RapidEye

Motorcar Components of America, Inc. (NASDAQ:MPAA) primarily manufactures and remanufactures aftermarket automotive components, and sells diagnostic gear for alternators and starters with purposes in ICE and electrical autos. Within the aftermarket automobile components section, Motorcar Components of America’s (“MPA”) largest product varieties are rotating electrical components, which embrace alternators and starters, brake associated merchandise, and wheel hubs. MPA has upwards of 40% market share within the alternators and starters aftermarket and upwards of 20% within the wheel hub aftermarket. The corporate sells these components to auto retailers equivalent to O’Reilly Automotive, Inc. (ORLY), AutoZone, Inc. (AZO) and Advance Auto Components, Inc. (AAP) and has fairly excessive buyer focus as a result of construction in that market. MPA’s prime three clients account for over 80% of gross sales.

MPA has benefitted from long-term demand tailwinds resulting from a rise within the common quantity of miles pushed per automobile and a rise within the common age of autos. These traits are being pushed by excessive prices for brand new and used autos and excessive prices of financing these purchases. So long as these traits proceed, MPA will proceed to learn from demand tailwinds, which can assist gas extra development sooner or later.

Nonetheless, regardless of the expansion and tailwinds, earnings haven’t grown resulting from declining margins. This has been attributable to concessions supplied to its clients, as market construction within the auto retailer business provides the retailers negotiating energy when coping with components producers.

That is additionally attributable to the corporate’s inverse relationship between earnings and rates of interest. MPA makes use of an accounts receivable low cost program whereby it sells receivables to banks with a purpose to get funds sooner. Whereas this reduces working capital wants, it raises curiosity bills resulting from the price of borrowing from these banks. These charges are variable, which implies that bills enhance enormously throughout instances of rising charges. The corporate notes in its 10-K that “for each $500,000,000 of accounts receivable we discount over a period of 180 days, a 1% increase in interest rates would have increased our interest expense by $2,500,000.” For a enterprise that has seen declining margins and value inflation, this relationship with rates of interest has been particularly detrimental.

Whereas this receivable program is constructed into the enterprise mannequin, it isn’t straight associated to the enterprise of producing/remanufacturing and promoting aftermarket automobile components. I consider this has created the chance with the inventory as we speak, as rising charges, thus declining EPS expectations, has pushed traders to promote MPAA regardless of favorable long-term tailwinds and enterprise fundamentals. MPA’s EV is at the moment 4.5x my estimate of FY2025 EBITDA, which is sort of low given its significance in its business and given comparable multiples, particularly from a non-public fairness deal in 2022 involving an business peer, BBB Industries.

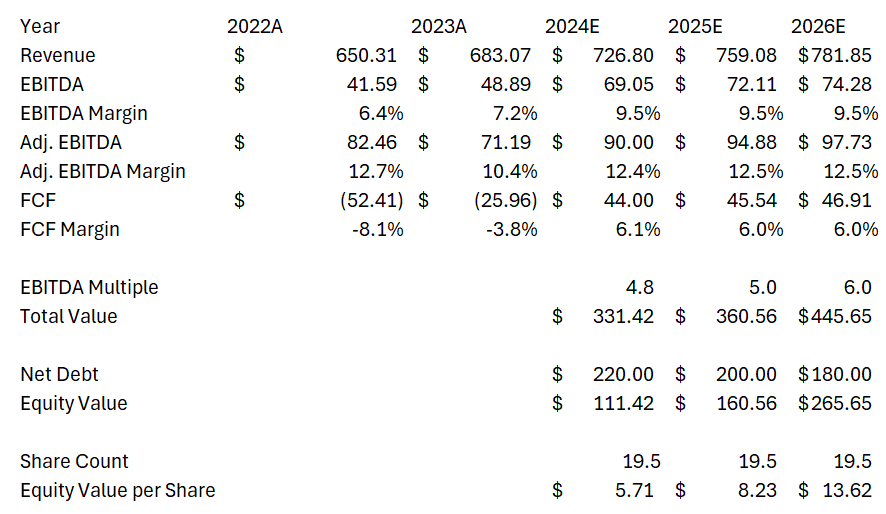

Assuming EBITDA of about $72mm in FY2025, $200mm in internet debt, and a 5x a number of, I see a reputable path for MPAA to commerce at round $8.25 as quarterly outcomes proceed to indicate stable enterprise and business fundamentals as a result of beforehand talked about demand tailwinds.

