Richard Drury

Tesla, Inc. (NASDAQ:TSLA) has continued to underperform YTD, with the corporate’s share worth declining greater than 30%. The corporate is all the way down to an nearly $500 billion market capitalization, and its core enterprise as a automobile firm continues to undergo. The corporate continues to spotlight companies that do not exist, similar to humanoid robots, or self-driving taxis, however its latest full self-driving (“FSD”) worth reduce highlights the weak point.

As we’ll see all through this text, Tesla will proceed to underperform, as its core enterprise stays weak, and it fails to color a practical image for earnings from different companies, as segments like self-driving stay years behind targets.

Tesla Highlights

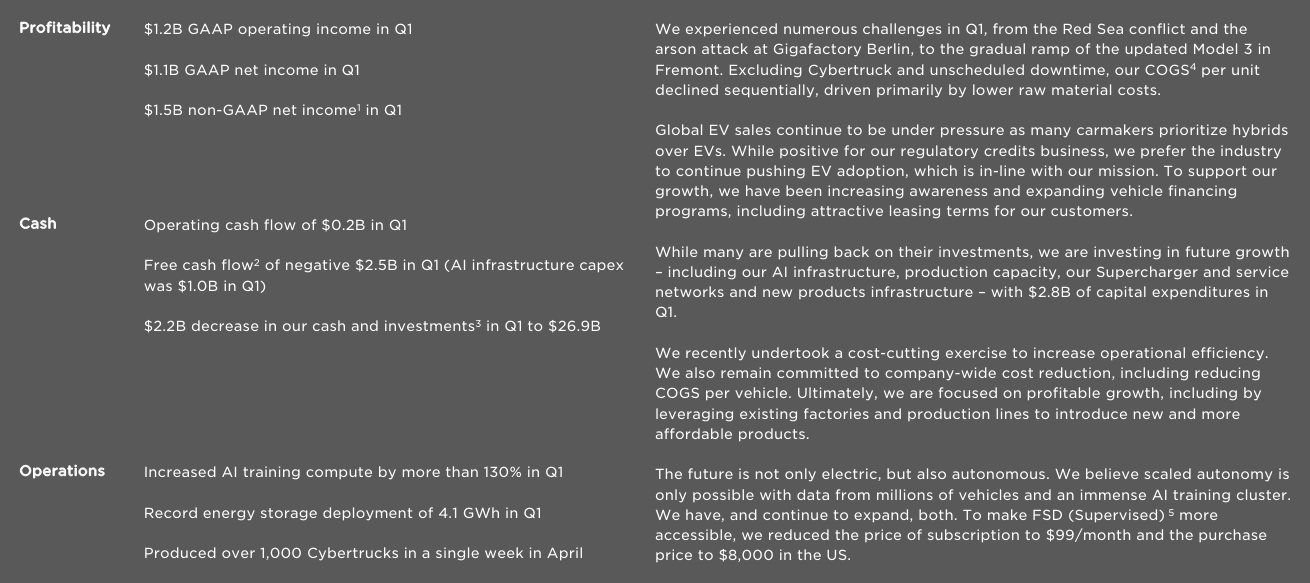

Tesla had an extremely tough quarter as demand for its autos stays weak, mixed with different continued challenges.

Tesla Press Launch

The corporate’s profitability petered out with simply over $1 billion in GAAP internet revenue. That provides the corporate a P/E of greater than 100. The corporate had an working money move of greater than $0.2 billion, with free money move (“FCF”) at a large $2.5 billion. AI infrastructure capex was $1 billion, that means even after the expansion the corporate was chasing, it had massively destructive FCF.

That damage the corporate’s money and investments considerably. The corporate is constant to chase development, however there isn’t any assure that chasing that works out. If it does not, the corporate may have spent billions of {dollars} of capital for nothing.

The corporate talks about billions spent to amass AI GPUs, the recent subject of the yr. Nonetheless, it fails to color an image of what it might accomplish with these versus rivals which have $10s of billions extra to spend on capital, similar to Meta Platforms, Inc. (META), which is spending nearly $40 billion on capex. The corporate’s core enterprise continues to drive the overwhelming majority of its income and had a troublesome quarter.

Tesla Monetary Efficiency

Tesla has continued to wrestle financially, as the corporate has seen weak demand for what’s the majority of its enterprise, autos.

