We Are

Opener

I make investments actively within the inventory marketplace for two main causes. Firstly, and maybe most clearly, I search to beat the market and create wealth over the long run. Secondly, I genuinely take pleasure in selecting shares. I derive satisfaction from estimating my odds, studying about nice companies, and sharing my insights right here.

Certainly, there are quite a few methods to revenue available in the market. Buying and selling, for instance, provides potential returns, albeit with unfavorable odds – although it is not a path I pursue. Basic worth investing entails shopping for undervalued shares, requiring a eager eye to discern that their present points are usually not vital. This method calls for excessive ability and expertise. Then there’s high quality development investing, or GARP (development at an inexpensive worth), which, for my part, is the optimum method for personal buyers because of the benefits they possess over massive funds, akin to endurance, freedom to take a position with out restrictions, and an limitless time horizon. For my part, worth performs require increased technical abilities that I am unsure each retail investor has. If you purchase a top quality firm, you remove enterprise threat to a a lot larger extent, in distinction to a worth play the place the enterprise may very well be poor, however the worth is wonderful.

Whereas my predominant focus lies in high quality GARP investing, I sometimes delve into worth performs, notably in high-quality companies. As we speak, I will share two GARP alternatives I’ve not too long ago invested in, however one might describe them as a worth play if they like.

Oddity Tech

That is the most important holding in my portfolio. I not too long ago added a big quantity in the course of the drawdowns, which I view as merely background noise for the long-term thesis and alternatives to decrease my common price. My purpose is to put money into long-lasting compounders. I do not essentially have to discover a firm that may return 100 occasions the cash I invested, however I do wish to discover companies that may compound at the next charge than the market over the long run. Nevertheless, Oddity (ODD) is an organization I can see returning ten occasions my cash in a decade. To see this firm at a $20 billion valuation in 2034 would not be an unrealistic dream, though very optimistic.

Let me provide you with a brief pitch: Oddity is a founder-led, high-growth enterprise aiming to disrupt the sweetness trade. Their technique primarily revolves round leveraging expertise, using a differentiated promoting method, and providing high-quality merchandise. Presently, it has two profitable manufacturers, IL Makiage, and SpoiledChild, with two extra on the way in which. When you seek for IL Makiage/SpoiledChild on Google and discover the websites, you will encounter a complete totally different expertise than with different magnificence manufacturers. At Oddity, a lot of the main target is on the tech aspect – the best way to promote you the perfect product by way of machine studying and algorithms. You do not simply purchase merchandise blindly; you’ll be able to even strive before you purchase.

Now, you would possibly say these are simply advertising and marketing gimmicks, however the merchandise themselves are fairly good, with nice evaluations on each manufacturers on Trustpilot. You may see it in Oddity’s numbers – the corporate is rising like a weed, and the CEO, Holtzman, is continually speaking about slowing down development to a 20% annual tempo. What number of corporations have you ever heard of attempting to sluggish development?

Turning to the primary quarter. As we mentioned final yr, we intentionally slowed the enterprise down within the again half of 2023 with a purpose to tempo our development, whereas our groups centered on big preparations for 2024.

