Kirk Fisher/iStock Editorial through Getty Photos

The inventory of expertise firm Tesla, Inc. (NASDAQ:TSLA), which focuses on driving humanity in the direction of a sustainable future, has lengthy been seen as expensive and overvalued. Specializing in pricing metrics equivalent to price-to-earnings or price-to-sales might trigger buyers to ignore this firm, however these taking the time to worth the corporate may as an alternative discover a very compelling alternative.

On this article, I’ll worth the corporate utilizing a sum-of-the-parts strategy, and what we are going to uncover is a reasonably valued firm with a variety of optionality at at present’s buying and selling value. To get a way of what that optionality might suggest, I’ll do a separate calculation the place I embrace hypothetical optionality transformed to worth.

The explanation I take advantage of a sum-of-the-parts strategy for Tesla is as a result of the totally different enterprise segments have totally different margin profiles, scalability, and maturity. Throwing a blanket over these and never breaking the segments aside would make it very troublesome to precisely venture numbers, as you lose out on the granularity.

Automotive

The principle enterprise section of Tesla is the manufacturing of electrical automobiles. Traditionally, we now have seen the ramping of assorted fashions, and Tesla has already solved the key challenges that include the manufacturing course of. The gigafactory precept is on a copy-and-paste foundation, and whereas heavy on capital expenditures, I count on Tesla constructing out extra gigafactories to be a comparatively clean course of. A construct out will likely be vital, as Tesla is near capability because it stands.