Current Quarterly Outcomes and Business Backdrop

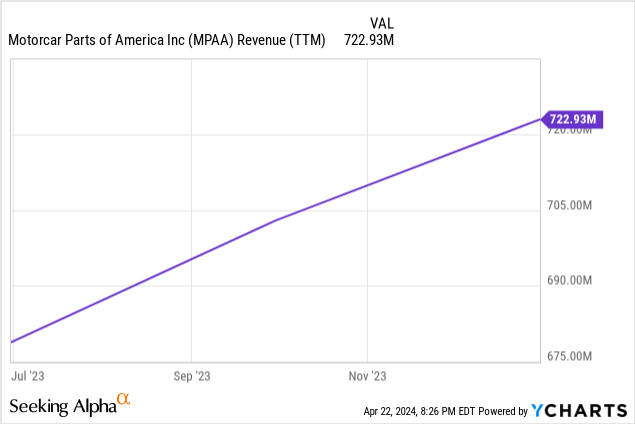

MPA’s monetary outcomes over the previous 9 months have been stable as the corporate has continued to develop organically and achieve market share. Margins have improved when in comparison with FY2023 resulting from larger promoting costs, decrease freight prices, and enhancements within the provide chain. For FY2024 ending March 31, income is anticipated to be round $726mm, representing development of about 6% when in comparison with the prior 12 months, and adjusted EBITDA is projected to be about $90mm, representing development of about 25% when in comparison with the prior 12 months.