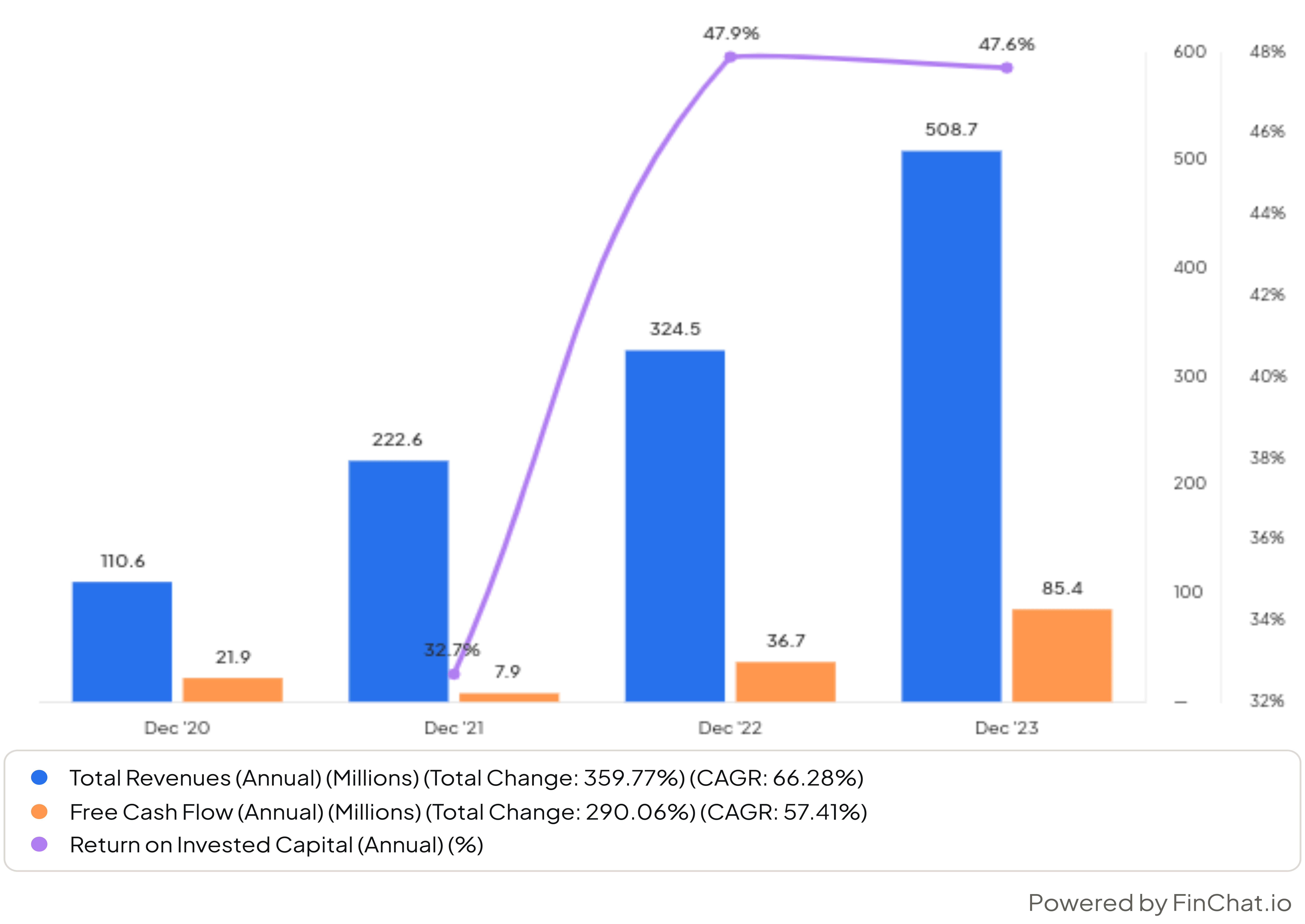

ODD is rising (finchat)

The distinctive half right here is that the corporate is tremendous worthwhile, with a 20% EBITDA margin goal which they’ve exceeded, and a 47% ROIC (!). The mix of stable top-line development and excessive ROIC is a profitable one in lots of instances. The bonus is that Oddity continues to be small, and the sweetness market is big. I see loads of development forward for Oddity, with numerous earnings.

Now, guess the valuation – you assume it is most likely uninvestable with a sky-high valuation, proper? Not fairly. Since Oddity is a small Israeli firm, I assume People aren’t comfy shopping for it and not using a large margin of security, particularly with the latest tensions with Iran that additional dropped the inventory. The actual fact is, as an Israeli, there shall be no impact on Oddity. The overwhelming majority of gross sales are in North America, and the Israeli employees are within the R&D phase and may make money working from home in case of a large struggle right here, plus their workplaces are within the comparatively secure Tel Aviv.

Again to valuation, the truth that a affected person investor can now purchase the inventory at 23 occasions NTM earnings is absurd to me. Take into account that gross sales grew 44% final quarter. If I assume 20% top-line development wanting ahead, which is definitely a lot decrease than the expansion Oddity has offered, with this NTM PE I get a 1.1 PEG. Sure, it is not the low worth we noticed in November, which I nonetheless remorse not understanding concerning the inventory again then, however in my opinion, it’s low-cost for a enterprise that may develop profitably with an enormous TAM forward.

