Andrii Yalanskyi

REIT Efficiency

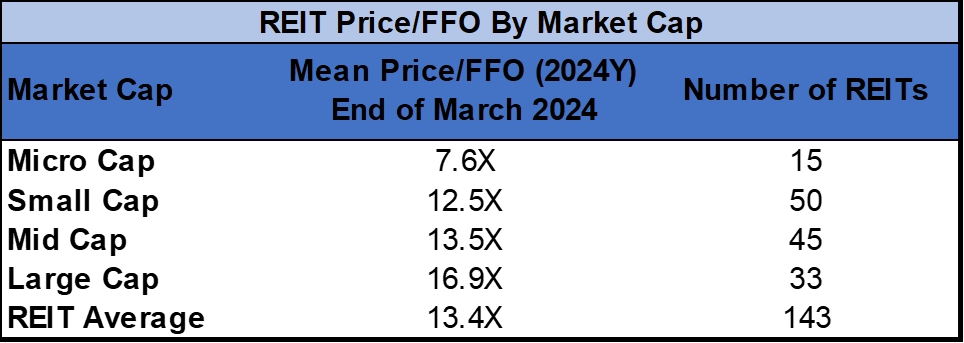

In March the REIT sector recovered a few of its losses from the primary two months of the yr, however nonetheless closed out Q1 2024 within the crimson. Fairness REITs averaged a +3.26% complete return in March and outperformed the broader market. The NASDAQ (+1.8%), Dow Jones Industrial Common (+2.2%) and S&P 500 (+3.2%) all noticed strong beneficial properties in March albeit smaller beneficial properties than the typical REITs. The market cap weighted Vanguard Actual Property ETF (VNQ) fell in need of the typical REIT in March (+1.96% vs. 3.26%) however has seen smaller losses yr to this point (-1.28% vs. -2.87%). The unfold between the 2024 FFO multiples of huge cap REITs (16.9x) and small cap REITs (12.5x) remained flat in March as multiples expanded 0.1 turns for each massive caps and small caps. Buyers presently must pay a mean of 38.5% extra for every greenback of FFO from massive cap REITs relative to small cap REITs. On this month-to-month publication, I’ll present REIT information on quite a few metrics to assist readers determine which property varieties and particular person securities presently provide the most effective alternatives to attain their funding objectives.

Supply: Graph by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

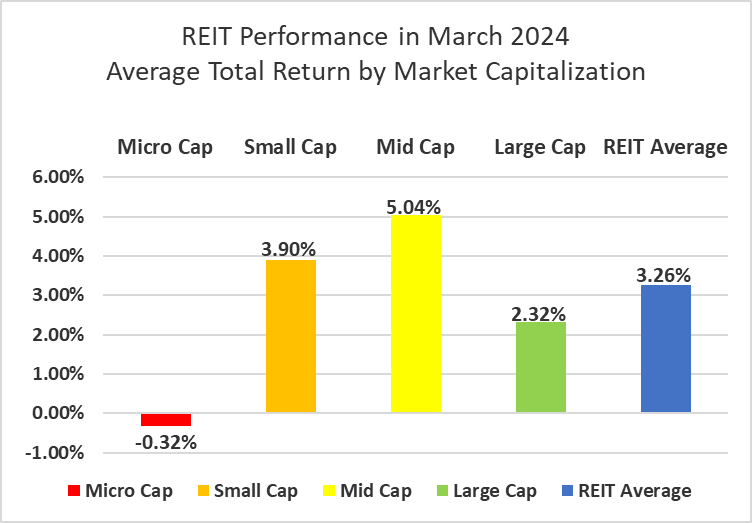

Mid cap (+5.04%), small cap (3.90%) and enormous cap REITs (+2.32%) completed March within the black, whereas micro caps (-0.32%) completed in unfavorable territory once more in March. Massive caps have outperformed small caps by 238 foundation factors via the primary quarter of 2024.

Supply: Graph by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

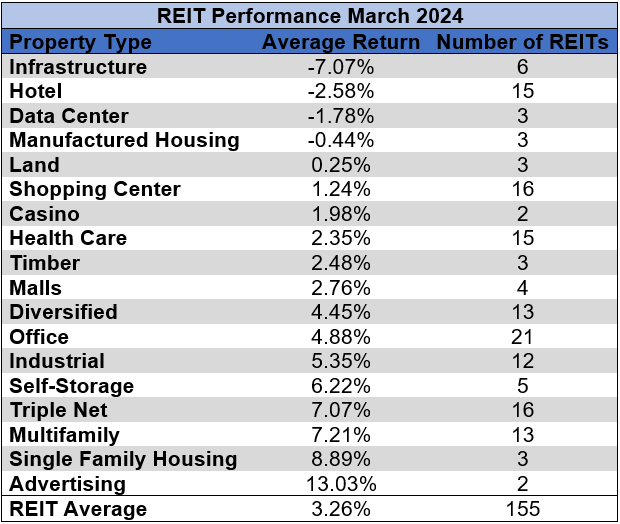

14 out of 18 Property Varieties Yielded Constructive Whole Returns in March

78% % of REIT property varieties averaged a optimistic complete return in March. There was a 20.1% complete return unfold between the most effective and worst performing property varieties. Promoting (+13.03%) was the main property kind in March, pushed by OUTFRONT Media (OUT) (+16.84%) which had the 6 th highest complete return amongst REITs in March.

Infrastructure (-7.07%) badly underperformed all different property varieties but once more in March. CorEnergy Infrastructure Belief (OTCPK:CORRQ) (-63.00%) continued to freefall for the reason that frequent shares might be worn out in chapter.

