champpixs

CAH is overvalued

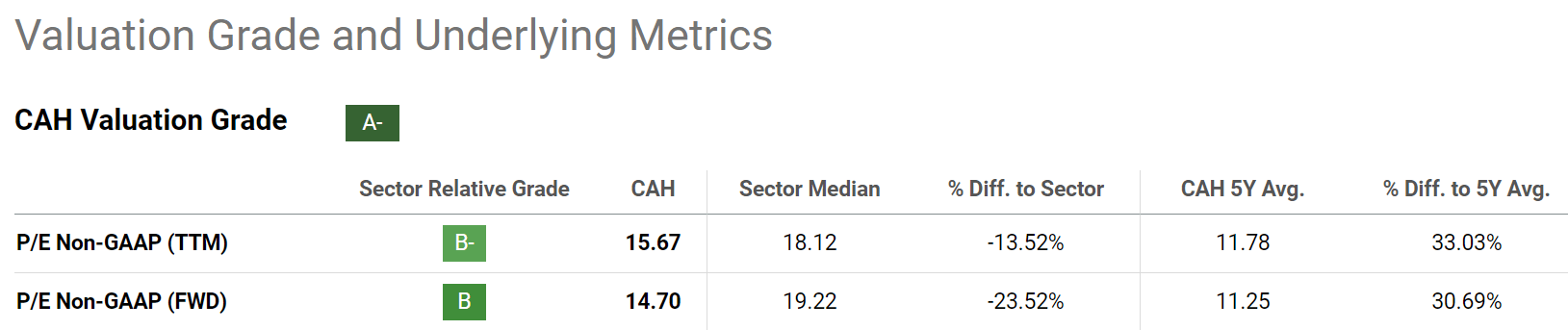

Cardinal Well being (NYSE:CAH) caught our consideration just lately after we have been screening for shares with yields noticeably exterior their regular vary. And CAH actually caught our consideration as a result of its dividend yield is presently means out of its historic vary. As you may clearly see from the charts beneath, its present yield of 1.88% is among the many lowest ranges in at the very least 5 years. It’s decrease than its 5-year common yield of three.25% by a whopping 42%, implying substantial overvaluation. Different valuation metrics comparable to P/E paint the identical image. As seen within the second chart beneath, at its present value of $106 as of this writing, it’s buying and selling at a TTM P/E of 15.7x, about 1/3 above its 5-year common.

When the valuation ratios are so out of the bizarre vary for a mature inventory like CAH (BTW, it’s a dividend champion), our rapid response is that the inventory has gained a brand new essential development catalyst just lately so it might probably develop at extraordinary charges now relative to its previous. However that’s not what I see after digging into the inventory additional, as detailed subsequent.

