Diego Thomazini

Symbotic Inc. (NASDAQ:SYM) leverages its synthetic intelligence and robotics expertise to drive effectivity inside warehouses. This expertise naturally gravitates in direction of the biggest retail, grocery and wholesaling corporations, with Walmart Inc. (WMT) being its dominant buyer. The corporate has grown at an unimaginable tempo and is on the cusp of profitability. Nevertheless, there are some dangers that make me hesitant to be a long-term holder of this inventory. As a substitute, I shall be watching the following earnings report intently and assessing the potential for a place at the moment. As the corporate is about to report its Q2 2024 leads to two to a few weeks (estimated May 6th, final yr it was launched Could 1st), traders and merchants ought to keep watch over this comparatively obscure inventory.

Heavy development and shrinking losses, in addition to a valuation that is not as aggressive because it first appears

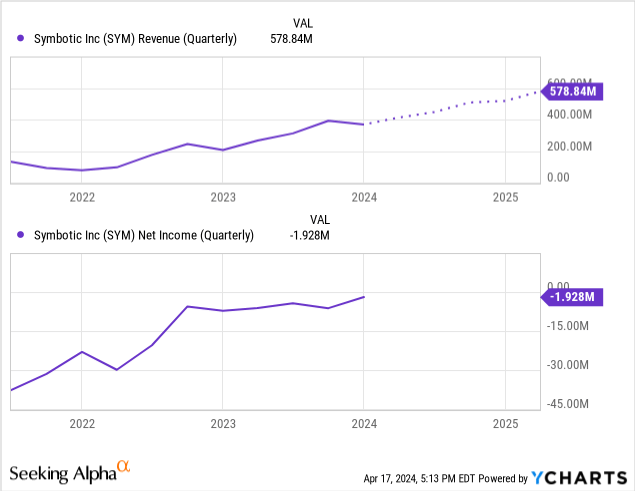

SYM sits in that candy spot of corporations that I typically like for speculative investing – heavy development that is about to show money circulate constructive. The corporate had an outstanding fiscal 2023 with income doubling from $593 million to $1,177 million. As soon as heavy internet losses have additionally been rapidly dissipating. In fiscal Q1 2024 ended December 2023, SYM achieved income of $369 million, a internet lack of $13 million and adjusted EBITDA of $14 million. This compares favorably to Q1 2023 when the corporate had income of $206 million, a internet lack of $68 million and an adjusted EBITDA lack of $16 million. The next chart illustrates the sample of bettering working efficiency:

As income is projected to shut in on $600 million per quarter in 2025, there’s a good probability that the corporate will obtain money circulate constructive operations by then. Nevertheless, with this development comes a seemingly aggressive valuation. SYM is graded a C- by Seeking Alpha, with all income, earnings, money circulate and e-book worth metrics coming in properly above business averages. Nevertheless, the trailing 12-month and even ahead wanting valuation metrics do not inform the total story. A joint venture with GreenBox has resulted in order backlog rising to $23 billion. The corporate is valued at barely greater than 1x of its backlog. To meet this backlog would suggest years of heavy income development. It will additionally consequence within the diversification of SYM’s buyer base which is crucial given what I’ve recognized as the one largest alternative but in addition single largest risk to the corporate’s future.

The Walmart threat makes me hesitant to be a long-term holder

The chance that retains me cautious of holding this inventory might be summed up in a single phrase: Walmart. What’s the firm’s biggest driver of success additionally hangs over the corporate’s head like a knife. This threat is clearly demonstrated in a single chart on the company’s annual report ended September 30, 2023:

SYM’s annual report

From fiscal 2022 to 2023, “Customer A”, aka Walmart grew from 39.5% of income to 86.6% of income. Whereas income grew from $593 million to $1,177 million, income attributed to Buyer A grew from $234 million to $1,019 million. Meaning income from all different sources truly shrank from $359 million to $158 million. The heavy backlog generated from the GreenBox JV will diversify SYM’s buyer base. Nevertheless, as of this second ought to Walmart ever discover another resolution, the harm performed to SYM can be catastrophic. Walmart can also be a notoriously onerous negotiator, forcing gross margins of their distributors right down to the bottom potential level. Gross margins for SYM sit at just below 20%. Whereas income development has resulted within the margins slowly climbing in direction of that 20% mark, there isn’t any telling if the corporate’s largest buyer will demand a few of that margin for itself.

