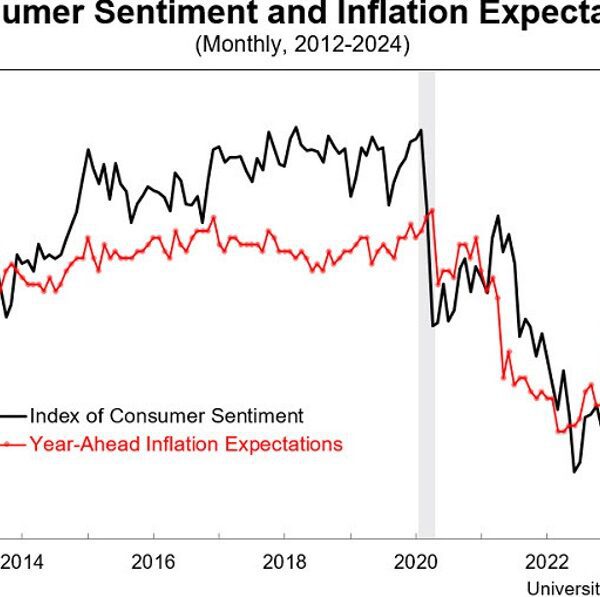

Screenwriters check with “second-act problems.” After the characters and the stakes of a narrative are established within the first act, issues can get a bit messy and complicated because the central battle is escalated earlier than pushing towards an final decision. The markets have entered such a muddled center part after a primary quarter by which the plot strains have been neat and tidy and the rally freed from issues. The primary act of 2024 had the consensus embrace a narrative of brisk financial development, a robust and rebalancing labor market, ebbing inflation, an upswing in earnings development, repeated document highs in inventory costs and the prospect of a Federal Reserve trying to trim charges into all this. A lot of this stays both true or believable, nonetheless. But a 3rd straight warmer-than-expected CPI studying final week reawakened bond-market volatility, gave an additional push to a revived reflation-asset commerce and resurfaced issues that imperfect tradeoffs may must be made amongst development, inflation, valuation and Fed coverage. The consequence was a 1.5-percent weekly drop within the S & P 500 , with Friday’s setback exacerbated no less than considerably by a collective clenching-up of danger markets on some geopolitical fear. Rally examined Every week after the S & P ended its first 2% dip in additional than 5 months, an early trace of a possible change in market character , the index retreated to the touch its 50-day transferring common for the primary time since November. It did, nevertheless, bounce off that line to shut above it for the 110 th straight session, in accordance with Bespoke, making it one of many dozen or so longest such streaks previously 80 years. Think about this check of the rally’s resilience ongoing moderately than settled. I’ve repeatedly stated this has not principally been a Fed-driven market, within the sense that it did not “need” price cuts to occur quickly or to be deep with a purpose to keep supported given the in any other case sturdy macro. This does not imply the market might simply shrug off the circumstances beneath which the Fed would retreat from its easing bias altogether this 12 months. That is as a result of the Fed merely wants inflation to quiet down only a bit — even in a still-strong economic system — with a purpose to punctuate the tightening cycle with a “normalization” reduce or two. So, if there are not any cuts, it means inflation will likely be extra cussed, which in all probability means longer-term yields would hold threatening to pinch fairness progress. Bear in mind, the pivot towards an easing bias by Chair Jerome Powell late final 12 months was so avidly embraced by the market as a result of it meant the Fed not noticed the necessity to smother development with a purpose to suppress inflation. Earlier than then, Powell was routinely saying the economic system wanted to run “below potential for a sustained period” to corral inflation. He would regularly level out that services-sector inflation was actually about wage development, so the job market may want to melt up lots to tug down costs there. Because of this the considerable drop in inflation by November — a steeper decline than the Fed had been forecasting — instantly freed Wall Road to deal with good financial information as excellent news for shares. This dynamic hasn’t been reversed, however the sign has grown a bit staticky, draining some conviction from the macro bullish case with the S & P 500 nonetheless 24% above the October low. Leaping yields, gold The jumpiness within the bond market manifests a few of this dissonance. The ICE BofA MOVE Index , the VIX of the Treasury market, so to talk, bottomed at a two-year low on March 28, the date of the final all-time excessive within the S & P 500, and has shot larger since because the 10-year yield vaulted 4.5%, earlier than settling a bit with that geopolitical bid on Friday. .MOVE 5Y mountain ICE BofAML MOVE Index, 5 years A torrent of hedging exercise additionally washed over the equity-option and VIX futures market, an indication that merchants are desperate to pay as much as defend positive factors. Gold has gone practically vertical this month, with stupendous volumes within the SPDR Gold Shares (GLD) ETF Friday