deepblue4you

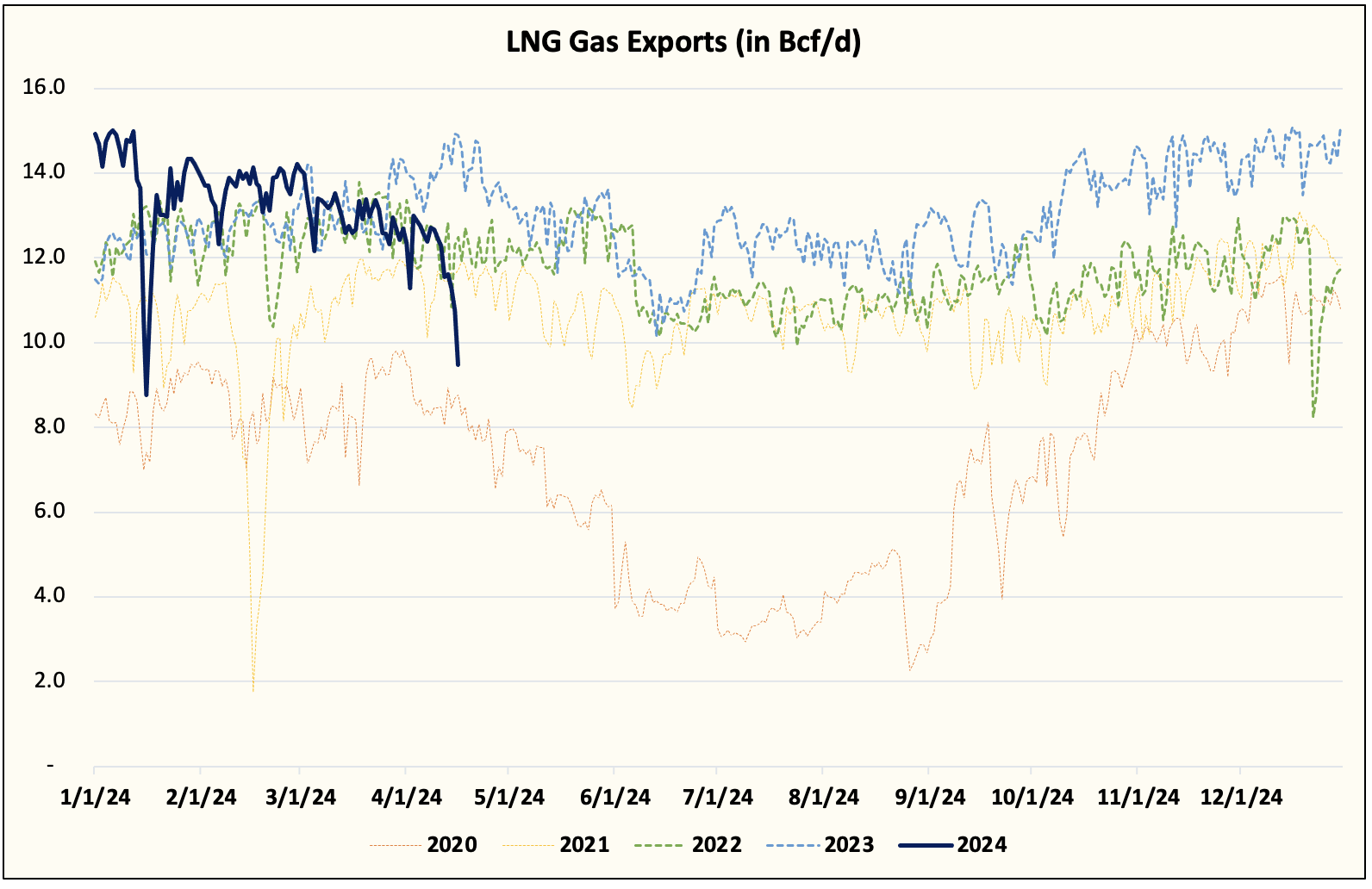

In our NGF stories as of late, we pointed to the tightening market fundamentals we have been seeing for pure fuel. Decrease manufacturing coupled with structurally greater demand this yr will lead to a gradual restoration available in the market. Till, in fact, Freeport had “issues” once more and LNG feedgas is down meaningfully. The drop in LNG feedgas has despatched the U.S. fuel market, as soon as once more, again right into a surplus.

