jewhyte

I revealed my ‘Strong Buy’ thesis for Microsoft (NASDAQ:MSFT) in my initiation report, revealed in July 2023. Since then, the inventory worth has surged by about 17%. I highlighted Microsoft’s functionality to combine AI-powered options into all their software program and platforms. They launched their Q3 FY24 earnings on April 25th with 17% of fixed income progress and 23% of working revenue progress, beating the market expectations. I’m inspired by their Copilot and Azure AI, extending Microsoft’s present know-how benefit. I reiterate my ‘Strong Buy’ ranking with a one-year goal worth of $510 per share.

Acceleration of Giant Azure Offers and Infrastructure for 3rd Social gathering AI Fashions

My largest takeaway from their Q3 result’s the acceleration within the variety of massive Azure offers, and Azure’s functionality to offer third-party AI fashions to enterprise clients. To spice up computing powers, Azure groups up with NVIDIA (NVDA) and AMD (AMD) to leverage the huge GPU computing energy, and supply 3rd celebration AI fashions to enterprise clients.

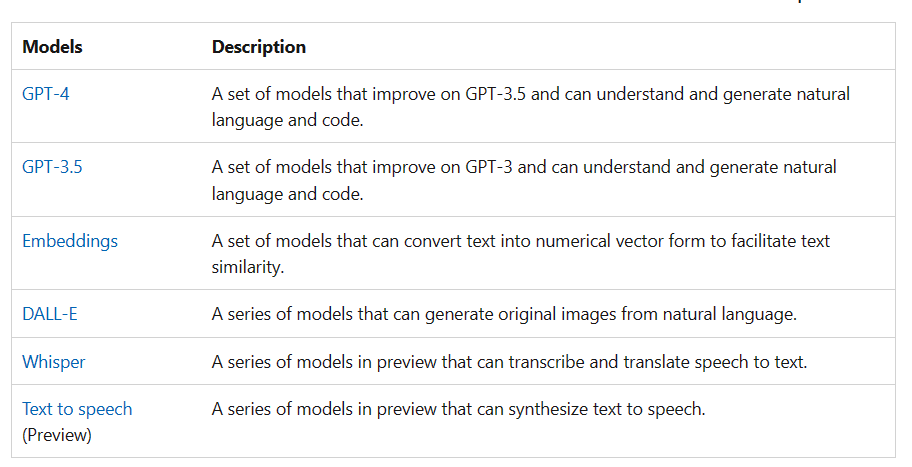

As an illustration, Azure affords OpenAI Service, granting REST API entry to OpenAI’s highly effective language fashions together with the GPT-4, GPT-4 Turbo with Imaginative and prescient, GPT-3.5-Turbo, and Embeddings mannequin sequence, as disclosed of their manual. These fashions would allow Azure customers to conduct massive mannequin machine learnings and deal with numerous AI-related workloads.

As communicated over the earnings call, >65% of the Fortune 500 make the most of Azure’s OpenAI Providers. I count on the business adoption will speed up within the close to future, as Microsoft extends their companies to small and mid-sized enterprises at reasonably priced prices. The first prices for AI computing are GPUs and vitality prices. With extra firms coming into the enticing GPU market, I forecast the price of GPUs will decline extra time. The bettering value construction might pave the way in which for business adoptions amongst small and mid-sized clients.

Microsoft Web site

Microsoft anticipates that Azure OpenAI and associated APIs atop Azure might turn into the foremost progress driver for his or her cloud infrastructure enterprise. Azure’s AI fashions might provide builders finest instruments to carry out massive language fashions and implement AI associated workloads. In consequence, Microsoft has been securing bigger and extra strategic Azure offers with a rise within the variety of $1 billion plus Azure commitments. In the course of the earnings name, Microsoft indicated that they skilled an acceleration within the variety of massive Azure offers within the quarter. The variety of offers surpassing $100 million elevated by 80% year-over-year, which is sort of exceptional. As such, I’m fairly optimistic about their Azure AI progress within the upcoming years.

