Joa_Souza/iStock Unreleased through Getty Photos

Funding Thesis

I like to recommend shopping for Itaú (NYSE:ITUB) shares. Over time, gamers who labored in Brazilian banking operations confronted main challenges, and Itaú is the principle participant on this market. Just lately, competitors with fintechs introduced challenges to the financial institution, which promptly initiated a serious operational and cultural change in its operations, aiming to face disruptive competitors.

Even with an incredible observe document of outcomes, the corporate trades at a P/E a number of of simply 7.5x, with its historic common being greater than 10x. Moreover, Itaú is predicted to report glorious ends in 2024, as occurred in 2023, and the corporate can distribute good dividends to shareholders.

Introduction

After many years of evolution and changes, the banking sector in Brazil has giant conglomerates within the highlight. It’s estimated that only 3% of the Brazilian grownup inhabitants doesn’t have a checking account.

A local characteristic is that the outcomes from providers (accounts, playing cards, investments), insurance coverage and pensions are fairly vital for banks. From a structural perspective, the sector goes by way of main modifications, some tendencies are larger competition within the provision of banking providers, notably fintechs, and the reduction in the variety of bodily businesses and employees.

The present interest rate reduction cycle stimulates the capital market, and technology brings a greater understanding of buyer wants when providing credit score and providers.

The Brazilian banking sector is dominated by Itaú, Banco do Brasil, Bradesco, Santander and Caixa Econômica Federal. Regardless of competing with one another, each concentrate on various kinds of demographics:

- Itaú has at all times been notable for serving the high-income demographics;

- Banco do Brasil has experience in serving Brazilian agribusiness and public servants;

- Bradesco focuses primarily within the center and low-income public;

- Santander focuses on entrepreneurs;

- Caixa Econômica Federal is well-known for providing real estate financing and different providers.

Now, let’s higher perceive Itaú’s historical past and enterprise mannequin, and the way this data corroborates my bullish thesis for the shares.

