Stewart Sutton

My Thesis

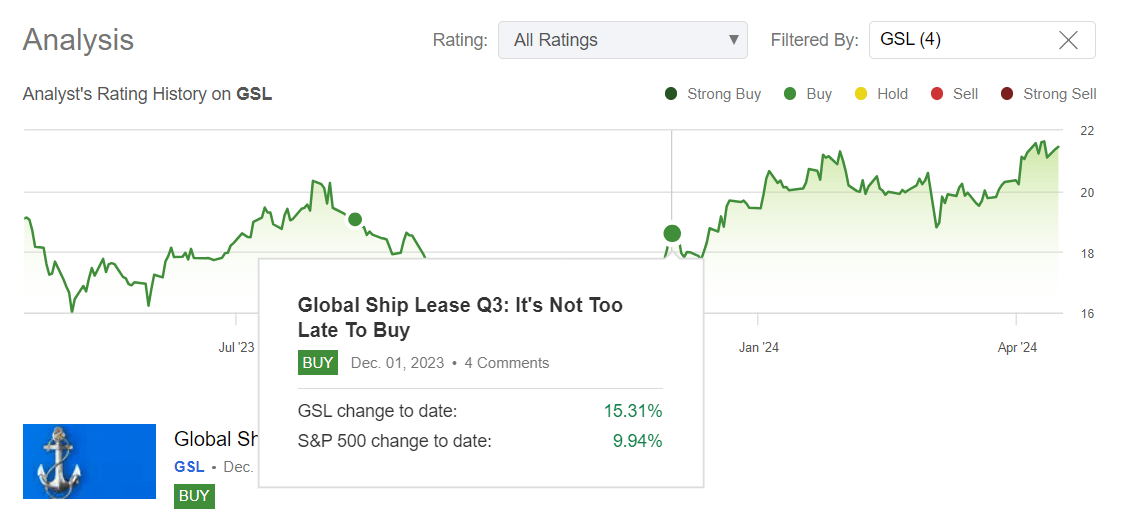

Since August 2021, I’ve revealed 4 bullish articles on International Ship Lease, Inc. (NYSE:GSL), declaring that the market was underestimating the corporate’s development prospects, which has led to a pointy valuation low cost.

In search of Alpha, Oakoff’s protection of GSL inventory

At the moment, nevertheless, I’m involved that the present undervaluation could also be justified, as new ships will quickly be coming onto the market. The present dividend yield of seven% seems to be good however doesn’t present a enough margin of security for my part. I’ve due to this fact determined to downgrade GSL to “Hold” and advocate that traders write call options or trim their current lengthy place.

My Reasoning

In early March, GSL reported its Q4 and full-year 2023 results, exhibiting an working income of $178.9 million within the final quarter, marking an 8.4% YoY enhance. For the total yr of 2023, GSL’s working income reached $674.8 million, up 4.5% from the earlier yr. Adjusted EBITDA for This fall 2023 was $127.1 million, a major rise of 27.1% YoY, whereas For FY2023, it was $462.1 million (+16.0% YoY). That’s, GSL’s monetary development gained momentum within the final quarter in comparison with the full-year outcomes. The management explained it by “geopolitical uncertainties and trade disruptions in regions such as the Red Sea and the Panama Canal, which led to a large-scale rerouting of container ships, resulting in a shortage of supply and demand for container ships.”