Tesla Press Launch

The corporate noticed whole automotive revenues of $17.4 billion down 13% YoY with even extra QoQ weak point. The corporate’s This autumn-2023 income was greater than $21.5 billion, which is a hefty weak point. The corporate’s vitality technology and storage income stays sturdy, with 7% YoY development, but it surely stays lower than 10% of the corporate’s income.

Companies and many others. additionally proceed to carry out effectively off the corporate’s automobile rely. Nonetheless, nothing could make up for autos, with the corporate’s income lowering considerably. The corporate’s gross revenue dropped a large 18% YoY as its margins proceed to say no and gross revenue is now at lower than $3.7 billion for the quarter.

Versus a market capitalization of greater than $500 billion, the corporate is buying and selling at a P/E of roughly 40. Not an ideal look for an organization with declining earnings. Web revenue dropped greater than 50% YoY and the corporate’s annualized P/E is now greater than 100. FCF was a large destructive $2.5 billion and the company’s cash has declined.

Given continued weak point, we see no path for the corporate to show issues round and justify its valuation.

Tesla Operational Efficiency

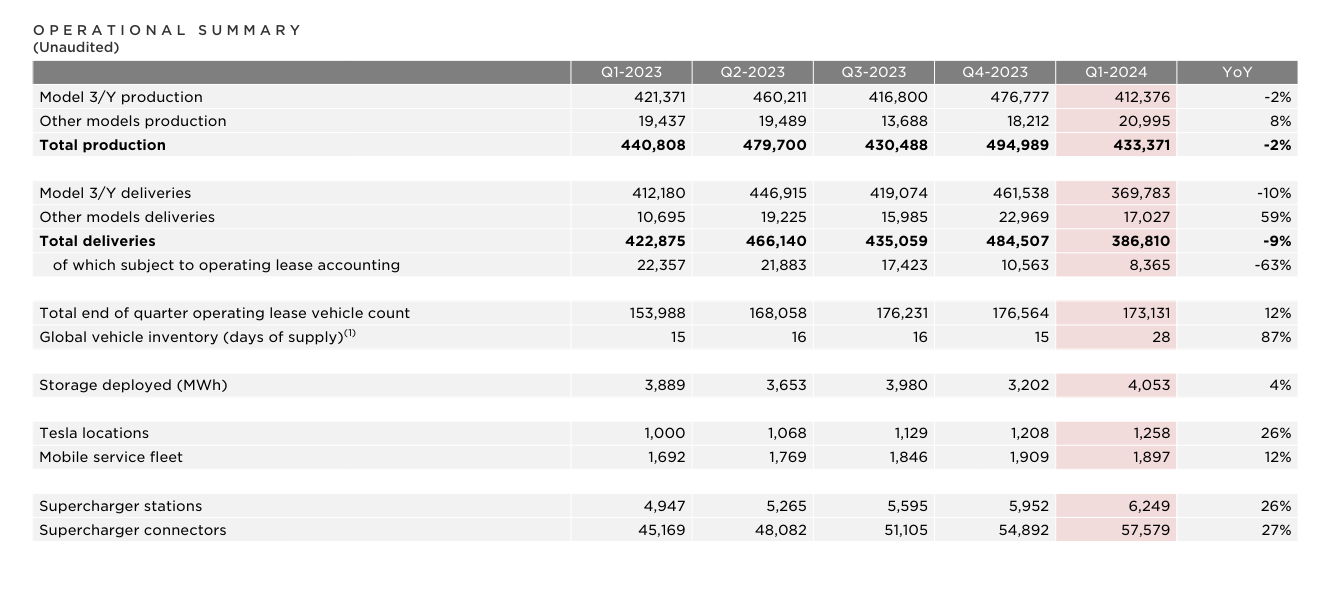

The corporate’s operational efficiency was impacted by delivery and different impacts, but it surely was additionally impacted by weak demand.

Tesla Press Launch

The corporate’s whole manufacturing for the quarter was simply over 430k down each YoY and QoQ. The corporate’s manufacturing has remained unstable, because it initially zoomed previous 1 million autos/yr however has struggled to cross 2. The corporate additionally noticed among the weakest efficiency in deliveries, by way of the ratio of autos produced versus delivered.