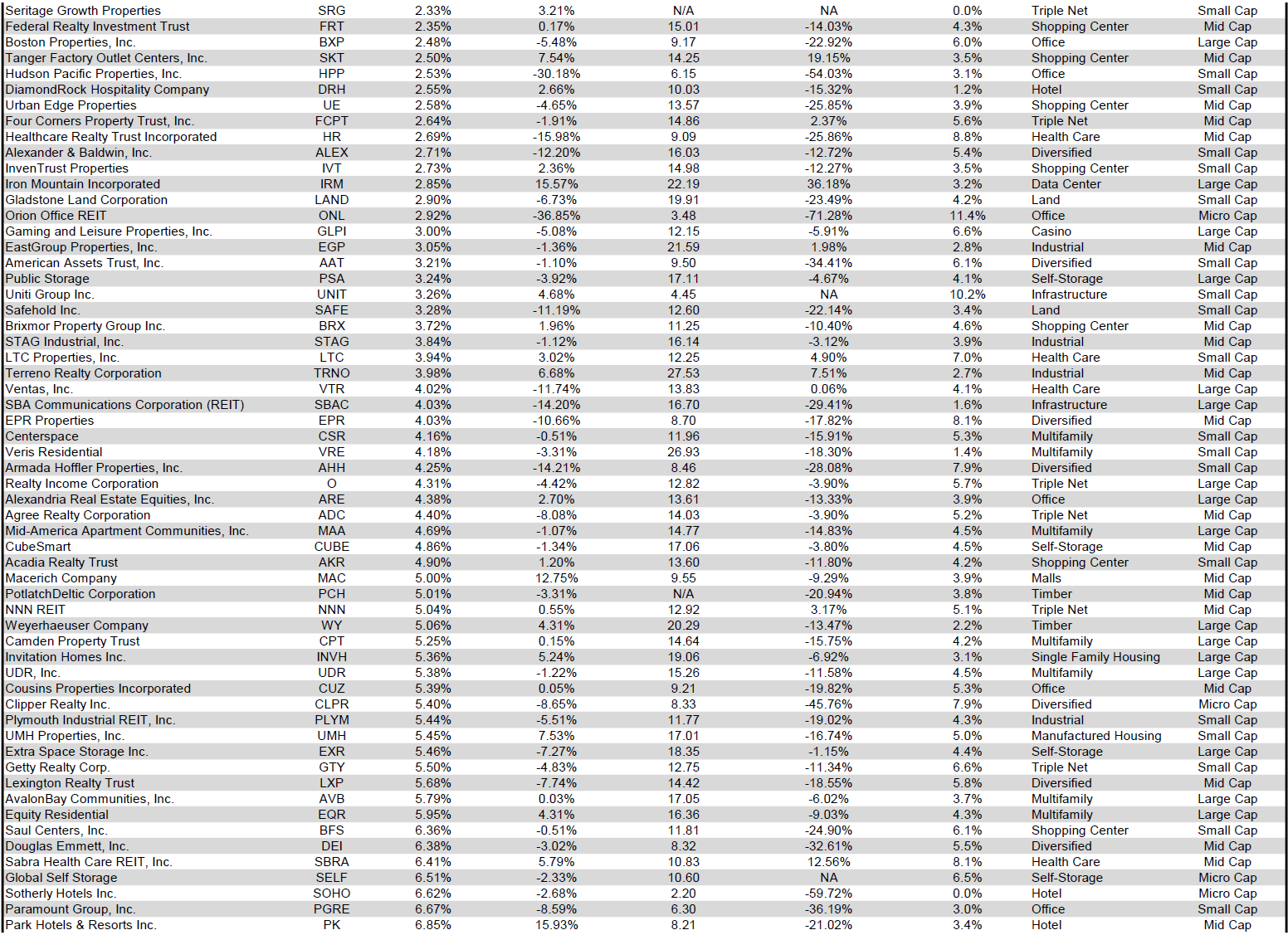

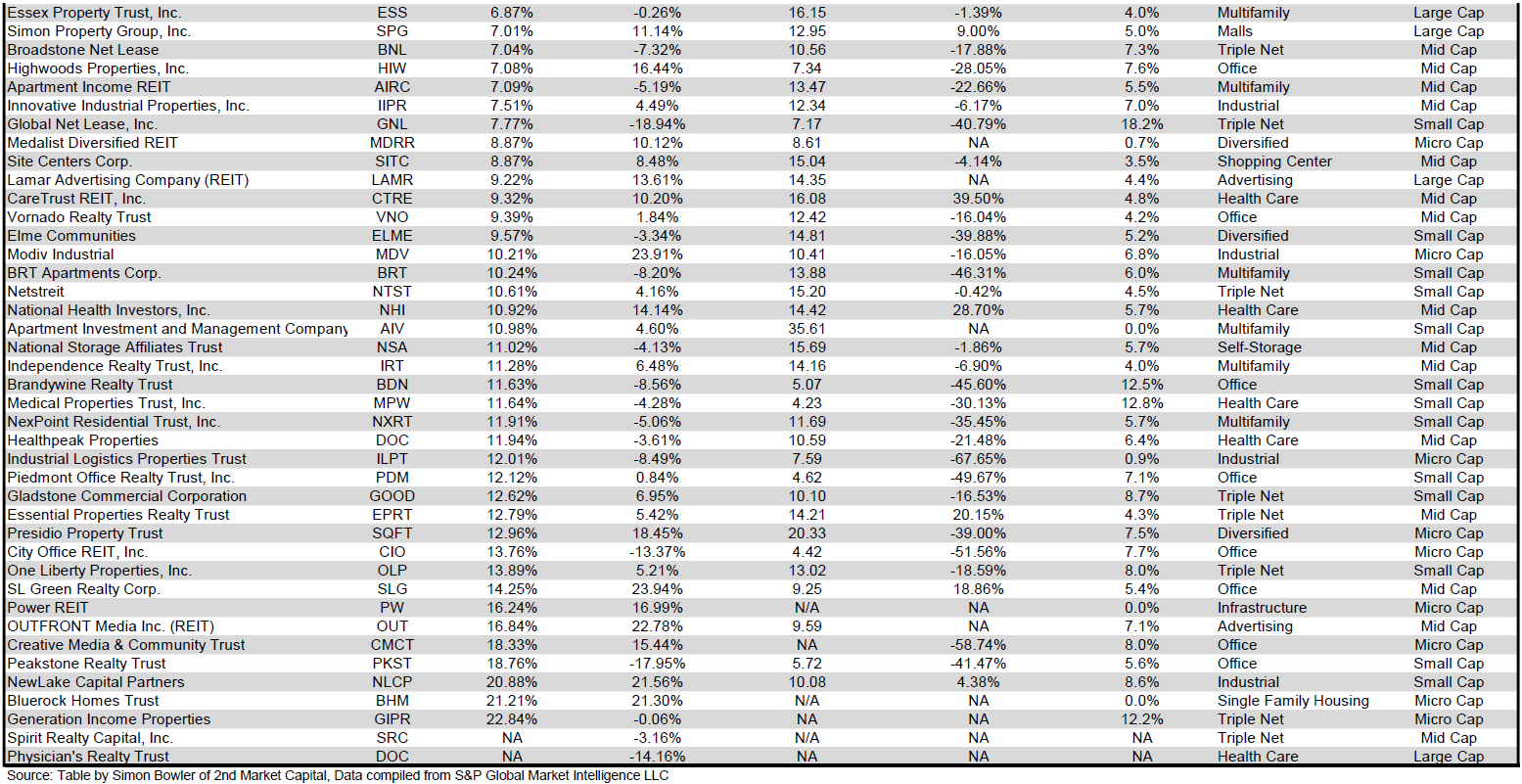

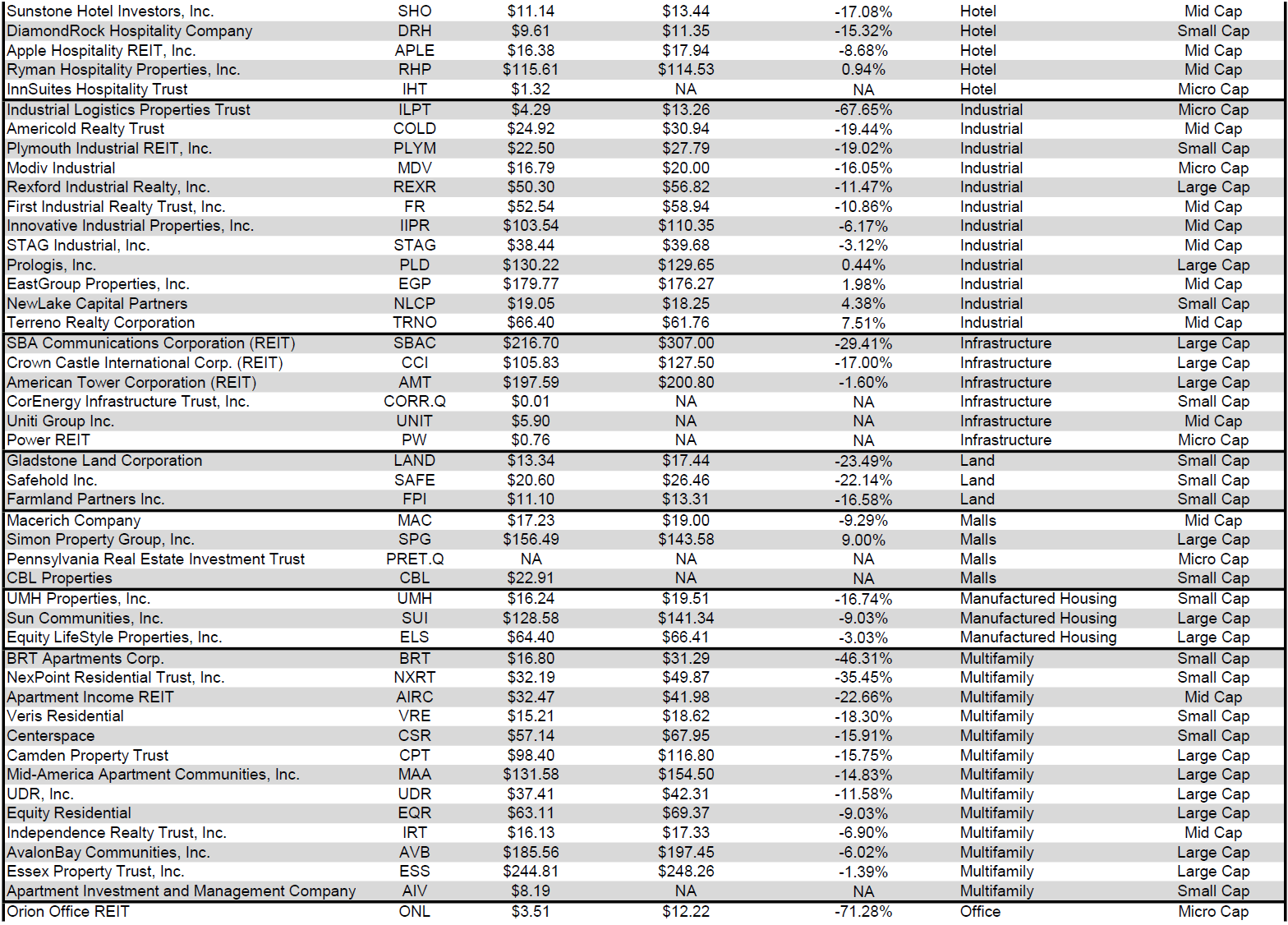

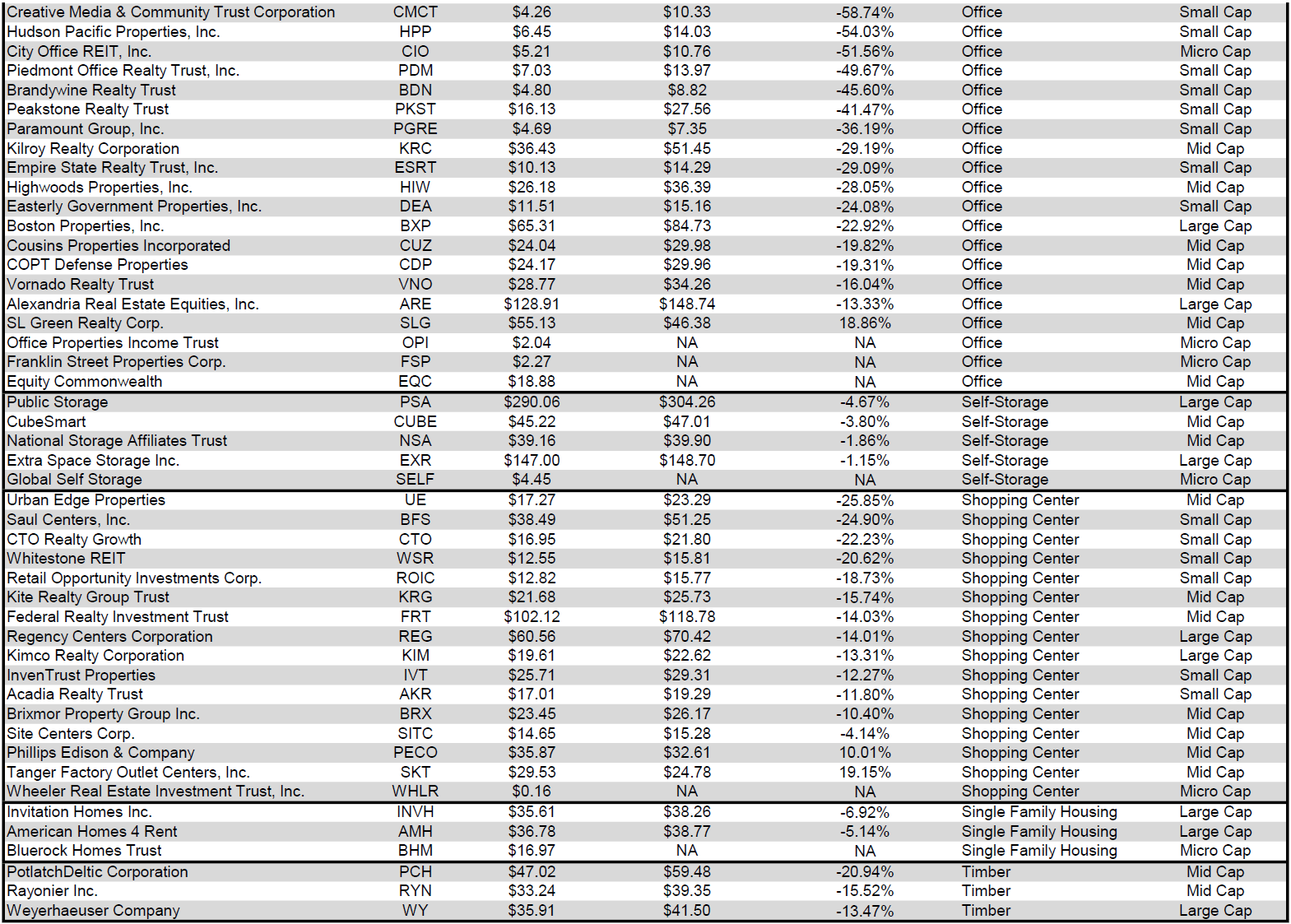

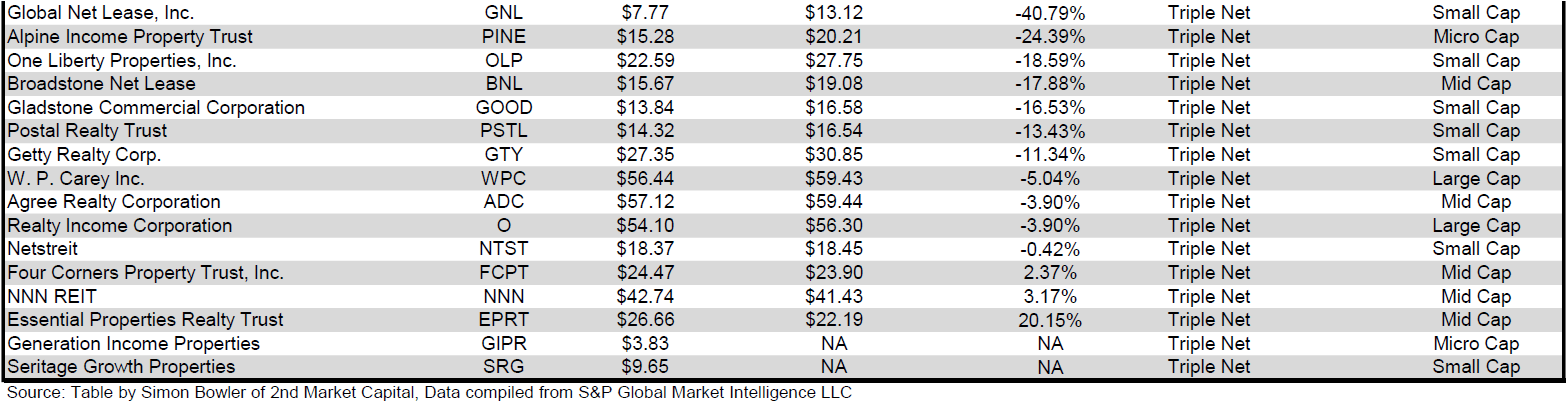

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

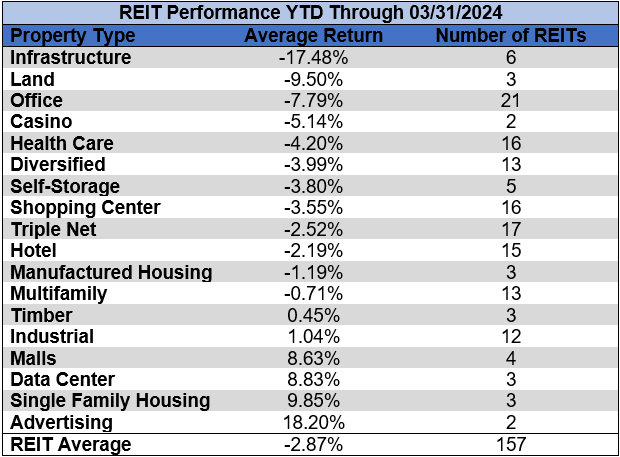

Infrastructure (-17.48%) and Land (-9.50%) have seen the worst common complete returns yr to this point. Promoting (+18.20%) and Single Household Housing (+9.85%) outperformed all different REIT property varieties within the first quarter of the yr.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

