Tippapatt

Introduction & Funding Thesis

Doximity (NYSE:DOCS) is a cloud platform for US medical professionals that has severely underperformed the S&P 500 and Nasdaq 100 YTD. I initiated a “hold” ranking on the inventory on January 16, and it predicated on my perception that the corporate was seeing its income progress gradual, regardless of displaying monetary robustness by bettering margins.

The corporate reported its Q3 FY24 earnings in February, the place income and earnings grew 17% and 32% YoY, respectively, beating expectations. The administration additionally raised their steerage for each income and Adjusted EBITDA for FY24. Though the corporate stays centered on driving sturdy AI-led product improvements whereas rising profitability, the corporate’s slowing income progress stays a priority.

The corporate is seeing the variety of clients with no less than $100,000 in subscription income decline, whereas the Internet Retention Price (NRR) is weakening as properly, indicating that it’s having points with buyer churn and adoption relative to the tempo of recent buyer wins. On the identical time, macroeconomic headwinds proceed to persist, dampening pharmaceutical budgets. Whereas I imagine that Doximity has the potential to have the ability to revive its progress story, given its tradition of innovation and the chief hiring of Lisa Greenbaum as Chief Industrial Officer, the administration hasn’t offered clear ahead steerage. Due to this fact, I’ll proceed to remain on the sidelines and search for proof of a turnaround with a purpose to provoke a place, ranking it a “hold.”

A fast primer about Doximity

Doximity is a digital platform for US medical professionals that helps them collaborate with their colleagues, conduct digital affected person visits, keep up-to-date with the most recent medical information and analysis, and higher handle their careers, thus permitting them to unlock productiveness and supply higher care for his or her sufferers.

When it comes to their enterprise mannequin, the platform is free for all physicians, making it the biggest medical skilled community within the US. The corporate generates income from pharmaceutical producers and healthcare methods on a subscription-based pricing mannequin, the place their clients get entry to a set of business merchandise, corresponding to Advertising, Hiring and Telehealth options, which profit from broad doctor utilization.

Doximity’s ecosystem advantages from highly effective community results with deeper engagement from medical professionals that will increase the breadth of their instruments, attracts extra members, and drives worth for his or her income producing pharmaceutical and well being system clients, which in flip permits Doximity to drive focused product innovation, making a win-win for all.

The nice: Income met expectations and margins are increasing with a strong product pipeline

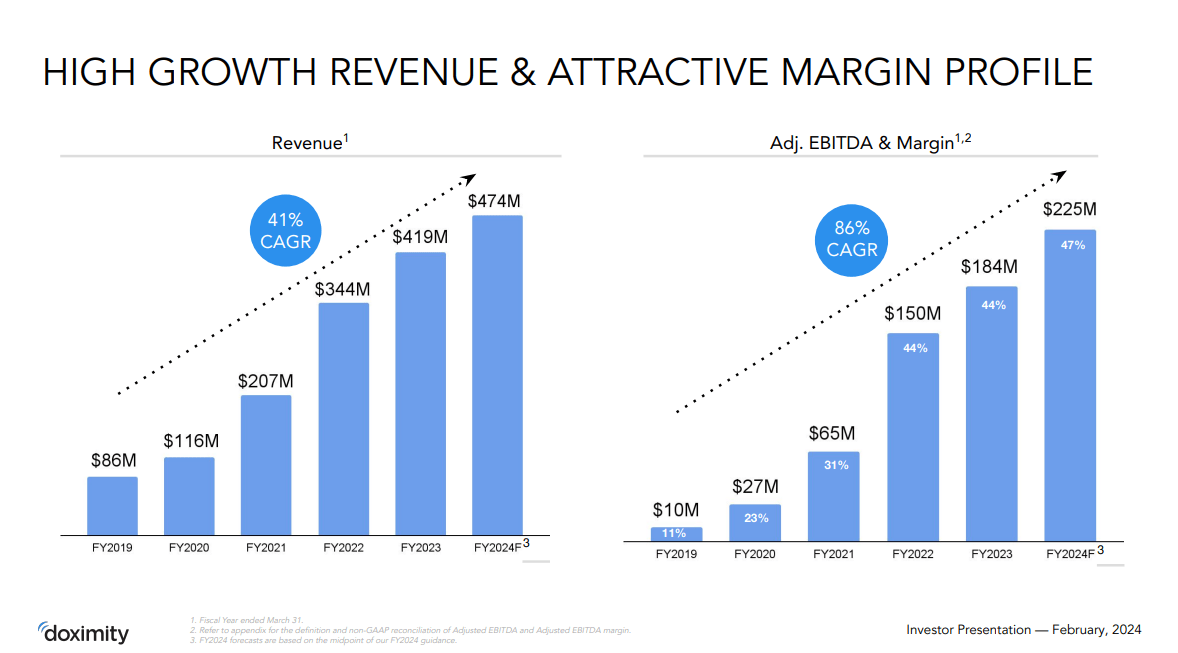

Doximity reported its Q3 FY24 earnings, the place each income grew 17% YoY to $135.3M, exceeding expectations by 6%. In my earlier put up, I talked about Doximity’s complete addressable market (TAM) which was estimated at $18.5B. Through the earnings call, Jeffrey Tangney, CEO of Doximity, raised the midpoint of their income steerage for the total FY24 by $8M, or 2%, to roughly $474M. This may symbolize a YoY income progress charge of roughly 13.1%.