Historical past And Enterprise Mannequin

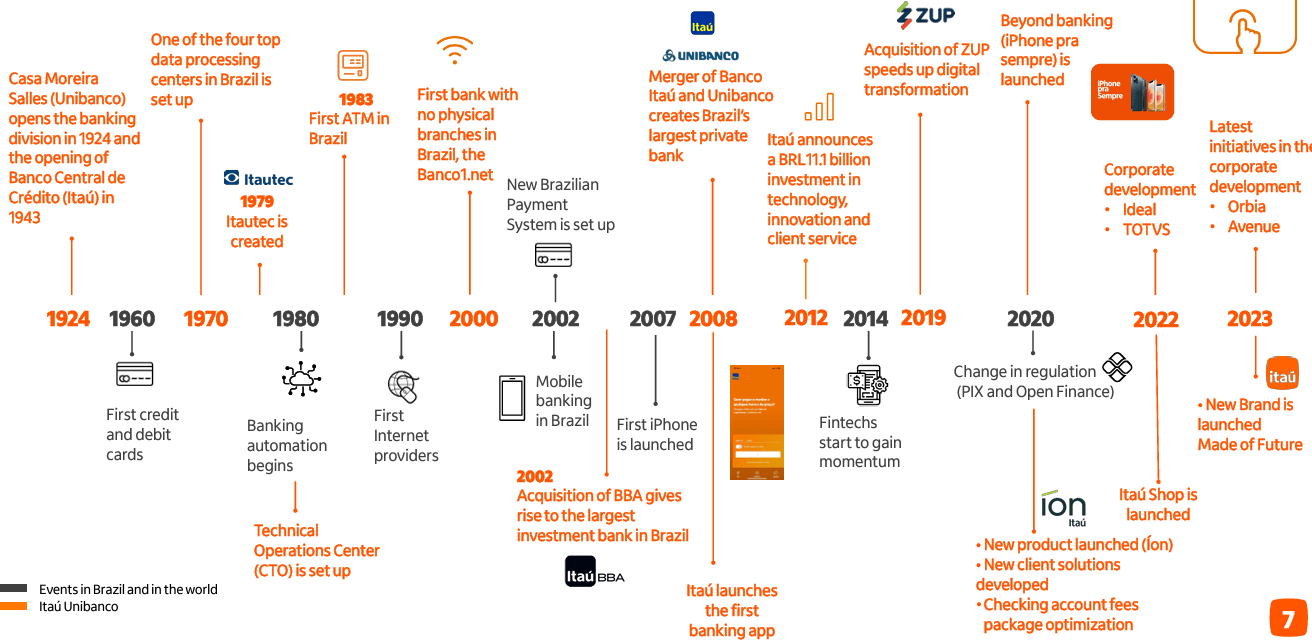

Itaú is the largest bank in Brazil and Latin America. The corporate has greater than 95 thousand staff and is current in additional than 18 nations. The financial institution turns 100 years previous in 2024 and beneath we’ve its historical past in a timeline:

Timeline (IR Firm)

In keeping with its institutional presentation, these are Itaú’s primary numbers:

- Credit score: Itaú Unibanco has round 16% of the entire credit score within the Brazilian financial system.

- Mortgages: Positioned 1st amongst non-public banks with a market share of twenty-two.6% in SBPE financing in November 2023.

- Playing cards: Market chief with a 27% market share in income in September 2023, with an entire portfolio of options

- Agribusiness: The corporate information an 89% improve in its portfolio within the final three years (from $9.2 billion to $17.4 billion). It’s believed that agribusiness GDP may attain $540 billion, equivalent to 25% of Brazil’s GDP in 2023. The financial institution additionally mentions that it has tripled the variety of prospects within the final two years.

- Automobiles: In third place in origination in December 2023 with a market share of 10.6% in December 2023.

- Consigned Loans: 11.9% market share within the credit score portfolio in September 2023, with 22% market share within the INSS (pension system) and 25.6% within the enterprise sector in September 2023.

- SMEs: 2nd place in Brazil, with an entire ecosystem of services and products.

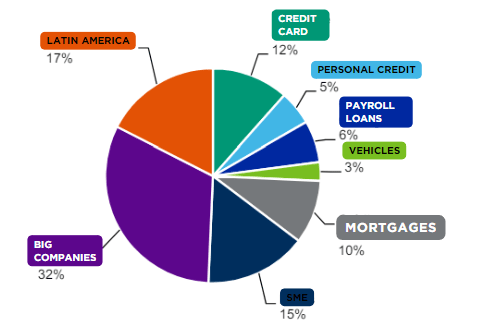

Traditionally, Itaú’s asset high quality has been supported by a diversified credit score portfolio, each by way of purchasers. By way of merchandise, Brazil represented 82.5% and operations in Latin America accounted for the remaining 17.5% in December 2023:

Itaú Credit score Portfolio (IR Firm)

You will need to do not forget that within the final 10 years, some digital banks similar to Nu and Inter have been searching for to disrupt the market, primarily serving the younger public.

With an announcement about simplifying banking actions, Nu is the Brazilian firm with the best potential to disrupt the market. The financial institution was based in 2013 and reached an unbelievable 90 million customers in 2023. As a reference, Itaú took virtually 100 years to succeed in 95 million prospects.

This accelerated progress can be seen in market worth, Nu has the 4th highest market cap amongst Brazilian corporations, and is simply two positions away from overtaking Itaú. Nonetheless, Itaú has been on the battlefield for 100 years and is modernizing. Subsequent, we are going to see the actions taken by Itaú to face the competitors, and the way they corroborate my bullish thesis for the shares.

Modernization

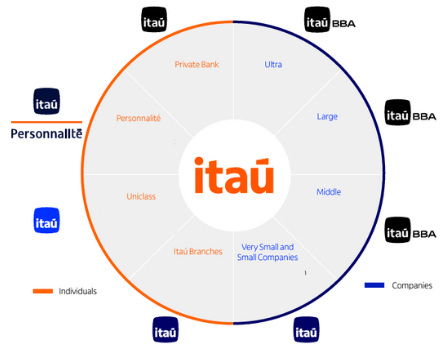

As I discussed within the introduction to this report, banks in Brazil earn cash from numerous actions, similar to playing cards, investments, insurance coverage, amongst others. Let’s take a look at Itaú itself, the corporate has a big ecosystem of services and products:

Itaú Ecosystem (IR Firm)

This diversified ecosystem was one of many greatest aggressive variations 10 years in the past, when competitors was restricted to the 5 largest banks in Brazil. Nonetheless, this was seen as a possibility by fintechs, as Brazilian banking merchandise had been complicated, filled with merchandise and obscure. Beneath, I’ll clarify some methods that Itaú is exploring to be extra aggressive in opposition to fintechs.