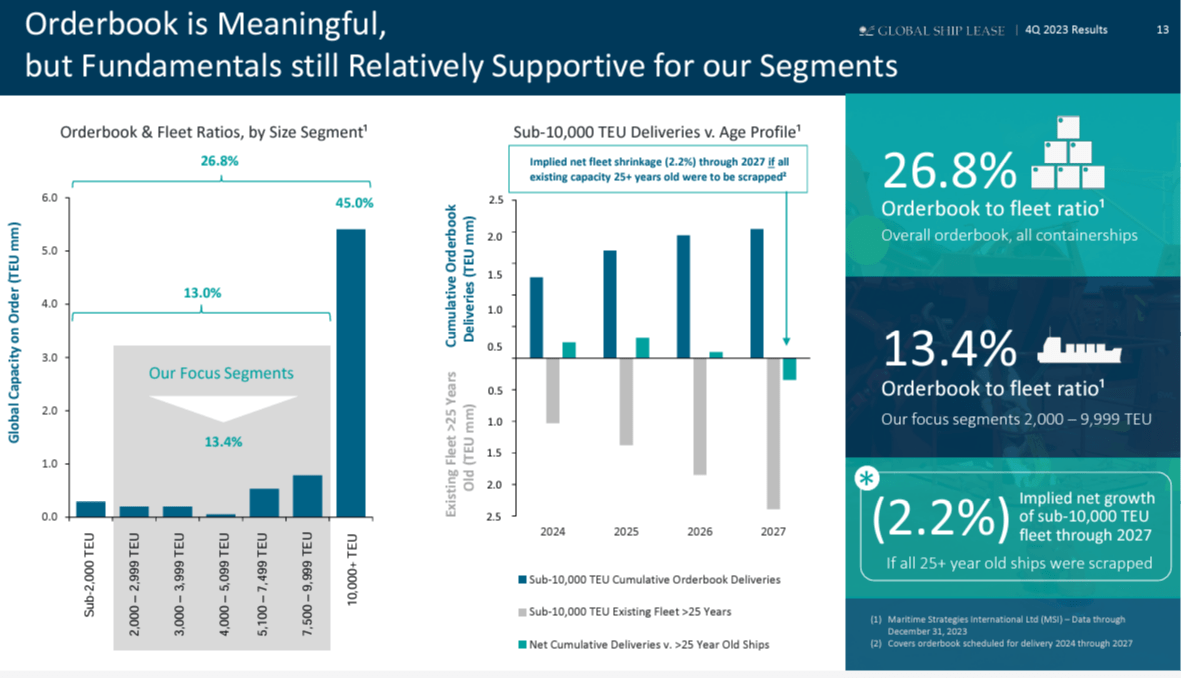

As I famous in my earlier articles on GSL, the corporate’s concentrate on high-quality, mid-sized, and smaller containerships offers it a bonus over the remainder of the market, because the shoppers (liner corporations) get entry to a extra versatile tonnage, which is essential throughout instances of uncertainty and disruption (what we’re going through so far). Primarily, the mid-size vessel market area of interest is in a positive place in comparison with bigger vessels: as of in the present day, there aren’t as many new orders for mid-size ships as there are for these over 10,000 TEU (Twenty-foot Equal Unit). So this implies there’s an opportunity to patiently navigate by means of the slower elements of the enterprise cycle. When disruptions out there now not have such a optimistic influence as they do now, being on this area of interest ought to nonetheless be advantageous, for my part.