Searching for Alpha Searching for Alpha

Progress projections

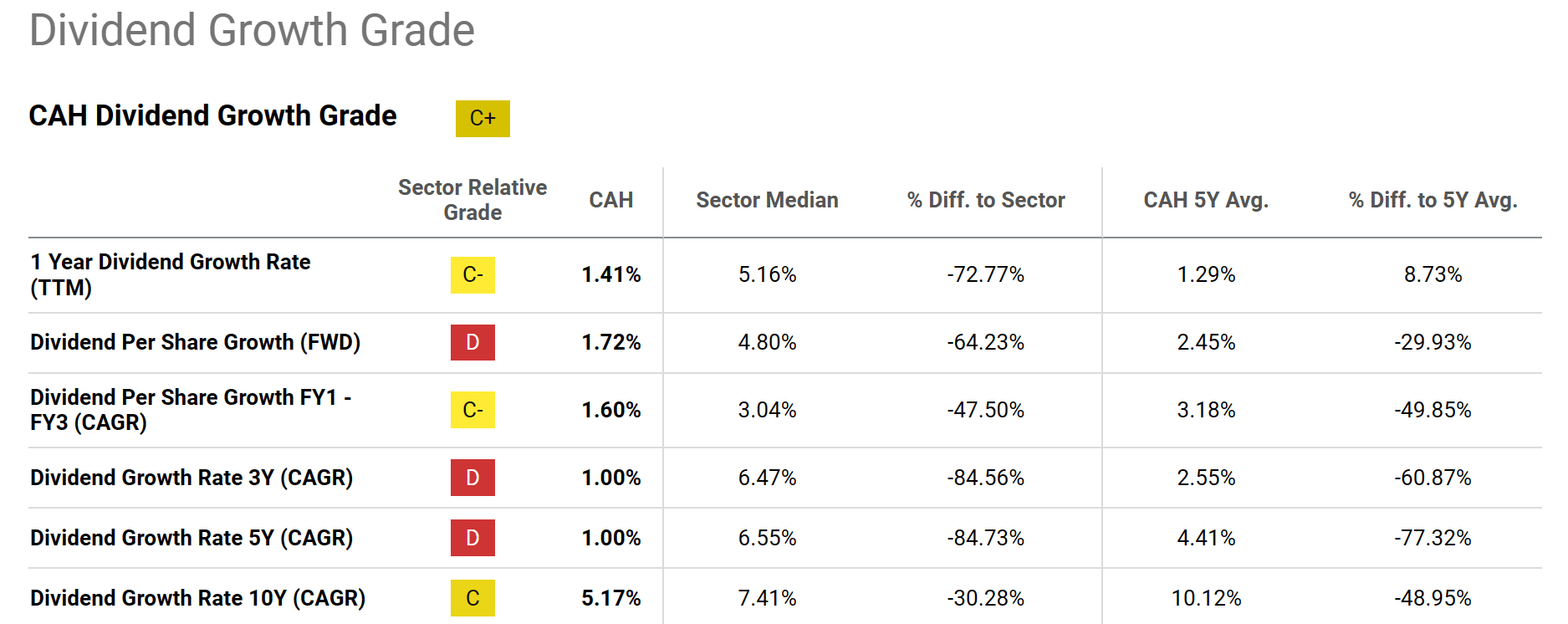

The following chart exhibits CAH dividend development charges in recent times. Given its dividend champion standing, I feel it is rather affordable to make use of its dividend payouts as an indicator of its true financial earnings. Below this assumption, I do probably not see something standing out by way of development charges. Total, CAH receives a dividend development grade of C+ solely. Its dividend development charge has been within the vary of 1.41% to 1% previously 1, 3, and 5 years. And the FWD development charge is projected to be at 1.72%, barely increased however not sufficient to justify the valuation premium simply talked about.