IHS, HFIR

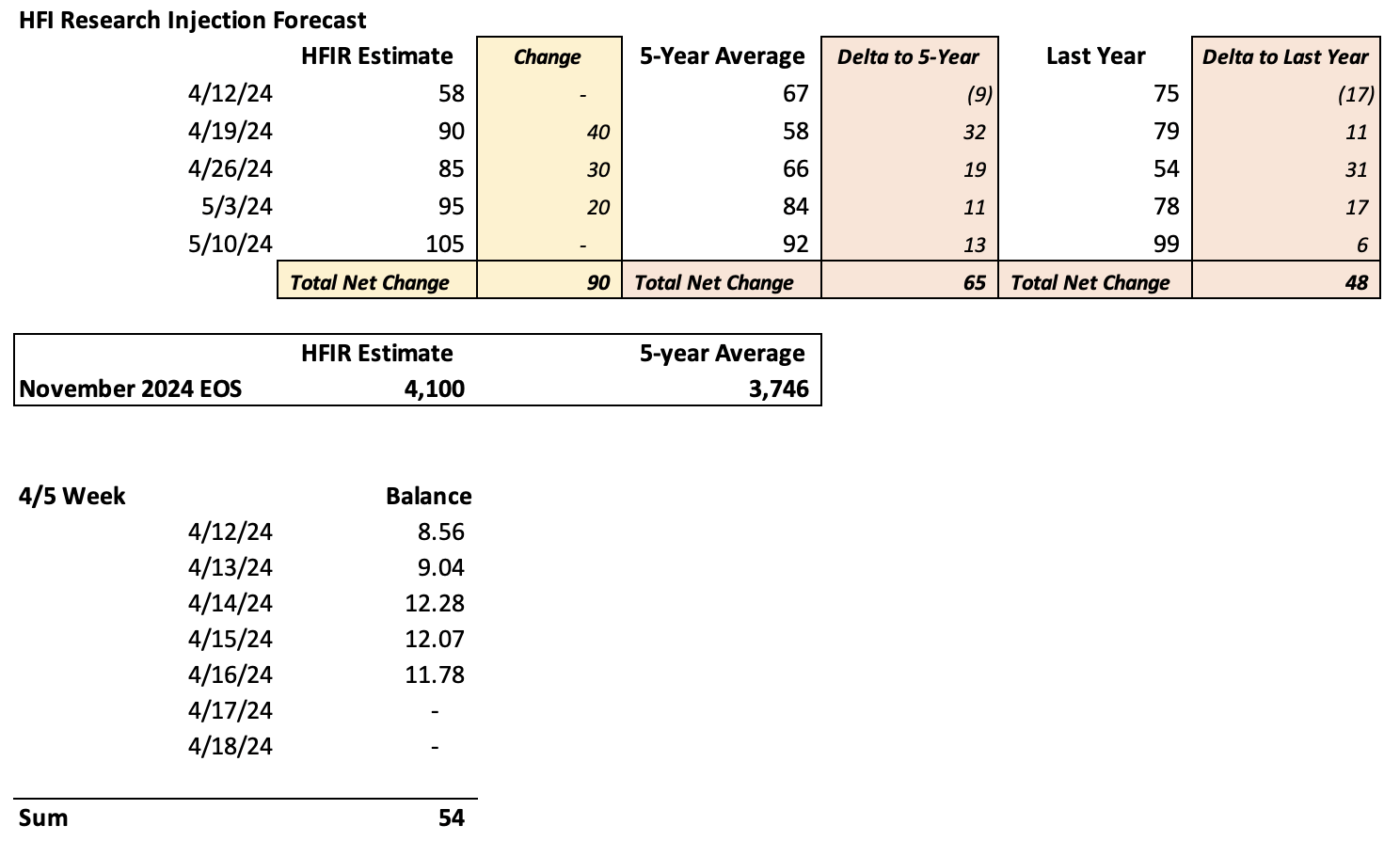

Whereas the drop shouldn’t be anticipated to final for a very long time, it does current a large headwind for the U.S. fuel market. For our pure fuel stability for the subsequent 5 stories, we see a +65 Bcf injection whole versus the 5-year common.