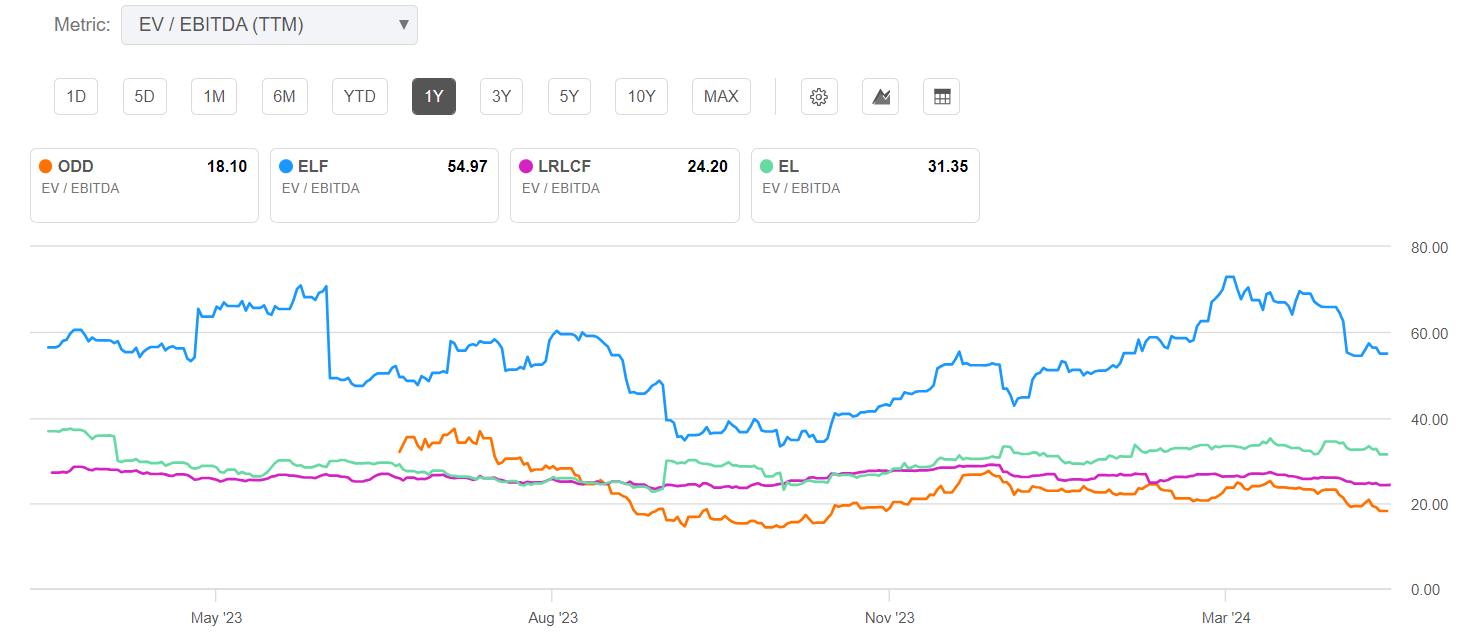

For my part, there are twin engines right here – a number of enlargement in addition to earnings development that may final. Only for comparability, it has the bottom a number of amongst friends like L’Oréal, ELF, and Estée Lauder, regardless of rising with the very best ROC and probably the most room for development. Perhaps I sound too bullish, however there are dangers, primarily within the lack of model relevance, shopper style, and competitors.

EV/EBITDA (looking for alpha)

You may additional dig into the corporate within the following article I wrote in January.