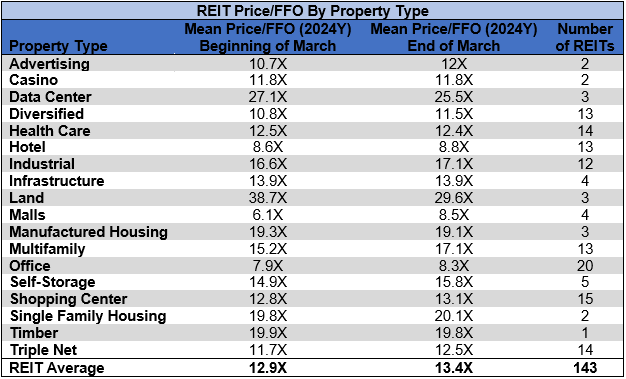

The REIT sector as a complete noticed the typical P/FFO (2024Y) enhance 0.5 turns in March from 12.9x as much as 13.4x. 61.1% of property varieties averaged a number of enlargement, 27.8% noticed a number of contraction and 11.1% held a gradual a number of. Land (29.6x), Knowledge Facilities (25.5x), Single Household Housing (20.1x), Timber (19.8x) and Manufactured Housing (19.1x) presently commerce on the highest common multiples amongst REIT property varieties. Workplace (8.3x), Malls (8.5x) and Resorts (8.8x) are the one property varieties that common single digit FFO multiples.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

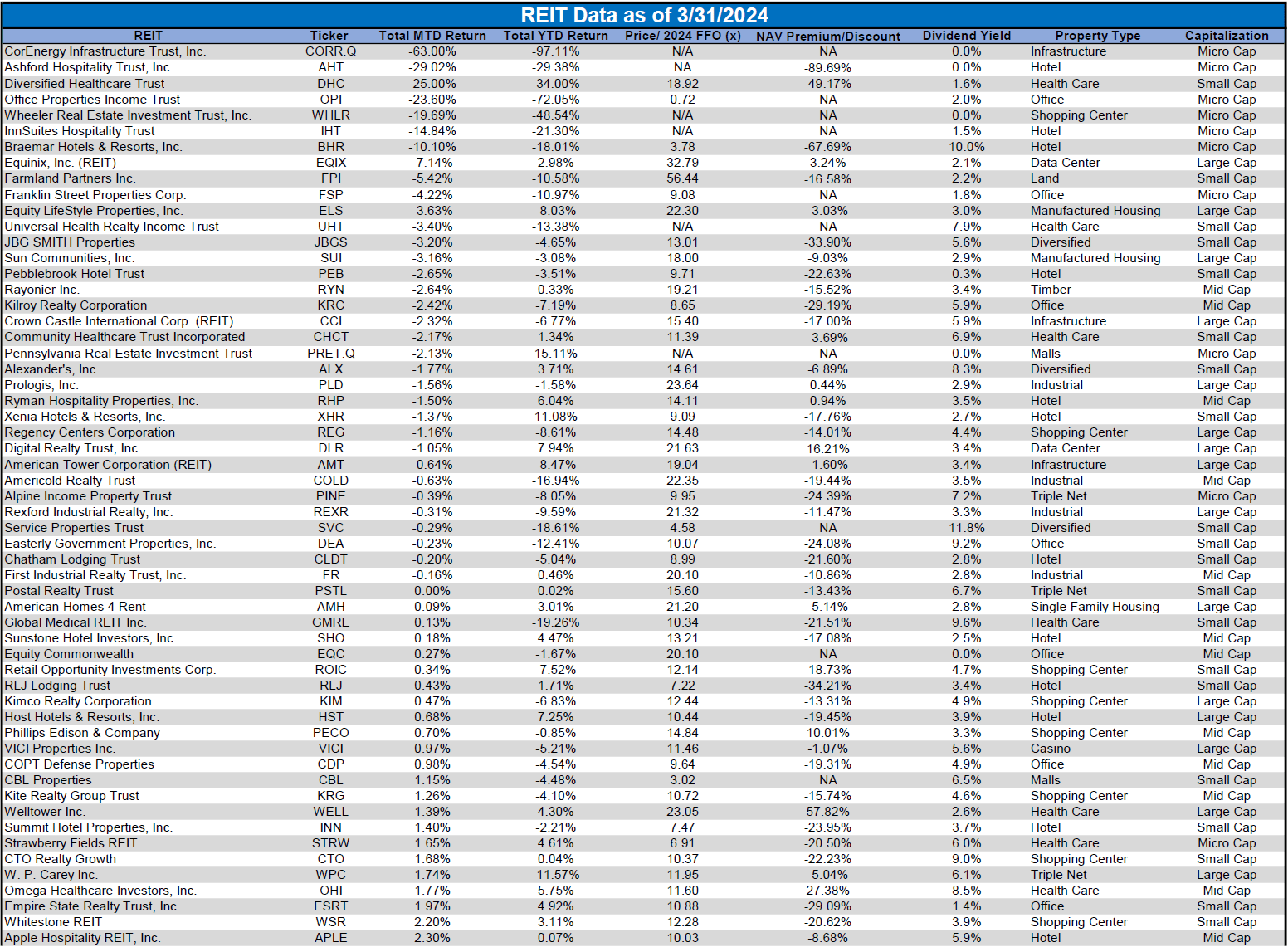

Efficiency of Particular person Securities

Technology Revenue Properties (GIPR) (+22.84%) bounced again from a brutal February (-23.46%) to complete the primary quarter basically flat (-0.06%). As a micro-cap REIT that has posted unfavorable FFO/share in 6 of the previous 10 quarters, there was elevated volatility of each earnings and share value relative to lots of their triple web REIT friends.

CorEnergy Infrastructure Belief (-63.00%) continued to freefall all through March because of the chapter 11 chapter submitting announcement on February 25th. Since frequent shareholders will obtain no proceeds from the upcoming chapter, the inventory has now plummeted to roughly $0.01/share and completed Q1 with a -97.11% complete return.

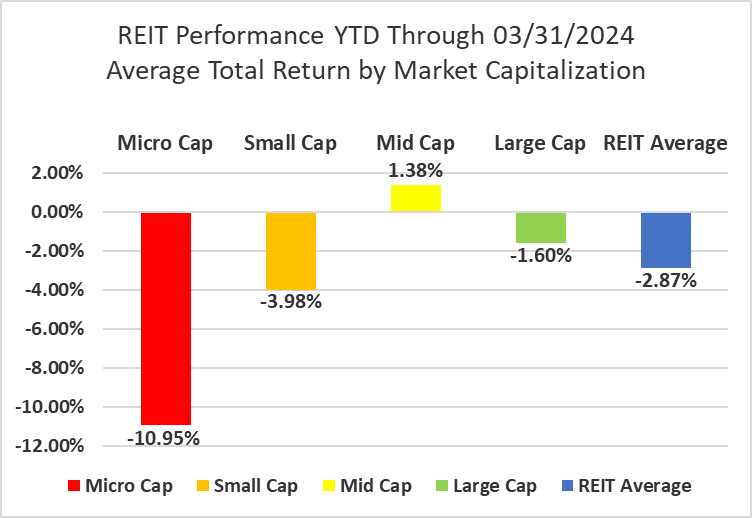

78.06% of REITs had a optimistic complete return in March. Through the first quarter of 2023 the typical REIT had a -1.23% return. The REIT sector kicked off the primary quarter of 2024 with a reasonably related -2.87% complete return.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

For the comfort of studying this desk in a bigger font, the desk above is offered as a PDF as well.