Searching for Alpha

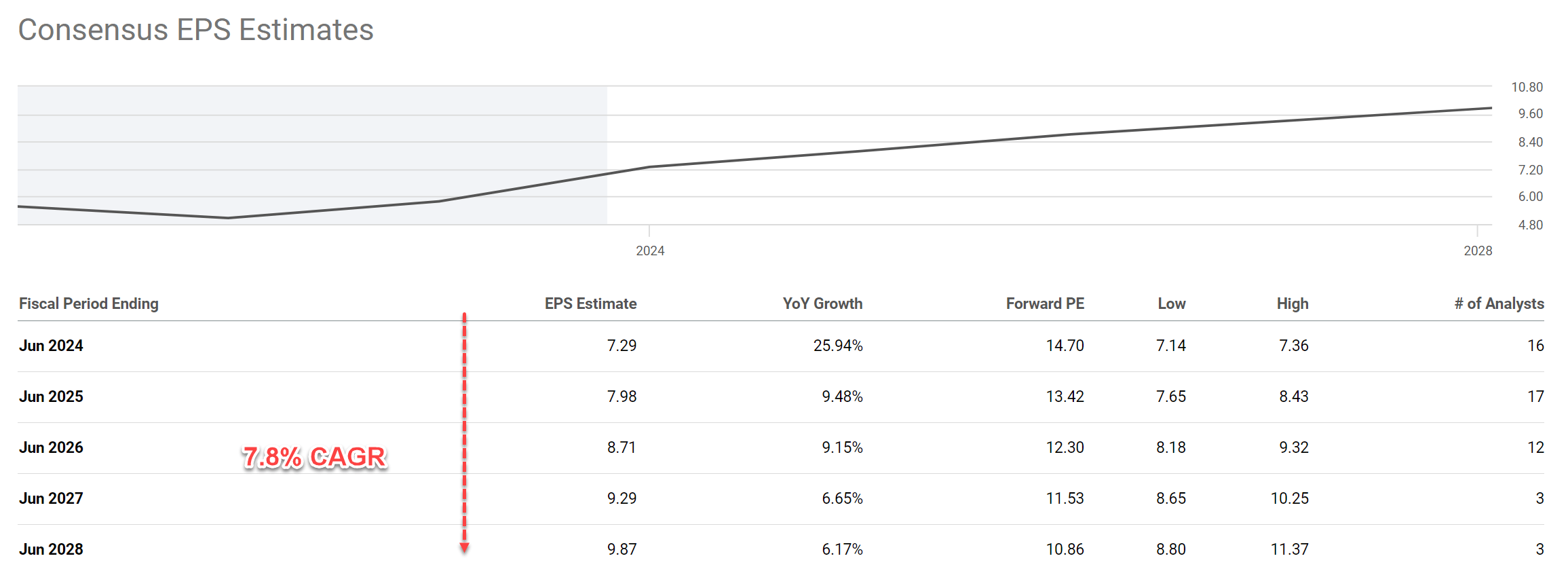

Trying additional out, consensus initiatives a average development charge within the mid-single digits for the following 5 years. Based mostly on the estimates of EPS proven within the desk beneath, analysts have consensus estimates for CAH’s future earnings to develop at a 7.8% CAGR for the following 5 years. Extra particularly, for FY 2024, its EPS is estimated to be $7.29, representing a reasonably large YoY development of 25.94%. However beginning in FY 2025, its EPS is estimated to develop at a way more tempered charge, leading to a median development charge of round 7.8%.

Subsequent, I’ll argue that A) such a projection is on the aggressive finish, and B) even at this development charge, the inventory remains to be fairly overvalued.

Searching for Alpha

Return projections

My methodology for estimating the natural development charges of mature is detailed in my different articles. The outcomes are that:

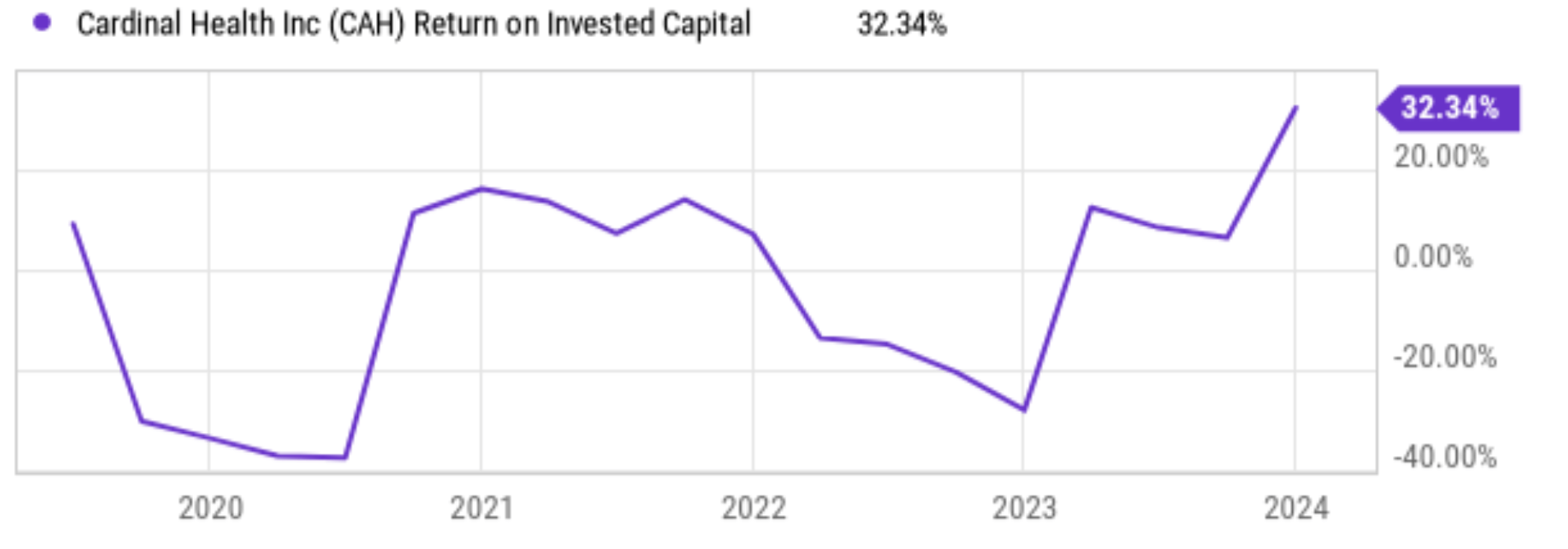

The tactic entails the return on invested capital (“ROIC”) and the reinvestment charge (“RR”). The ROCE for CAH is round 32% presently as seen within the chart beneath. Its RR is about 10% on common. With these inputs, CAH’s development charge could be ~3.2% (32% ROIC x 10% RR = 3.2%). Be aware this quantity is the actual development charge with out inflation. To acquire a notional development charge, one would wish so as to add an inflation escalator. Assuming a median inflation of two.5% would deliver the terminal development charge to five.7%.