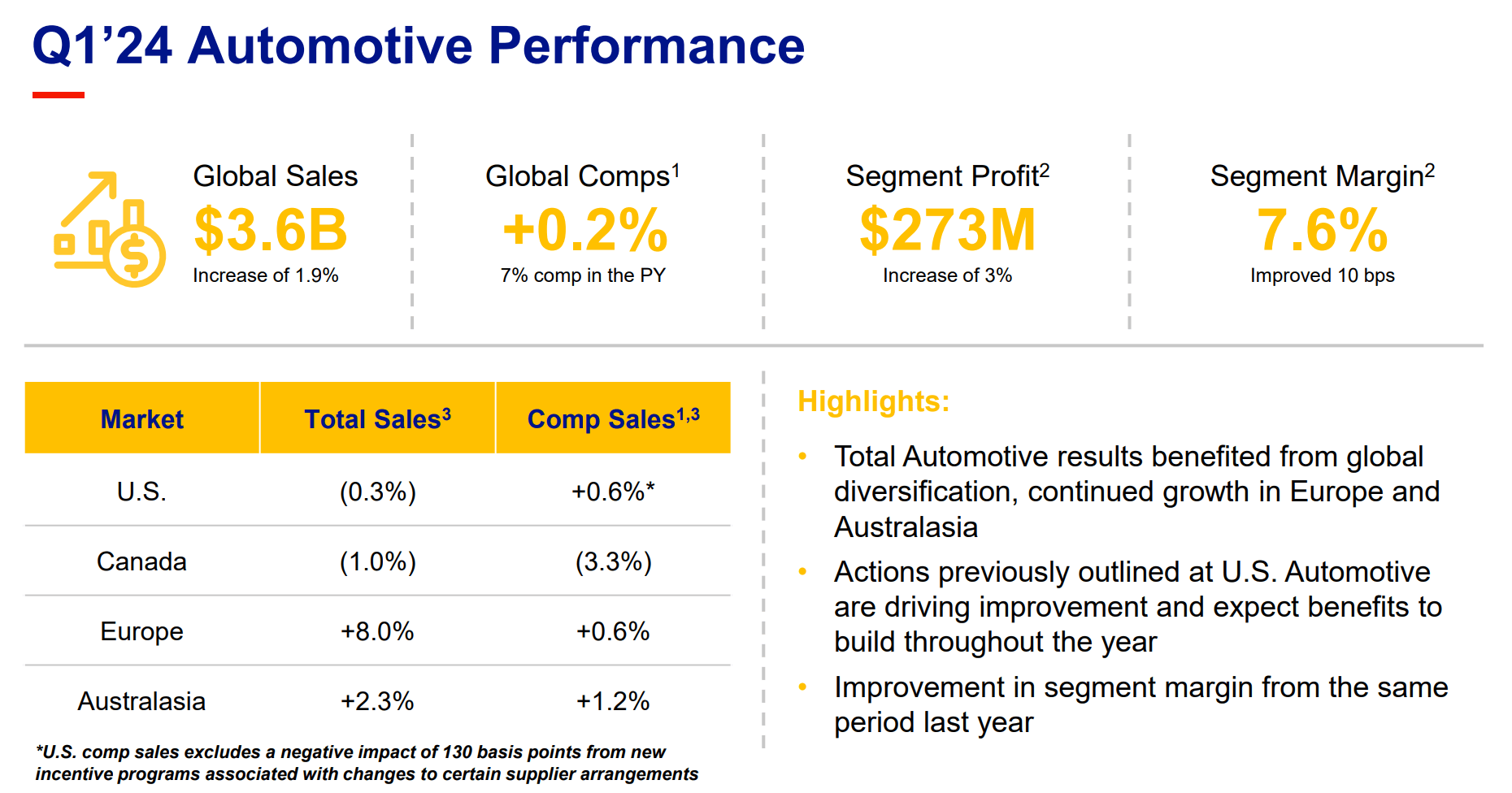

Importantly business fundamentals stay constructive regardless of MPA noting sudden demand weak spot in November and December 2023. Whereas different auto half retailers are anticipated to report quickly, Real Components Firm (GPC) lately reported constructive earnings outcomes. GPC operates two segments, certainly one of which is its Automotive Components Group. This section is an auto components distributor that buys merchandise from corporations like MPA and sells them to do-it-for-me (“DIFM”) auto retailers and do-it-yourself (“DIY”) auto half retailers. Gross sales to DIFM clients makes up about 80% of GPC automotive income, whereas DIY clients make up the opposite 20%.

In its earnings name, GPC referred to as out continued demand tailwinds equivalent to an ageing automotive fleet, a rise in miles pushed, and elevated new and used automobile costs. Moreover, GPC referred to as out an enchancment in US automotive gross sales versus the prior quarter, the identical quarter by which MPA talked about softer demand in November and December. The total quote from GPC’s convention name is as follows:

Within the U.S., Automotive gross sales have been basically flat through the first quarter with comparable gross sales growing roughly 1%. This represents a notable enchancment from the fourth quarter in each reported and comparable gross sales. The primary quarter efficiency was consistent with our expectations. As we moved via the quarter, we noticed a sequential enchancment in common day by day gross sales development every month.

In the course of the quarter, we additionally noticed constructive shopping for behaviors from our unbiased homeowners, a development that we count on to proceed over the course of the 12 months. From a buyer section perspective, gross sales to business clients within the quarter have been barely down, whereas gross sales to Do It Your self clients have been roughly flat. For business, Auto Care continued to outperform whereas main accounts underperformed, pushed by a cautious finish client.

GPC Automotive Q1 2024 Monetary Outcomes Abstract (GPC Q1 2024 Earnings Presentation)

Whereas MPA sells primarily to auto retailers and never DIFM auto retailers, this commentary bodes properly for the business. MPA’s inventory did soar about 8% on the information of those outcomes, however I consider the inventory stays low-cost regardless of this transfer.

Valuation and Value Goal

MPAA’s low EV/EBITDA ratio is as a result of firm’s sensitivity to rates of interest. Rates of interest are elevated and appear to be they might keep elevated, that means MPA’s earnings will stay depressed. Nonetheless, I believe this issue, which is unrelated to enterprise fundamentals, is creating a chance for traders which might be keen to have a look past the following 12 months. MPA has excessive market share and is a excessive worth vendor to its clients. This truth, together with longer-term demand tailwinds, lead me to consider that the enterprise will have the ability to get via this tough interval. If the corporate manages this, the inventory’s upside could be very enticing.