Dividend Yield

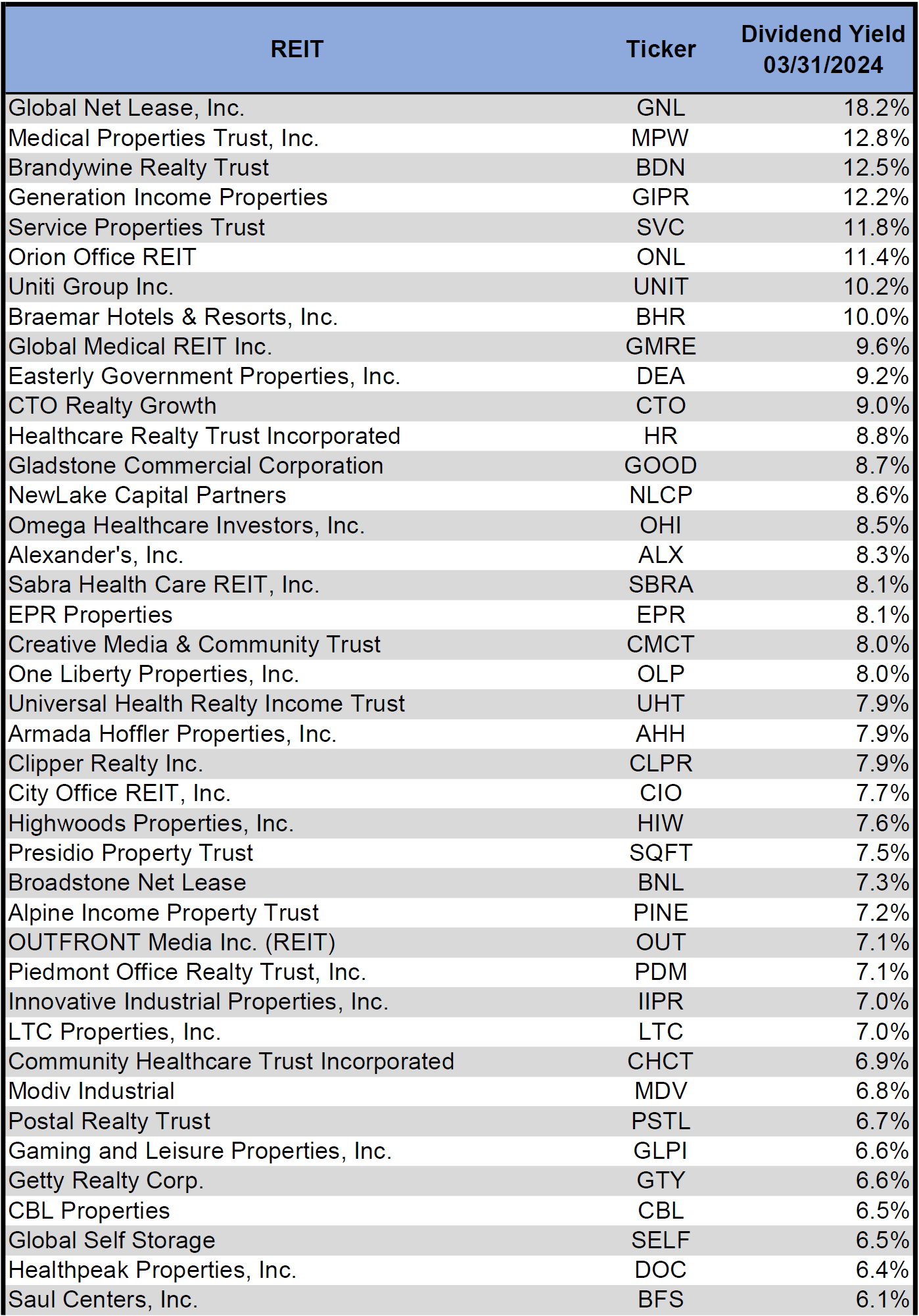

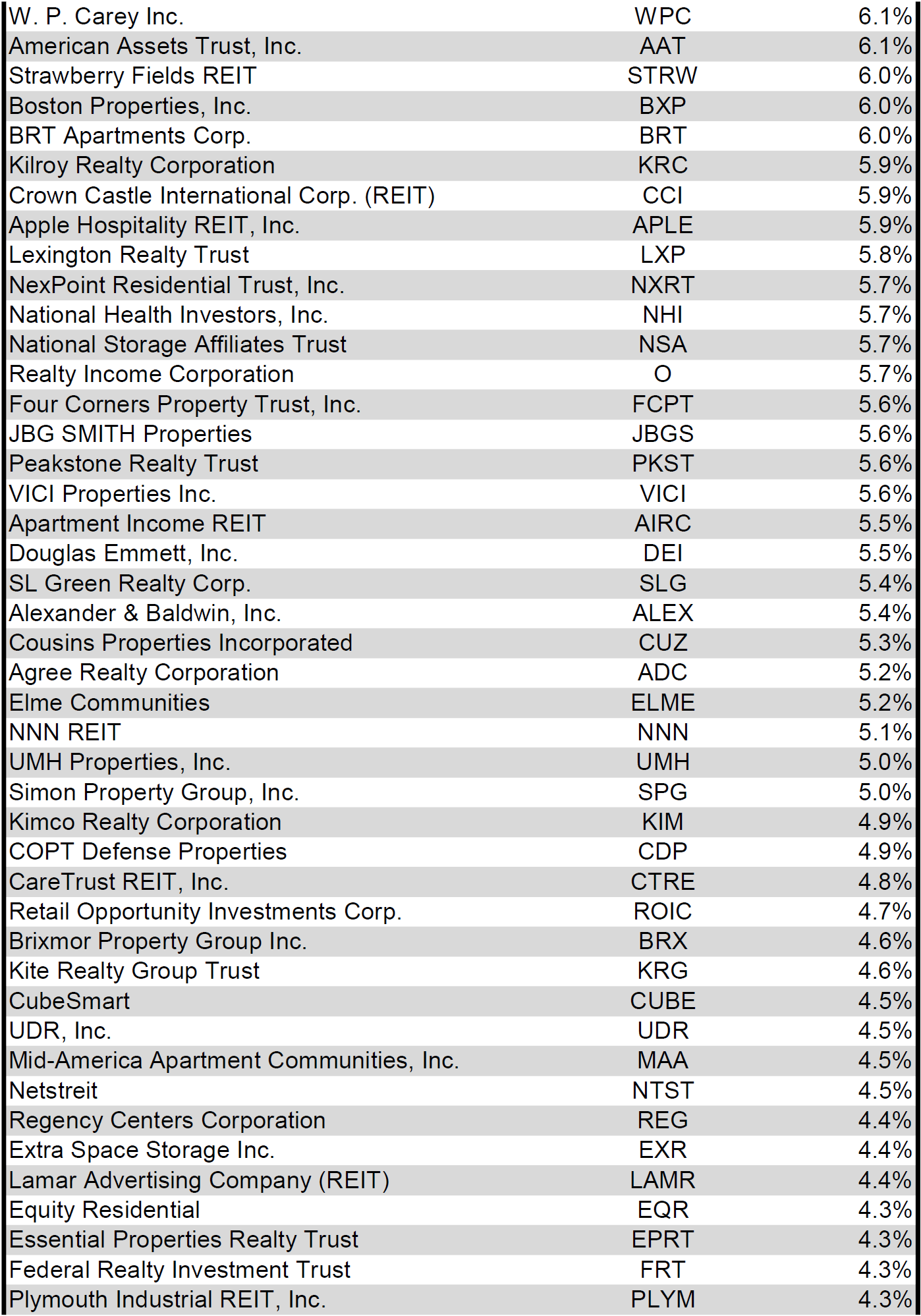

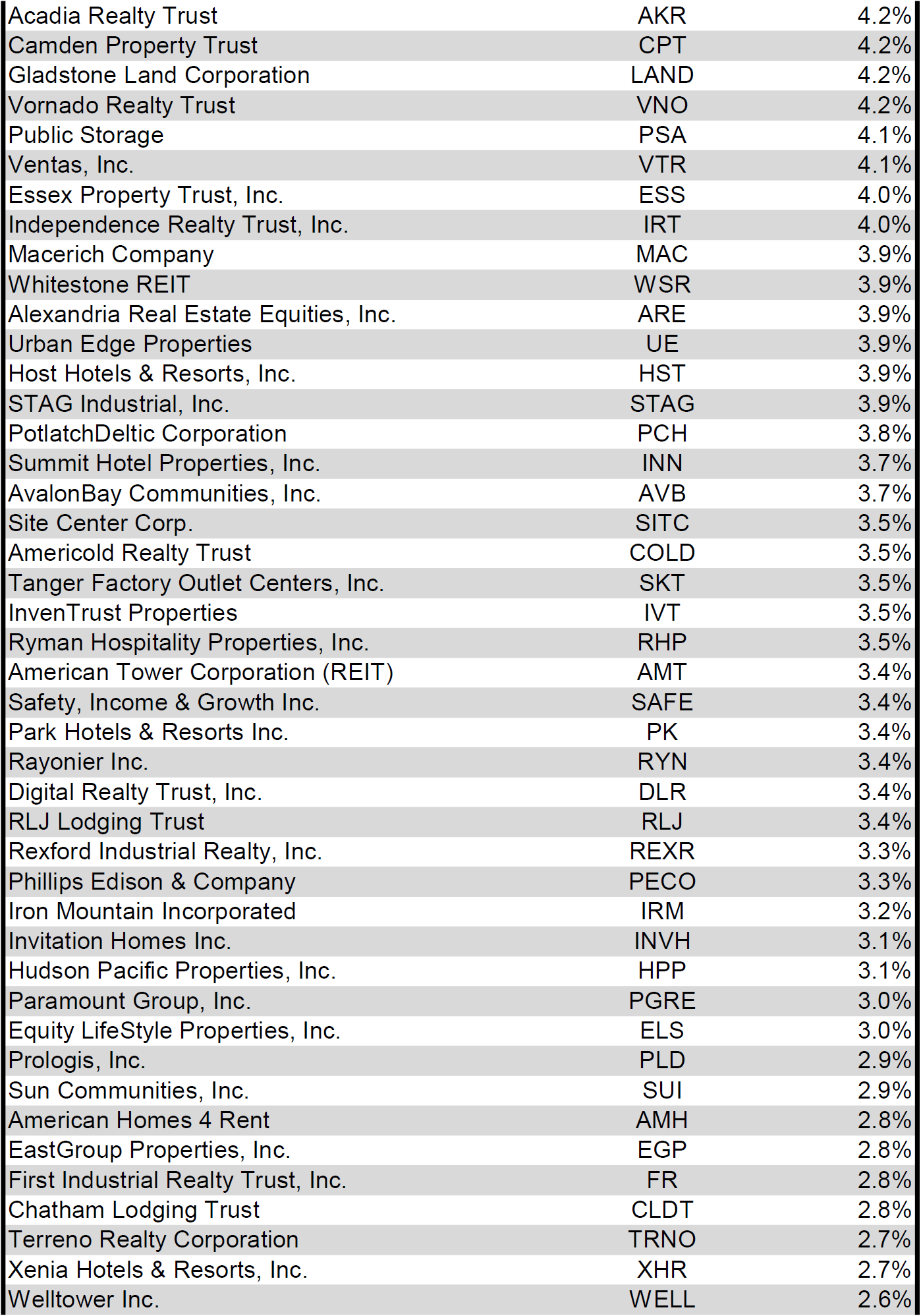

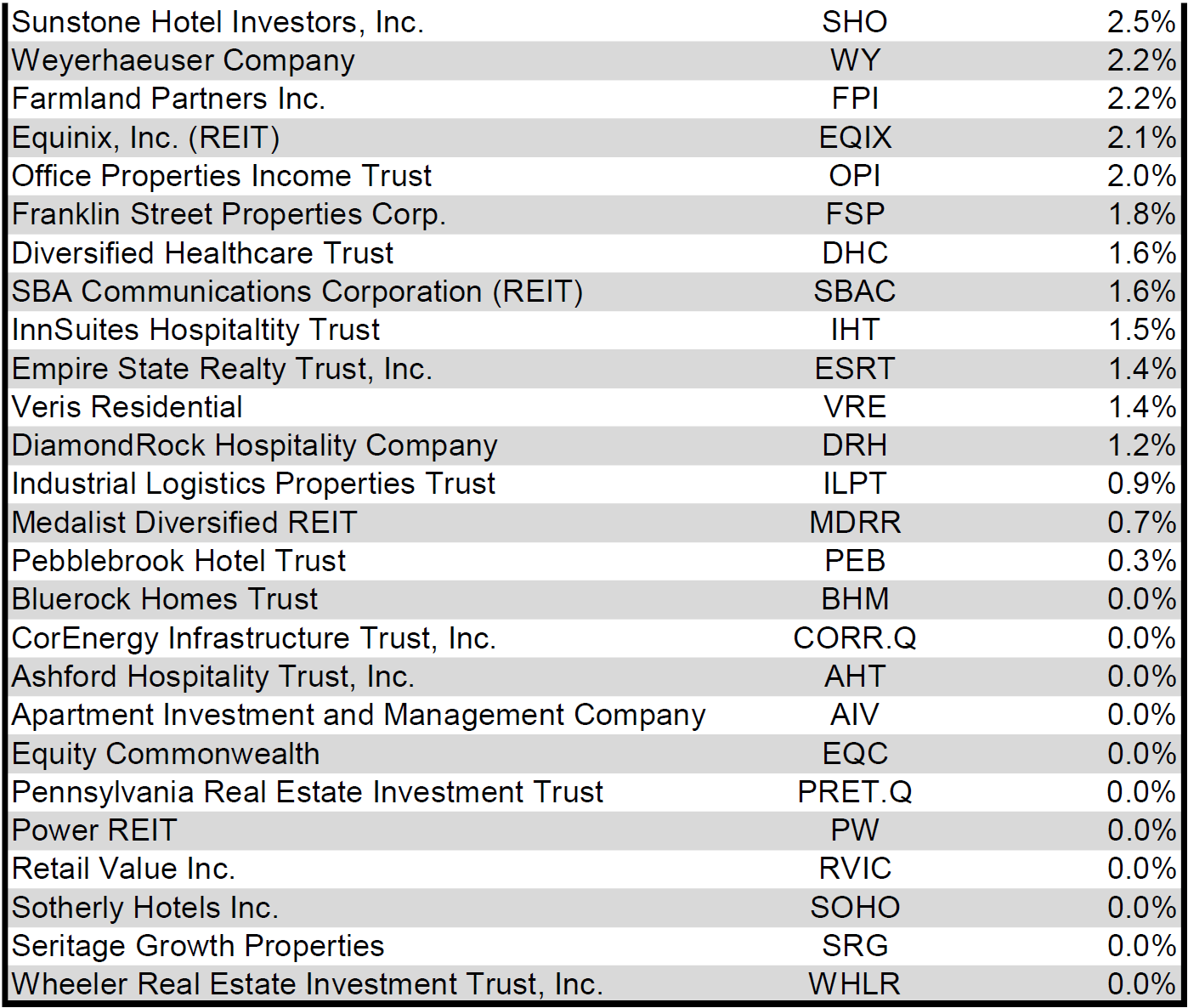

Dividend yield is a vital part of a REIT’s complete return. The significantly excessive dividend yields of the REIT sector are, for a lot of buyers, the first motive for funding on this sector. As many REITs are presently buying and selling at share costs nicely under their NAV, yields are presently fairly excessive for a lot of REITs throughout the sector. Though a very excessive yield for a REIT might typically replicate a disproportionately excessive danger, there exist alternatives in some instances to capitalize on dividend yields which are sufficiently engaging to justify the underlying dangers of the funding. I’ve included under a desk rating fairness REITs from highest dividend yield (as of 03/31/2024) to lowest dividend yield.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

For the comfort of studying this desk in a bigger font, the desk above is offered as a PDF as well.