HFIR

At a time when pure fuel storage is already bloated, that is going to essentially harm sentiment and the restoration course of.

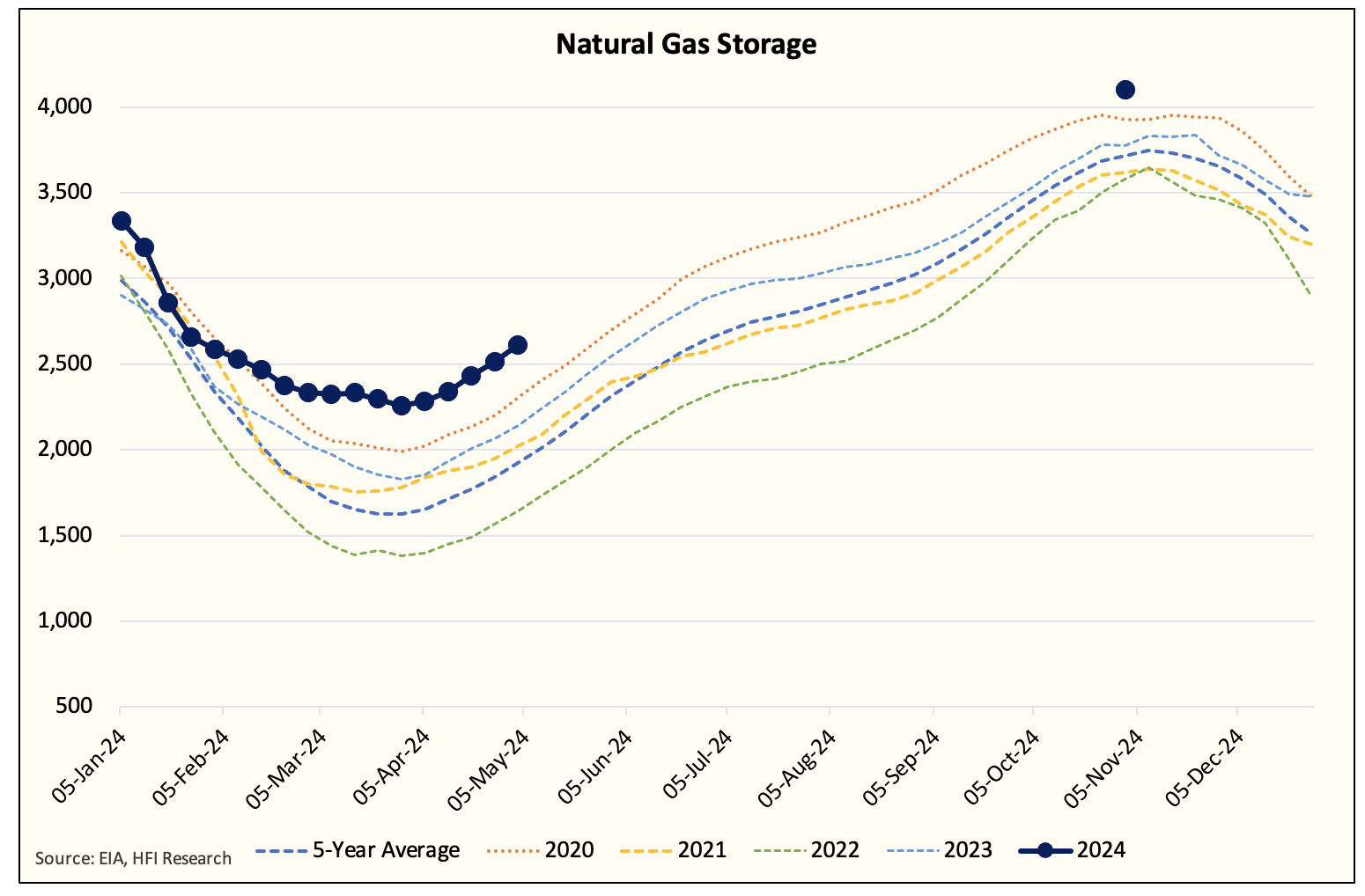

EIA, HFIR

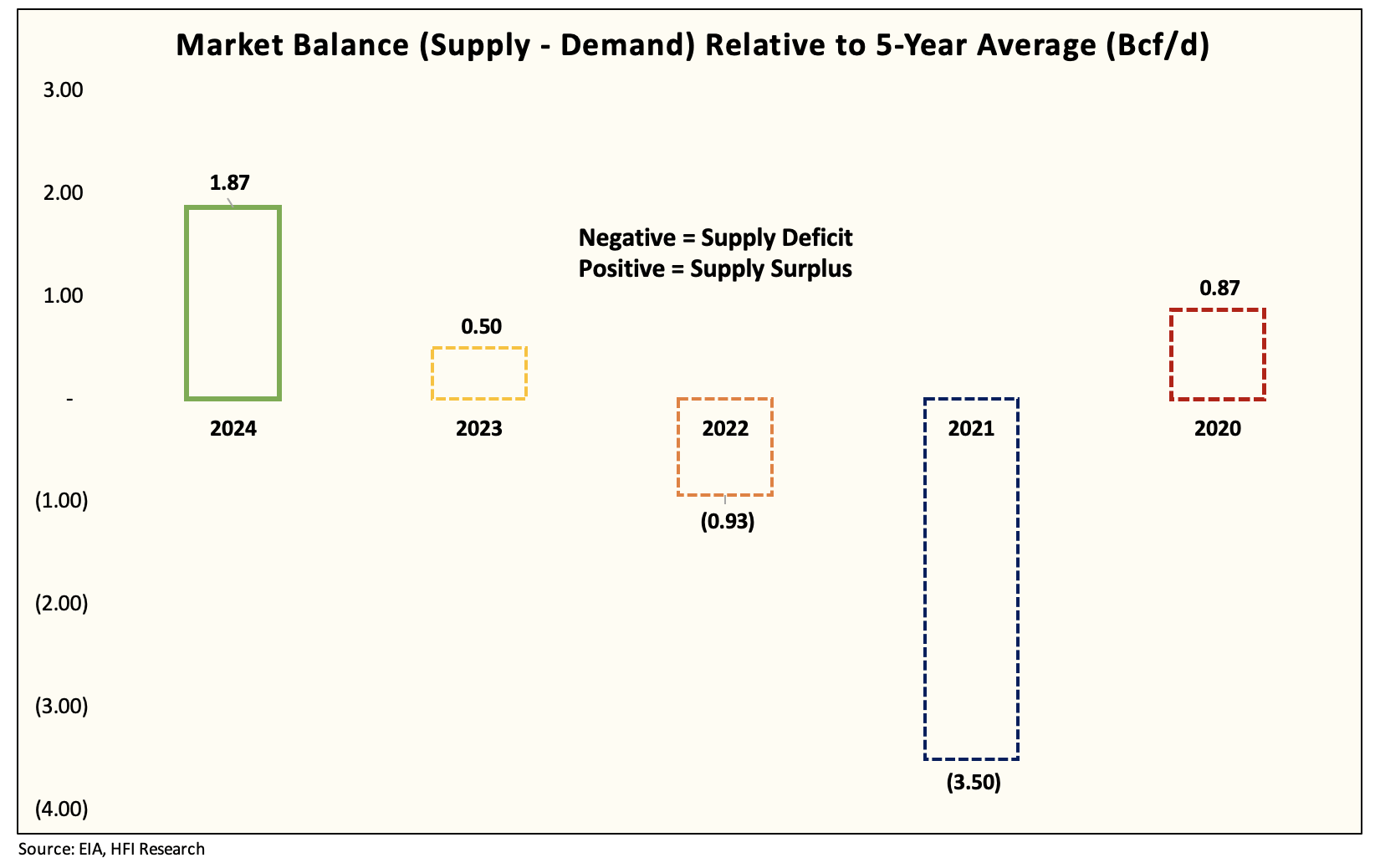

We estimate that due to the LNG feedgas drop, the U.S. fuel market is now +1.87 Bcf/d in surplus.

EIA, HFIR

This can be a dramatic change from final week’s implied stability of -1.4 Bcf/d deficit.