All In One App and Know-how

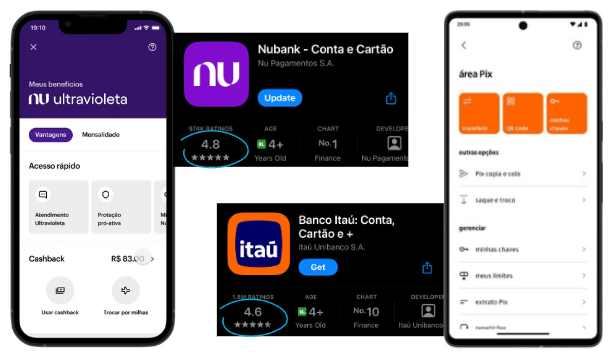

One of many methods utilized by fintechs was the creation of a single software that consolidated all of the merchandise provided, with a easy and sensible expertise for the consumer. These apps are known as “Super App” in Brazil, and beneath I’ll present a comparability of the analysis of customers who downloaded the Nu and Itaú app:

Analysis Of Nu And Itaú Apps (The Creator and iOS)

The numbers converse for themselves, Nu is probably the most searched app within the finance section in Brazil and has a ranking of 4.8 on the iOS system, whereas Itaú (regardless of being the biggest financial institution in Latin America) is simply in tenth place and has a ranking of 4.6.

When confronted with this, the financial institution started to take motion. With 95 thousand staff, the variety of financial institution staff has not modified considerably since 2019, when it was 100 thousand. Nonetheless, there was a considerable change within the composition of the workforce. The variety of expertise staff elevated from 5 thousand in 2019 to greater than 20 thousand in 2024:

Know-how Workforce (IR Firm)

Moreover, the president of Itaú, Milton Maluhy Filho, said that the financial institution ought to launch a new tremendous app within the first quarter of this yr. The venture is internally known as One Itaú.

The app is an evolution of iti, the financial institution’s digital platform for low-income individuals (a competitor to Nu), which can now serve the complete buyer base. In keeping with the president, there are virtually 15 million prospects who will be capable to take pleasure in a greater expertise.

Itaú’s profitable historical past of 100 years working within the Brazilian banking market, and its technique of renewing itself to face the competitors, corroborates my bullish thesis for the shares. Now, in order that we are able to have an excellent deeper view, we are going to perform a monetary evaluation of the corporate and its rivals.

Itaú Fundamentals

Within the following, I’ll use In search of Alpha information to match Itaú with its friends in Brazil, Banco do Brasil (OTCPK:BDORY), Nu Holdings (NYSE:NU), Bradesco (NYSE:BBD), and Banco Santander (NYSE:BSBR):

| Title | Itaú |

Banco do Brasil |

Nu | Bradesco |

Santander |

| Ticker | (ITUB) | (BDORY) | (NU) | (BBD) | (BSBR) |

| Market Cap | $54B | $30B | $51B | $26B | $19B |

| Internet Revenue TTM | $16B | $6B | $1B | $3B | $2B |

| Internet Revenue Margin | 26.6% | 27.6% | 27.8% | 20.8% | 24.2% |

| Internet Revenue CAGR 3Y | 20.5% | 33% | – | -3.4% | -11% |

| ROE | 18% | 19.7% | 18.2% | 8.9% | 8.4% |

| Dividend Yield | 1.54% | 8.84% | – | 3.13% | 6.36% |

When analyzing the outcomes, we are able to see that the web revenue margin, internet revenue CAGR within the final 3 years, and ROE of Banco do Brasil are increased than Itaú. Nonetheless, do not forget that Banco do Brasil is a state-owned firm, which had questionable administration by the Staff’ Social gathering till 2016, when the turnaround started.

The identical Workers’ Party received the presidential elections in 2022 in Brazil and is again in command of managing Banco do Brasil. Moreover, as I discussed, Banco do Brasil has nice publicity to agribusiness, and the sector goes by way of a crisis as a result of newest local weather occasions created by El Niño, this has the potential to worsen the corporate’s outcomes.