Due to this fact, I feel the above consensus estimate is on the extra aggressive finish. Moreover, word that CAH’s ROIC has been fairly uneven in recent times and its present ROIC of 32% is among the many peak stage in at the very least 5 years. I anticipate its common ROIC to be decrease in the long term.

Searching for Alpha

Now, on to return projections. Once more, given its dividend champion standing, CAH is a case to use the discounted dividend mannequin (“DDM”). To be extra particular, I’ll use a two-stage DDM mannequin. As detailed in my earlier article:

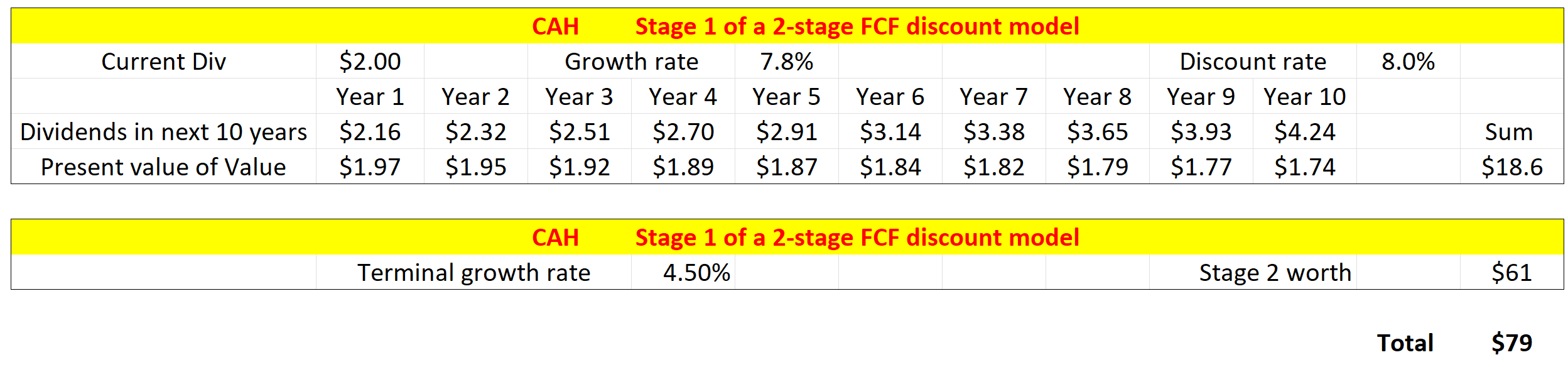

There are a complete of three key parameters within the 2-stage DDM: the low cost charge, the expansion charge in stage 1, and the terminal development charge. For the low cost charge, I relied on the so-called WACC, the weighted common price of the capital mannequin. The low cost charge for CAH is about 8.0% on common in recent times following this mannequin.

For the expansion charge within the 1st stage, I might be on the beneficiant facet and use the CAGR of seven.8% implied within the consensus projections. Additional, I will even prolong this development charge for five years, basically assuming its earnings can develop at a 7.8% annual charge for the following 10 years.

For the terminal development charge, I’ll assume it might probably maintain the identical ROIC because it did previously 7 years (which turned out to be round 20%) and the identical 10% RR. I additionally assumed an inflation escalation issue of two.5%. All these result in a nominal development charge of 4.5%.

With all of the parameters estimated above, the following desk summarizes the outcomes. Be aware I used its FWD dividend of $2.0 per share. The truthful value of CAH is round $79. Even below all of the somewhat aggressive assumptions, there may be nonetheless an excessive amount of valuation threat to my liking in comparison with its present value of $106.

