EschCollection

Summer time final 12 months, I wrote a bullish article on Alexandria Actual Property Equities, Inc. (NYSE:ARE), the place I upgraded the inventory to purchase because of the mixture of the next elements:

- Traditionally depressed P/FFO a number of.

- Robust like-for-like efficiency with no indicators of decay going ahead.

- Sturdy stability sheet, the place the embedded construction of borrowings shields ARE from materially rising curiosity expense.

In a nutshell, it appeared that ARE had suffered a significant a number of contraction merely attributable to a extra aggressive low cost issue and the overall dislike towards the workplace section, whereas its underlying enterprise was nonetheless rising properly.

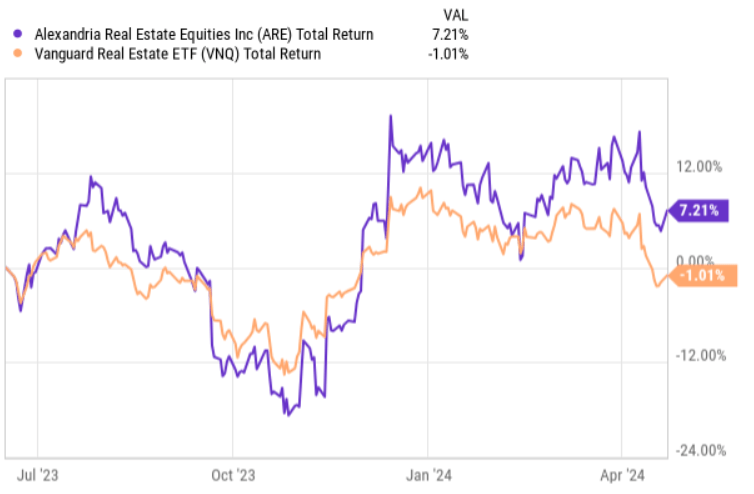

Since then, the Inventory has delivered comparatively stable returns, outperforming the broader REIT market.

YCharts

On the similar time the efficiency, particularly if we exclude the dividend impact, has actually not been that vital to doubtlessly trigger considerations about already exhausted upside.

Only recently, ARE issued its Q1, 2024 report, which reveals a number of attention-grabbing dynamics that, for my part, additional assist the purchase thesis right here.

Let’s now dissect the earnings bundle and assess the attractiveness of ARE.

Thesis overview

All in all, the latest quarterly efficiency was robust throughout the board, displaying no indicators of weakening profile.

For instance, some of the vital metrics – similar retailer web working earnings – , which actually captures the scenario in portfolio (i.e., the demand for current properties) got here in very robust. On a money foundation, the NOI determine elevated by ~ $133 million, which translated to a progress of seven.6%, in comparison with Q1, 2023 interval. The NOI on a money and similar retailer foundation elevated by 4.2%.

Because the occupancy remained secure, the important thing driver for the continued progress was the embedded lease escalators, which on common permit ARE to extend rents by 3% per 12 months. Aside from these lease escalators, ARE additionally managed to extract a profit from earlier leasing exercise outcomes, which warrant double digit lease progress from contract renegotiates / extensions or tenant replacements.

What can be value mentioning is the momentum in leasing exercise, the place additionally in Q1, 2024 ARE registered robust leasing volumes which have resulted in ~ 33% rental progress (and 19% on a money foundation).

By taking a look at these core metrics, it’s positively truthful to say that ARE’s funding technique (i.e., concentrate on trophy-type and life science primarily based properties) is enjoying out properly, having restricted headwinds from the struggling workplace house.

Now, as soon as now we have established that ARE is certainly in a sound place when it comes to having fun with secure demand for its properties, let’s check out the principle FFO progress drivers forward.

To begin with, you will need to underscore the underlying construction of ARE’s borrowing profile, which has grow to be a good higher asset within the context of latest rate of interest dynamics, the place the state of affairs of upper for longer has clearly strengthened. As of now, ARE has 32% of its complete debt maturing in 2049 and past, and the overall weighted-average remaining time period of debt is at 13.4 years, the place 98.9% of those proceeds are primarily based on a set charge. That is certainly one of many best debt maturities profiles in the entire publicly traded fairness REIT business.

