richcano

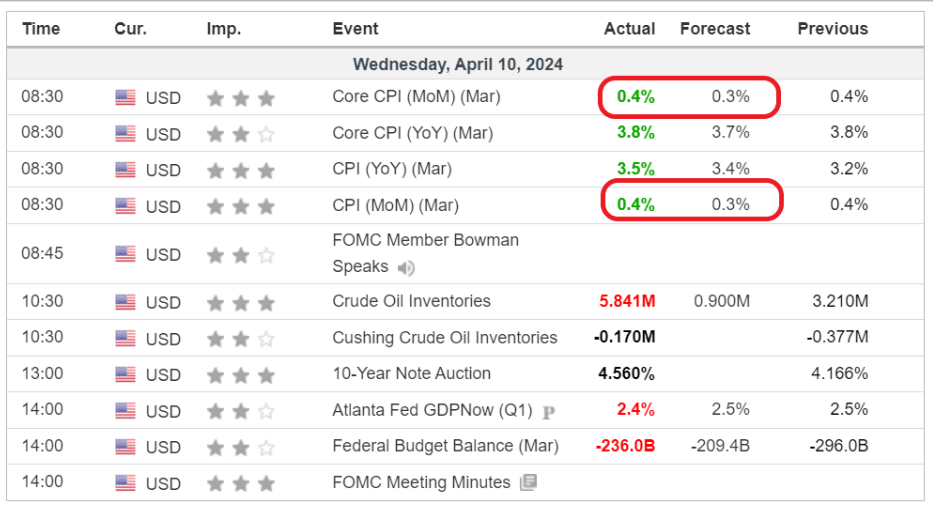

On a day (April tenth, 2024) the place the Client Worth Index (“CPI”) shocked forecasters to the upside on each headline and core readings (Determine 1), traders may naturally be inclined to hunt the protection of Treasury Inflation-Protected Securities (“TIPS”).

Determine 1 – March CPI shocked to the upside (investing.com)

Treasury Inflation-Protected Securities are treasury bonds issued by the U.S. authorities that present principal and coupon safety in opposition to inflation. The principal of a TIPS will increase/decreases with CPI inflation/deflation such that when the TIPS bond matures, traders are paid the higher of the adjusted principal or authentic principal. TIPS bonds additionally pay fastened charge bi-annual curiosity that’s calculated on the adjusted principal, so the curiosity funds are protected against inflation as nicely.