For enterprises conducting AI workloads, they’ve to maneuver these workloads to cloud first, then make the most of present AI fashions for LLMs. It could be extra handy for enterprises to make use of Hyperscalers’ AI associated APIs, as enterprises don’t have to handle completely different distributors ((cloud infrastructure and mannequin supplier)). Extra importantly, enterprises can select and swap completely different AI fashions supplied by their cloud infrastructure supplier. Subsequently, Azure has distinctive benefit for its AI mannequin choices.

Adoption of Copilot

In September 2023, Microsoft introduced their Copilot strategy. As an AI companion, Copilot might incorporate the context and intelligence of the net and work knowledge, bettering productivities for customers. As disclosed, Copilot will likely be rolling out throughout Microsoft’s main functions and platforms. Particularly, the following Home windows 11 replace introduced Copilot and new AI-powered capabilities to all main apps. Their search engine and browser: Bing and Edge, have been powered by the newest AI fashions. Moreover, OpenAI’s GPT-4 Turbo is out there in Copilot and enterprise clients can leverage OpenAI’s newest mannequin for his or her AI-related workloads.

As communicated within the earnings name, GitHub Copilot has considerably enhanced productiveness for IT builders, being utilized by 1.8 million paid subscribers, representing a 35% year-over-year progress.

Most significantly, Microsoft is making Copilot out there to every type and sizes of enterprises. Practically 60% of the Fortune 500 enterprises are actually utilizing Copilot service. I feel Copilot will deliver Microsoft to a recent new stage, embedding AI into all main functions. Key causes are:

It prices $30 per person per 30 days for subscription to Copilot for Microsoft 365, which incorporates every part in Copilot plus AI in Phrase, Excel, PowerPoint, OneNote, Outlook, Groups, Copilot Studio, and knowledge safety. As indicated within the newest conference, their administration said that Microsoft performed a survey with 100 CIOs, and 38% of them are anticipated to undertake Microsoft’s Copilot within the subsequent 12 months. I anticipate Copilot goes to have a excessive adoption price, as these AI-powered capabilities might enhance worker’s productivities and save further prices for enterprise clients. As well as, enterprises may have to undertake the newest AI-powered 365 with a purpose to entice skilled abilities.

Microsoft 365 Chat is certainly a core characteristic of Copilot, enabling it to research a wild vary of information sources together with emails, conferences, chats, paperwork, and net contents. I argue that solely Microsoft possesses the true functionality to leverage all sources of information and combine these knowledge factors to offer helpful insights for enterprise clients. With Microsoft’s expansive ecosystem encompassing the working system, e-mail companies, Staff conferences, numerous functions, search engine, workplace suite, and web browser, the combination of Copilot with these present functions holds immense potential, in my opinion.