With the addendum executed, we’ve one other huge competitor, Nu. Nonetheless, Itaú has a a lot increased revenue, and an extended historical past of outcomes. Anyway, let’s examine the valuation of the corporate and its friends.

Valuation Is Enticing Given The Historical past

Within the banking sector, the Worth/Earnings (P/E) a number of is an efficient comparability metric, and stands out for its capacity to replicate relative profitability and progress expectations.

Nonetheless, Itaú is acknowledged because the financial institution with the very best administration high quality in Brazil, it has a premium in its valuation in comparison with its rivals. Moreover, Nu surpassed break even lately and nonetheless has a small revenue, leading to a particularly stretched P/E ratio.

Due to this fact, I’ll use Itaú’s personal historic Worth/Earnings to search out out if the corporate is affordable:

Valuation (In search of Alpha)

Based mostly on the historical past, we conclude that the corporate is affordable, since it’s worthwhile and its present a number of of seven.34x is discounted in comparison with the historical past of the final 5 years of 10.2x, which suggests a possible appreciation of 38%. I like to recommend shopping for Itaú shares with a goal value of $8.31. Now let’s have a look at what In search of Alpha’s Quant software signifies.

Itaú In keeping with the In search of Alpha Quant & Issue Grades

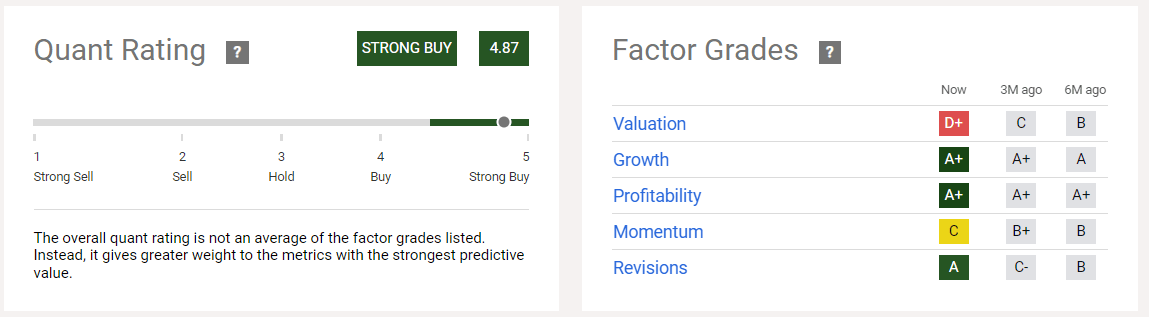

In keeping with In search of Alpha Quant, Itaú is a robust purchase, and this contributes to my bullish thesis on the inventory. Nonetheless, the valuation observe in Issue Grades caught my consideration:

Quant Rating & Issue Grades (In search of Alpha)

Itaú’s ranking of D+ in valuation did not make a lot sense to me, so I opened the valuation in all metrics, and the one ones that had unhealthy grades had been P/B and dividend yield.

Valuation Metrics (In search of Alpha)

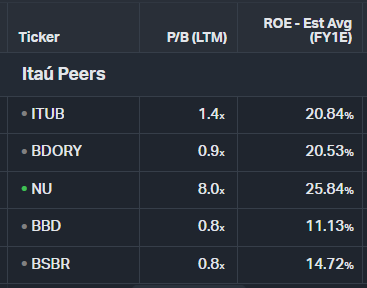

Properly, once we analyze the P/B, it’s acceptable to additionally take a look at the ROE:

P/B and ROE (Koyfin)

Once we analyze the 2 indicators, we see that there’s a justification for Itaú to have a better P/B than its friends, the corporate has a better ROE than Banco do Brasil, Bradesco and Santander.

One other quantity that caught my consideration was the dividend yield, however I’ve cause to consider that this might be the icing on the cake for Itaú’s thesis, however earlier than speaking concerning the dividends, I want to speak about Itaú’s newest outcomes.