Virtually, because of this ARE continues to be able to defend its FFO technology from surging curiosity expense as it may keep away from refinancing giant chunks of debt now when the rates of interest are excessive. Curiously, if we take a look at how the weighted-average rate of interest has advanced since Q1, 2023, we’ll discover solely a marginal uptick in the price of financing – about 25 foundation factors (to three.92%). The rationale why we see this enhance is as a result of ARE continues to speculate and appeal to incremental debt proceeds to fund the CapEx.

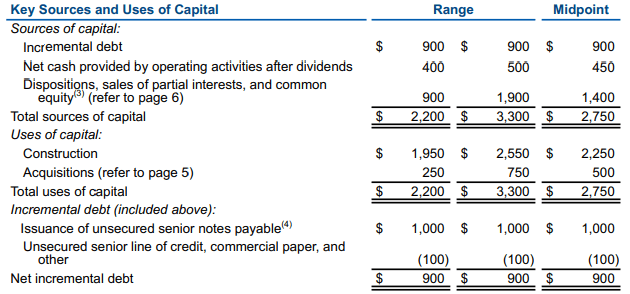

The desk under spotlight that this 12 months, ARE will broaden its debt base by ~ $ 900 million by primarily investing in new building, the place the projected IRR are inherently higher than within the M&An area.

ARE Q1, 2024 earnings supplemental

The desk additionally reveals {that a} main a part of the overall progress capital can be funded by fairness, the place retained FFO will play an vital function. This sends a transparent message that ARE stays cognizant of its debt profile and that the administration just isn’t keen to imagine fairly speculative danger by deploying notable a part of its $6 billion liquidity line.

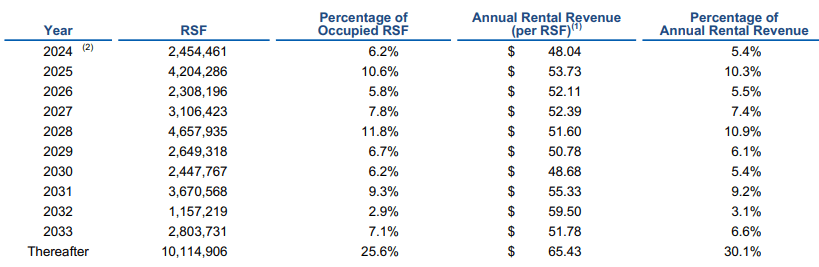

Additionally, by trying on the Q1, 2024 knowledge we are able to observe some success in ARE’s technique to concentrate on natural progress. Specifically, this quarter, ARE positioned into service natural improvement initiatives aggregating ~ 343 thousand RSF had been 100% leased throughout a number of submarkets, delivering incremental annual NOI of $26 million.

Furthermore, one other vital progress driver for ARE will extremely possible stem from the opportunistic lease expiry profile, the place for the rest of 2024 and 2025 the Firm should resign leases that presently account for ~16% of the overall ABR.

ARE Q1, 2024 earnings supplemental

Towards the backdrop of double digit leasing spreads, secure portfolio occupancy and the truth that roughly 6% of the overall 2024 and 2025 lease expiries are related to New York, which is the one main market, the place ARE’s emptiness ranges are up, we must always count on a positive enhance to the FFO from the following leasing exercise.

The underside line

In my view, ARE’s attractiveness has gone up because the publication of my bull case again in Summer time final 12 months. Whereas the Inventory has outperformed the REIT index, if we modify for the dividends we’ll arrive at ~2.7% worth appreciation. Within the context of strong Q1, 2024 knowledge and respectable progress prospects for 2024 and 2025, Alexandria Actual Property Equities, Inc. stays a stable purchase at traditionally low P/FFO of 9.5x.

![Web Design Glossary: 38 Terms & Definitions You Need To Know [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/05/bG9jYWw6Ly8vZGl2ZWltYWdlLzM4X3dlYl9kZXNpZ25fdGVybXMxLnBuZw.webp.webp)