Monetary Recap and FY25 Outlook

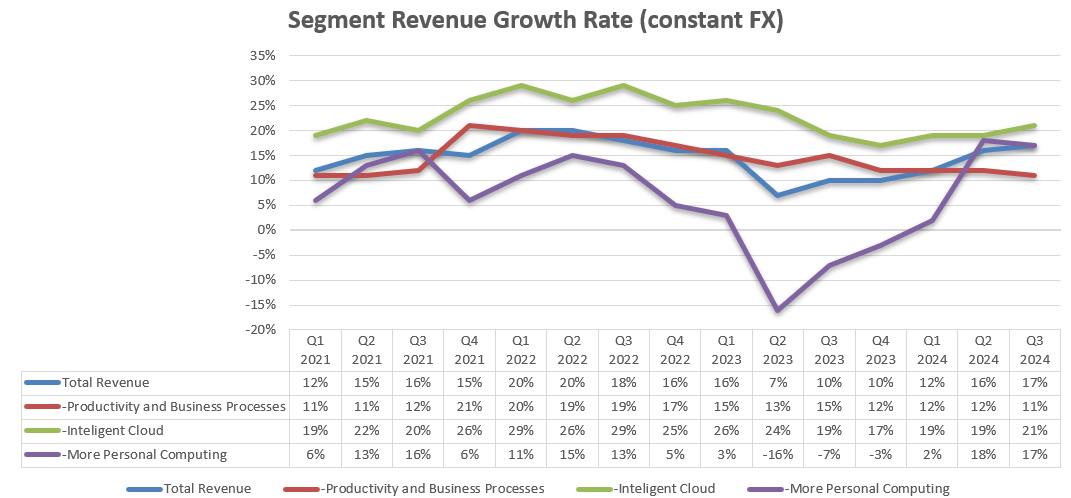

In Q3 FY24, Microsoft delivered 17% fixed income progress and 20% EPS progress, beating the market expectations. As illustrated within the chart beneath, Microsoft’s enterprise progress has been accelerating in latest quarters, primarily pushed by sturdy clever cloud progress and the market restoration of private computing.

Microsoft Quarterly Earnings

As Microsoft has already delivered sturdy topline and earnings progress prior to now three quarters, they’re extra more likely to ship double-digit income progress and 20%+ EPS progress for FY24. The market can pay extra consideration to their FY25’s progress potential, and I’m contemplating the next facets:

-For Azure Cloud enterprise, I assume they’ll preserve 20%+ progress over the following few quarters. As communicated by all the foremost hyperscalers, together with Microsoft, Amazon (AMZN) and Alphabet (GOOGL), enterprises started to optimize their cloud consumptions in 2023 with a purpose to cut back the general IT spending price range. In the latest quarter, the three cloud gamers all indicated that the optimization was nearing completion, they usually count on cloud spending to normalize within the close to future. As such, I anticipate Microsoft’s cloud progress will speed up in FY25. As well as, Microsoft has expanded their AI capabilities in Azure infrastructure, offering third-party AI APIs for enterprise clients. These AI capabilities would improve their income progress potential in FY25, in my opinion.

– Microsoft nonetheless has big progress potential of their Workplace E5 penetration. In the course of the latest conference, Microsoft discloses that Workplace E5 solely has 12% penetration price amongst their Workplace 365 base, as such, they’ve an enormous progress alternative by means of E3-E5 upgrades. Workplace E5 supplies enhanced safety features together with Cloud App Safety, Defender, in addition to BI Professional utility. Cloud safety is sort of essential for enterprise clients and the improve from E3 to E5 might deliver further worth for enterprise clients, higher leveraging Microsoft’s Copilot and associated AI functionalities. Consequently, I anticipate the improve might contribute to large progress for Workplace 365.

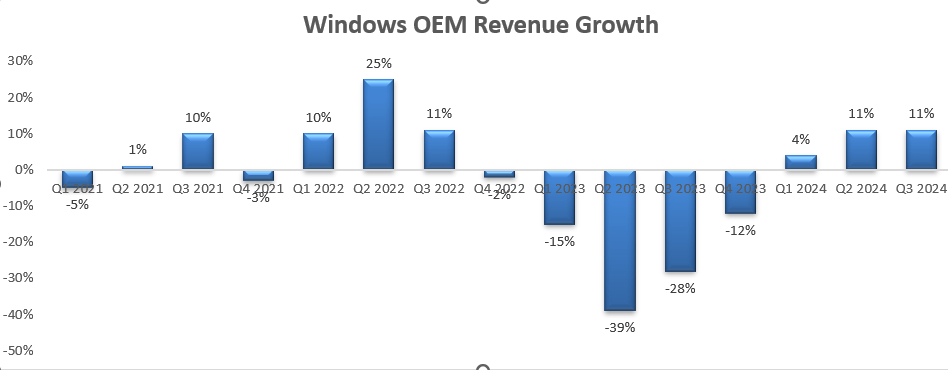

– Lastly, Home windows OEM progress is tied to the PC cargo to some extent, which is sort of risky in nature. As depicted within the chart beneath, Home windows OEM grew by 11% in Q3 FY24, rebounding from sluggish progress in FY23.