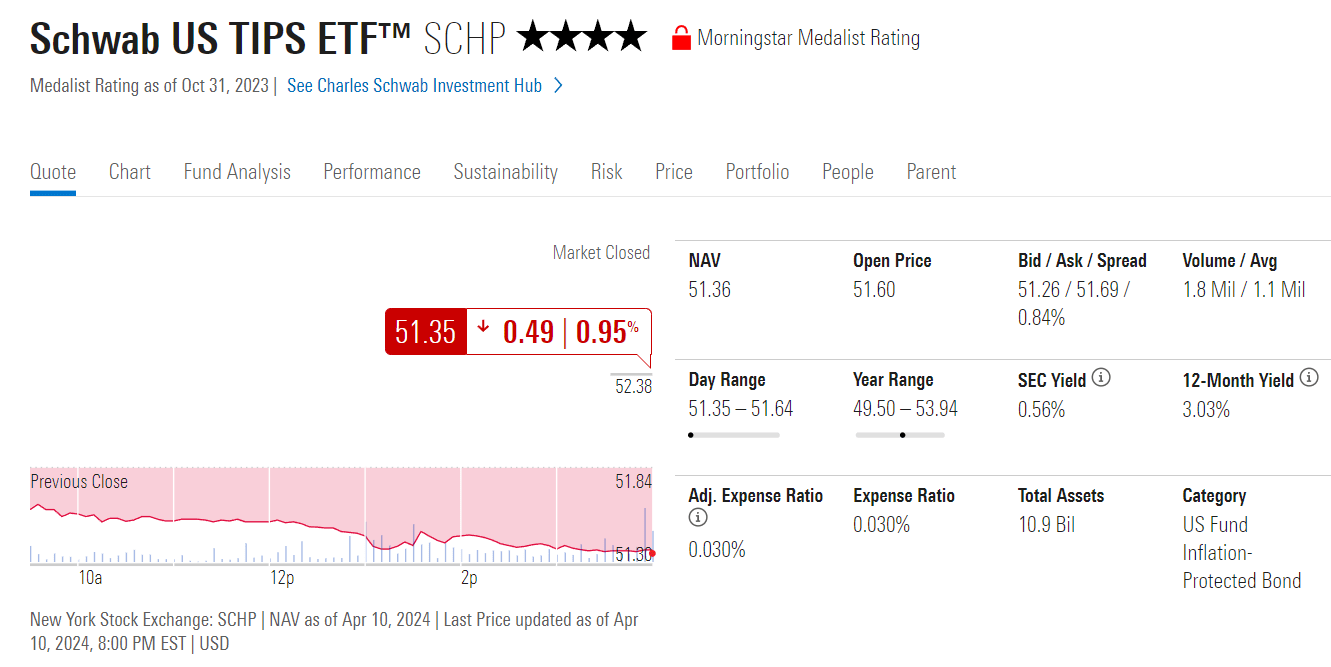

Nevertheless, holders of TIPS funds just like the Schwab U.S. TIPS ETF (NYSEARCA:SCHP) had been most certainly shocked by the market response of those ETFs on April tenth, as SCHP fell 0.95% (Figures 2).

Determine 2 – SCHP fell 0.95% on April tenth, 2024 (morningstar.com)

Was this merely a bout of panic promoting, or had been there elementary causes behind SCHP and TIP’s weak spot?

TIPS Funds Have Length Threat

As I’ve written in prior articles on SCHP and TIP, April tenth was an excellent reminder that TIPS funds have rate of interest period danger that’s not usually mentioned by analysts and traders.

Not like a single TIPS bond, which if held to maturity, will successfully defend traders from each inflation and rate of interest danger, a portfolio of TIPS bonds just like the SCHP ETF introduces portfolio rate of interest danger that’s not hedged.

