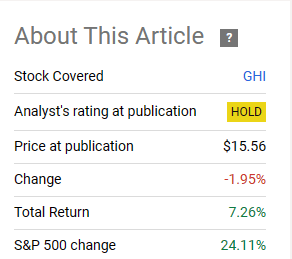

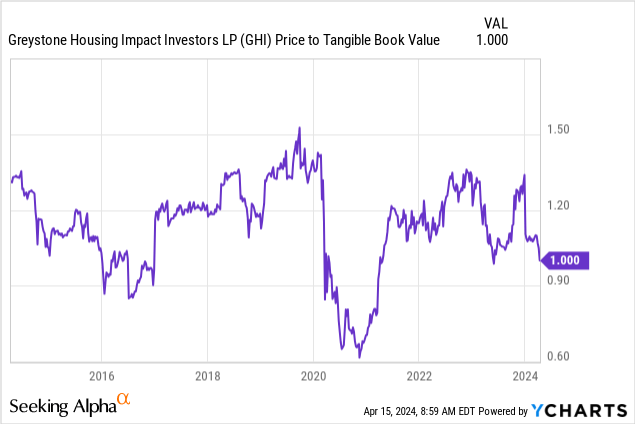

It has been a while since we up to date the views on Greystone Housing Affect Buyers LP. (NYSE:GHI). In November 2022, we took a unfavorable stance on the corporate in mild of the rising dangers to fund the distribution. We maintained that into February 2023, however the giant worth decline after that allowed an improve.

Looking for Alpha

Greystone misplaced floor (even on a complete return foundation) between the Promote and the Maintain scores, however has since then delivered a mean efficiency.

Looking for Alpha

We have a look at the not too long ago launched Q4-2023 results and inform you the place you wish to purchase this extremely tax-advantaged yield.

