istanbulimage

Funding Thesis

Opera (NASDAQ:OPRA) appears to have been navigating by a type of renaissance previously twelve months or so, and the current DMA regulation in opposition to appstore platforms ought to present much-needed impetus for the corporate.

Nonetheless, I imagine the firm nonetheless has an elevated danger profile arising from focus dangers that concentrate on a couple of income drivers and an opaque shareholder base, which explains why the corporate is buying and selling at a ahead EV/EBITDA of simply 11x regardless of demonstrating working earnings development persistently for the previous three quarters. Additionally, buyers appear to be overlooking the projected 5.3% dividend yield, suggesting dangers lurk on the horizon.

Given the combo of danger and reward for Opera, I’ll advocate a Maintain ranking for the time being as I look ahead to its Q1 FY24 earnings report next week.

Opera laps a vital 2023 heading into Q1 2024

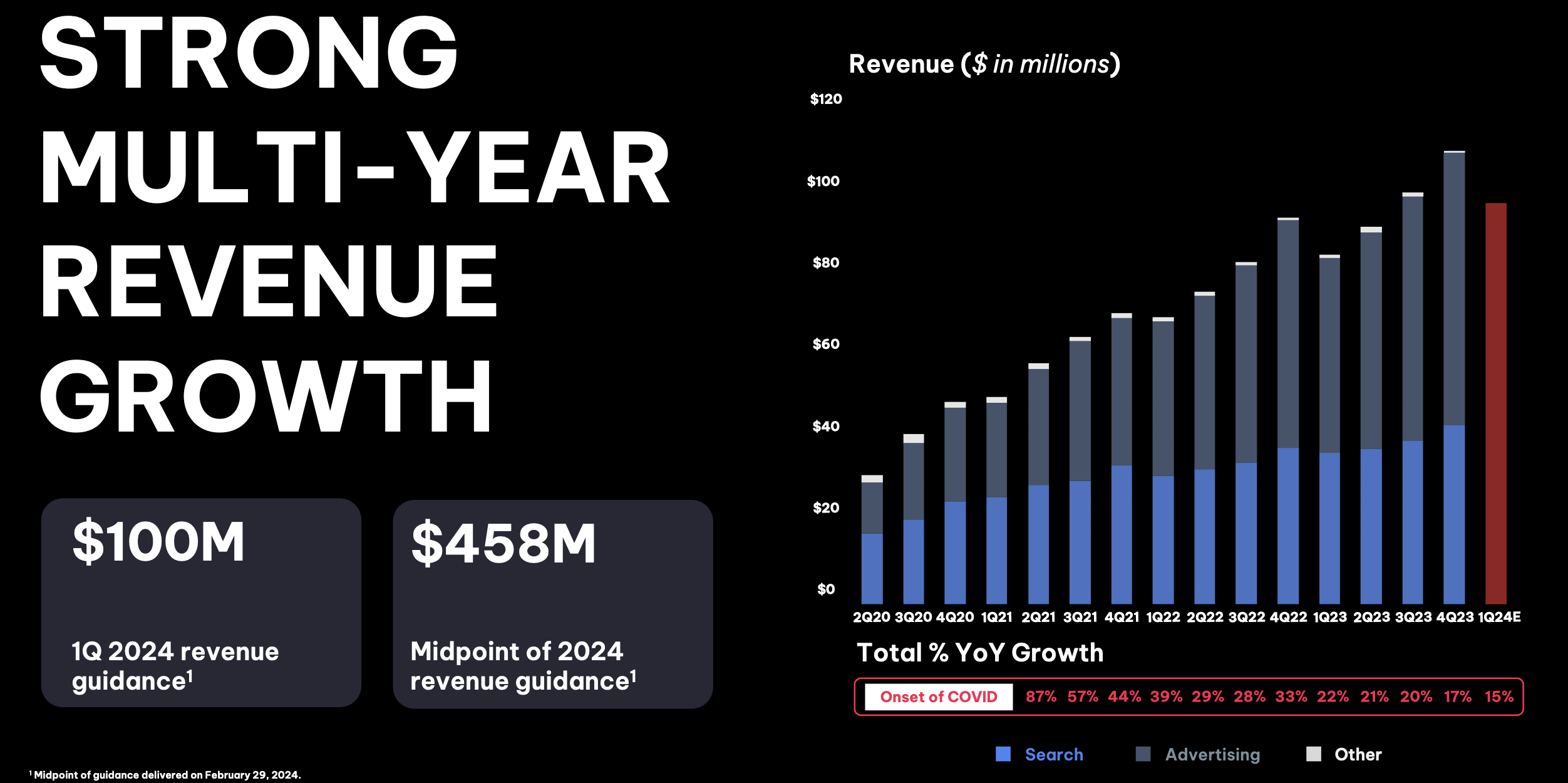

Within the full year FY23 earnings report, the Oslo, Norway-headquartered firm, reported This autumn FY23 adjusted EBITDA of $27.8 million at a 25% EBITDA margin, forward of midpoint consensus expectations of $23 million. For the total 12 months, adjusted EBITDA grew 38% to $94 million on the again of a 20% improve in FY23 income to $397 million.

Per my evaluation, the browser firm continued to profit from a string of development initiatives that that they had laid out in the beginning of the 12 months, as seen within the chart beneath, which gave a lift to their income.

Opera’s browser merchandise are securing extra income on account of advertisements (FY23 Investor Presentation, Opera)

Within the first quarter earnings call final 12 months, administration spelled out a couple of high-level methods, prime amongst them being integrating Opera’s browser into units manufactured by OEM system producers akin to PCs and gaming units. This has allowed Opera to increase its advert stock throughout browsers and different browser-related merchandise, giving it the enhance that may be seen from Promoting income on the again of its Ads Product Platform.

