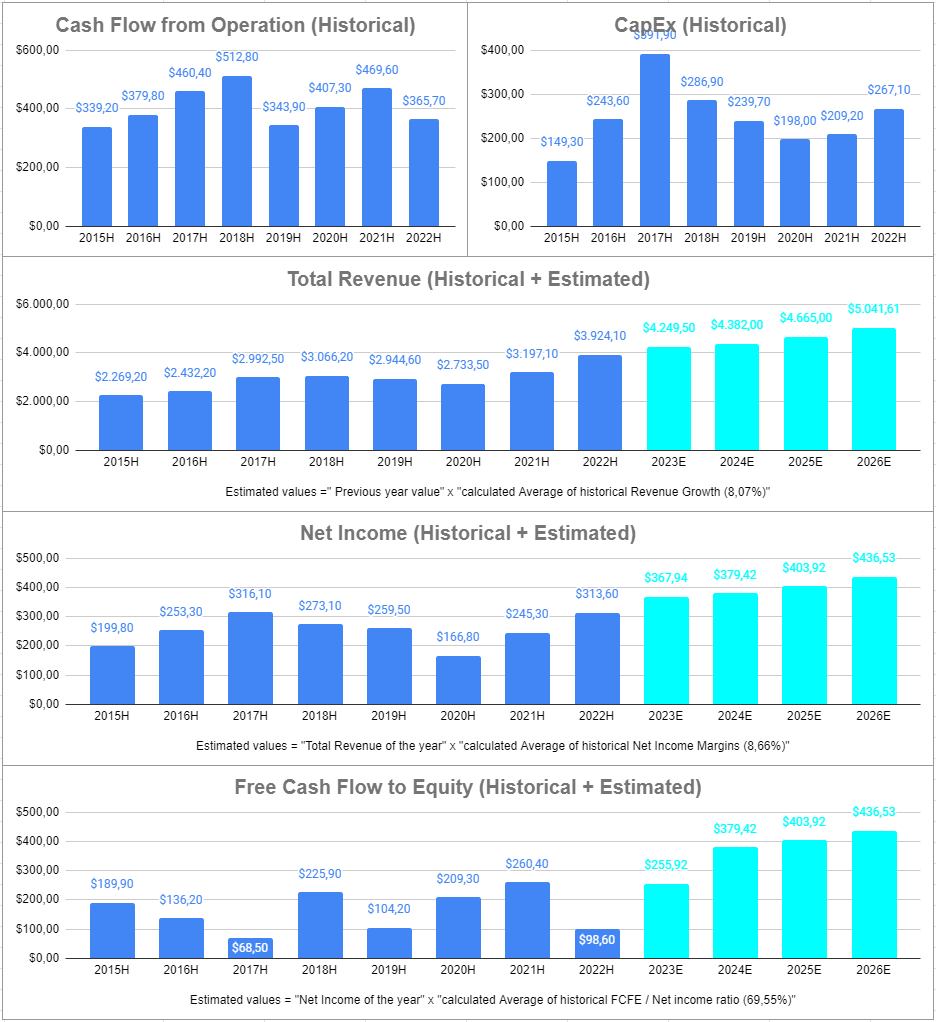

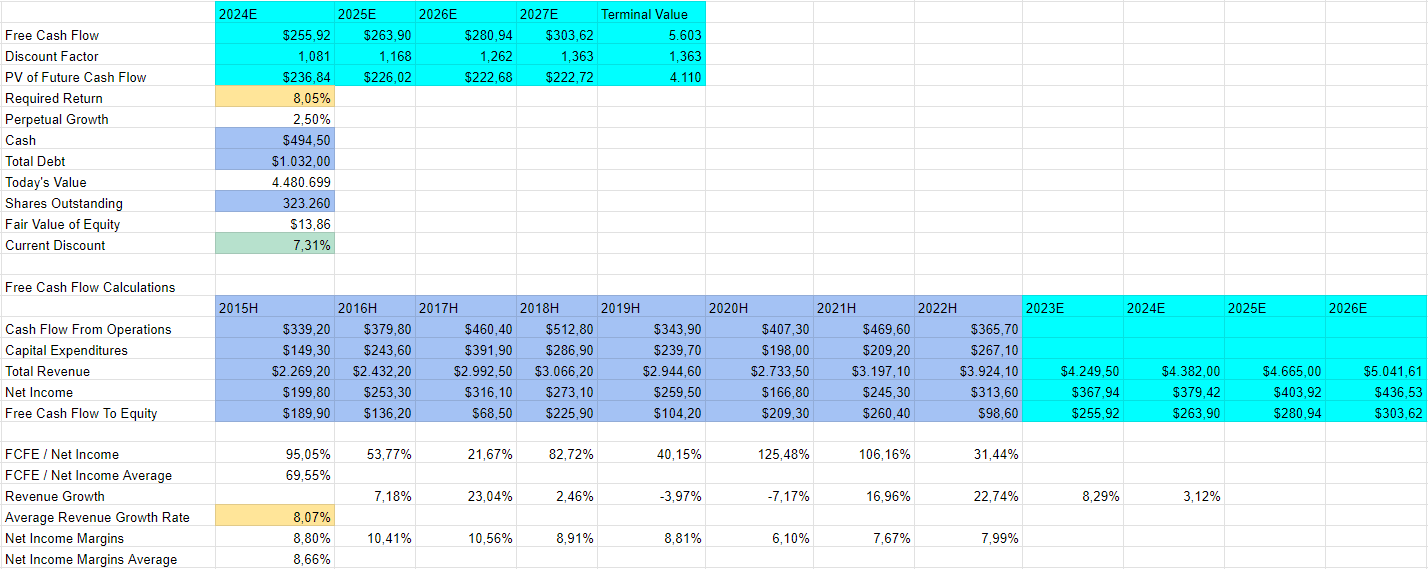

Here’s a visible recap of the principle knowledge used for DCF calculation (historic in darkish blue; estimated in lighter blue).