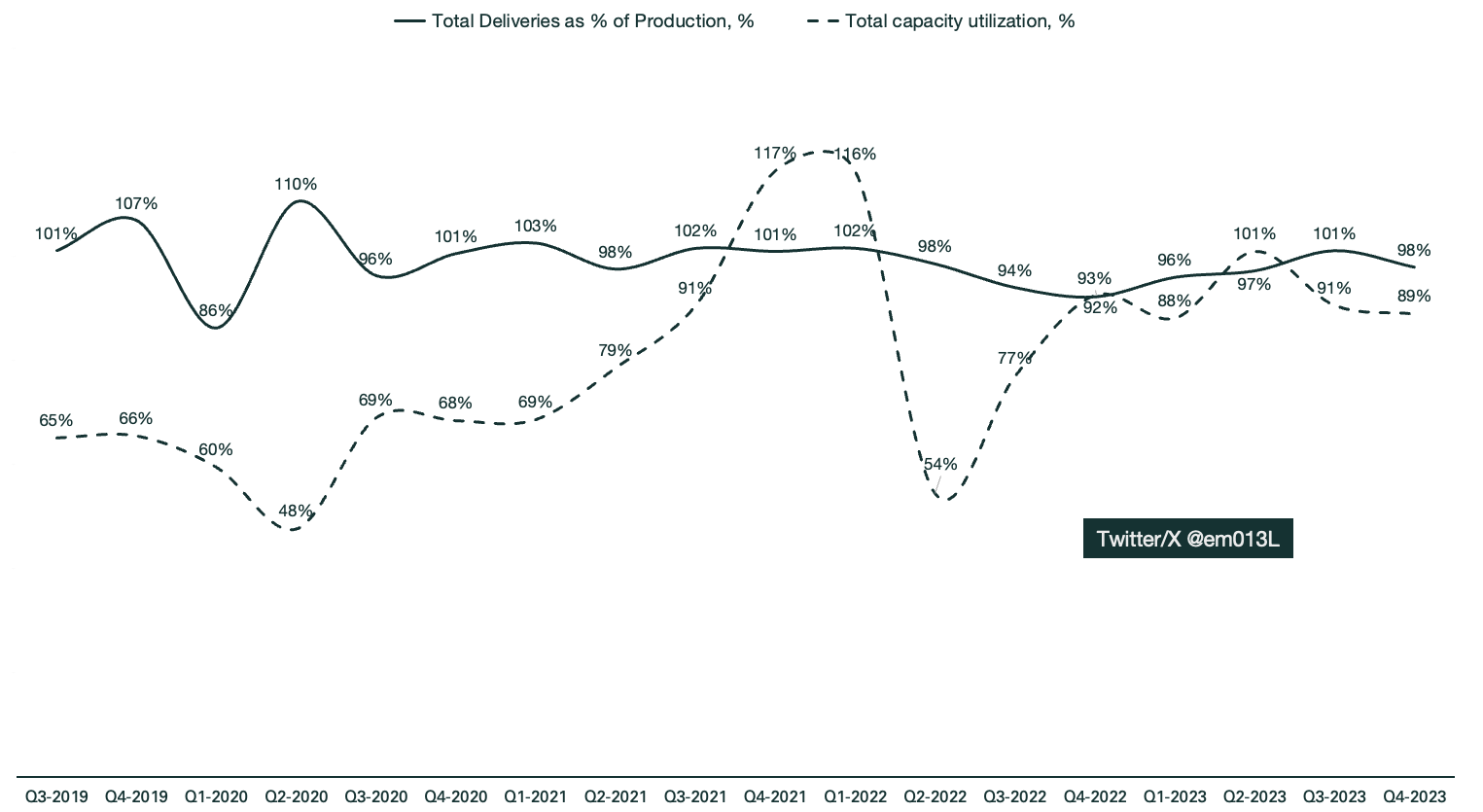

Emir Mulahaliliovic X@em013L, Tesla SEC Filings

Tesla constantly stays at ~90% capability and sells roughly all manufactured automobiles every interval. This must enhance exponentially, and I count on it to, as the worldwide EV market compounds at 23.4% yearly via 2033 (supply: Precedence research). The present annual manufacturing capability is ~2.25 million automobiles; I venture Tesla to ship ~5 occasions that in 2033.

I venture that Tesla will lose market share within the EV area however acquire market share as a proportion of the worldwide automotive market, as EVs will make up a larger portion of world automotive gross sales.

In relation to margins, I venture that Tesla will see larger general margins in comparison with different automobile producers because of manufacturing effectivity and model fairness. I venture working margins to extend from ~10% to ~13% by 2033.