|

Promoting Income Section |

This autumn FY23 |

Q3 FY23 |

Q2 FY23 |

Q1 FY23 |

|

Y/Y Development |

20% |

24% |

25% |

26% |

|

% of Whole Income |

60% |

59% |

57% |

56% |

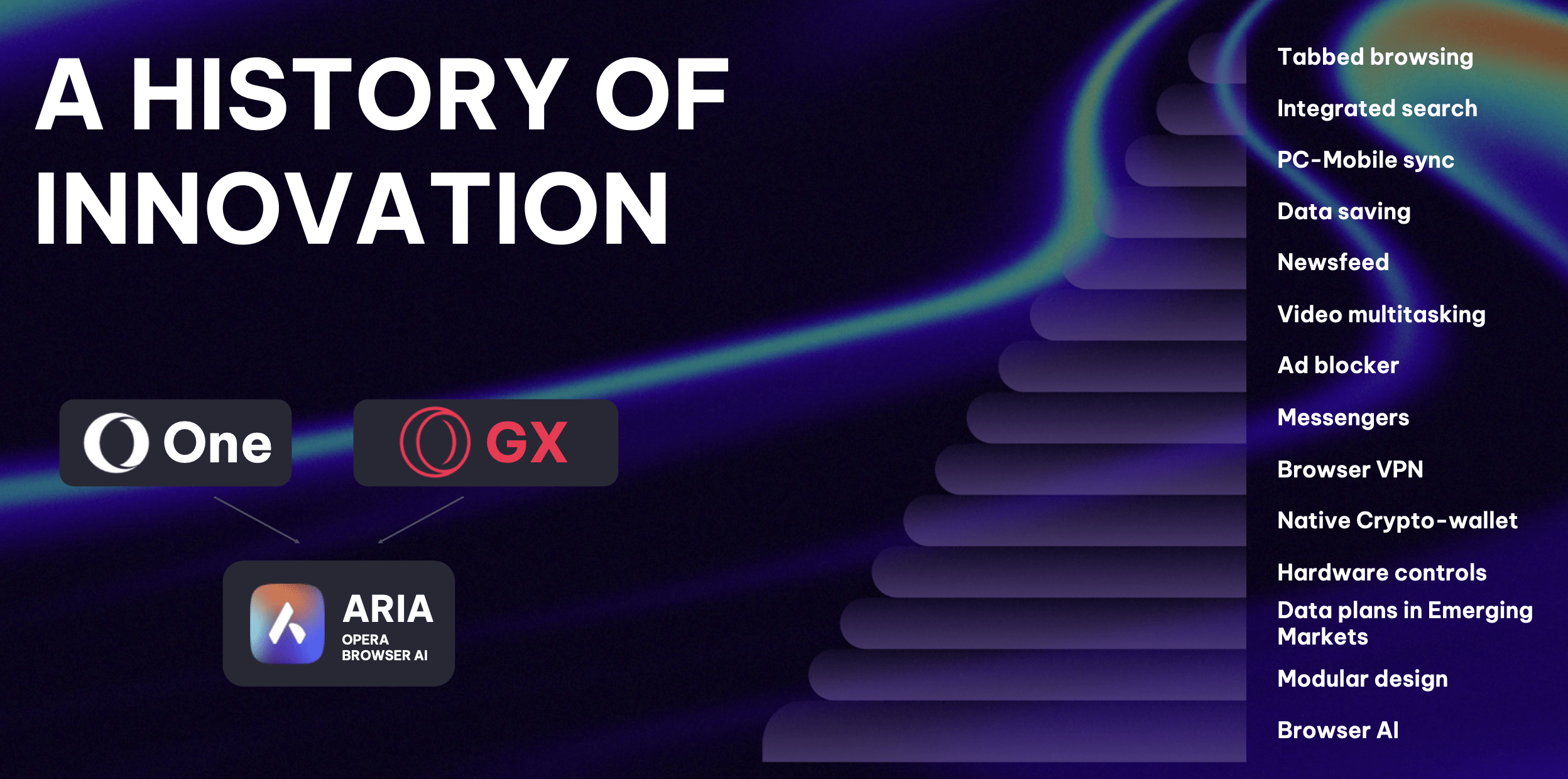

As well as, I seen that Opera has been fairly busy all year long, launching merchandise and options all 12 months. The corporate has launched a bunch of options, as will be seen within the slide beneath. Most of those options are both a part of their flagship browser product, the Opera One browser, supposed for a large viewers, or their GX browser, which finds relevance largely amongst players all around the world.

Opera’s browser merchandise and options (FY23 Investor Presentation, Opera)

Furthermore, Opera launched their own conversational AI chatbot, Aria, final summer time, which, together with different characteristic rollouts all year long, has, in my view, given the corporate’s browser product a lift in downloads, income, and margins.