GSL’s This fall IR presentation

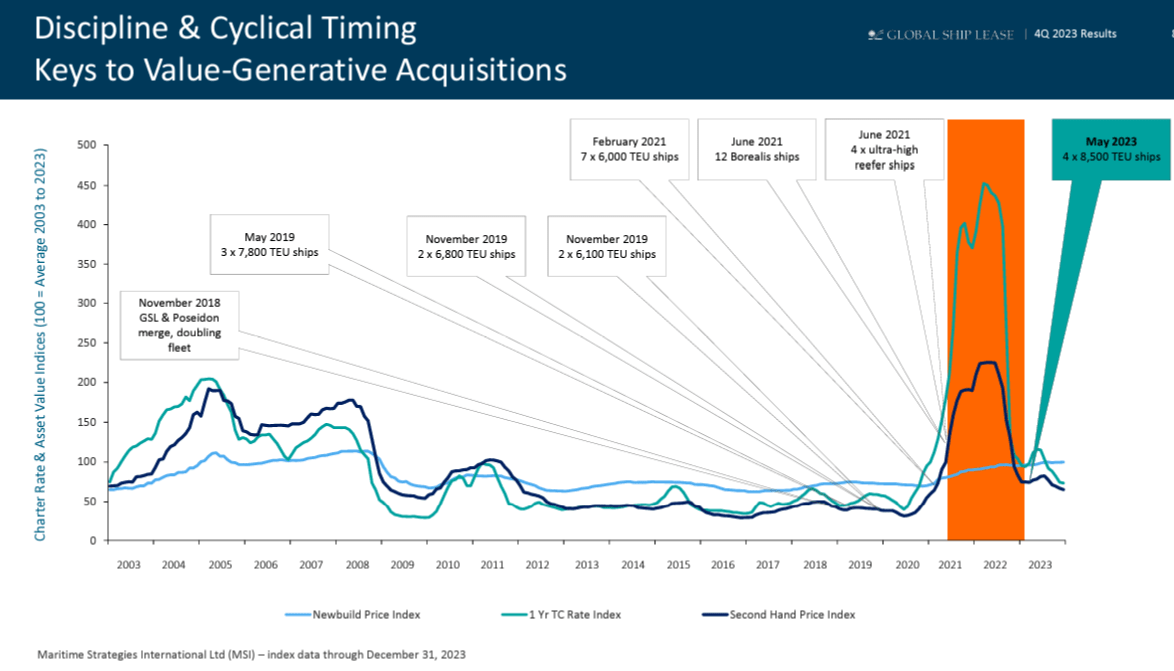

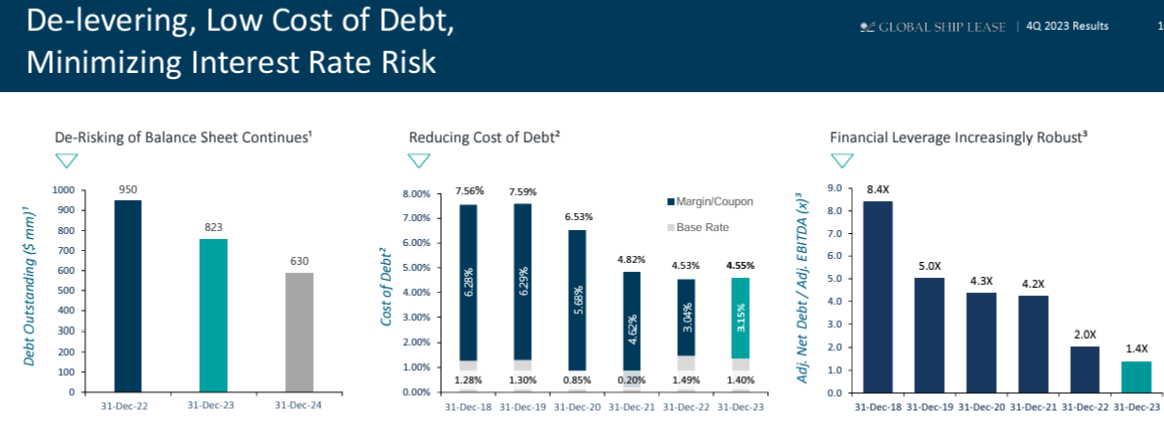

GSL ended the final quarter of 2023 with stable floor, benefiting from strong constitution cowl (2.1 years of TEU-weighted common contract cowl). GSL additionally took strategic steps and invested in its fleet and monetary standing: An essential step was the acquisition of 4 8,500 TEU vessels with connected charters, a call pushed by administration’s confidence of their potential for danger administration and return on funding.

GSL’s This fall IR presentation

Usually, fleet expansions and investments appear applicable in the present day, given the state of the corporate’s steadiness sheet and its means to generate money move. GSL’s gross debt decreased from $999.5 million in 2022 to $823.2 million in This fall 2023, whereas money amounted to $294.7 million (together with the restricted portion). Web debt to adjusted EBITDA now stands at 1.4x – instances much less in comparison with what we may have seen simply a few years in the past:

GSL’s This fall IR presentation

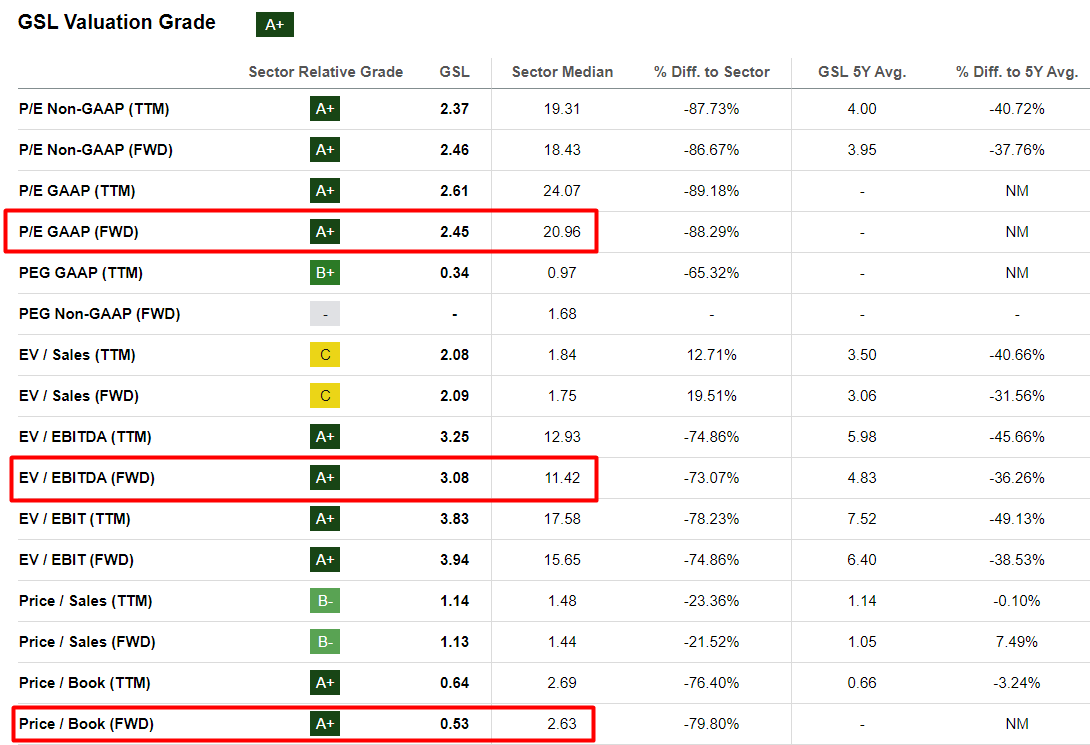

By the way in which, the present market capitalization is ~$752 million, so money is ~39% of the market cap, which is lots. With a P/E ratio for the following yr of two.45x and an EV/EBITDA (additionally forwarding) of barely greater than 3x, the company’s valuation certainly appears very favorable to me:

In search of Alpha, GSL’s Valuation, Oakoff’s notes added

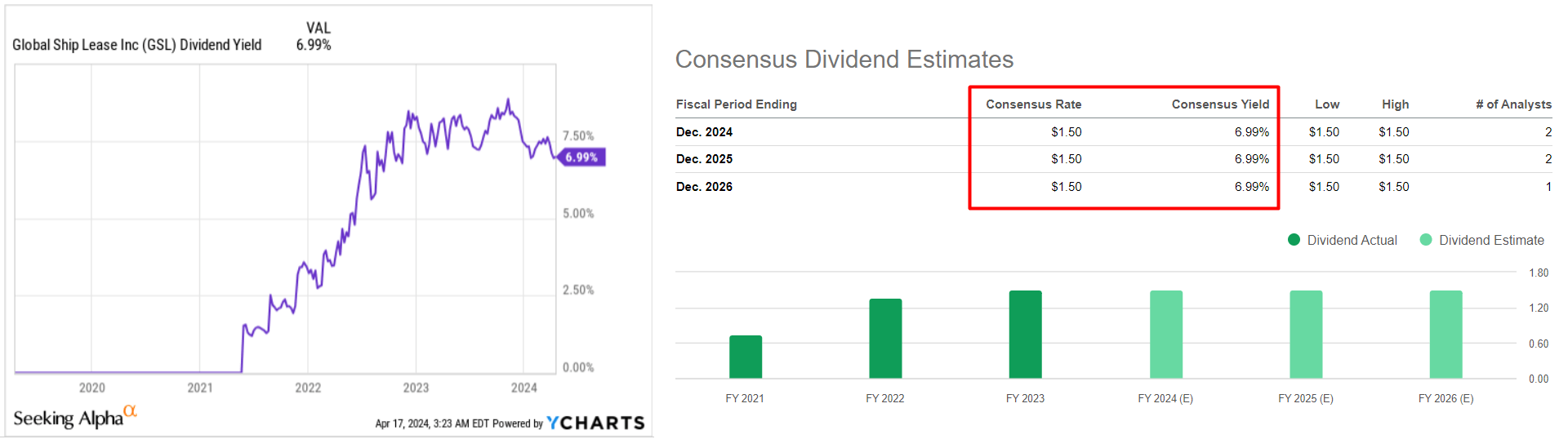

On the identical time, the corporate continues to purchase its shares from the market – because the third quarter of 2021, GSL has already purchased $54.5 million price of shares, representing >7% of its present market capitalization. As well as, GSL has maintained its quarterly dividend of $0.375 per share – the FY2024 dividend yield is now ~7%, and consensus expects the yield to stay the identical over the following 3 years:

YCharts, In search of Alpha, GSL, Oakoff’s notes added

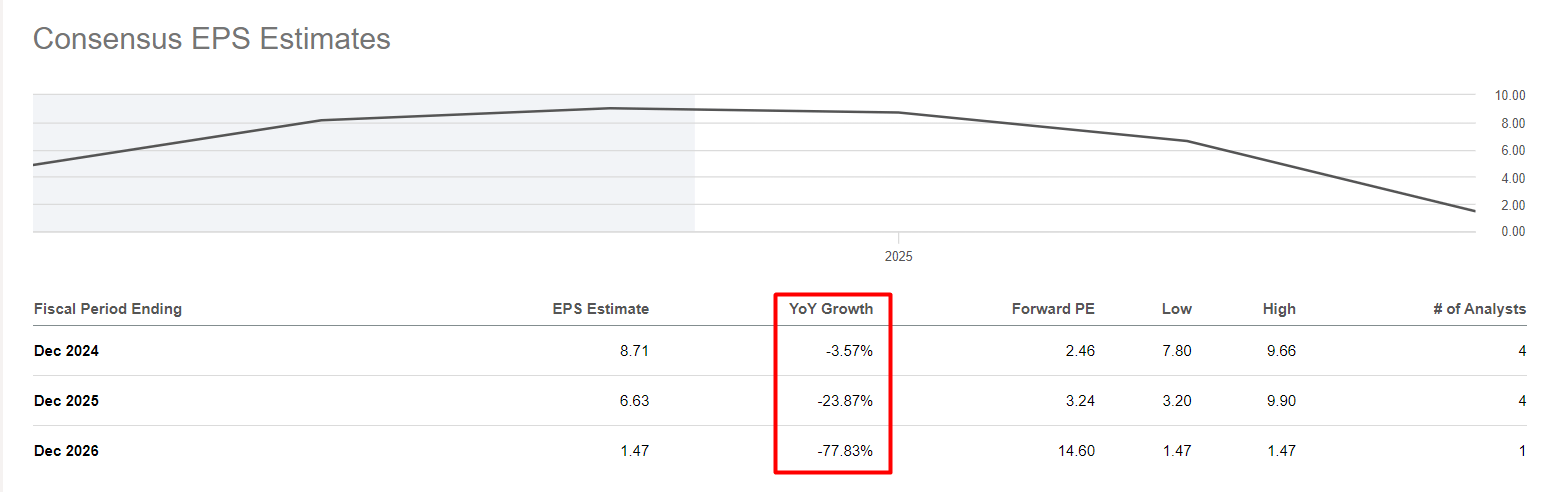

Up to now in my story, GSL has regarded like an apparent “Buy”, however there are some nuances to think about. First, the state of affairs across the commerce disruptions appears too unpredictable. It is nonetheless a tailwind for now, but when it all of the sudden subsides, we’ll very probably see what the consensus estimates are warning us about in the present day: the decline in revenues as the availability of recent ships continues to extend.

In search of Alpha, GSL, Oakoff’s notes added

Which means that by the tip of 2026, the presently favorable P/E ratio must be round 14.6x – that may be a huge distinction to my thesis.

Secondly, wanting on the dividend yield of seven% for the following 3 years, I can not convey myself to name GSL’s shareholder return enough, even bearing in mind the share buybacks. For my part, this 7% signifies restricted upside potential. In fact, with the present transportation disaster nonetheless ongoing (and judging by the geopolitical situation in the Middle East, there is no such thing as a finish in sight), it’s unlikely that dividend forecasts 3 years forward will show to be the last word fact. However counting on the continued uncertainty as an upside catalyst on this state of affairs isn’t very wise for my part.

Your Takeaway

I like the way in which International Ship Lease’s monetary state of affairs seems to be in the mean time: The steadiness sheet is powerful; the leverage is steadily lowering, and the contract revenues are enough for stable FCF era within the coming quarters. You possibly can name me too demanding, however I don’t like that GSL’s dividend yield is just 7%, contemplating the danger of the brand new provide of vessels coming to the market quickly – the yield must be larger for GSL to be known as “cheap”. The worth/earnings ratio is low in the present day, however as we will see from the consensus forecasts, it ought to rise considerably in 3 years. All this confuses me a bit – so I’ve determined to downgrade GSL to “Hold” in the present day.

Whereas geopolitics is taking part in into the palms of the bulls, I feel it is sensible to promote short-term name choices and gather the premium on an current lengthy place. However earlier than you enter the choices market, I extremely advocate you research this subject in additional element (I’m not an professional in derivatives buying and selling).

Good luck together with your investments!