Lululemon

Properly, within the case of Lululemon (LULU), after all, I do not anticipate a 10X return, however I do suppose it should outperform over the long run. Right here, it’s affordable to imagine that the market will stabilize after the latest drop for the reason that report, and can perceive that there’s a possibility for dual-engine development, each in multiples and earnings. I consider the market will finally appropriate itself, because it’s the character of Mr. Market to initially punish, then reassess, and doubtlessly appropriate misjudgments. This adjustment would possibly happen inside a month and even six months, but when the enterprise performs effectively, it is certain to occur. When it does, the turnaround might be swift. For example, after the report, Oddity skilled a 12% decline, however inside just a few days, all losses have been recouped as rational buyers acknowledged the optimistic features of the report (this was earlier than the tensions with Iran). I anticipate that quickly the market will acknowledge Lulu’s potential, maybe spurred by a catalyst.

Lululemon is a high-quality firm and a uncommon, long-lasting winner within the vogue area. The market punished it within the final earnings report because the steering was weak. Properly, Lulu’s valuation has been stretched for some time now, and the inventory hasn’t climbed for 3 years. Nevertheless, the valuation has been stretched for a great motive. There are usually not loads of companies on this trade which have managed to take care of a robust model with excessive returns on capital and development for such a very long time, like Lululemon. In fact, the large mannequin is Nike (NKE), which has a robust model that doesn’t deteriorate for many years. I believe the market is a bit pessimistic about Lulu’s future. Sure, the expansion most likely will not be on the 20% CAGR as we’ve seen in the previous couple of years. However at a 15% bottom-line CAGR, together with buybacks, it will likely be above market expectations and can probably result in a number of enlargement or a return to its imply.

What are the explanations that would propel such development? Firstly, it’s a premium, super-strong model with loads of development forward. It nonetheless has loads of untapped markets it might develop into. Israel is an instance. They’ve just one retailer right here, in one of the well-known squares in Israel, which can be a means of selling. Curiously, the rising competitor, Alo, opened proper subsequent to it.