Microsoft Quarterly Earnings

IDC predicts that the worldwide PC cargo will develop at a CAGR of two.4% from 2024 to 2028, as detailed within the desk beneath. As such, I predict Microsoft will generate round 5% of income progress from Home windows OEM in FY25, reflecting 2.5% quantity progress and a pair of.5% worth progress.

IDC Report

Placing every part collectively, I calculate that Microsoft will ship 15% of topline progress in FY25.

Valuation Updates

As mentioned, the income is predicted to develop by 15% year-over-year in FY25, primarily pushed by 20%+ Azure cloud progress, E3 to E5 upgrades, and Copilot and Azure AI stack progress. Please notice that Microsoft accomplished the acquisition of Activision Blizzard in Q2 FY24, which will likely be reported in Extra Private Computing section.

On the fee facet, Microsoft has been engaged on their value optimization initiatives. The entire variety of headcounts on the finish of December 2023 was 2% decrease than one yr in the past. On the identical time, Microsoft has been growing R&D spending on AI, which might exert some value strain on gross income. I anticipate Microsoft will obtain a 10bps margin growth from gross margin, and 20bps from gross sales & advertising and marketing expense leverage. The gross sales & advertising and marketing spending as a % of complete income declined from 15.8% in FY18 to 10.7% in FY23. I anticipate Microsoft might proceed to profit from the working leverage from their gross sales & advertising and marketing bills as Microsoft is offering extra merchandise associated to AI and cross-selling might enhance salesforce productivities.

The income, working income and internet revenue are projected as follows:

Microsoft DCF – Creator’s Calculations

With the intention to calculate free money circulate to fairness, I modify their internet revenue with depreciation & amortization, working capital adjustments and internet borrowings.

Microsoft FCFE- Creator’s Calculations

The price of fairness is estimated to be 12% for Microsoft with these assumptions: risk-free price 4.22% (US 10-Y Treasury Yield); fairness danger premium 7% and beta 1.12 (SA’s DATA). Discounting all the longer term FCFE, the one-year worth goal is calculated to be $510 per share. As Copilot and Azure AI stack haven’t generated significant progress for Microsoft at current, the market is likely to be underestimating the sturdy progress potential from these AI associated investments.

Key Dangers

Microsoft has been allocating greater than 13% of complete income in the direction of capital expenditures, primarily pushed by growing funding on cloud infrastructure, knowledge facilities and AI associated investments. I don’t anticipate Microsoft will decelerate their capital expenditure within the close to future. As communicated over the earnings name, Microsoft will improve their CAPEX spending in FY25.

Their cloud enterprise remains to be rising at 20%+, and the growing AI calls for require them to spice up computing energy and buy extra GPUs from Nvidia and AMD. Though the growing CAPEX would affect their free money margin within the close to future, I feel Microsoft is making the best funding for his or her future progress.

As reported by the media, Microsoft will cease packaging its Groups videoconferencing app with its Workplace software program after the observe attracted antitrust scrutiny. With out bundling, Microsoft may encounter some headwinds for his or her Groups progress. Clients might want to buy Groups subscription individually, and in that case, clients may go for different videoconferencing apps like Zoom (ZM).

Conclusion

I consider Microsoft is nicely positioned to capitalize on AI associated investments, with each Copilot and Azure AI holding vital progress potential within the AI period. Microsoft’s complete AI choices span throughout working system, looking out, gaming, Workplace 365, cloud infrastructure, emails, and on-line collaborations. I’m inspired by their acceleration of enormous Azure offers in latest quarters, signaling enterprises are ramping up their funding in AI and cloud transition. Consequently, I reiterate my ‘Strong Buy’ ranking with a one-year goal worth of $510 per share.