That has pushed the corporate’s stock to nearly double to twenty-eight. Storage and companies stay sturdy, but it surely’s clear that demand for the corporate’s autos stays extremely weak.

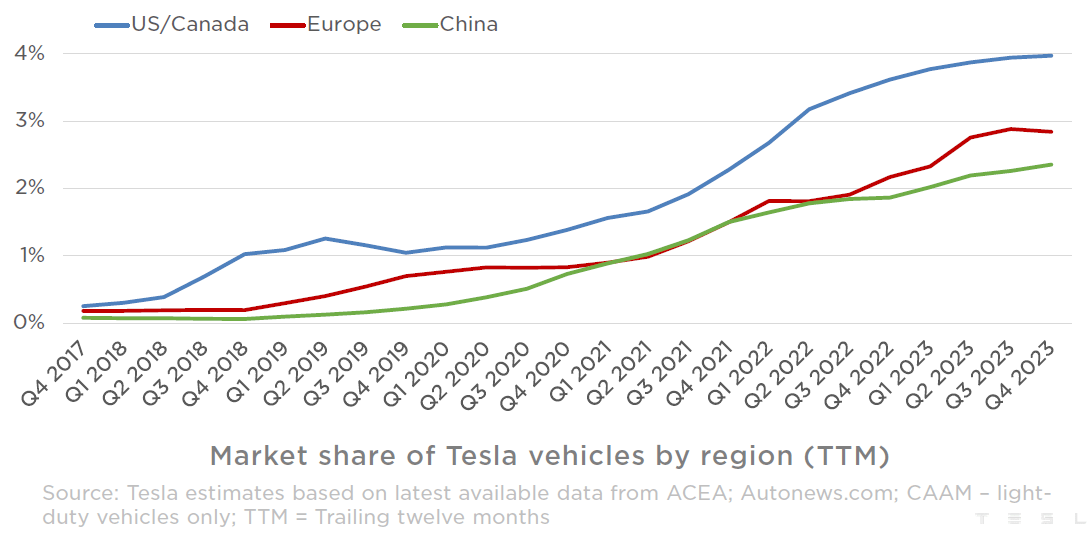

Tesla’s Market Share Progress Slows Down

The weak demand is visualized by the picture above, which highlights the market share of Tesla by area. It initially appears to be like promising, with a This autumn 2022 market share of roughly 3.5% within the U.S. / Canada, 2% in Europe, and a pair of% in China. By year-end 2023, the corporate’s market share was 4% U.S./Canada, and roughly 2.5% Europe, and a pair of.5% China.

Nonetheless, from year-end 2022 to year-end 2023, BEVs market share grew from 9% to 11%. So whereas the market share by BEV grew by 2%, the corporate solely gained 1.5% in its core markets, displaying it isn’t rising as quick because the BEV markets. That reveals the corporate’s market share is declining. We see this with elevated low-cost competitors, the place the corporate has been dethroned in markets similar to China.

Tesla Different Companies

The corporate has plenty of different companies; nonetheless, we count on none of them to be aggressive.

Tesla Press Launch

The corporate has been forced to qualify all of its FSD as “Supervised” as a result of lawsuits, and it is reduce its value for a subscription by 50%. The CEO originally promised to have greater than 1 million robotaxis on the highway a number of years in the past, however that section continues to wrestle, when rivals similar to Waymo are already actively incomes income from their robotaxis.

The corporate is increase a large portfolio of synthetic intelligence GPUs and has greater than 35k H100 equal GPUs value nearly $1 billion. What’s it utilizing these GPUs for? Loads of issues. What’s it utilizing these GPUs for which are earning profits? Nothing. The corporate is chasing quite a few different companies whereas its core enterprise continues to undergo.

There are some associated different companies similar to its battery cell manufacturing that may assist scale back prices, however its different companies like humanoid robots are aspect quests it has no experience in.

Our View

Tesla is chasing development, but it surely wants the flexibility to justify its valuation, with $10s of billions of revenue wanted to justify its valuation.