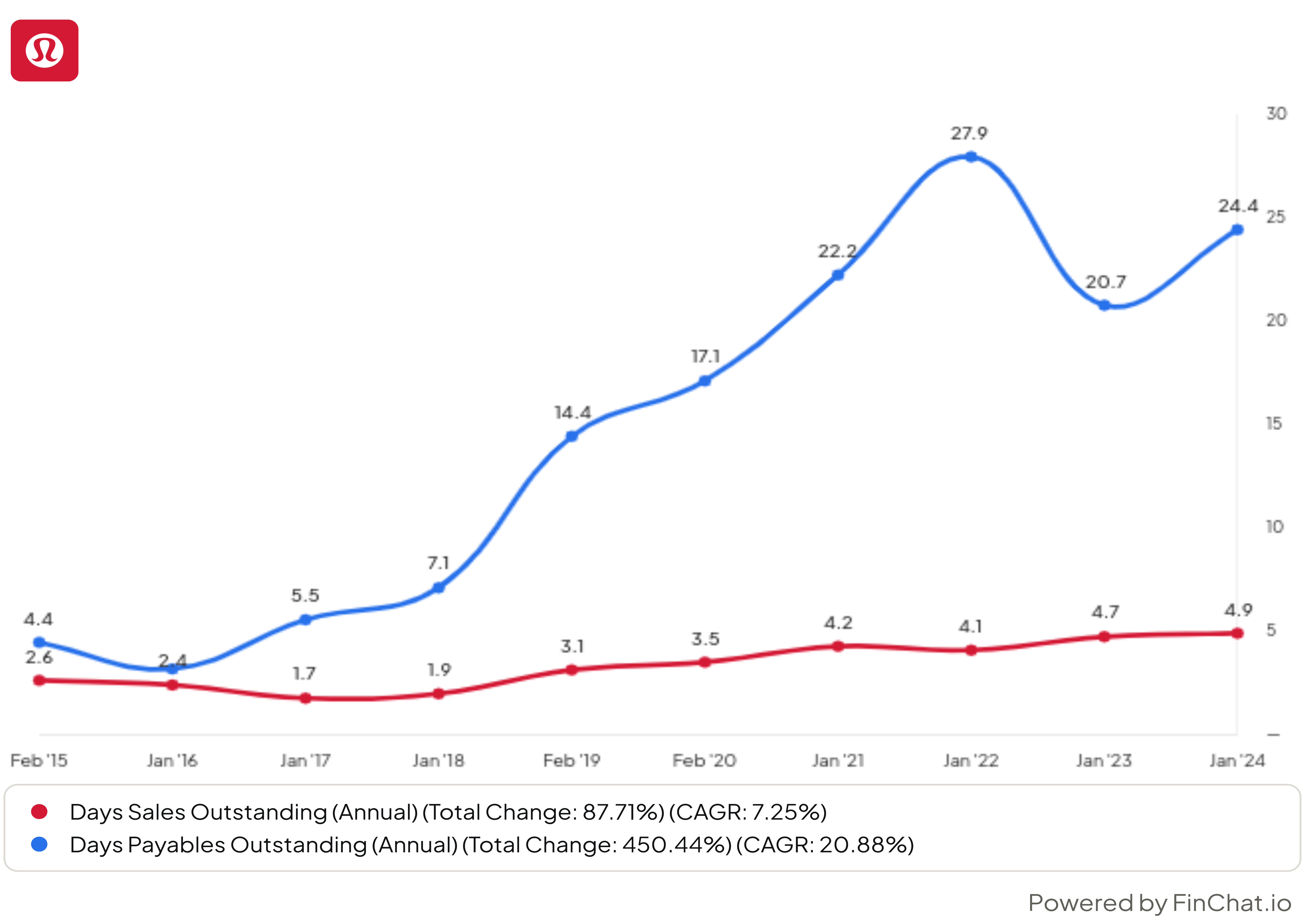

Lulu has a working capital benefit. It has detrimental working capital, which implies that like a great retailer, it’s amassing money earlier than paying suppliers, with a DSO of 5 and DPO of greater than 20. It’s a DTC vendor and is doing what Nike has been dreaming of and dealing on for years. It has greater than 40% of income by way of its e-commerce ventures. Nearly all of gross sales come from North America, so there may be loads of world enlargement forward. It’s also increasing into different markets like males’s put on, mountaineering, informal put on, and extra.

Unfavorable WC (finchat)

It’s the super-strong model energy main it ahead, together with premium costs. Premium is the center floor between mass-market manufacturers like Nike and luxurious manufacturers like Dior (OTCPK:LVMHF), and I believe Lululemon is the proper model for it. I requested my girlfriend’s associates what they consider the model. First, the value is simply too excessive for them, nevertheless it additionally makes them need it due to the standard and standing image. Considered one of them moved to the US and acquired a pair. She says it is a standing image, and he or she needed to have it. However, some ladies recognize Alo Yoga and suppose it’s a reliable competitor, whereas some suppose Alo has much less premium enchantment than Lululemon.