Opera’s technique has made some floor in market share and person acquisition

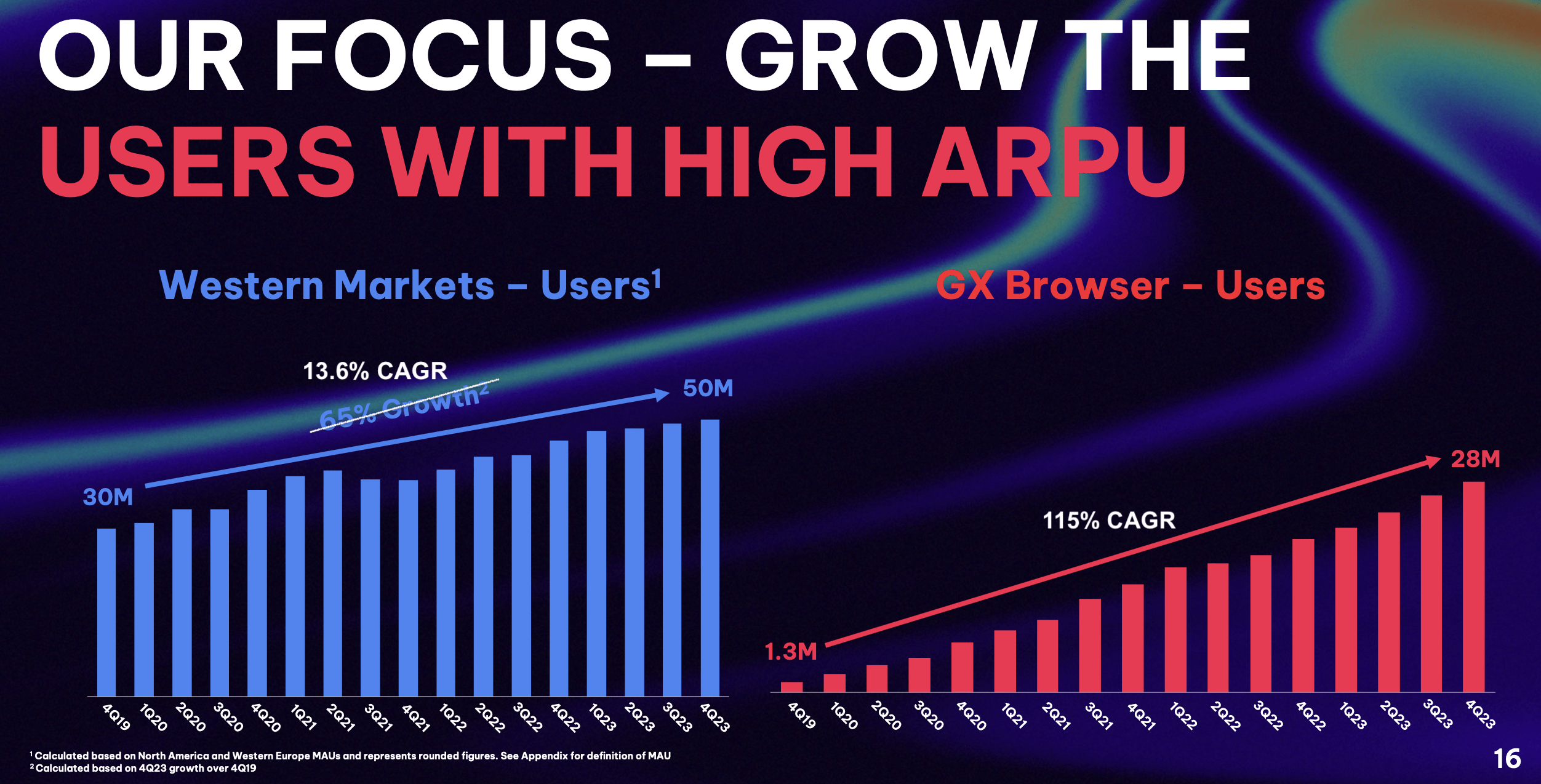

I imagine the checklist of product options that I listed earlier has been useful to Opera when it comes to its person base enlargement. The corporate’s browser all the time had a comparatively sturdy base among the many rising market inhabitants, in my view, because of the increased share of PCs in rising markets. However the firm has been working to extend its presence within the higher-margin developed markets that it calls ‘Western Markets’, which embody MAUs (Month-to-month Lively Customers) within the North American and European areas. I’ve added a slide beneath that illustrates Opera’s person development within the Western and Gaming markets with my very own annotations on CAGR development.

Opera’s person development over the previous 5 years’ price of quarters (FY23 Investor Presentation, Opera with writer’s annotations)

This can be a good signal of power for Opera in my opinion. Nonetheless, on the identical time, I be aware that Opera’s share in the browser market has receded from a excessive of three.3% seen in October to 2.5% market share, nearer to the two.34% market share quantity seen a 12 months in the past. If this development continues, it’s more likely to put some strain on Opera, because it seems the corporate’s browser product is barely dropping market share to bigger rivals akin to Apple’s Safari and Google’s Chrome.