Writer

Different dangers and remaining ideas

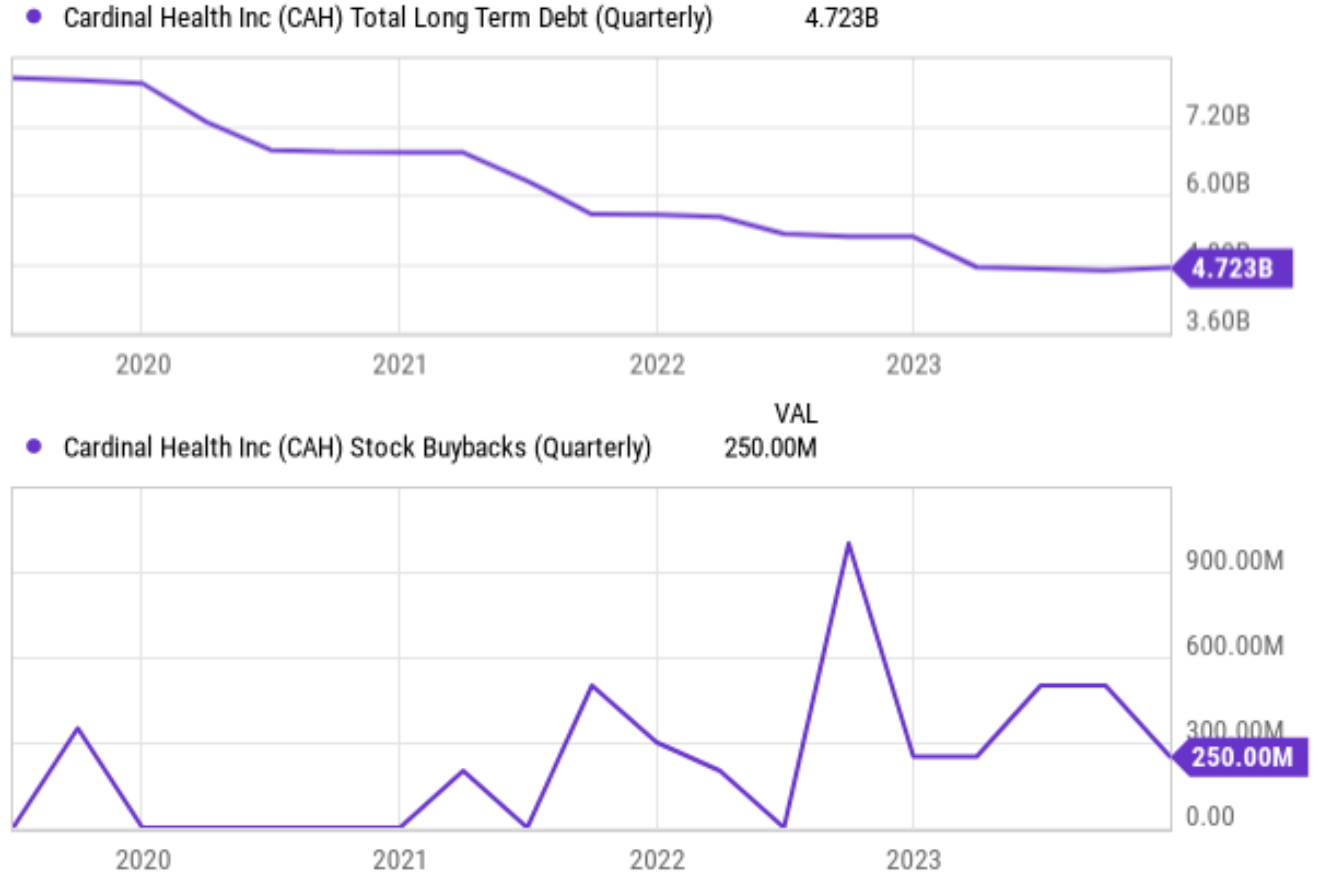

I have been specializing in the draw back dangers up to now. And there are some highlights in its enterprise fundamentals that I must level out. The Pharmaceutical division is a key development space in my opinion. It has been reporting double-digit YOY development charges in current quarters. I anticipate the momentum to proceed, pushed by model and specialty pharmaceutical gross sales development from present prospects. Additionally, the corporate enjoys robust monetary power, which I anticipate to turn into even stronger as the corporate makes use of its earnings to pay down debt (see the highest panel of the following chart) and increase its liquidity place. As a matter of truth, in spite of everything these, the corporate nonetheless has further money to be a constant purchaser of its personal shares (see the underside panel of the chart beneath).

Weighing the above elements, I charge CAH as a maintain below present circumstances. Its distinguished place within the secure pharmaceutical distribution business gives some safety. Its future earnings development projections are average, however wholesome sufficient for a mature enterprise. My foremost concern is the valuation dangers. The present excessive P/E ratio and low yield recommend the inventory is considerably overvalued, severely limiting the potential upside.

Searching for Alpha