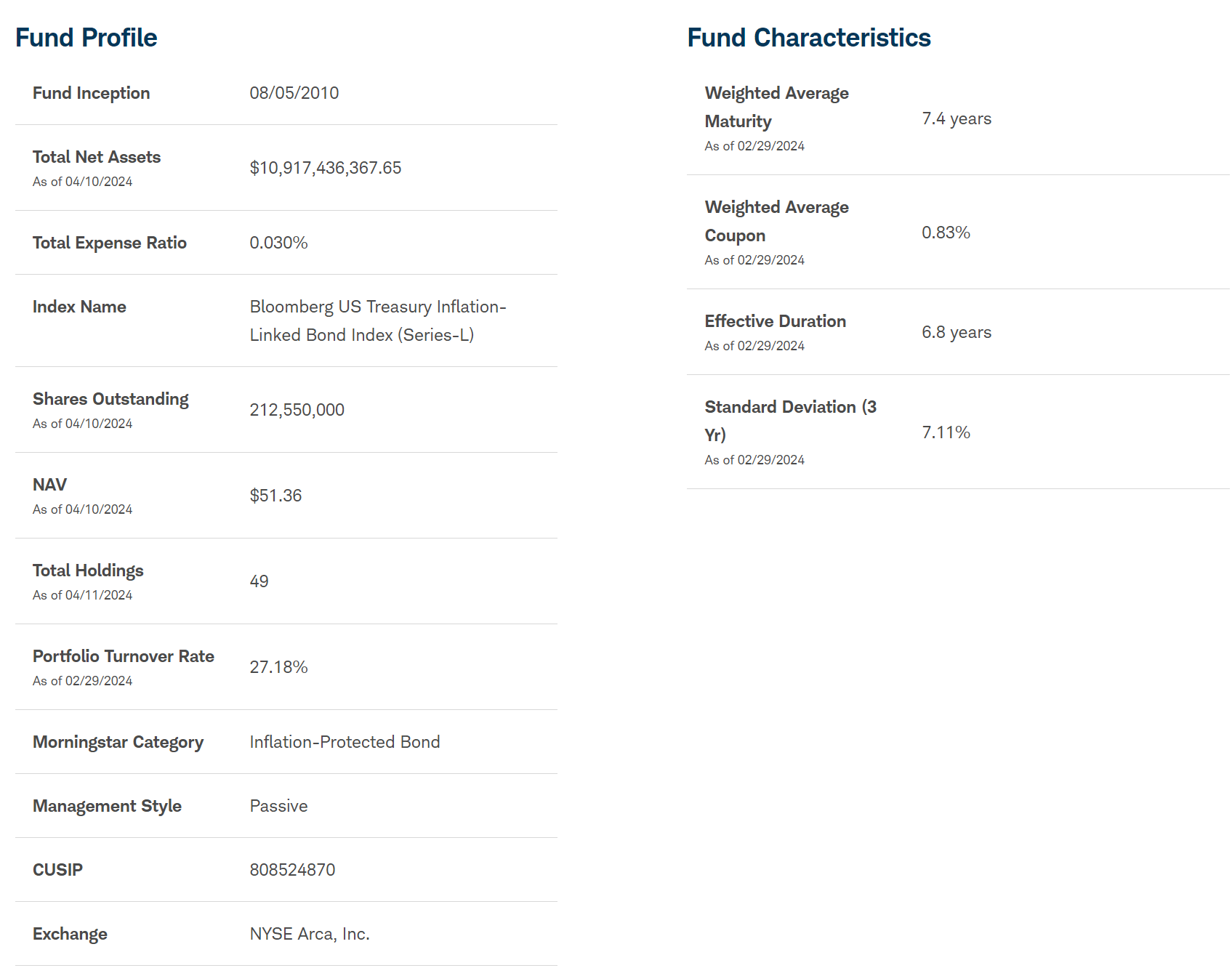

For instance, SCHP’s portfolio incorporates 49 TIPS bonds with a 6.8 12 months efficient period (Determine 3).

Determine 3 – SCHP portfolio overview (schwabassetmanagement.com)

Inflation Shock Shocked Curiosity Charges Larger

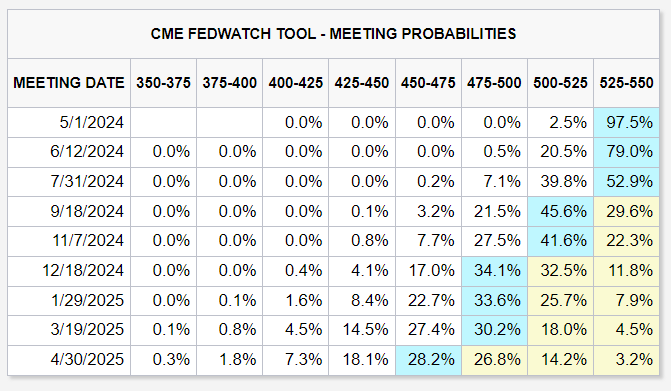

What occurred on April tenth was {that a} third consecutive ‘scorching’ month-to-month CPI shock brought about market contributors to successfully push out their expectations for the primary charge minimize by the Federal Reserve to September (Determine 4). The variety of anticipated cuts in 2024 was additionally lowered to 2.

Determine 4 – Market expectation for Fed charge minimize pushed out to September (CME)