Valuation multiples stay compressed on account of focus dangers

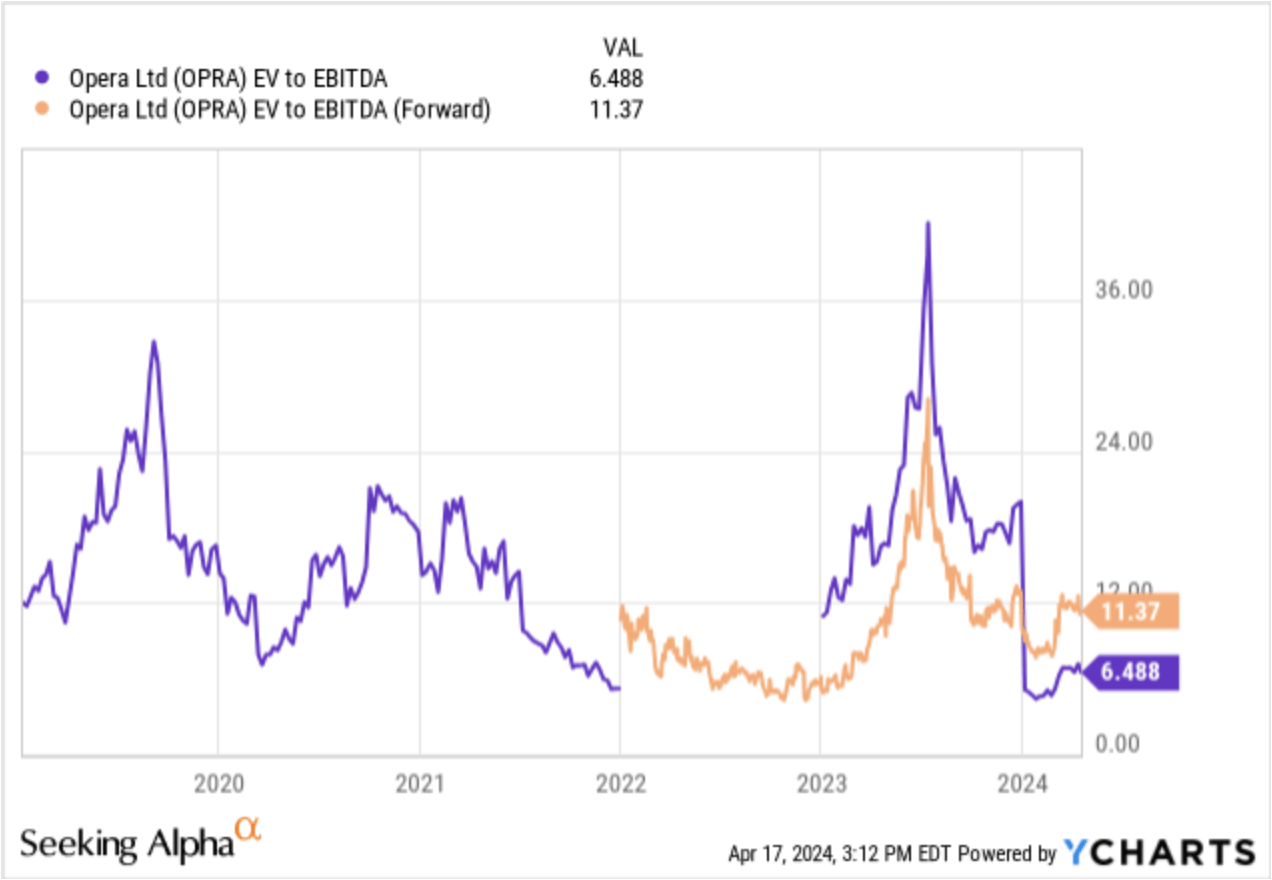

Earlier than I headed over to valuing the corporate, I wished to take a look at the dangers as a result of I seen that the corporate has a historical past of buying and selling at comparatively low valuation multiples. First, let me development the valuation multiples of Opera over time, as listed beneath.

Trailing vs Ahead EV/EBITDA for Opera (YCharts)

I imagine there are a few causes which may be inflicting valuation compression regardless of the earlier earnings beats.

In my view, a big a part of their income streams are on account of customers’ on-line search wants on Opera’s browsers. Presently, a revenue-sharing deal between Opera and Google ensures Google Search is the default search engine in Opera browsers. I’ve listed the traits beneath:

|

Income From Search |

2022 |

2021 |

2020 |

|

Income generated from person’s search exercise on Opera |

44.9% |

51.3% |

46.1% |

|

Google’s contribution to Opera’s whole income stream |

42.3% |

48.6% |

51% |

The corporate is actively working to cut back its dependence on search and Google by increasing its advertisements enterprise. Plus, their current AI chatbot, Aria, ought to assist with this in some unspecified time in the future shifting ahead. On the last earnings call, administration mentioned that within the rapid time period, Aria has delivered on its aim of making consciousness, however shifting ahead, they plan to monetize Aria by including monetizable hyperlinks and securing affiliate marketing online income if customers click on by on these hyperlinks. Primarily based by myself private checks, I imagine the corporate is properly positioned to monetize income from this channel inside Aria, however I anticipate these preliminary income streams from Aria to be fairly small as in comparison with whole income since it’s nonetheless in its early days for the product.