Offsetting this working threat is the truth that Walmart owns a considerable quantity of shares, over 76 million between all classes of common stock, or a 13% stake. Walmart has an awesome incentive to maintain SYM robust whereas proudly owning over $3 billion value of inventory. Nevertheless, ought to Walmart disclose that it has or intends to promote a few of these shares, that provides one other layer of threat to holding SYM inventory outdoors of working efficiency points.

Given the excessive dependency on Walmart and the catastrophic impression on each SYM’s enterprise and inventory value ought to that relationship deteriorate in any manner, I really feel extra snug slapping a impartial opinion on SYM inventory and taking a look at choose alternatives to carry the inventory relatively than being a long run holder.

How I shall be taking part in SYM because the fiscal Q2 report nears

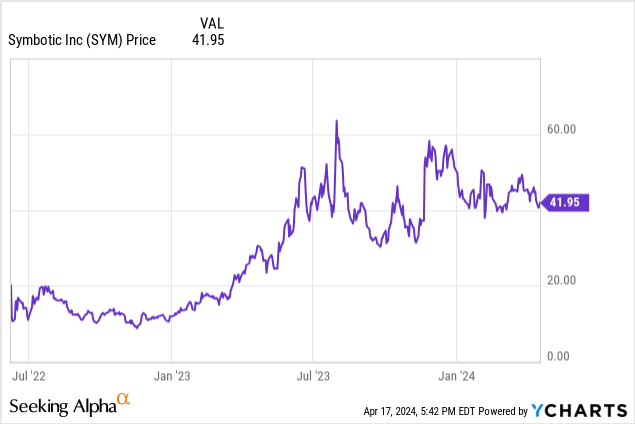

Offered beneath is a chart of the final three earnings releases, the steering that was disclosed within the earlier quarter’s launch, the inventory value on the open, the inventory value on the shut and yesterday’s inventory value.

SYM SEC filings, Yahoo Finance

Q3 2023 and Q4 2023 noticed great beats in comparison with forecast. That resulted in will increase in SYM in comparison with yesterday of fifty% and 40%, respectively. Q3 noticed a 38% intraday transfer upward from the open, accounting for almost all of the achieve. In distinction, most of This autumn’s achieve was a spike from yesterday, however nonetheless managed a 9% intraday enhance from the open. Whereas Q3 noticed a pullback into the $40s inside two weeks, This autumn noticed a spike to just about $60 within the 4 days following the earnings launch earlier than additionally finally pulling again into the $40s. The expectations for Q1 have been so sky-high that though it hit the highest finish of steering, the inventory value sank 24% on the day, with an 8% drop from the open.

The corporate has projected between $400 and $420 million in income for this upcoming quarter. For SYM to have an analogous response because it had with Q3 and This autumn 2023 outcomes, my guess is the income would should be north of $450 million. Ideally inching even nearer to profitability on file EBITDA outcomes. With quarterly income being such a low proportion of the $23 billion in contract backlog and quarter-to-quarter income being so unstable (Fellow Looking for Alpha analyst Miletus Analysis explains the unpredictability round SYM’s delivery-based income recognition fairly properly), I do not even need to attempt to verify if SYM can beat its forecast. Latest historical past has proven that it is a significantly better risk-to-reward proposition by ready for the outcomes to return out, then assessing a purchase or promote technique after the actual fact.

Since saying its excellent beat for fiscal Q3 final July, the inventory has been vary certain. It has given again most of its positive aspects seen instantly after Q3 outcomes regardless of continued huge development in income. SYM’s short interest is over 20% of the float. This can be a results of the float being a lot smaller than the total share rely due to insider possession, Walmart’s possession stake and the completely different lessons of widespread shares. The brief curiosity can act as gasoline to the hearth for a superb quarter as shorts scramble to cowl earlier than they get margin calls. It will possibly additionally reverse the downtrend of a disappointing quarter as shorts take the chance to cowl low. Nevertheless, a excessive brief curiosity can even cap the positive aspects over the long term as an aggressively shorted inventory is mostly an indication that skilled market gamers really feel the inventory is overvalued indirectly.

Whereas SYM has a really tempting development and profitability profile, the reliance on Walmart, the inventory’s tepid response to continued aggressive income development since Q3 and brief curiosity has me leaning in direction of a impartial opinion on the inventory. I shall be reviewing the following quarterly outcomes intently to see if that can change.