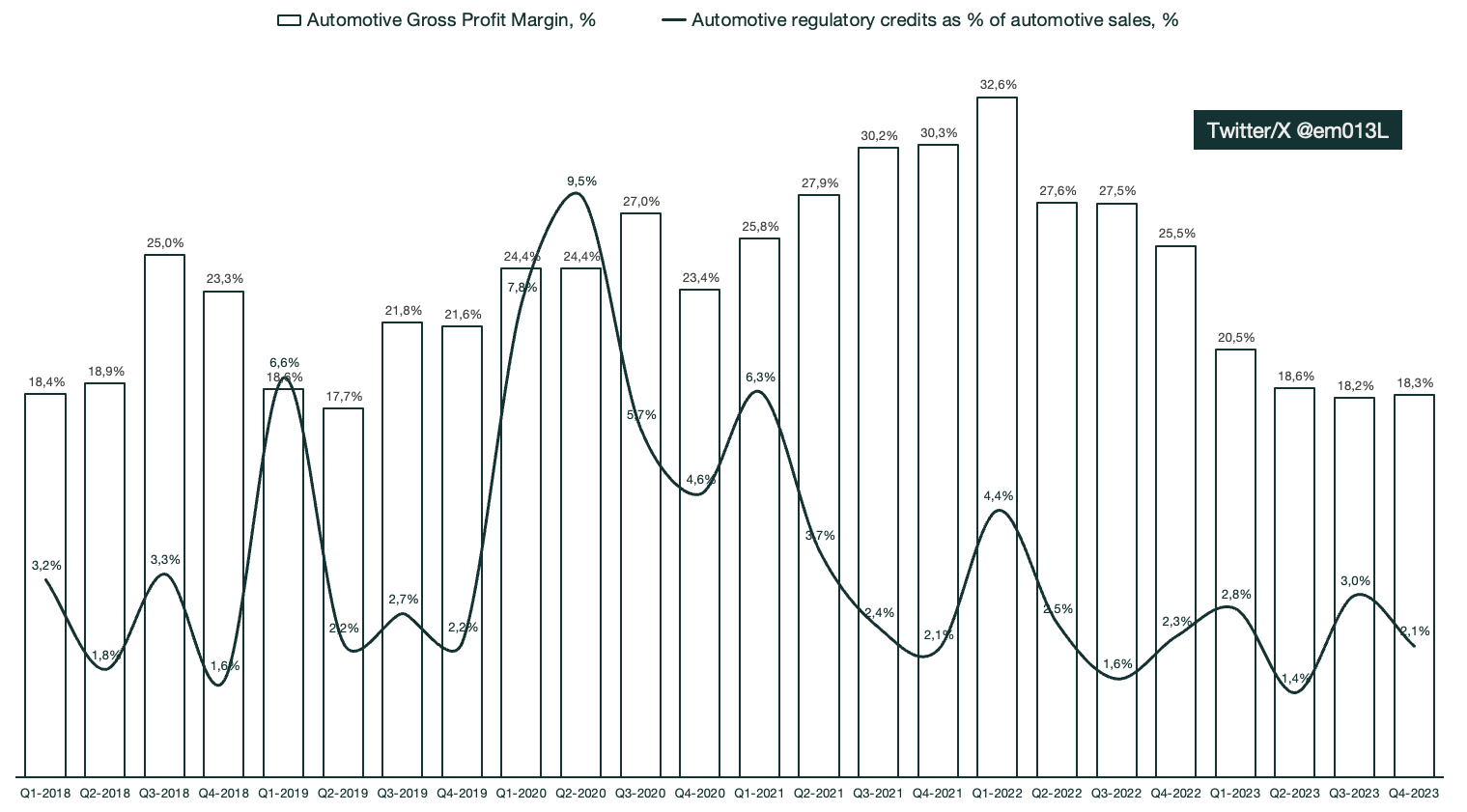

I selected to not embrace regulatory credit in my projections, as it’s nonetheless troublesome to correlate them to enterprise efficiency. In idea, regulatory credit ought to increase margins or incentivize extra gross sales, however such a correlation doesn’t seem traditionally. Regulatory credit will logically enhance globally to incentivize clients to maneuver to EVs as we inch nearer to net-zero objectives. As such, they are often seen as optionality, which means we get their upside totally free exterior this valuation.