One other attainable concern is the construction of their present shareholders. An government on the board has a major controlling curiosity within the firm, holding virtually four-fifths of the corporate, which creates one other focus danger for the corporate. Such excessive concentrations from one Board member can create conflicts of curiosity throughout the firm, in my opinion.

Principal Shareholders in Opera (Type 20-F, Opera)

Opera’s Valuation and Outlook

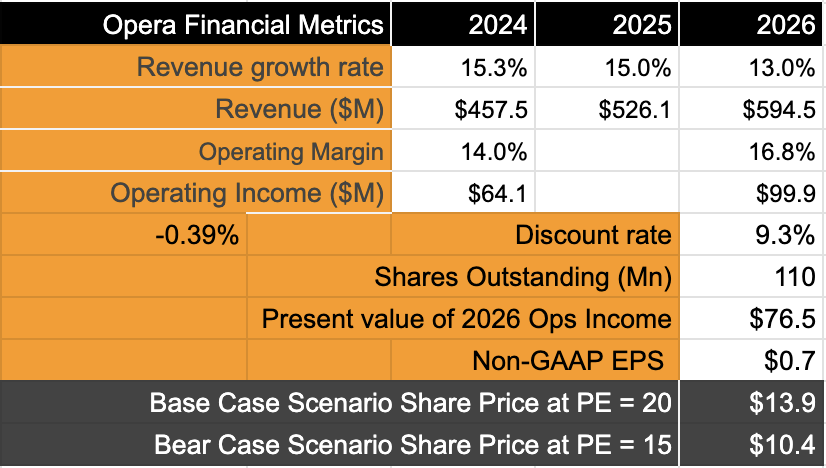

Primarily based on my observations listed earlier, I lay out my assumptions for valuing Opera beneath:

- As a result of lack of long-term working fashions, I’ll use consensus estimates. I imagine my assumptions additionally embody the recent search partner deal extension between Opera and Google.

- I anticipate working margins to be flat or barely declining this 12 months earlier than reversing increased and nearer to their FY23 margins of +16% on the again of continued features within the higher-margin markets.

- A reduction price barely higher than market expectations.

Opera’s valuation exhibits the inventory is priced in heading into earnings (Writer)

Primarily based on these estimates, Opera seems to be rising working earnings at ~16% CAGR whereas income grows ~14.4% CAGR between FY23 and FY26. These are sturdy development numbers, however I imagine it is going to be tough to justify a ahead PE for Opera that’s north of 20x, given the dangers and uncertainties I identified earlier, except the corporate has a major bump in its Q1 FY24 earnings and is ready to maintain the momentum by the 12 months.

For now, given my estimates, I see roughly a -4-5% draw back at present ranges for Opera in my base case assumption as seen above.

Different components to search for

Opera reviews subsequent week, and I can be looking ahead to a couple of issues listed beneath:

- Sustained momentum in its advertisements enterprise in addition to continued penetration into the Western markets

- Any change in outlook when it comes to monetization income from the AI chatbot product Aria?

- Any additional constructive commentary about its juicy dividends is at the moment projected at an annualized 5.3%. Within the final name, I imagine administration didn’t sign arduous commitments in dividend payouts, saying, “We would like to be in a position where we can increase it and certainly not decrease it.”

- Particular tailwind commentary on how they may profit from the EU’s DMA regulation.

- Presently, Opera initiatives full-year adjusted EBITDA to develop 15.2% y/y in FY24 to $108 million on the midpoint, a lot slower than the 38% development seen in FY23. That is anticipated to be achieved on the again of 15% y/y income development in FY24 gross sales, which ought to be ~$457.5 million at midpoint.

Takeaway

Opera has actually demonstrated a resolve to make the most of the AI tailwinds that they noticed by final 12 months. In 2023, they have been capable of take some market share from rivals, however these features have since seemed to be given again.

Sure dangers stay, and the corporate will want a powerful outperformance in Q1 FY24, whereas being anticipated to boost its outlook for the 12 months.

For the time being, I price this as a Maintain.