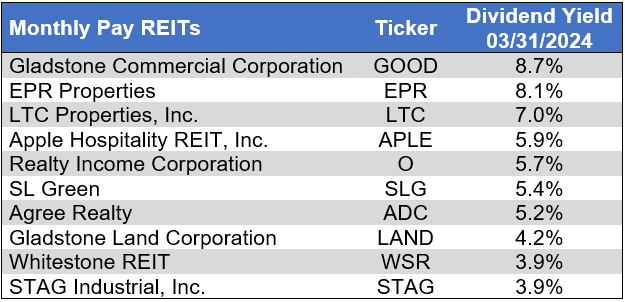

Though a REIT’s determination relating to whether or not to pay a quarterly dividend or a month-to-month dividend doesn’t replicate on the standard of the corporate’s fundamentals or operations, a month-to-month dividend permits for a smoother money move to the investor. Beneath is an inventory of fairness REITs that pay month-to-month dividends ranked from highest yield to lowest yield.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

Valuation

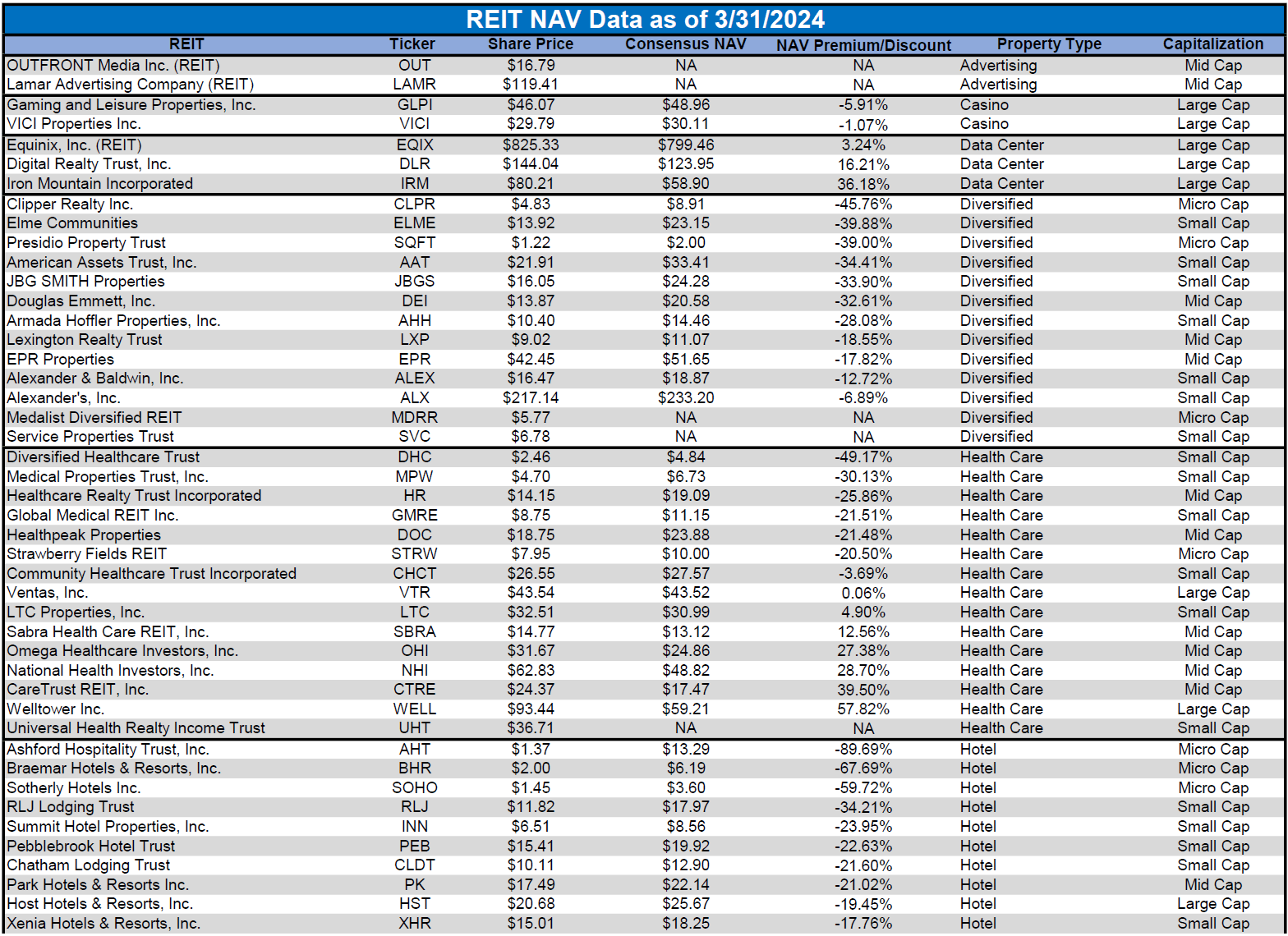

REIT Premium/Low cost to NAV by Property Sort

Beneath is a downloadable information desk, which ranks REITs inside every property kind from the biggest low cost to the biggest premium to NAV. The consensus NAV used for this desk is the typical of analyst NAV estimates for every REIT. Each the NAV and the share value will change over time, so I’ll proceed to incorporate this desk in upcoming problems with The State of REITs with up to date consensus NAV estimates for every REIT for which such an estimate is offered.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

For the comfort of studying this desk in a bigger font, the desk above is offered as a PDF as well.

Takeaway

The massive cap REIT premium (relative to small cap REITs) narrowed barely in March and buyers are actually paying on common about 35% extra for every greenback of 2024 FFO/share to purchase massive cap REITs than small cap REITs (16.9x/12.5x – 1 = 35.2%). As might be seen within the desk under, there’s presently a powerful optimistic correlation between market cap and FFO a number of.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

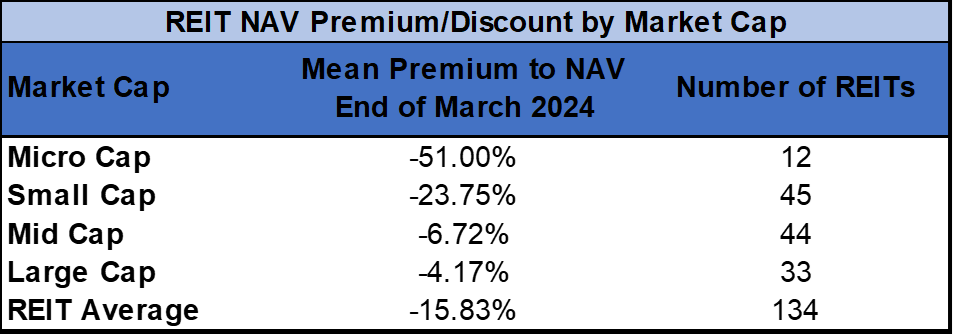

The desk under reveals the typical NAV premium/low cost of REITs of every market cap bucket. This information, very similar to the info for value/FFO, reveals a powerful, optimistic correlation between market cap and Worth/NAV. The common massive cap REIT (-4.17%) and mid cap REIT (-6.72%) commerce at single-digit reductions to NAV. Small cap REITs (-23.75%) commerce at simply over 3/4 of NAV and micro caps on common commerce at lower than half of their respective NAVs (-51.00%).