Emir Mulahalilovic X@em013L, Tesla SEC Filings

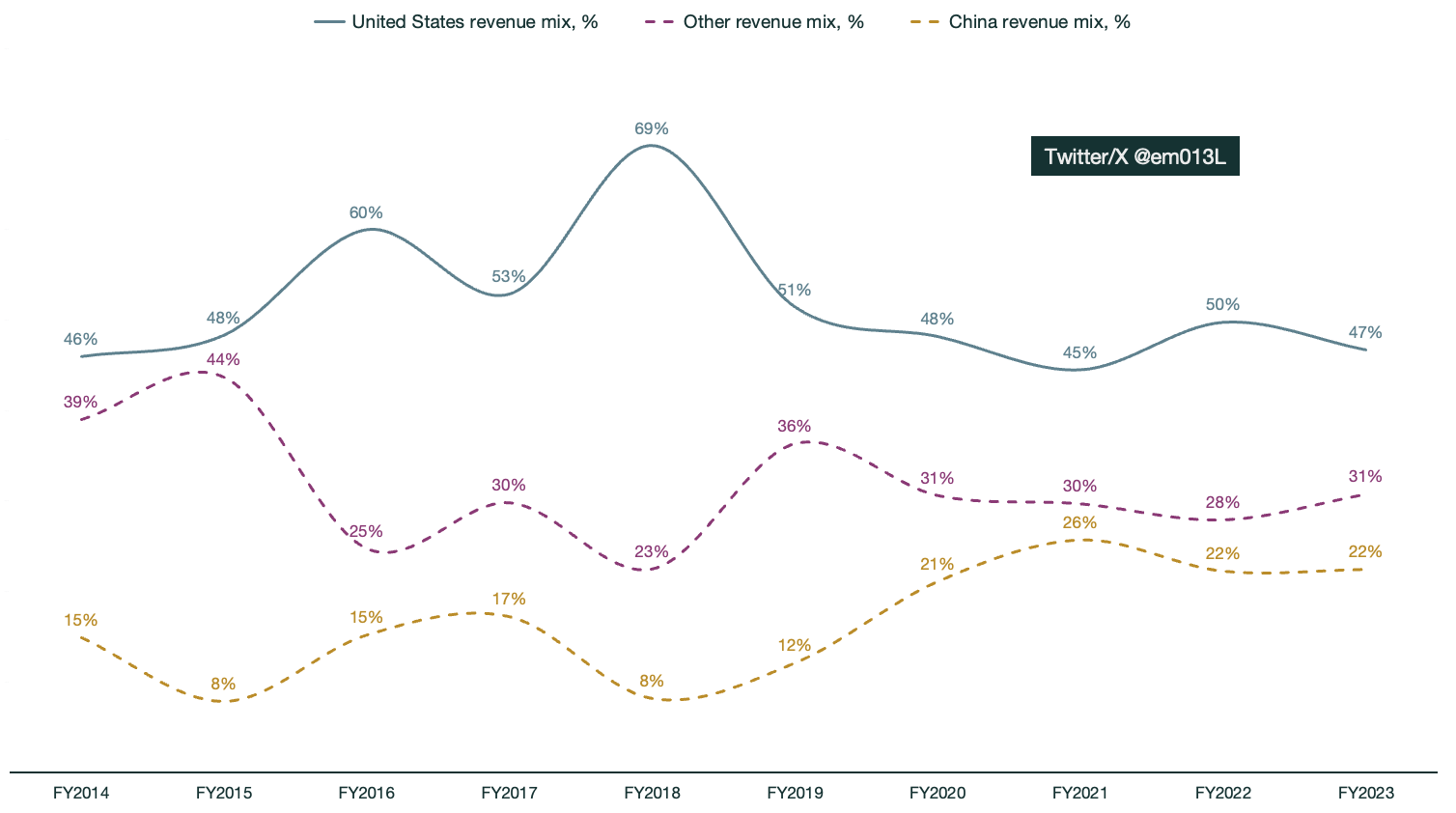

Whereas the Shanghai manufacturing unit can manufacture automobiles at greater gross margins in comparison with factories positioned within the west, I do not see China taking a bigger half within the general income combine because of fierce competitors inside the nation. Traditionally, it appears to have stagnated at ~20–25%, and whereas different revenues exterior the U.S. have been largely shipped from Shanghai, I think about the manufacturing unit in Germany will begin protecting extra of the west exterior america. I count on nations with comparatively cheaper labor to cowl for that over time, for instance, by constructing out a manufacturing unit in nations equivalent to Mexico.

Emir Mulahalilovic X@em013L, Tesla SEC filings

Companies, excluding Robotaxi and robotics

I’ve formulated the companies section to be made up primarily of full self-driving (FSD) and automobile servicing revenues. I venture this section to account for ~20% of Tesla’s general earnings earlier than curiosity and taxes (EBIT).

Moreover, I particularly selected to not embrace the potential Robotaxi and robotics segments, though they’re anticipated to be very vital for Tesla. This was performed for 2 most important causes:

- The optionality of not assigning them worth

- Unproven industries make it troublesome to venture precisely.

The principle driver on this section is FSD, and earlier than we will begin projecting numbers, we have to make a number of assumptions.

