Ariel Skelley/DigitalVision through Getty Photos

Since I last wrote about the home builder United Properties Group (NASDAQ:UHG) in December, its value is down by 12.3%. Even on the time, the dangers to the corporate had been clear, prompting a Maintain score on the inventory. Not the least of those dangers was the state of the housing market, with high-interest charges pricing out potential patrons.

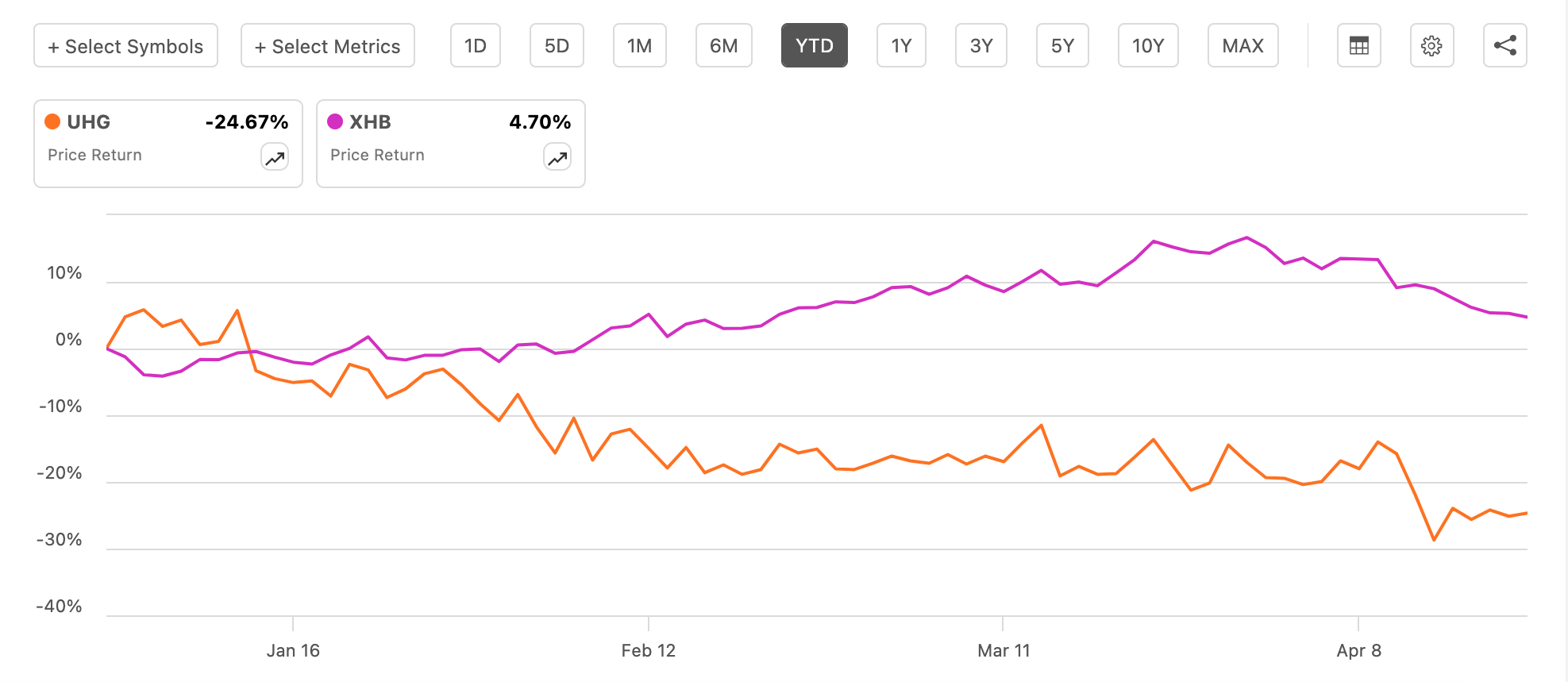

Nevertheless, even at the moment, the broader housing market was seeing an uptick. That is evident from the efficiency of the SPDR S&P Homebuilders ETF (XHB). The development continues, growing the hole between the efficiency of UHG and the sector (see chart under).

This implies that there’s extra occurring right here than simply the market circumstances. Right here, I take a better have a look at why UHG is underperforming and whether or not there’s any chance of a turnaround within the foreseeable future.

United Properties Group and SPDR S&P Homebuilders ETF, Value Returns, YTD (Supply: In search of Alpha)

Improved housing market circumstances

One huge cause for the inventory’s underperformance once I final checked was its weak fundamentals. The corporate’s revenues had dropped by 15.8% year-on-year (YoY) within the first 9 months of the 12 months (9m 2023) and the working margin had seen a pointy decline on larger working bills too.

However issues are altering, not less than on the income entrance. Restoration within the housing market is starting to indicate up for UHG, which noticed a small 1.5% year-on-year (YoY) enhance in revenues within the last quarter (This fall 2023) in distinction to an 11.6% decline for the complete 12 months 2023.