A Transient Overview

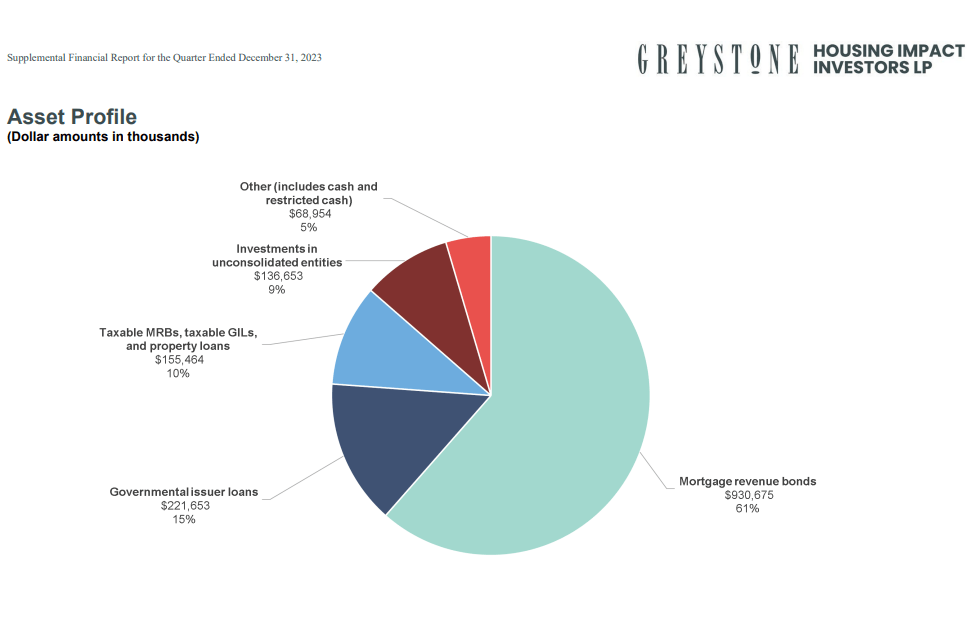

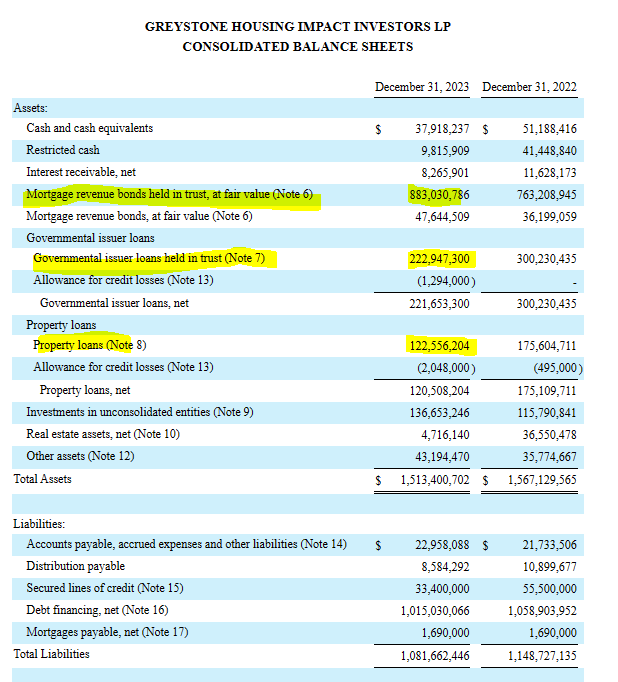

The corporate owns Mortgage income bonds and related investments which make the majority of its asset base.

GHI This fall-2023 Supplemental

The corporate additionally owns bodily actual property and that has been the asset that has rescued its distributable earnings as we will see beneath. Earlier articles have coated the corporate asset base in additional element.

This fall-2023

For earnings traders, it’s typically arduous to look previous the quantity that’s being paid. If the dividend or distribution is coming in, they’re detached to cost declines. In addition they appear impervious to fundamentals declining. One motive is that they assume the whole lot should be positive if the fee is coming in. The opposite one is that there’s a lag usually, between the basics going out the window and the distribution following suite. Let’s examine how that is enjoying out for GHI.

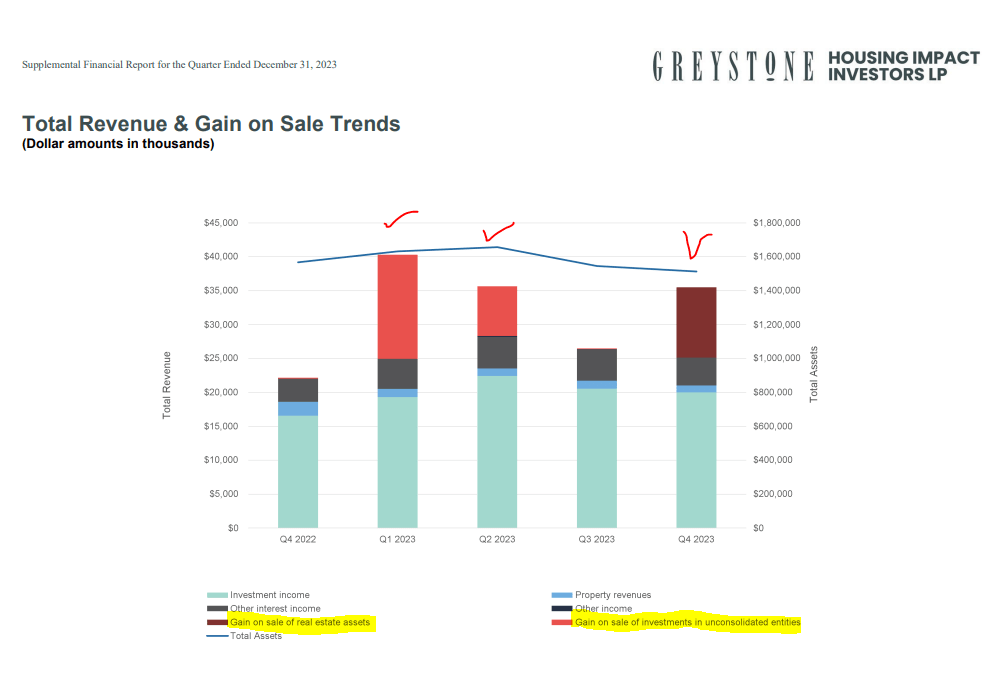

For all of 2023, we’ve seen the distribution funded by promoting actual property belongings.