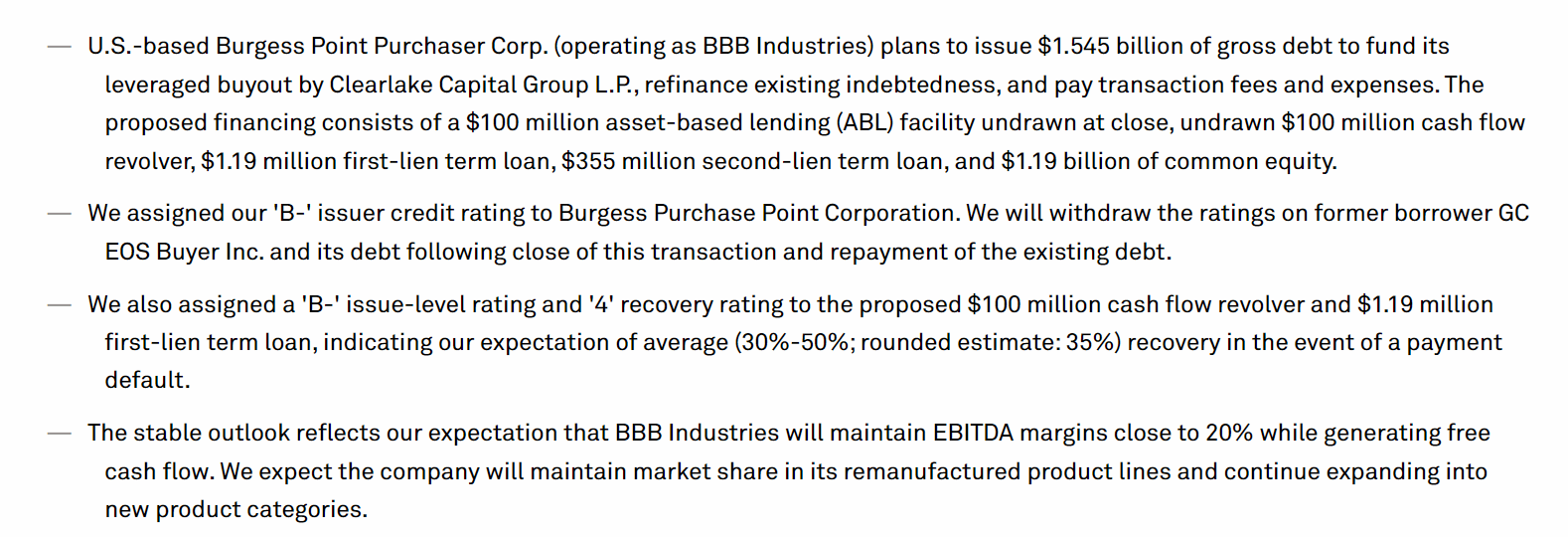

For context, BBB Industries, one other aftermarket automotive half producer/remanufacturer, was lately exchanged in a non-public fairness deal in 2022. I used to be unable to search out a lot knowledge on BBB Industries financials or the information concerning the 2022 personal fairness transaction, however particulars from a Bloomberg article and particulars from S&P Global concerning a debt issuance following the personal fairness transaction, lead me to consider BBB was bought for a 10x EBITDA a number of.

Abstract of S&P World Debt Score for BBB Industries Debt Issuance (S&P World)

The Bloomberg article cites an nameless supply that claims BBB Industries was valued at $2.7bb within the deal. Together with this, the S&P World debt score overview wrote that BBB Industries took on $1.545bb of gross debt to fund the deal which took its leverage ratio up from 6.6x to eight.6x. S&P additional states within the report that, “combined with sourcing opportunities, labor productivity, and material savings, the company should generate fiscal 2022 adjusted EBITDA margins of 19%-20%, leading to our fiscal 2022 forecast for adjusted leverage of 8x-8.5x.” Be aware that S&P World appears to be together with an issuance of $1.19bb in frequent fairness within the $1.545bb gross debt determine.

This information offers us with two equations (complete debt/EBITDA earlier than and after the deal) and two unknowns (debt and EBITDA). Fixing for the 2 unknowns results in EBITDA of $772.5mm and complete debt of $5.098bb previous to the transaction. This quantity of debt plus the $2.7bb fairness worth cited within the Bloomberg article results in an EV of $7.798bb which is nearly 10x the $772.5mm EBITDA determine I calculated above. Once more, I used to be unable to search out a lot knowledge on BBB Industries financials to verify this with, so I’m taking these estimates with a grain of salt.

I don’t count on MPAA must be valued with an EV/EBITDA ratio of 10 given BBB Industries’ bigger scale and better margins (20% adjusted EBITDA margins in line with S&P World in comparison with about 13% for MPAA), nonetheless this comparable offers some indicator that MPAA trades at a low valuation and has excessive upside if the curiosity expense difficulty goes away with decrease rates of interest, or if administration is ready to scale back debt via its initiatives to neutralize working capital.

Beneath is an illustrative mannequin which exhibits a bullish consequence if development continues and MPA is ready to generate money to cut back debt over the following few years. With a 5x EBITDA a number of on FY2025 EBITDA, and $200mm of internet debt, I see a reputable case for the inventory to commerce at round $8.25, offering stable upside from present ranges.

Illustrative Monetary Mannequin (Created by Writer)

This valuation is additional supported by open market purchases of the inventory by insiders over the previous 12 months and as lately as one month in the past at costs larger than present costs.

Dangers

If rates of interest stay elevated for an extended time frame, or in the event that they proceed to rise from present ranges, MPA’s earnings will proceed to endure. It will proceed to justify a low a number of and should create the necessity for MPA to difficulty debt. This sadly makes an funding in MPA a little bit of a wager on rates of interest, which can be a irritating consequence if enterprise fundamentals proceed to enhance. MPA additionally has identified accounting complexities resulting from core accounting in its remanufacturing enterprise. I’m selecting to not contact on this intimately because it has been properly coated previously, and I believe the end result for the inventory received’t be determined by this accounting. Nonetheless, there are dangers that monetary outcomes could must be restated resulting from accounting points.

MPAA can be a comparatively illiquid inventory. The inventory trades on common, lower than $500,000 of quantity per day which can make it tough to promote a place with out bringing the worth of the inventory down. If an investor could have a have to promote the inventory rapidly for any purpose, it will be finest to not put money into MPAA in any respect.