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

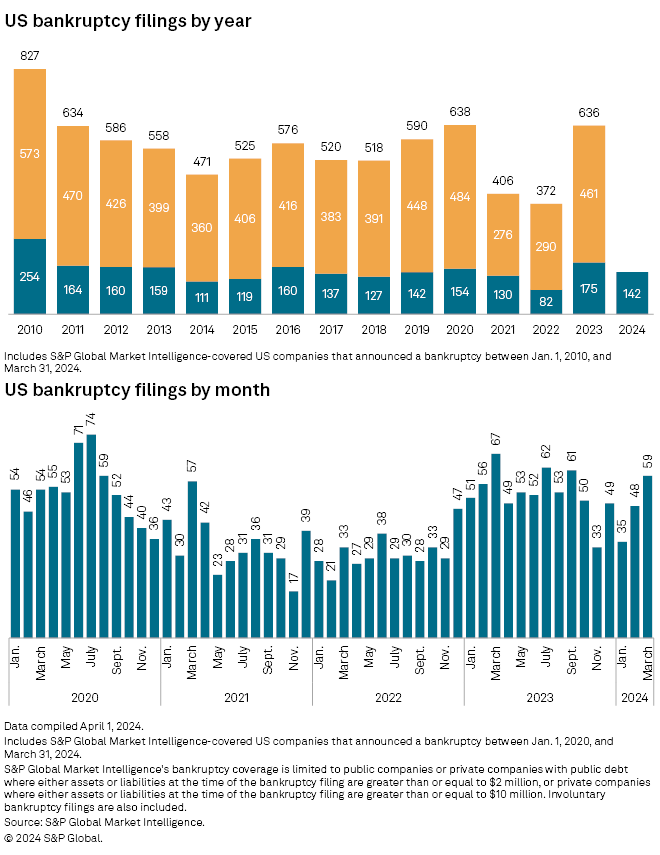

Chapter filings once more elevated month-over-month in March however have now decreased year-over-year in every of the primary three months of 2024. As of the top of Q1, 2024 chapter filings are down 18.9% in comparison with the identical interval of 2023. There have been 4.1% fewer chapter filings in Q1 2024 than the typical variety of Q1 filings since 2010.

S&P International Market Intelligence

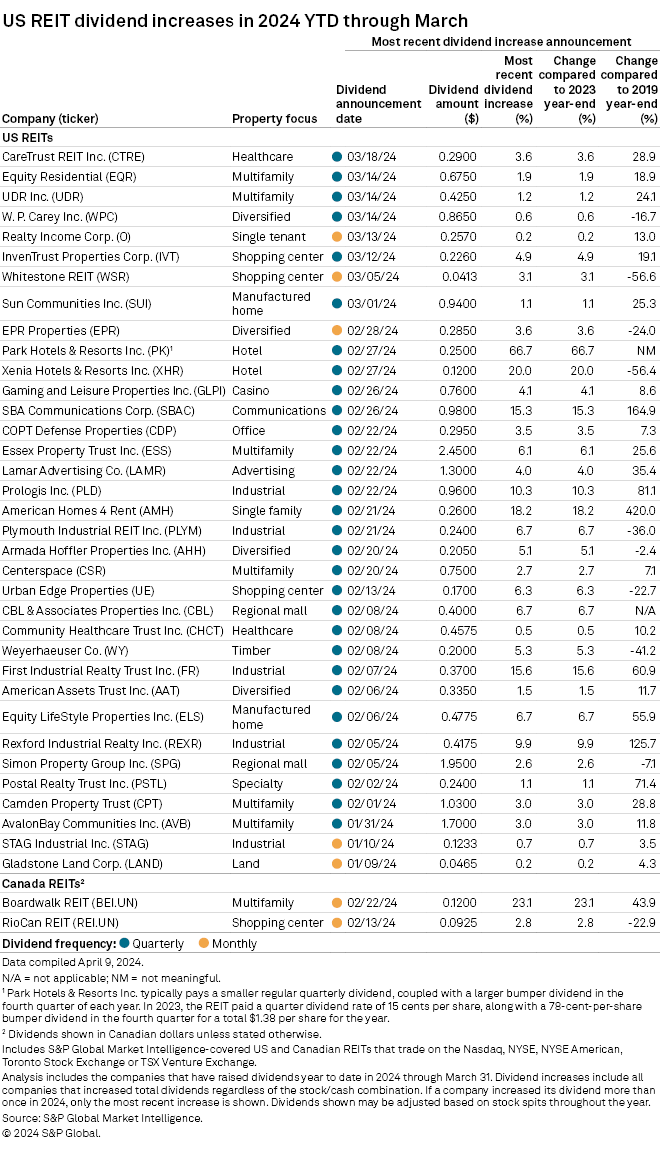

8 REITs introduced dividend hikes in March, 6 of that are quarterly and a couple of of that are month-to-month. This brings the whole to 35 REITs that raised their dividends in Q1. The most important March enhance was from InvenTrust Properties (IVT) with a +4.9% hike adopted by +3.6% from CareTrust REIT (CTRE) and +3.1% from Whitestone REIT (WSR).

S&P International Market Intelligence

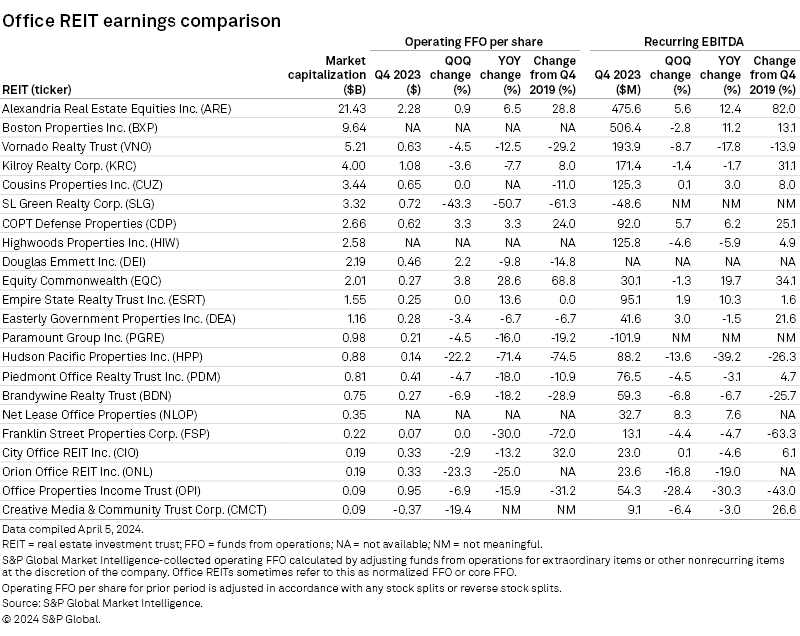

Workplace is the property kind that has arguably been the toughest hit over the previous 5 years because of the pandemic period government-imposed lockdown and the ensuing acceleration of the earn a living from home development. The workplace REITs which have seen the most important FFO/share declines since This autumn 2019 are Hudson Pacific Properties (HPP) (-74.5%), Franklin Road Properties (FSP) (-72.0%) and SL Inexperienced Realty (SLG) (-61.3%).

S&P International Market Intelligence

An ideal illustration of the truth that not all workplace properties are the identical is Alexandria Actual Property Equities (ARE). Their portfolio of high-demand life science properties is dramatically outperforming non-medical workplace properties, with working FFO/share progress of +28.8% from This autumn 2019 to This autumn 2024 and a outstanding +82% enhance in recurring EBITDA.

Supply: Desk by Simon Bowler of 2nd Market Capital, Knowledge compiled from S&P International Market Intelligence LLC. See essential notes and disclosures on the finish of this text

REIT share costs have been impacted by a unfavorable notion of fundamentals within the business actual property sector as a complete, however a comparability of general occupancy charges by property kind vs. REIT occupancy charges for a similar property varieties reveals that REIT properties are clearly outperforming the broader business actual property sector. REITs sometimes personal larger high quality belongings, which helps to gas this elementary outperformance. There are definitely quite a few dangers inside the true property sector, however the magnitude of a few of these property degree dangers is decrease for a lot of REITs on account of their superior portfolios.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.