GHI This fall-2023 Supplemental

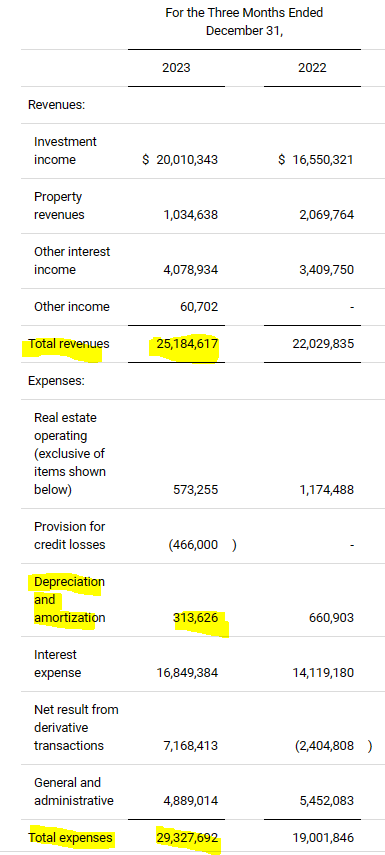

This fall-2023 was no totally different. You possibly can see that to some extent even with out deeper prying as the entire revenues are lower than complete bills, even in case you exclude depreciation.

GHI This fall-2023 Press Launch

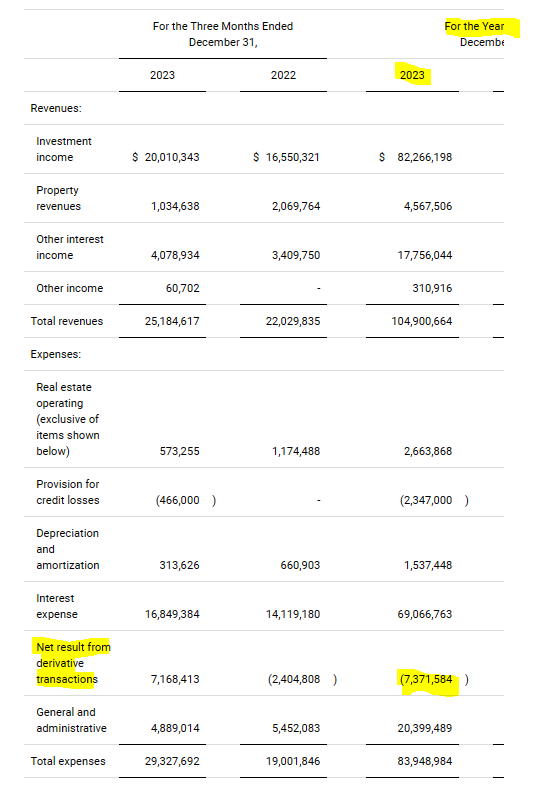

The image is a bit clouded although, by the online outcome from “derivative transactions”. You possibly can see above that it provides $7.16 million to bills and therefore subtracts the identical from internet earnings. Over time (not essentially on this quarter) the spinoff transaction influence ought to fade. We truly see that once we visualize the entire yr 2023. By-product transactions had a a lot smaller influence in share phrases and really decreased bills (enhanced earnings) by $7.3 million.

