CHUNYIP WONG

In February, we mentioned Exxon Mobil (NYSE:XOM) as an organization that was a beneficial alternative due to its steady execution. Since then, the corporate’s share value has gone up by greater than 16% versus shut to three% for the S&P 500. That, mixed with a weaker pricing atmosphere, exhibits how the corporate wants excellent execution to justify its valuation.

Exxon Mobil Quarterly Outcomes

Exxon Mobil had sturdy outcomes from the quarter, however traders want to concentrate to what’s now a lofty valuation of virtually $470 billion.

Exxon Mobil Investor Presentation

The corporate had $8.2 billion quarterly GAAP earnings, giving the corporate a P/E ratio of greater than 14. The corporate had $14.7 billion in CFFO, and continues to speculate closely in its enterprise, to the tune of virtually $6 billion in capital expenditures. Which means the corporate’s FCF is $9 billion, giving the corporate a FCF yield of seven.6% annualized.

It isn’t unhealthy FCF, but it surely’s nothing to be significantly enthusiastic about from a shareholder return perspective. The corporate’s web debt stays minimal, and the corporate does proceed to spend most of its money move to shareholder returns, primarily by a dividend of simply over 3%. These are whole shareholder returns of virtually 5.8%, a powerful yield.

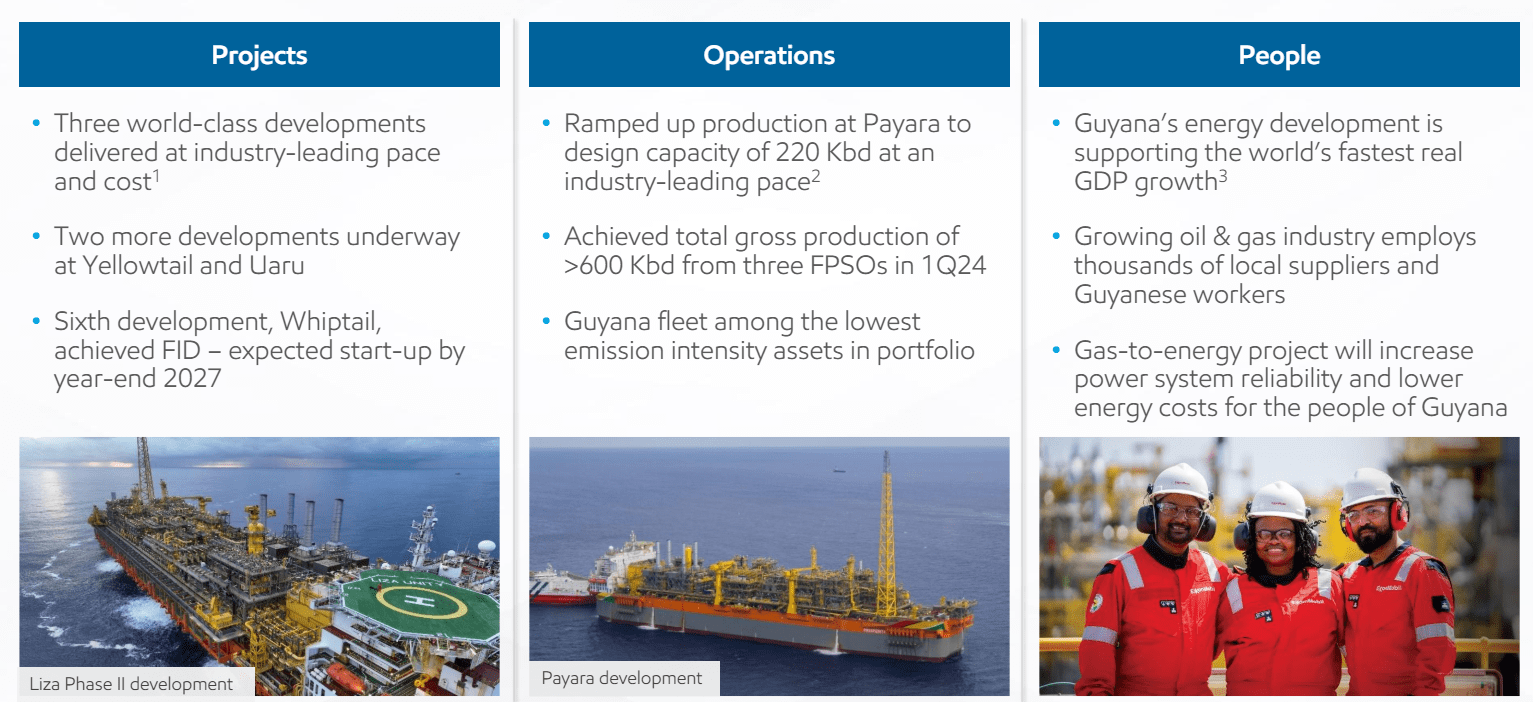

Exxon Mobil Guyana

The corporate’s development engine continues to be Guyana. There’s an asterisk right here that the corporate has filed for arbitration over Chevron’s deliberate acquisition of Hess Company. Chevron has mentioned that it’ll stroll away if it can not buy Guyana, however there’s an consequence the place Exxon Mobil should purchase Hess Company’s stake in Guyana, serving to it considerably.

Exxon Mobil Investor Presentation

The corporate has continued to construct up quite a few world-class FPSOs with three already delivered at an industry-leading tempo and price. The corporate has two extra developments underway at Yellowtail and Uaru, which collectively will add nearly 500 thousand barrels / day of manufacturing. The corporate has additionally achieved an FID on Whiptail.

The 4th and fifth initiatives will take manufacturing from the asset in the direction of a large 1 million barrels / day, as the corporate’s 3 FPSOs have handed >600 Kbd in manufacturing within the 1Q24. The immense property and fleet right here will allow substantial shareholder returns.

Exxon Mobil Development Tasks

Exxon Mobil’s development initiatives are anticipated to considerably assist general earnings, displaying continued energy in execution.

Exxon Mobil Investor Presentation

The corporate is concentrated on constructing a powerful portfolio of high-volume merchandise, and by 2027 it expects to have >20Mta, offering billions of USD in earnings. The corporate expects these initiatives to drive a considerable % of the corporate’s development. The corporate has a number of initiatives which might be began up and with a high-grade portfolio, it might proceed to upscale them.

These development initiatives with excessive margins related to the corporate’s present property make it a beneficial funding.