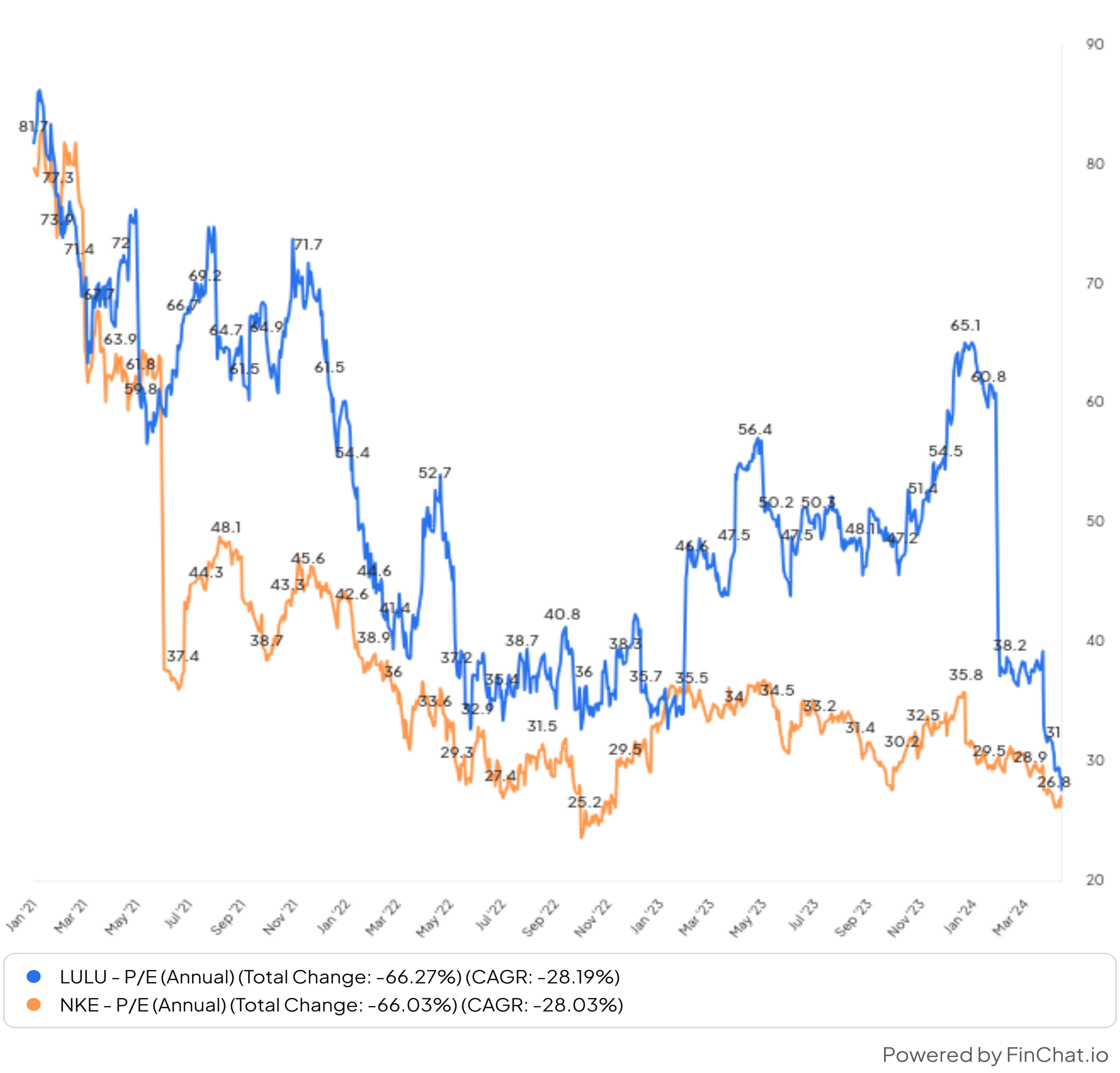

I believe {that a} TTM PE of 28, which is considerably beneath previous averages, makes Lulu fairly low-cost. Additionally, 23 occasions NTM earnings for a corporation that’s prone to develop EPS within the mid-teens space together with greater than a 40% ROIC is unquestionably affordable, and you will not discover that so much within the American markets. On high of that, Nike is buying and selling at the same a number of regardless of decrease development, decrease margins, and fewer effectivity.

Lowest a number of in years (finchat)

The primary threat, in my opinion, is the rising competitors. I do not wish to put money into the attire trade as a result of shopper preferences are altering quick, and types might be hit arduous, as seen with Below Armour (UA).

The second threat, in my opinion, is that males in some markets will see the model as extra female. I believe it’s now like that in Israel. Lulu might want to make investments closely in advertising and marketing to alter males’s view of the model as a result of proper now, it appears many males see it as a sport-focused girls’s model. Such funding in advertising and marketing might have an effect on margins, that are already stretched excessive, and we should not anticipate extra from them.

You may additional delve into my final articles on Lulu, here and here.

Conclusions

I consider that the risk-reward ratio right here is tilted in favor of long-term patrons, and at present costs, each shares might outperform the market. Moreover, I might like to emphasise that each shares are potential compounders, which means they may very well be held for years. Even when they appear costly, these are usually not shares to dump after a double.

There are dangers, in my opinion, and I would not underestimate them. Nevertheless, I believe that affected person buyers have an edge with these sorts of shares. In contrast to large funds, they’ll maintain and watch for catalysts, as funds are scrutinized quarterly. Simply sit tight and watch for the compounding impact.

I hope you loved the article and sit up for your feedback