GHI This fall-2023 Press Launch

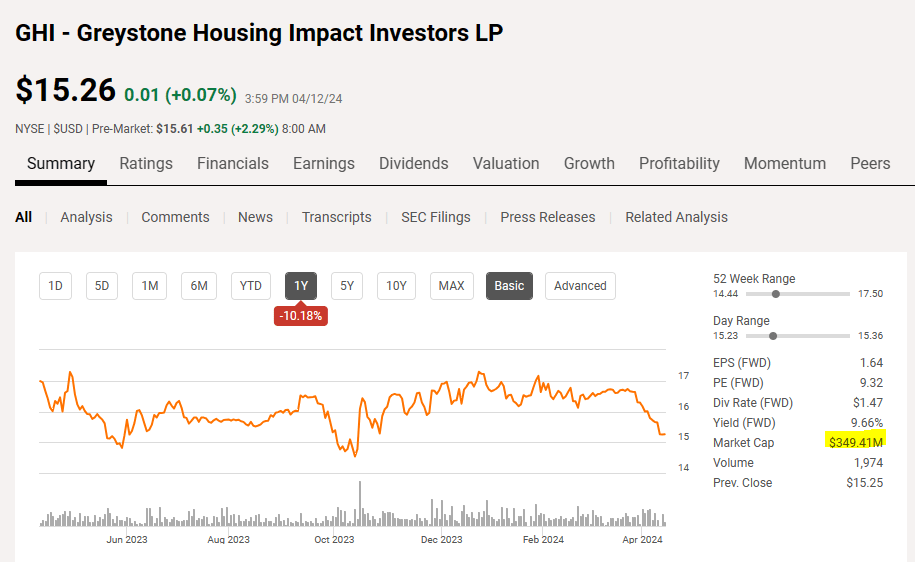

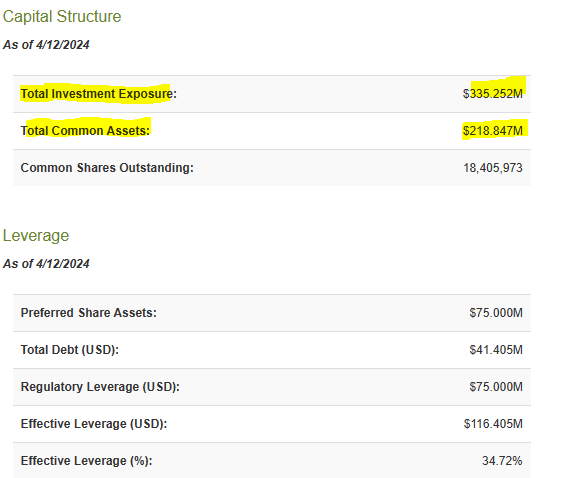

The present final analysis run fee, excluding depreciation, spinoff adjustments and provision for credit score losses, is about $3 million 1 / 4. So that’s $12 million a yr. Now if an organization had a internet earnings (additionally money obtainable for distribution) run-rate of $12 million and a market capitalization of $350 million, what would you count on its dividend yield to be?

Looking for Alpha

3.42%, appropriate? However we’ve a 9.66% dividend yield simply listed above that. So the straight strategy to inform you that is that if you’re probably not paying consideration at this level, you’ll probably get “gifts” just like the one Ares Business Actual Property Company (ACRE) simply dropped in your lap just a few months again.

The place Is The Cash Coming From?

GHI’s unfold earnings enterprise is just not producing a lot in any respect. Promoting the bodily actual property belongings although, was a unbelievable earnings supply.