simply because the gold worth put in a doable short-term shopping for crescendo, speeding from $2,400 an oz. to $2,440 earlier than recoiling to $2,360. @GC.1 1Y mountain Gold, 1-year This twitchy cross-asset motion in some unspecified time in the future might mirror a useful upwelling of dealer nervousness and a rebuilding of a wall of fear, although the center of the squall isn’t any event for such a assured forecast. In such a interval of flux, when it is a wrestle to bridge the story from setup to satisfying conclusion, it helps to return to the define by stacking up what we all know, or are fairly certain of, in regards to the present backdrop. Bull market’s backdrop First, it is a bull market, and never a very mature or excessively beneficiant one but. Whether or not one dates it to the final word October 2022 S & P 500 low or, as some desire, to final October when market breadth bottomed, the development is larger, the overshoots are inclined to occur to the upside, the pullbacks are in the end contained and buyable. The uncommon persistence and breadth of the rally (up 10% two straight quarters, no 2% dip in 5 months) from October 2023 via March strongly suggests an final peak has not been reached, primarily based on any variety of research of previous markets that behaved equally. Even so, as I wrote right here two weeks in the past once I recited a few of these stats, “In those prior 11 times the S & P entered the second quarter up at least 10%, the smallest pullback the rest of the year was 4%, and those were in the 1960s.” The smallest setback in latest many years throughout such years was greater than 6%. We’re now in a 2.7% pullback. It is protected to surmise that in some unspecified time in the future the market was going to grab on some set of credible excuses to endure an honest little shakeout at minimal. To not recommend the stickiness in CPI inflation is a mere empty excuse, however some perspective on the inflation image is price a point out. There ought to nonetheless be lagging disinflation in shelter working via coming reviews. And extra crucially, the Fed’s 2% inflation goal is predicated on the PCE measure, whose consumption-based weightings have taken it decrease than CPI. Economists see the core PCE annualized achieve coming in round 2.8% (the report is due in two weeks). The Fed members’ newest median forecast for core PCE at year-end was 2.6%, and their median anticipated variety of price cuts this 12 months was three. This isn’t an unlimited distance to journey to set the stage for a kind of “optional” price cuts to happen. The rethink of the Fed path has carried out nothing to interrupt the corporate-earnings restoration now anticipated, and doubtless required with a purpose to validate present full valuations. FactSet’s John Butters figures first-quarter S & P 500 earnings development will exceed 7% over the prior 12 months, primarily based strictly on the common margin of outperformance versus forecasts seen over the previous 4 reporting intervals. The market reactions will likely be noisy and can expose pockets of “excess belief” amongst traders in sure favourite themes. When Fastenal fell in need of expectations final Thursday, shares of this play on large industrial-capex themes fell 6.5% and dragged down WW Grainger 3.5%. But each shares are nonetheless outperforming the S & P this 12 months. As Citi US fairness strategist Scott Chronert put it on Friday, “Markets have priced in a higher probability of the Goldilocks scenario playing out this year, introducing more downside risk to ‘good but not good enough’ news… A buying opportunity may present as we progress through the reporting period if we see consistent positive surprises followed up with a rightsizing of market implied growth expectations.” Tactically, with short-term momentum damaged, a reset of attitudes is underway. The S & P 500 closed Friday at precisely the identical degree of 5 weeks earlier, on March 8 – which was maybe the second of most investor confidence within the “we can have it all” thesis. The day earlier than, Powell had stated the Fed was “not far” from with the ability to trim charges, then on the 8 th a near-perfect employment report cemented the soft-landing consensus. The market, in its manner, is doubling again to check these premises.