Exxon Mobil Investor Presentation

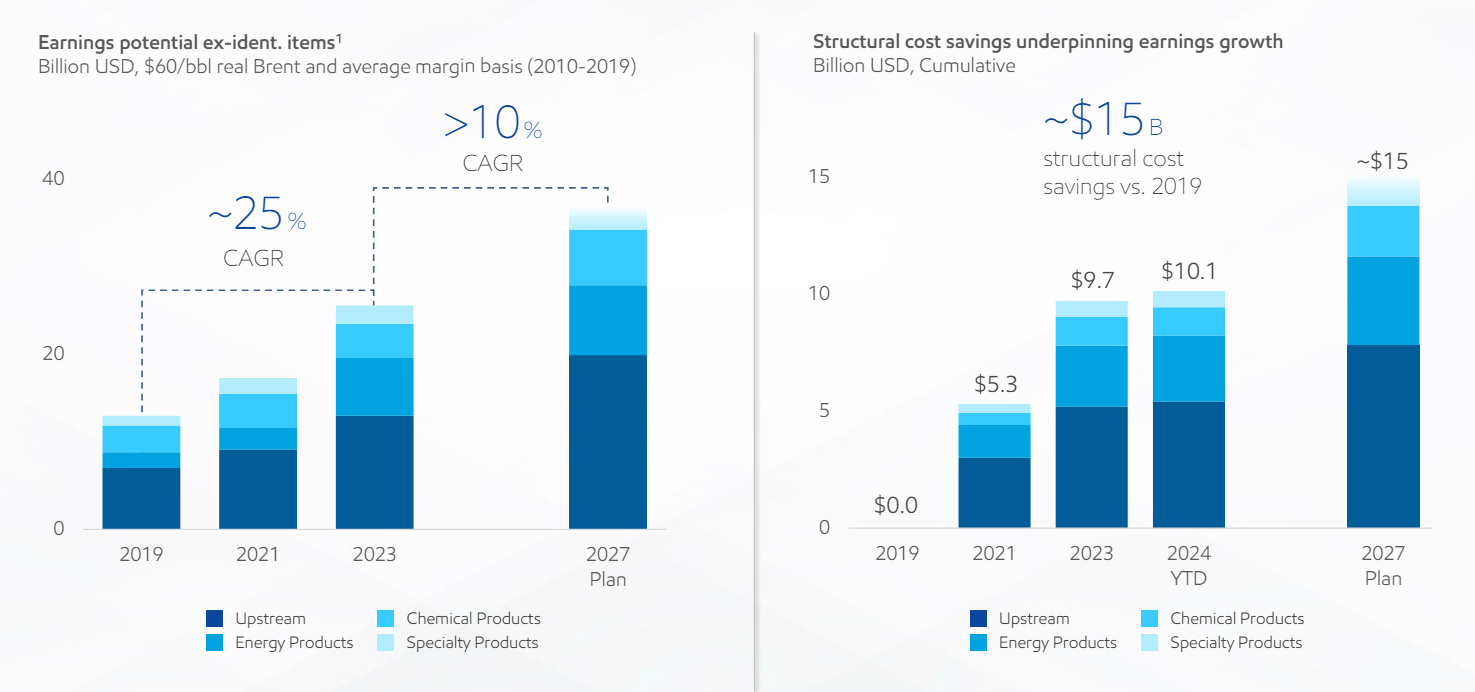

The corporate expects general earnings to have the ability to enhance considerably from present ranges in the direction of $40 billion by 2027. The corporate expects to be benefited by structural price financial savings as nicely. General earnings of virtually $40 billion would present some constant earnings development.

Nevertheless, it additionally exhibits how the corporate is overvalued.

Exxon Mobil Steerage

Exxon Mobil is concentrated on continued sturdy shareholder returns as part of its steerage. Nevertheless, to justify its valuation, the corporate wants to take care of its energy.

Exxon Mobil Investor Presentation

The corporate expects double-digit earnings development by 2027 because it ramps up Guyana and continues to ramp up quite a few different sturdy initiatives primarily based on the corporate’s property. The corporate expects structural price efficiencies will assist the corporate considerably as nicely. Nevertheless, with a P/E of greater than 14x, the corporate wants important earnings development.

Nevertheless, even with this earnings development, the corporate continues to be going to have a double-digit P/E ratio. That is on the comparatively excessive costs within the present market. The corporate additionally operates in a market the place long-term demand stays questionable because the world strikes past fossil fuels. Exxon Mobil is sluggish to regulate to local weather change and that continues to be an enormous danger.

The corporate at its present valuation cannot simply drive double-digit shareholder returns, making it a poor funding in a dangerous atmosphere.

Thesis Threat

The most important danger to our thesis is the pricing atmosphere. Brent crude is at only a hair below $90 / barrel, with continued battle within the Center East, nonetheless, pure gasoline costs stay extremely weak at lower than $2 / mmBtu. LNG initiatives are anticipated to proceed rising, supporting costs, however the general market is predicted to stay weak. That might dramatically harm earnings.

Conclusion

We mentioned above how Exxon Mobil was a powerful funding as a result of its regular execution. Since then, the corporate’s share value has gone up nearly 20%. That has modified the thesis for the corporate and its capacity to proceed driving long-term shareholder returns. The corporate now wants excellent execution, particularly in a unstable pricing atmosphere.

That is powerful to do. The corporate has long-term dangers if oil and pure gasoline demand go down, and already within the U.S. pure gasoline demand is being pressured. LNG may help, however the issue with commodities is inelastic provide, that might put sturdy pressures on costs. We do not suggest promoting Exxon Mobil, however we suggest being cautious about extra investments at present costs.