GHI-10-Ok

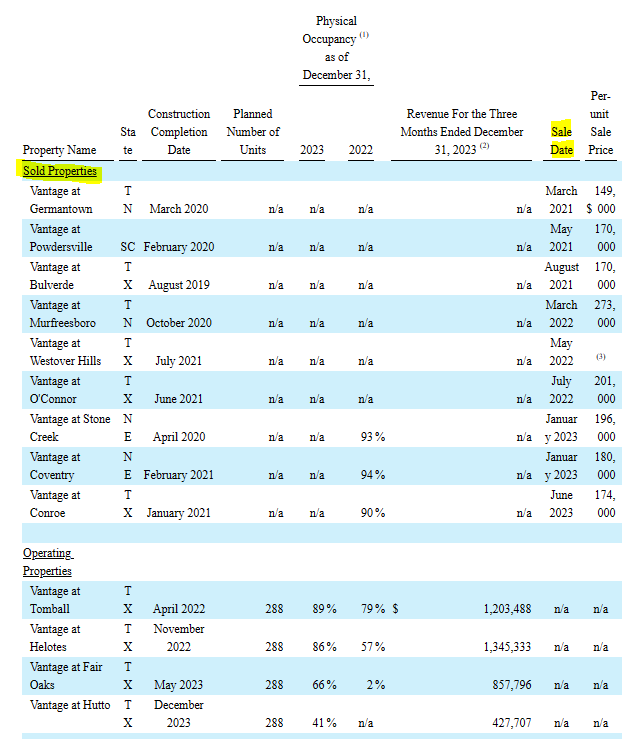

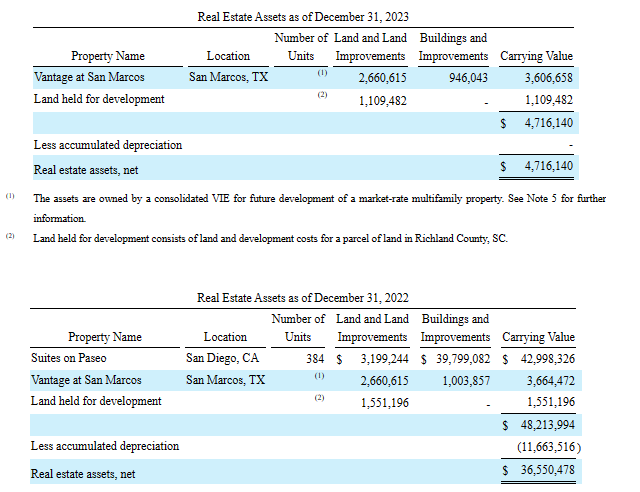

On the backside, you may see the remaining working properties. You can too see the change in the actual property belongings from December 31, 2022 to December 31, 2023.

GHI-10-Ok

So this a part of the sale exercise has to return to a crawl in 2024, as there may be not a lot there to assist it. However GHI nonetheless has one other space the place some gross sales would possibly occur. These are the investments in unconsolidated entities.

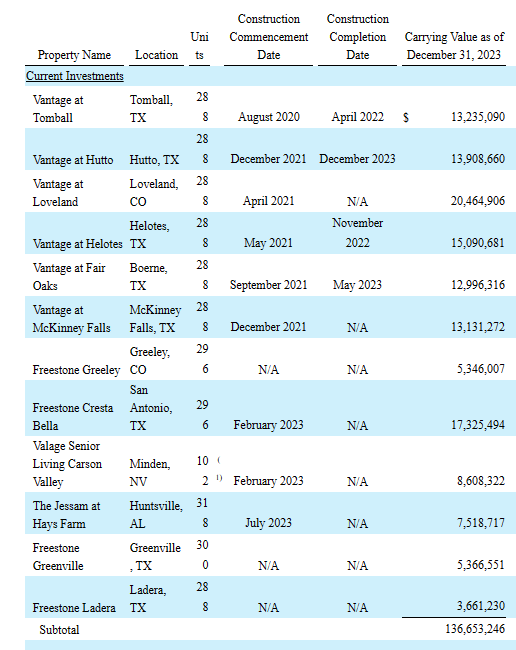

GHI-10-Ok

On the prime half of this desk, we are able to see the development accomplished date and greater than half are nonetheless underneath development. However asset gross sales listed below are nonetheless possible in 2024 with some assist to money obtainable for distribution.

Outlook & Verdict

The bottom enterprise for GHI is just not doing that nice. These mortgage income bonds are long-term bonds and whereas some do regulate upwards with rate of interest adjustments, their unfold earnings has been crushed because the Fed hiked. At the moment, as we confirmed above, this section (plus the instantly owned actual property) is producing nearly $3 million internet in curiosity earnings, each quarter. So $1.2 billion of belongings are producing simply $12 million in internet funding earnings a yr.