Newest Outcomes And The Icing On The Cake

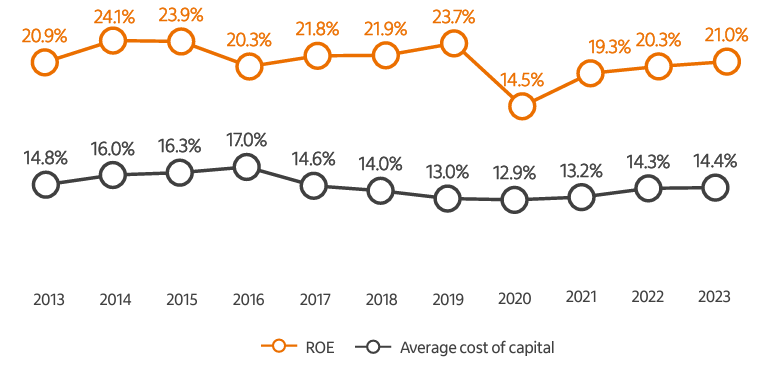

Itaú reported strong ends in 4Q23, with a recurring internet revenue of $1.9 billion (ROE of 21.2%), a rise of 4% Q/Q and 23% YoY.

ROE And Common Value Of Capital (IR Firm)

The general numbers adopted a optimistic pattern, and the steerage was partially met, apart from the expansion of the credit score portfolio, with simply 3.1% YoY, subsequently beneath the low-end of the steerage (5.7%-8.7%). Moreover, the financial institution launched its promising steerage for 2024:

- Credit score portfolio: enlargement of 6.5% to 9.5% y/y;

- Monetary margin with prospects: improve from 4.5% to 7.5% y/y;

- Monetary margin with the market: from $0.6 billion to $1 billion;

- Credit score price: from $6.7 billion to $7.3 billion;

- Income from providers and insurance coverage outcomes: progress of 5.0% to eight.0% y/y;

- Non-interest bills: enlargement from 4.0% to 7.0% y/y;

- IR/CS fee: 29.5% to 31.5%.

For my part, Itaú managed its portfolio very effectively amid a difficult situation, with out harming progress or the power to generate earnings. The corporate additionally introduced an extraordinary dividend of $2.2 billion, bringing the yr’s payout to roughly 60%. The financial institution additionally launched a $500 million buyback program.

Moreover, I consider that this payout stage needs to be maintained in 2024, given the corporate’s excessive capital ratio. The prospects are fairly optimistic, however it’s essential to know the dangers of the funding.

Dangers To The Thesis

The weak progress of the credit score portfolio within the annual comparability, nonetheless reflecting the selectivity seen over the previous few quarters, may proceed all through 2024. If there isn’t a strong inflection within the default fee, it’s probably that the financial institution won’t have faith to develop extra vigorously once more. Due to this fact, it won’t have the amount to compensate for the weakening margin, which needs to be seen within the coming quarters given the rate of interest discount cycle.

Competitors is one other related threat. As talked about, Itaú has a extra resilient high-income consumer profile, whereas Nu focuses on younger and medium/low-income purchasers. If Nu or one other Brazilian fintech manages to discover a disruptive enterprise mannequin to serve high-income prospects, Itaú should be much more efficient in its modernization plan.

A closing level of consideration issues prices. The steerage signifies that non-interest bills will rise between 4% and seven% in 2024, greater than the inflation forecast for the yr. In 2023, this line grew 6.5% and reached $11.5 billion. The financial institution says that core bills will develop beneath inflation. The largest prices would come from investments, for instance, in expertise and hiring monetary advisors. Given the dimensions of the financial institution, the dangers are numerous, and the investor should pay attention to them earlier than investing.

The Backside Line

Itaú’s valuation based mostly on the P/E a number of signifies a related low cost in comparison with its historical past, even with the corporate reaching glorious outcomes in comparison with its rivals, similar to sturdy profitability.

The rise of competitors made the financial institution modernize, not like rivals similar to Bradesco and Santander, which have an ROE of lower than 10% and a tradition that’s nonetheless previous. Lastly, Itaú ought to pay good dividends to shareholders on the finish of 2024, provided that its payout can go from 30% to 60%.

Based mostly on this evaluation, I like to recommend shopping for Itaú shares. Traders ought to take note of its lengthy historical past of excellent outcomes, worthwhile operations, and skill to reinvent itself. This funding thesis presents an incredible risk-return ratio for me.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.