Tesla Press Launch

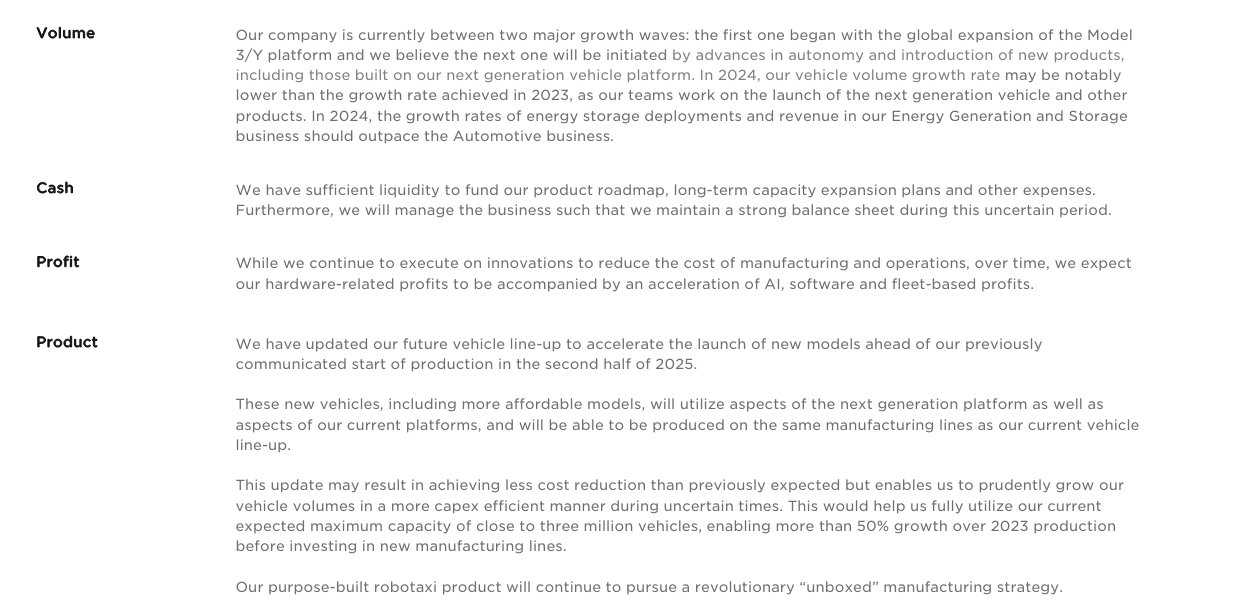

The corporate argues it’s between two main development waves, with the second anticipated to be initiated by advances in autonomy and new merchandise, together with a brand new technology automobile platform. What does that learn to us? The corporate admits it peaked with its present enterprise, regardless of its prior discussions of ~40% annualized development.

The corporate is anticipating automobile quantity development fee to be weak in 2024. The brand new merchandise it expects to drive the following wave do not exist. A brand new automobile program might assist the corporate out, however China is at present outcompeting at an inexpensive platform. Within the U.S., the corporate might outperform, with protections, however outdoors that we count on China to outcompete.

The corporate broadcasts it is getting into a area, similar to humanoid robots, that are successfully fully unbiased of its core energy. The corporate has mentioned it’s going to begin promoting helpful robots within the subsequent yr, but it surely’s 4 years and counting after its robotaxis estimate.

The corporate has been unable to persuade us why it is going to hit its lofty technological ambitions this time round, on condition that after years of guarantees, it is didn’t construct a major enterprise outdoors its core automobile enterprise.

Thesis Danger

The biggest danger to our thesis is Tesla’s continued concentrate on manufacturing dominance and the corporate’s capacity to innovate. Whereas the corporate has but to have successes that justify its valuation, a breakthrough with FSD or one thing else, might flip that round. The corporate is a poor funding in our view, however a “golden goose” occasion might at all times flip issues round.

Conclusion

Tesla has managed to construct an extremely spectacular enterprise. There isn’t any denying that the corporate has had some spectacular accomplishments within the midst of constructing the most important publicly traded automobile firm on the planet. There’s additionally no denying that the corporate’s EV enterprise stays sturdy and unparalleled in its goal market.

Nonetheless, when you’ve a market capitalization of greater than $500 billion, much more issues than that. Tesla, Inc. wants a path to $10s of billions in annual income, and proper now, we’re not seeing that. The corporate is itemizing hypothetical companies, however we do not see a path to growing them. General, that makes the corporate a poor funding.

Please tell us your ideas within the feedback under.