GHI-10-Ok

The query turns into whether or not actual property gross sales, can fund the distribution. We expect that’s extremely unlikely over the medium time period. The 2023 asset gross sales created a acquire as these had been accomplished just a few years again. Current completions are probably underwater or at finest prone to create marginal features. If we keep in the next for longer surroundings, the distribution is prone to be pressured finally.

So why not put a Promote on it?

In our framework, whereas the distributions are necessary, valuation goes a great distance into making the purchase, maintain or promote score. We didn’t simply make that standards up. Actually, once we put a “Sell” on it in 2022, this was the conclusion.

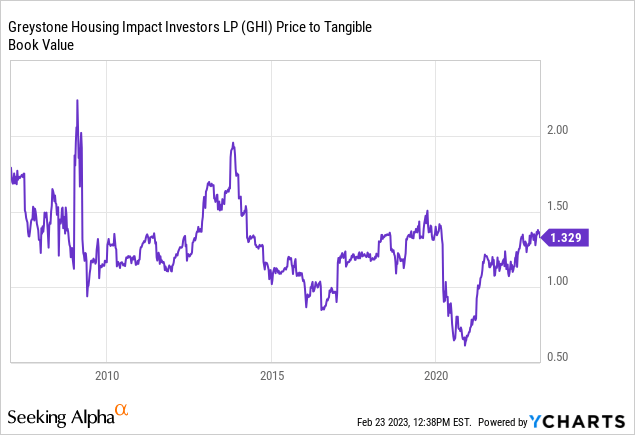

With borrowing charges nonetheless rising, GHI can have some complicated work to do in 2023 and maybe past. 2022, in contrast to 2021, had no provisions for credit score losses. We expect these will make a reappearance in a recession. On this surroundings, we do not assume it is in any respect unrealistic for this to commerce at a tangible e book worth per share.

Y-Charts From Earlier Article

Actually it has finished so previously when rates of interest had been far decrease and it was producing a stable unfold earnings.

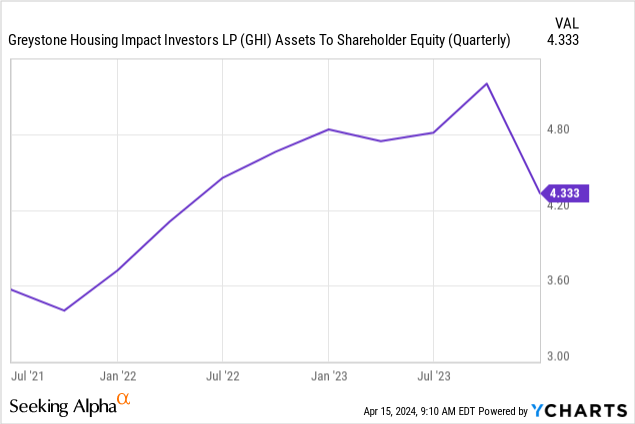

So it’s arduous to get extraordinarily bearish right here regardless that we see the distribution as utterly unsustainable exterior of an enormous fee lower cycle. Since we do not assume that is happening, the distribution will realign sooner or later. It is usually arduous to get extraordinarily bullish right here because the bonds portfolio could be very delicate to rate of interest adjustments and in addition to some extent, credit score spreads. We’ve refused to purchase closed finish muni funds buying and selling at huge reductions to NAV, just because they used plenty of leverage. For instance, BNY Mellon Municipal Bond Infrastructure Fund, Inc. (DMB)’s belongings to fairness ratio is about 1.54X.

That 4.33X can be understating issues right now as bonds have taken a success since December 31, 2023. So within the face of this leverage, an unsustainable base distribution, we moderately keep out till a cloth low cost exhibits up. We fee the inventory a “hold” and would possibly enter if we see a sub $13 worth or a distribution lower.

Please word that this isn’t monetary recommendation. It could look like it, sound prefer it, however surprisingly, it isn’t. Buyers are anticipated to do their very own due diligence and seek the advice of with knowledgeable who is aware of their goals and constraints.