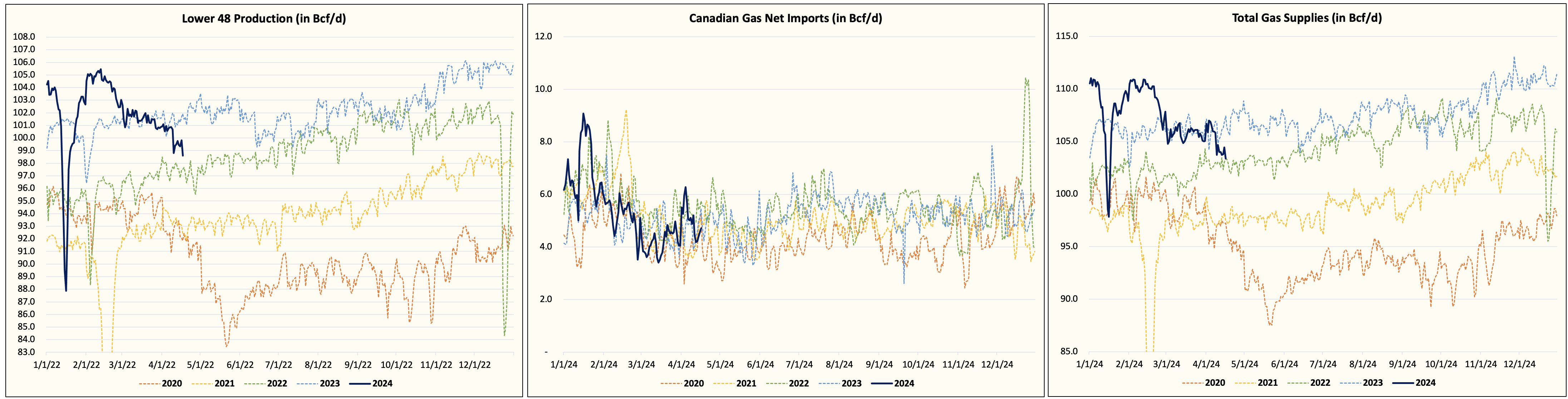

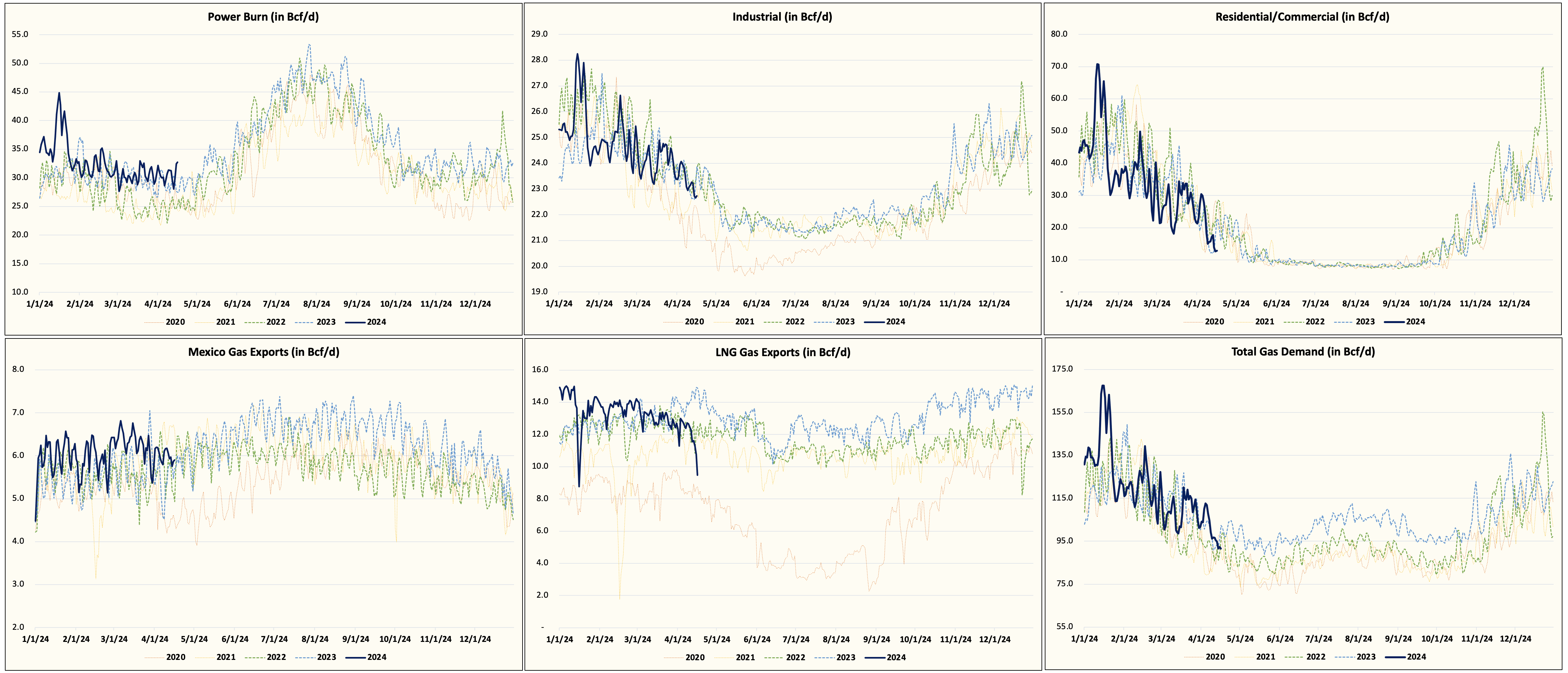

On the provision facet, we’re seeing very weak provide figures.

IHS, HFIR

Decrease 48 fuel manufacturing is averaging between ~99 to ~100 Bcf/d with the newest knowledge displaying a drop to only under ~99 Bcf/d. Canadian fuel web imports are in-line with historic averages, however at present’s worth pop seems to be associated to a pipeline outage in Canada, which might affect web imports. Whole fuel provides are close to 2022 ranges and down materially y-o-y.

Producer self-discipline is beginning to present, however the sizable drop in LNG feedgas (-5 Bcf/d y-o-y) is way outweighing any provide decreases we’re seeing.

IHS, HFIR

On the demand entrance, regardless of robust energy burn demand, we’re coming into the weakest demand interval of the yr. With none seen catalysts (other than LNG returning), the pure fuel market should power manufacturing decrease nonetheless to stability the market.

Even at ~99 Bcf/d, the decrease LNG feedgas has pushed the market right into a surplus, which suggests worth strain will proceed for some time longer.