Knowledge utilized in DCF mannequin (Knowledge from Looking for Alpha, graph from the Writer)

All historic knowledge is from SA (in USD tens of millions), I often don’t like to tinker an excessive amount of on DCF averages and numbers as a result of I believe that even when typically DCF outcomes could possibly be deceptive, modifying the bottom might result in biased outcomes. Subsequently, I left all averages used within the mannequin as calculated from historic knowledge; the required return is calculated on 2023 WACC, I discover the 8,05% quantity an excellent worth for an organization in automotive sector.

DCF calculation (Knowledge from Looking for Alpha, spreadsheet from the Writer)

The outcomes (round 12,12€) appear to point a good worth nearly completely in step with market valuation of the corporate. As for Wall Road analysts (supply: WSJ), the corporate is at the moment rated as Chubby, with a goal worth of €13.69, simply barely extra optimistic than my calculations. The P/E ratio of roughly 12.5 falls within the industry average, in step with the key gamers of the sector.

In conclusion, I take into account the corporate accurately valued by the market, as one might count on in a reasonably “predictable” sector akin to Brembo’s. Whereas I do not anticipate vital worth will increase within the brief time period, if costs proceed to carefully comply with monetary knowledge we might count on a major enhance to the inventory worth upon completion of ongoing tasks.

Threat evaluation

So far, I spoke concerning the causes that led me to assign a BUY score to Brembo, what I need to analyze now are the key dangers that an investor ought to take note of. I’ll attempt to comply with the identical order of the earlier half for consistency (every subsidiary spotlight dangers for a precedent part).

Enterprise macro-risks

On the macro aspect, the primary danger to be thought of is undoubtedly the cyclical nature of the reference market, carefully linked to automobile gross sales and subsequently to the general state of the financial system. Along with this, I’ve to recollect how the revenue margins within the sector are often reasonable, and the way for among the opponents they’ve even turned destructive prior to now years (see graphs within the “Financial” part).

This two elements create the annoying attribute of the reference sector of getting moderate-only development charges however with out the “safety” options of different defensive ones. For Brembo, we noticed this can be a barely much less vital drawback than for opponents (given the market section the corporate targets), however on the whole, the kind of enterprise is often not probably the most enticing for buyers.

Monetary dangers

We noticed how market cyclicality impacts Brembo in another way: being excluded from the mass car market, Brembo might characterize a extra defensive selection in case of financial slowdown, however on the similar time, we might count on it could trip much less efficiently enlargement intervals.

We might count on that in “good” market intervals the market section, the larger technological push, the lowered volumes, and the upper investments in branding would make the corporate much less worthwhile in comparison with opponents.

Dangers associated to ongoing tasks

The expansion that I count on within the coming years is the point of interest of my thesis, thus additionally an important level of verification.

Whereas Brembo sector will not be probably the most thrilling for buyers, it’s a sector I extremely recognize for its stability and predictability: given the traits of cyclicality and “slow steady growth”, selecting the best timing of entry can typically show to be significantly worthwhile. Two “right moments” to purchase on this sector are often at the start of a powerful expansionary financial section or if an organization is buying and selling at a reduction; in Brembo’s case, I see neither of those as true, and I justify the acquisition based mostly on the robust improvement section the corporate is experiencing.

If investments made by the corporate ought to fail to yield the best outcomes when it comes to volumes and visibility, the danger is to search out himself invested in a high quality enterprise however purchased at full worth, and having to accept moderate-only returns.

Conclusion

Brembo might not seem to be a very enticing purchase, given its reasonable historic development fee and a present worth kind of in step with the corporate’s honest worth.

Nevertheless, I recognize the solidity of the corporate, which had slow-but-steady development within the final years and which was in a position to stay worthwhile even in intervals of financial slowdown. Brembo has then secured an absolute management place in its market area of interest, because of a major technological benefit and a really robust model (the latter nearly unmatched).

Shopping for at present costs could also be somewhat “ahead of the curve” as most ongoing tasks will not be accomplished till 2025 and can then want extra time to be at full-speed. Investing now might subsequently require a interval of “patience” with preliminary reasonable returns, however might then assure to anticipate (and subsequently capitalize on) the section of development that Brembo’s investments might generate as soon as totally operational.

Above all, as soon as this section has handed, buyers will proceed to reap the advantages via dividends which, within the meantime, ought to have grown to very enticing ranges.

Lastly, I see the corporate as an ideal purchase for these searching for “unexciting” investments (i.e., not concentrating on large worth returns) however aiming to construct a high quality portfolio with a long-term time horizon to take full benefit of the dividend development this firm might present.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.