- I assume that on common, a subscription life cycle is ~5 years, i.e., the anticipated size of a buyer proudly owning the identical automobile. Which means that I’ll path subscription revenues on a 5-year foundation.

- The subsequent assumption is that I’ll exclude one-time purchases of FSD and solely use subscription revenues, for the sake of simplifying the mannequin. This begins at $99 for 2024 and 2025, ramping up slowly till reaching $399 in 2033.

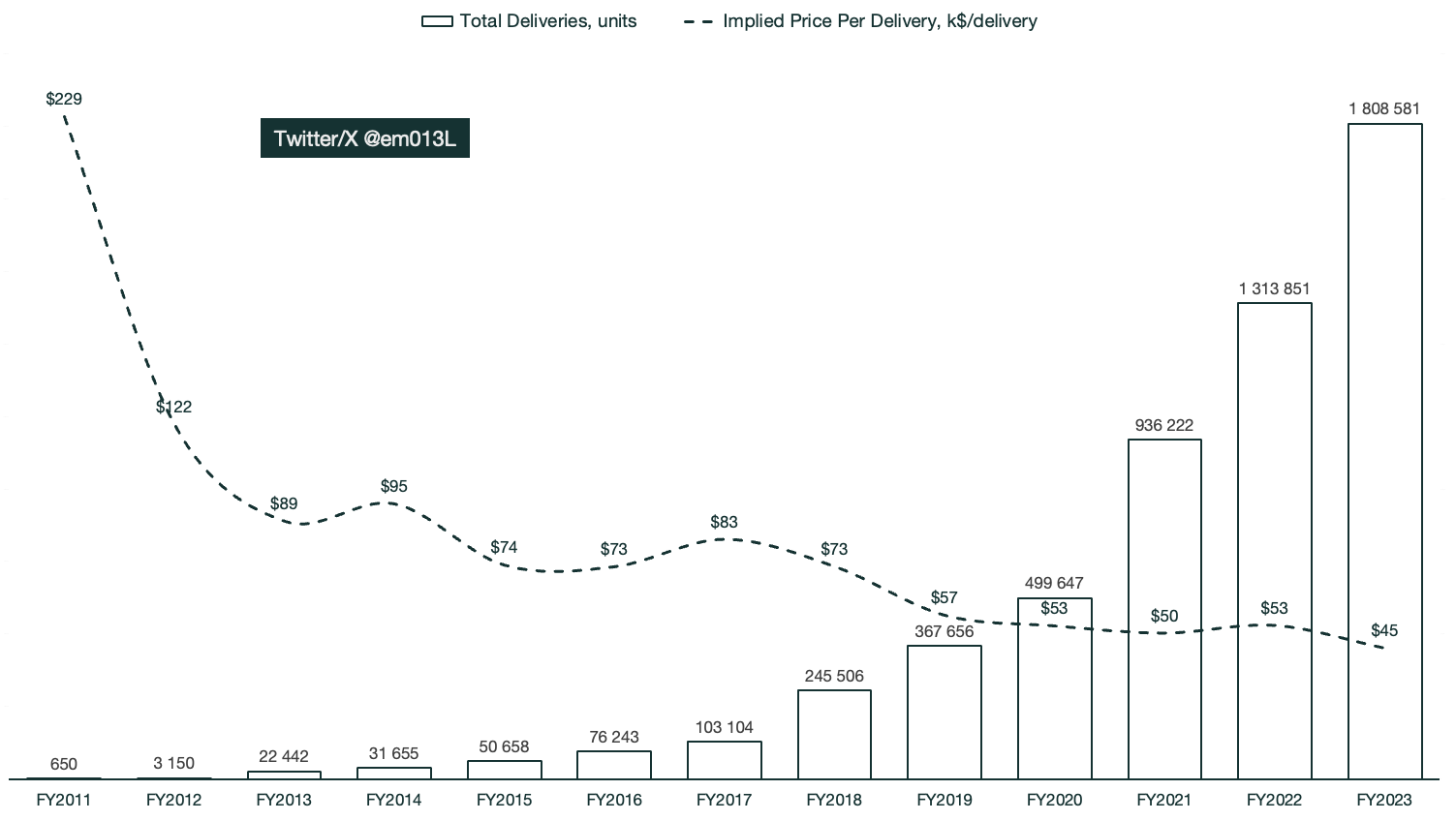

To get an understanding of the variety of automobiles to extrapolate FSD adoption charges from, I’ll assume a $45,000 common gross sales value per automobile. That’s equal to the present implied gross sales value per automobile. Attributable to our not but realizing the complete extent of the automobile lineup Tesla will carry via 2033, I selected to maintain it at $45,000. There are extra components that have an effect on common gross sales value in a direct-to-consumer mannequin, which Tesla has, particularly cyclicality, inflation, model fairness, and so forth.

Emir Mulahalilovic X@em013L, Tesla SEC Filings

The above assumptions make us arrive at ~13.5 million automobiles delivered in 2033. Hefty from at present’s place, however not unreasonable.

The adoption price is a bit difficult, however we all know that FSD is a significant purpose for Tesla and maybe the primary focus for the approaching annual intervals. CEO Elon Musk stated the next within the Q1 2024 earnings call:

However actually, the best way to think about Tesla is sort of totally by way of fixing autonomy and with the ability to activate that autonomy for a huge fleet. And I feel it is perhaps the largest asset worth appreciation historical past when that day occurs when you are able to do unsupervised full self-driving.

With this in thoughts, we all know {that a} world rollout is especially a difficulty of regulation. I ramp the adoption from 7% in 2024 as much as 25% in 2033. I don’t think about licensing FSD, offering even additional optionality within the valuation.

We do not have a lot readability by way of margins but, however we do know that the neural community coaching is heavy on capital expenditures. I’ve likened the working margins to these of a well-run software program enterprise, aiming for 27% in 2033 from a place to begin of seven% in 2024.

As for automobile servicing, I venture that it’s going to scale up by way of revenues as a proportion of the delivered automobiles. I’ve set working margins at an trade normal vary, from 8% to 12% in 2033, as they develop extra environment friendly in producing spare elements and performing servicing.