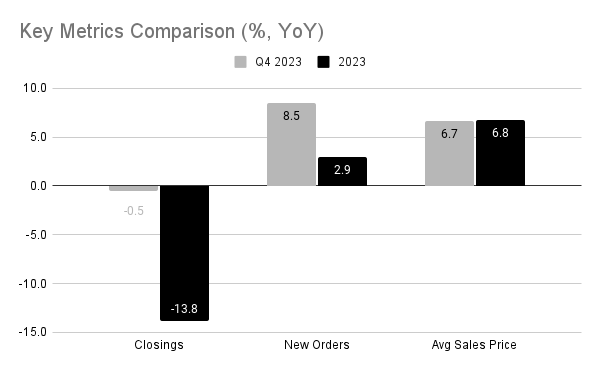

Whereas the change in common promoting value is nearly the identical in each This fall 2023 and the complete 12 months 2023, the ultimate quarter’s income turned out higher as residence closings stayed basically flat, an enchancment from the complete 12 months and new residence orders’ progress accelerated (see chart under).

Key Housing Metrics (Supply: United Properties Group, Writer’s Estimates)

Earnings weaken in This fall 2023

The gross revenue margin at 18.5% for This fall 2023 was barely decrease than the 19% for 2023 as the price of gross sales inched up a bit in comparison with a contraction for the complete 12 months. However the change is not large enough to be any supply of concern.

The working margin dropped too, to 2.7% in This fall 2023, in comparison with 3.5% for the complete 12 months 2023. This was partly as a consequence of a USD 1.8 million enhance in working bills on account of share-based compensation and transaction bills. Nevertheless, even excluding these distinctive bills, the whole working bills had been up by 54% in comparison with 31% for the complete 12 months.

A change within the truthful worth of by-product liabilities resulted in a web loss in This fall 2023, whilst the online revenue for 2023 rose by 80% on a corresponding huge enhance within the truthful worth of liabilities. Notably, in consequence, the online margin for 2023 rose to 29.5% in comparison with the already wholesome 14.6% in 2022.

2024 begins effectively, optimistic housing market outlook

2024 has began effectively for UHG. The corporate continues its inorganic growth with the buyout of Creekside Customized Properties for USD 16.9 million after it made two acquisitions final 12 months. This newest acquisition expands its footprint in South Carolina after it bought Rosewood Communities final 12 months, which is in the identical market.

By way of natural progress, too, the corporate has additionally had a very good begin to 2024, with one other 7.4% YoY rise in new orders in January-February. With the housing market additionally trying higher, this may increasingly effectively proceed. According to Freddie Mac “upward home price pressure” will be anticipated this 12 months, although it expects only a 0.5% enhance in costs in 2024 and 2025. However, that is an enchancment after a 13% YoY drop within the common home value on the finish of 2023.

Furthermore, with a 5.9% YoY enhance in new residence gross sales in February 2024, the related class for UHG, in comparison with the three.3% decline in current residence gross sales, likelihood is that the common promoting value for the corporate can proceed to see an uptick if the development continues, as was already seen final 12 months.

Elevated market multiples

The sharp bump up in web revenue has lowered the trailing twelve-month [TTM] price-to-earnings (P/E) ratio to only 2.5x, which could be very low by any normal. However because the revenue rise is simply as a consequence of accounting variations, I calculated the online revenue excluding the change in truthful worth of by-product liabilities too. This ends in a far larger P/E of 33.5x.

This adjusted P/E is way in extra of that for friends of an identical market capitalisation like Beazer Properties (BZH), with a presence throughout US states and manufactured, tiny and cell houses supplier Legacy Housing Company (LEGH) at 5.2x and 9.2x respectively.

To maintain the evaluation constant from final time, I additionally in contrast UHG’s EV/EBIT. First, at 27.6x, it’s miles larger than the 12.9x degree it was on the final I checked. Second, it’s additionally far larger than that for friends. Whereas BZH trades at 9.9x, LEGH is at 7.9x. Even when the bills for share-based compensation and transaction bills are added again into working revenue, the adjusted EV/EBIT at 24.6x remains to be far larger in comparison with friends.

The important thing level right here is that regardless of how we have a look at the market multiples, they simply do not look aggressive except after all the reported earnings determine is taken into account for 2023. That is though UHG’s value has deteriorated within the meantime.

What subsequent?

Going by the corporate’s bettering income efficiency and the improved outlook for the US housing market, the inventory does look extra promising. It’d even be a good suggestion to have it on the investing watchlist.

However its value remains to be too excessive in comparison with adjusted revenue figures, even after it has seen a value drop prior to now months, which is in any case at odds with housing shares. If the corporate’s first-quarter numbers, due subsequent month, present a pickup in earnings or if the worth corrects appreciably, there could be a stronger Purchase case for UHG. However proper now, it stays a Maintain.

Editor’s Observe: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.