Adam Gault

Thursday’s first-quarter GDP report delivered a one-two punch for markets: slower-than-expected development and hotter-than-expected inflation. In response, shares fell and US Treasury yields rose. At first look, the risk-off response appears to be like cheap. However a more in-depth have a look at the GDP numbers nonetheless leaves room for debate.

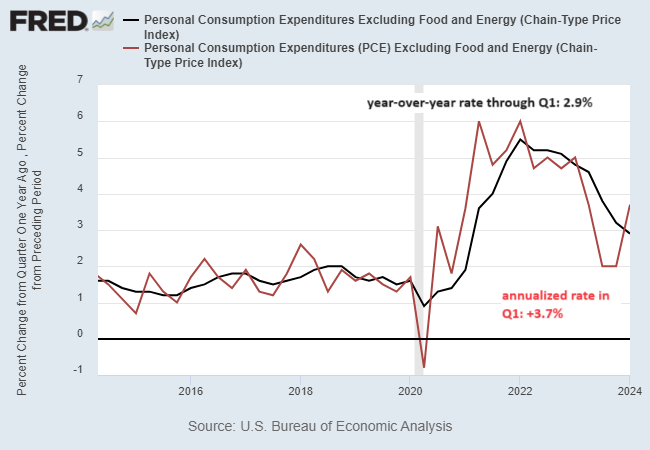

Let’s begin with the offending knowledge that despatched markets right into a tailspin: the private consumption expenditures worth index excluding unstable meals and power costs, a.ok.a. core PCE, which is alleged to be the Federal Reserve’s most well-liked inflation metric. On an annualized foundation in Q1, this metric turned up sharply, rising 3.7%, above expectations – information that despatched markets right into a tizzy (purple line within the chart beneath).

However the identical knowledge on a year-over-year foundation appears to be like cooler. Notably, core PCE by way of Q1 eased to 2.9% from 3.2% in This fall. The Q1 print marks the bottom tempo of inflation in three years.

Extra importantly, the year-over-year yardstick means that disinflation continues to be unfolding. The pushback, in fact, is that the annualized measure of core PCE factors to a pointy reflationary episode, which can sign that pricing strain is about to warmth up within the months forward.

That leaves us with the important thing query: Which core PCE inflation is the extra correct model of what’s occurring? The reply, in fact, is that nobody actually is aware of because the future continues to be unknowable. That mentioned, I are likely to favor the year-over-year development, for core PCE and different financial time collection. Why? It filters out some, maybe quite a bit, of the noise.

This time may very well be totally different, in fact, however historical past means that the annualized measure of core PCE has a behavior of leaping across the 1-year development. As such, it’s tempting to see the 1-year development because the sign and the annualized quarterly measure as noise. There are caveats to this view, however for probably the most half, it tends to carry true.

Accordingly, I’ll change my view if and when the 1-year development stops falling or, even worse, turns up. For the second, neither of these circumstances appears to be like probably, though I’m watching the incoming numbers intently from a variety of knowledge units for an early warning that my assumption is improper.

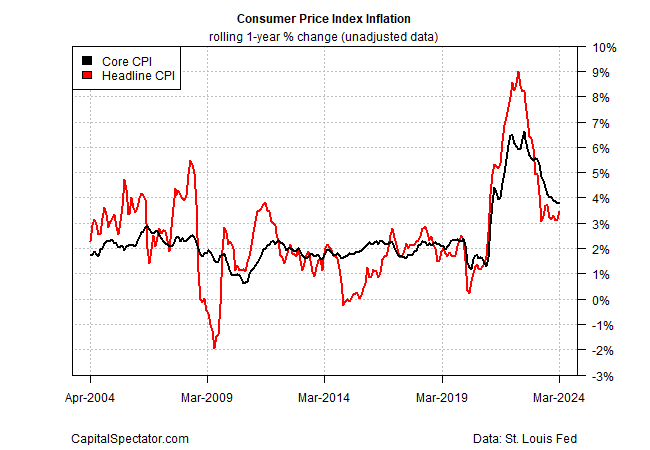

Be mindful too that Thursday’s sizzling core PCE knowledge for the annualized knowledge in Q1 is previous information. Recall that earlier this month we discovered that client worth inflation on the headline stage turned up in March. However core CPI in year-over-year phrases continues to be easing, albeit at a slower tempo recently.

The underside line: till the year-over-year charges of change in core PCE and core CPI flat line, or begin rising, I nonetheless anticipate disinflation to proceed. At what tempo and how briskly is open for debate, however in a binary framework that asks: Is disinflation persevering with, I’m nonetheless within the “yes” camp.

Editor’s Word: The abstract bullets for this text have been chosen by Searching for Alpha editors.