Through the earnings name, the CEO outlined that engagement reached a brand new excessive watermark in Q3, with energetic customers on a quarterly, month-to-month, weekly, and every day foundation up double-digit percentages on a YoY foundation. As Doximity continues to develop its social community of medical professionals by including new members, I imagine utilization on the platform will improve, thus deepening adoption, with 289 clients paying $100,000 in subscription income within the Trailing Twelve Months (TTM) interval. On the identical time, the corporate efficiently landed a number of main hospital purchasers in Q3.

Q3 FY24 Earnings Slides: Income and Earnings progress

Moreover, Doximity’s administration is laser-focused on driving continued product innovation and believes that the subsequent part of their progress might be led by AI. Through the earnings name, the CEO outlined how their HIPAA-compliant GPT product has already been serving to medical doctors enhance their productiveness by lowering their administrative load. Concurrently, the corporate will unveil their new shopper portal on the Pharmaceutical Shopper Summit in Might, which goes to have options corresponding to real-time engagement studies and prescription gross sales information, which is able to enhance general transparency and ease of use.

Shifting gears to profitability, Doximity generated an Adjusted EBITDA of $73.3M, which grew 32% YoY at a margin of 52.2%, in comparison with 48.2% in Q3 FY23. This was pushed by streamlining working bills, which grew at roughly 8% YoY, a lot slower than the speed of income progress. For the total FY24, the corporate is elevating its Adjusted EBITDA steerage by 6% to $225M, which might symbolize a margin of 47%, an enchancment of 310 foundation factors from 43.9% a yr earlier.

The unhealthy: Prospects with $100K+ spend is declining, NRR is weakening, Macro headwinds persist.

In my earlier put up, I talked about slowing income progress and declining NRR. Sadly, the corporate hasn’t made such progress on this entrance, regardless of sturdy product innovation. With income projected to develop 13.1% YoY, it’s a important slowdown from the 41% compounded annual progress (CAGR) it noticed between FY19 and FY24. On the identical time, consensus estimates level to even slower income progress of 10% in FY25.

There are two causes for that. The primary cause is tied to the gradual progress charge of consumers with $100K+ in subscription income, which grew 2% YoY to 289. Nonetheless, on the finish of FY23, there have been 294 clients with no less than $100K in subscription income, which might point out that there’s truly a decline of 1.7%, indicating that clients are lowering their spend and adoption on the platform. This ties with the second cause, the place we see NRR dropping to 115%, down from 119% a yr in the past, which additional reinstates the difficulty that Doximity is going through with buyer churn and never having the ability to drive adoption in comparison with the speed of recent buyer offers, which is making traders cautious about its future progress story.

Through the earnings name, the CEO talked about that macroeconomic headwinds proceed to persist, which is negatively impacting pharma budgets. In my earlier put up, I talked concerning the study by Deloitte, the place it discovered that the typical price to develop an asset from discovery to launch had been rising whereas the typical gross sales per asset have been on the decline, leading to larger funds scrutiny in pharma firms. This has been placing downward stress on the general gross sales momentum at Doximity.

Tying it collectively: Upside stays, however the progress story wants to come back again.

Trying ahead, Doximity is projected to develop its income and earnings by 13.1% and 22% YoY, respectively, in FY24. Given the shortage of ahead steerage by the administration, I’ll assume that Doximity will be capable to return to rising quicker than its present charge by FY26 at 15%, ought to its present efforts at product innovation and hiring Lis Greenbaum because the Chief Industrial Officer translate into a better variety of new buyer wins and deepening adoption of its platform amongst current clients. This may lead to a better variety of clients with $100K+ in subscription income and an bettering NRR. On the identical time, I’ll assume that Doximity administration will stay centered on profitability, and due to this fact the corporate will be capable to preserve its present Adjusted EBITDA margins of 47–48%. This may translate to a complete Adjusted EBITDA of $284M by FY26, which might be equal to $235M when discounted at 10%.

Taking the S&P 500 as a proxy, the place its firms develop their earnings on common by 8% over a 10-year interval with a price-to-earnings ratio of 15–18, I imagine that ought to Doximity be capable to revive investor confidence by reigniting its progress story, it ought to commerce at roughly 1.5x the a number of of the S&P 500. This may translate to a PE ratio of roughly 25, or a value goal of roughly $29.4, representing an upside of 27.9% from its present ranges.

Creator’s Valuation Mannequin

Whereas I imagine that the upside could be realized ought to the corporate return to progress mode, I imagine will probably be a risky journey. The administration has loads to show to translate its present product innovation and government hiring into new buyer wins and proceed to retain them whereas driving deeper adoption on the identical time. Up to now, the shortage of ahead steerage past FY24 is dampening investor confidence. And given my threat urge for food, I’ll select to be on the sidelines and look forward to additional course within the administration commentary or an uptick in gross sales momentum to provoke a place. For now, I’ll charge it a “hold.”

Conclusions

Whereas Doximity is driving sturdy product innovation and increasing its revenue margins, its income progress charge has been slowing, pushed by a decline in clients with $100K+ in subscription income, weakening NRR, and persisting macroeconomic headwinds. Ought to the corporate be capable to revive its progress story as soon as once more, given its innovation pipeline and the addition of Lisa Greenbaum as Chief Industrial Officer, I imagine there could possibly be a large upside from its present ranges. Nonetheless, given the shortage of ahead steerage from the administration, I’ll select to be on the sidelines and charge the inventory a “hold.”