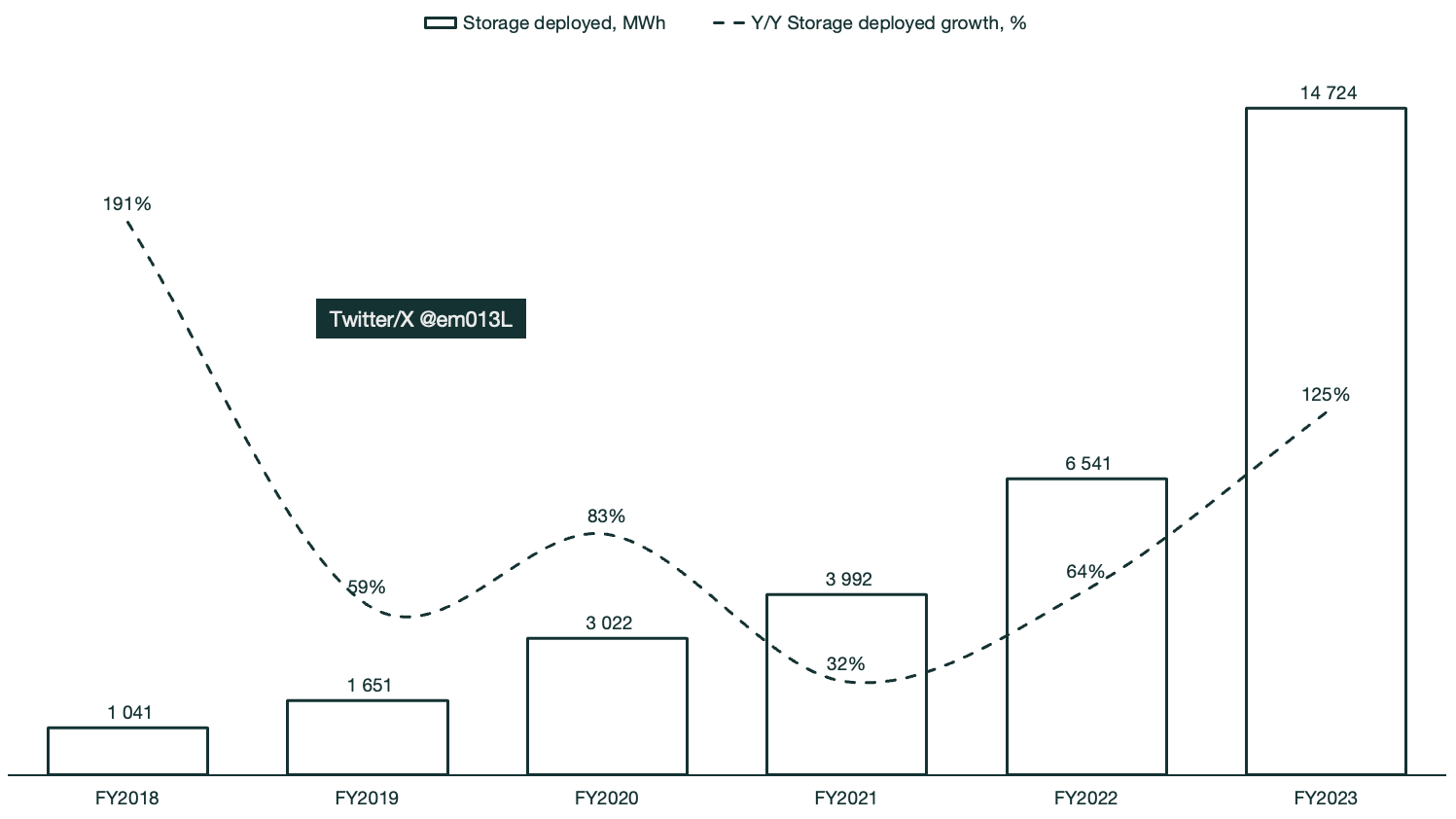

Power, excluding Supercharger community

The power section is probably the most worthwhile amongst Tesla’s totally different companies. Regardless of this, we now have surprisingly little perception into the metrics and key efficiency indicators that encompass it. Tesla shares storage and photo voltaic deployment metrics in megawatt hours and megawatts, however there isn’t any additional breakdown between these two. We have no idea the granular breakdown of what it prices Tesla to deploy these, and as such, we now have to generalize our assumptions till we acquire readability on the matter.

Photo voltaic has remained stagnant over a six-year interval; it is also notably lacking from Tesla’s Q1 2024 earnings presentation. Tesla deployed 326 megawatts of photo voltaic in 2018, notably greater than 223 megawatts in 2023. Sadly, the earnings name didn’t give us a lot readability into what Tesla plans for the longer term with photo voltaic. I additionally famous a lower in photo voltaic power techniques on the stability sheet.

Tesla’s focus appears to as an alternative be on power storage techniques. Power storage techniques have grown at a speedy clip whereas additionally sustaining wholesome margins. What was a big shock was yet one more forecast of robust progress by Tesla of their Q1 2024 earnings name:

We count on the power storage deployments for 2024 to develop at the very least 75% greater from 2023. And accordingly, this enterprise will start contributing considerably to our general profitability.

Emir Mulahalilovic X@em013L, Tesla SEC Filings

With storage techniques as the primary driver, I forecast Tesla to develop their market share of power techniques from ~1.6% in 2023 to ~8.4% in 2033. By the forecast interval’s finish, I venture Tesla’s working margins on this section to be 23%, or, in different phrases, very worthwhile.