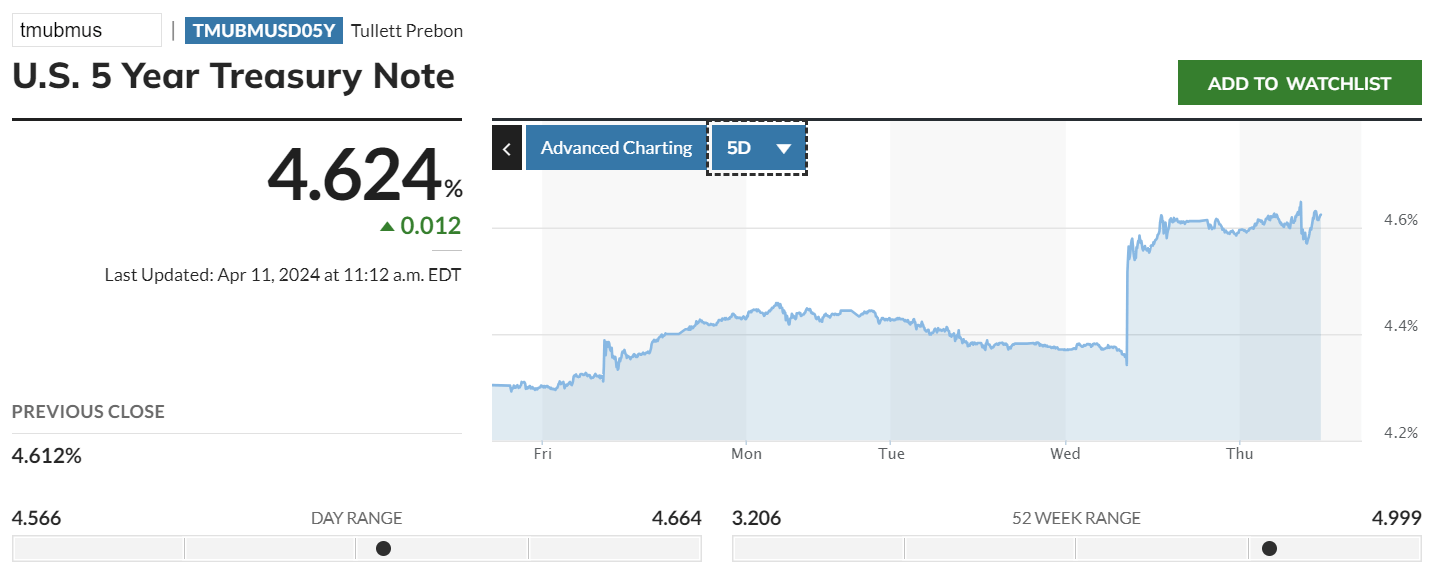

This variation in market expectations shocked rates of interest increased throughout the rate of interest curve, with 5 and 10 12 months treasury yields leaping 24 (Determine 5) and 19 bps respectively.

Determine 5 – 5 12 months treasury yields jumped 24 bps on April tenth (marketwatch.com)

So although the next than anticipated CPI studying elevated the principal on the TIPS bonds in SCHP’s portfolio, the soar in rates of interest lowered the online current worth of the ETF’s money flows.

Not like a single TIPS bond, these mark-to-market (“MTM”) declines in worth from rate of interest modifications in a bond fund is probably not recovered, because the SCHP ETF is managed to a hard and fast period. As time passes, the ETF will promote maturing bonds and substitute them with newer bonds such that the portfolio’s period is unchanged. This course of crystallizes unrealized losses from rate of interest modifications.

Uncertainty On Inflation Path Clouds Outlook For SCHP

The query now could be whether or not the newest inflation knowledge remains to be according to the Fed’s view that inflation is headed decrease however in a “bumpy” style, or whether or not we now have reached a brand new plateau of >3% core inflation with inflation probably reaccelerating.

If it’s the former, then excessive however declining inflation ought to enhance TIPS bonds’ principal and curiosity revenue whereas over time, market rates of interest ought to reasonable, which may present a ‘goldilocks’ surroundings for the SCHP ETF.

Nevertheless, if inflation has plateaued and is reaccelerating, then the Fed might have to carry coverage charges increased for longer, and will even have to boost Fed Funds charges within the coming quarters to stop inflation from working away. On this case, long-term rates of interest will seemingly should rise, which may put additional strain on the SCHP ETF.

Situation Evaluation Favours Shopping for TIPS Now

For now, my perception is that the Fed will err on the facet of inflation, because the bar to elevating Fed Funds charges after their public pivot in December could also be too excessive. With 5 and 10 12 months yields ~4.6%, I consider the SCHP ETF affords an uneven danger/reward at present valuations.

Within the base case, reasonably excessive however declining inflation readings will proceed to spice up principal and coupons for TIPS bonds, and thus the fund’s NAV. Lengthy-term rates of interest are additionally anticipated to modestly decline within the coming quarters.

On the draw back (or upside in yields), I consider ~5% could also be a quasi-cap on long-term rates of interest, because the Fed will most certainly sit on their palms until inflation immediately reaccelerates to 4-5% or increased.

Lastly, on the upside (draw back in nominal yields), if the economic system worsens dramatically, the Fed stands prepared to chop coverage charges to help jobs and the economic system. This could result in decrease nominal rates of interest and better NAV for SCHP.

Conclusion

With expectations for Fed charge cuts successfully pushed out to September, I consider long-duration TIPS ETFs just like the SCHP ETF affords an uneven danger/reward guess at present valuations.

So long as inflation doesn’t reaccelerate uncontrolled (>4%), I consider the Fed is most certainly going to sit down on their palms even when there isn’t any progress on inflation, so the draw back state of affairs is roughly 5% on long-term treasury yields in comparison with the present ~4.6% degree. Nevertheless, elevated inflation readings on this state of affairs ought to proceed to result in optimistic principal changes for the SCHP ETF, so additional NAV declines could also be muted.

However, the Fed has recommended (“2-sided risk discussions”) they could be prepared to chop rates of interest to help the economic system in the event that they see financial weak spot, even when inflation stays above the Fed’s 2% goal. This could result in decrease long-term rates of interest and a lift in NAV for SCHP.

As a result of uneven nature of this guess, I’m upgrading SCHP to a purchase.