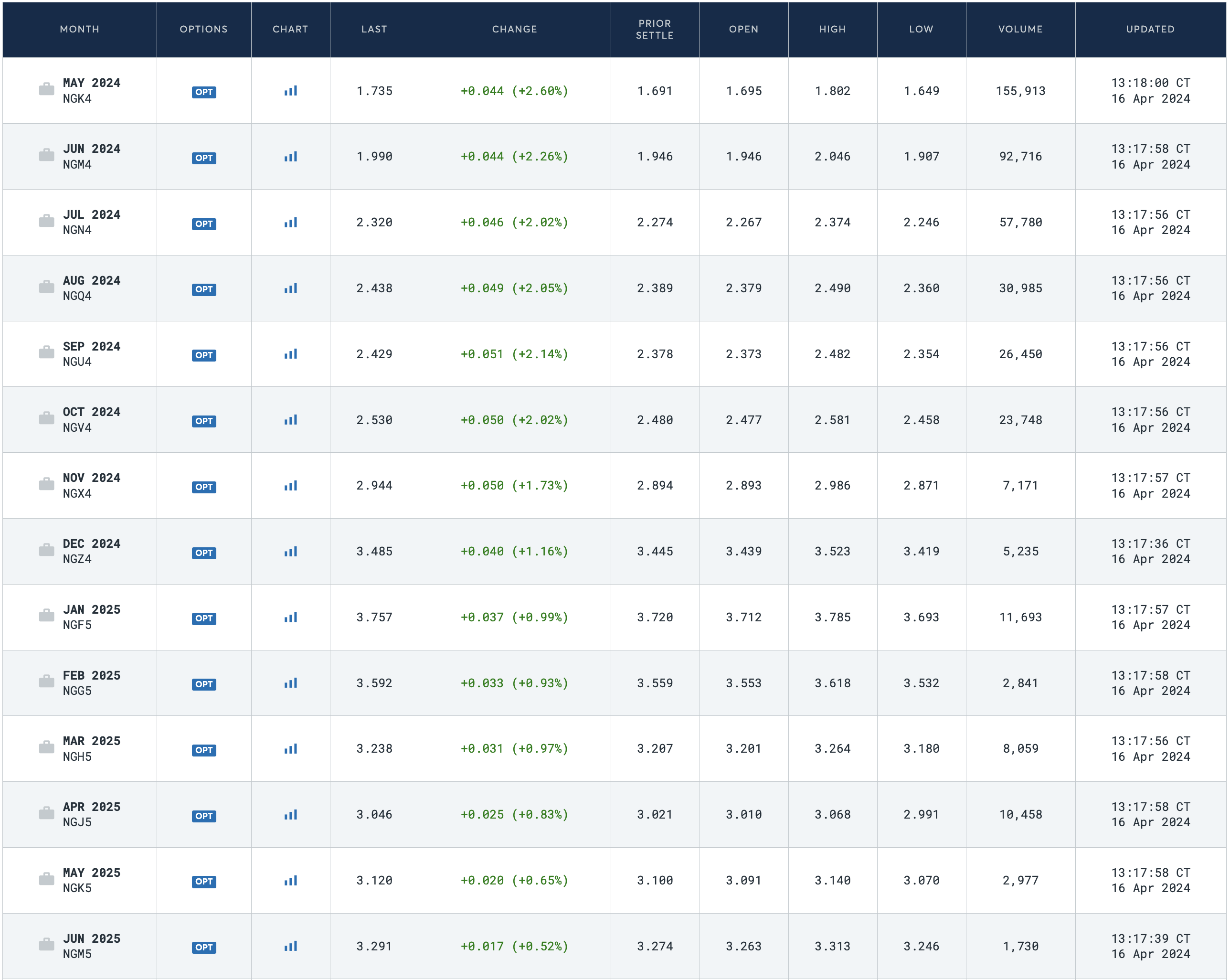

The true dilemma for buyers/merchants

However for buyers and merchants, the actual dilemma is within the steep contango within the pure fuel futures curve.

CME

Whereas on the floor, pure fuel costs at present are low cost, readers should be reminded that the futures curve is in steep contango.

Calendar 2025 costs are all above $3/MMBtu, so this doesn’t sign that the market believes the excess will proceed by this time subsequent yr.

That is an optimistic assumption as a result of we consider related fuel manufacturing development, no matter pure fuel costs, will proceed and overwhelm balances. And for the reason that bulk of the LNG export capability improve is approaching in late 2025, the market is probably going too optimistic that balances will tighten considerably this yr to warrant such a excessive worth common.

In our view, the best method to guess on greater pure fuel costs is to purchase excessive liquids-weighted producers that commerce at a reduction. For instance, a reputation like Crescent Level Power will give buyers sufficient fuel publicity with out worrying in regards to the impending doom that comes if pure fuel costs fail to recuperate.

The problem with shopping for pure fuel solely producers is that if the restoration fails for no matter cause (i.e., climate, LNG, overproduction from U.S. shale oil), you’ll be left holding on to one thing that’s already pricing in a giant restoration. Therefore, why we expect it’s miles higher to purchase a liquids-rich producer that has fuel publicity.

As for merchants, the chance in pure fuel shouldn’t be apparent to me. Regardless of low immediate fuel costs, it’s low for a cause and can stay low. Might and June contracts are within the coronary heart of shoulder season, so with no demand catalyst in sight, the upside is capped. And in case you are betting on greater pure fuel costs this summer time, July to September already commerce close to $2.4/MMBtu, which is able to additional restrict any upside potential.

To me, the obvious commerce will probably be to attend patiently for summer time fuel costs to drop close to $2/MMBtu earlier than considering an extended place. Till then, we do not see a good threat/reward setup.

Conclusion

The restoration course of within the U.S. pure fuel market will take time. Low pure fuel costs are wanted to ensure that the market to stability and regardless of the steep drop we noticed in manufacturing, the drop in LNG has canceled that out and extra. With storage already bloated, the market can’t afford to deal with these intermittent setbacks. It is going to be paramount for producers to stay disciplined all through the summer time months, even when costs begin to recuperate.