Thomas Barwick

Funding motion

Based mostly on my present outlook and evaluation of Darden Eating places (NYSE:DRI), I like to recommend a maintain score. My assessment of DRI suggests a poor FY25 SSS efficiency forward, given the inflationary atmosphere that impacts client visitors and its value base. Relative to Texas Roadhouse (TXRH), DRI efficiency can be comparatively poorer, which is a trigger for concern. Till DRI exhibits extra constructive SSS efficiency, I’m going to remain on the sidelines.

Primary Info

DRI owns and operates full-service eating places beneath a number of manufacturers, and the first manufacturers are Olive Backyard [OG] and LongHorn Steakhouse [LHS], which collectively characterize ~70% of 3Q24 income. DRI additionally has a Tremendous Eating section with two manufacturers: The Capital Grille and Eddie V’s, which account for 13% of 3Q24 income. The remaining income contributions are from different manufacturers.

DRI

Evaluate

DRI share value has continued to fall since its final earnings leads to late March, and I consider the share value goes to stay weak within the close to time period till outcomes present a extra stable turnaround momentum. My view is supported by two elements of the enterprise: (1) a poor gross sales outlook; and (2) margin compression.

Beginning with the gross sales outlook, same store sales have turned -1% in 3Q24 vs. constructive SSS over the previous 6 quarters, with the biggest model, OG, down by 1.7%. Tremendous Eating and Different had been each detrimental for the second consecutive quarter. It seems that macro stress has lastly sunk its tooth into DRI’s efficiency, the place weak spending from low-income shoppers has dragged down total efficiency. The revised FY24 same-store-sales [SSS] information of 1.5%–2% from 2.5%–3% prior additionally implies that the weak efficiency momentum has sipped into 4Q24 (because the implied 4Q24 SSS efficiency is -0.5% to 1%). The timing of administration’s steering is probably the best trace that 4Q24 is unlikely to see an enchancment as a result of the earnings name was held on March 21, which gave administration about 1 month of 4Q24 information already.

The worrisome half is that the weak gross sales efficiency appeared to stem from poor visitors as a substitute of pricing. We will estimate how a lot quantity has declined by deducting the reported pricing progress from the entire SSS. On this case, utilizing administration’s remark that pricing grew ~3.5%, it implies that 3Q24 visitors is down 4.5% (-1% SSS – 3.5% pricing progress). That is consistent with administration’s remark that they’ve taken share from the trade, which noticed a -6.5% visitors decline (administration famous OG visitors was down 3.8%, they usually beat the trade benchmark by 270 bps). It’s true that that is thought of a market share acquire, however I don’t assume this requires celebration as a result of, in comparison with TXRH, which noticed 9.9% 4Q23 (finish in Dec) SSS progress (5.1% from visitors), DRI 2Q24 (ends in Nov) and 3Q24 (ends in Feb) efficiency screens very negatively (regardless of pricing beneath inflation charges). My guess is that DRI has executed very poorly on its worth technique (low-income client transactions are famous to be a lot decrease vs. 3Q23), however this isn’t verifiable at this level, which goes to trigger an overhang on the inventory. Furthermore, with inflation staying stickier than anticipated, that is going to proceed placing stress on the lower-income client group, a headwind for DRI.

DRI may pull the lever of opening extra shops to drive prime line progress, however that choice appeared to have confronted its limits, as administration principally guided down on the variety of shops opening in FY25 (45–50 vs. FY24’s 50–55), highlighting persisting development and capex value inflation headwinds. Construct-out capability has additionally confronted constraints, as seen from begins and completions taking longer attributable to developer delays and financing points, utilities, allowing, and occupancy certificates, amongst others. Of all the explanations, financing points on the developer finish are a giant wild card that might deteriorate if the Fed doesn’t reduce charges (which is more and more probably given the inflation and scorching US financial system information).

Shareholders of DRI would take consolation in studying that DRI retailer margins truly improved sequentially and yearly to twenty.6% regardless of the gentle SSS efficiency. Nevertheless, I anticipate margins to compress within the coming quarters given the administration’s plan to underprice inflation (consistent with their worth technique) by 100–150 bps in 4Q24. This comes at a time when DRI’s prices are nonetheless beneath inflationary stress. As an example, beef continues to be in undersupply, which pushes the worth up, and labor prices are nonetheless rising at mid-single digits. One other key motive for DRI margin enlargement is that the corporate has pulled again on advertising and marketing bills, with 3Q24 spending simply 1.1% of income, which is effectively beneath the pre-Covid price of ~3% vs. gross sales. This may very well be one of many causes for the poorer efficiency vs. TXRH, and if that’s the case, DRI would wish to ramp up this spend to catch up, which goes to stress margins.

Valuation

Writer’s work

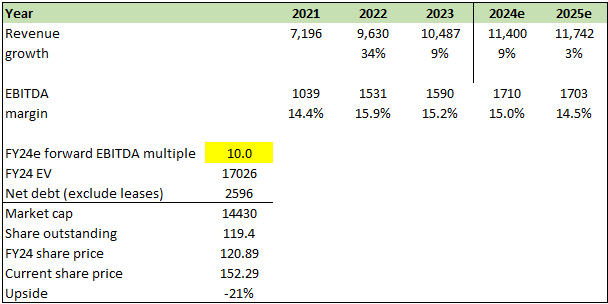

I consider DRI will see progress decline in FY25 (be aware FY24 ought to meet steering as we’re already 3 quarters in and administration has 1 month of 4Q24 information) given the inflationary atmosphere that ought to proceed to influence lower-income shoppers and slower retailer construct means given the trade constraints. I assumed 3% progress in FY25, pushed by ~3% progress (4% food away from home inflation – 100 bps underprice technique) and a pair of% retailer progress (guided for 45 to 50 in FY25), offset by 2% in visitors decline (giving the good thing about doubt that an ongoing worth technique would see some type of restoration). Decrease top-line progress, mixed with inflationary value stress and the necessity for extra advertising and marketing spending, ought to trigger margins to compress. With the poor outlook, I assumed DRI would commerce at 10x ahead EBITDA, barely beneath its historic common a number of.

Threat

Additional draw back threat is that if DRI’s poor relative efficiency widens towards TXRH, which may actually counsel poor execution on the pricing technique entrance. In that case, SSS may are available decrease than anticipated, placing extra stress on margins. This isn’t going to take a seat effectively with traders, as they may simply put money into TXRH for related publicity to the restaurant trade, placing extra stress on the inventory. Upside threat is that the DRI pricing technique permits it to realize extra visitors share, way more than the trade visitors decline, leading to web constructive visitors progress which might push SSS again to constructive progress. Additionally, if meals away from dwelling inflation comes down sooner within the coming months, it will additionally present a raise to trade and DRI visitors, boosting SSS progress.

Ultimate ideas

My advice is a impartial score for DRI, because it faces a difficult close to future attributable to a mixture of things. Inflationary pressures are hurting client spending, resulting in declining visitors and probably detrimental SSS efficiency. Margins are additionally prone to compress as DRI struggles to maintain tempo with rising prices whereas sustaining its worth technique. Whereas DRI noticed improved retailer margins within the final quarter, this may not maintain attributable to underpricing inflation and potential will increase in advertising and marketing spend. Contemplating these components and the potential for additional draw back threat, a maintain score is advisable for DRI till a clearer image of SSS turnaround emerges.