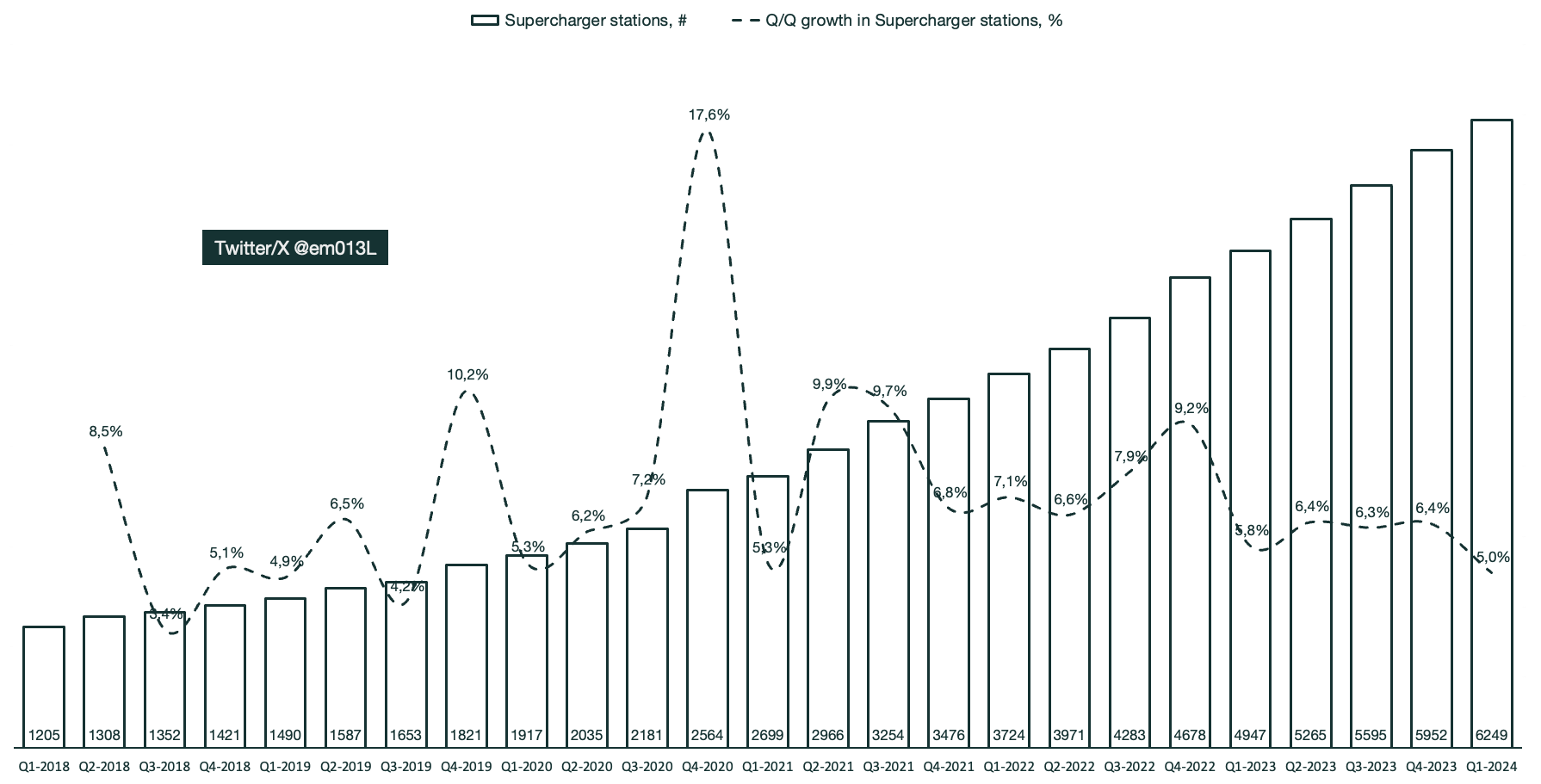

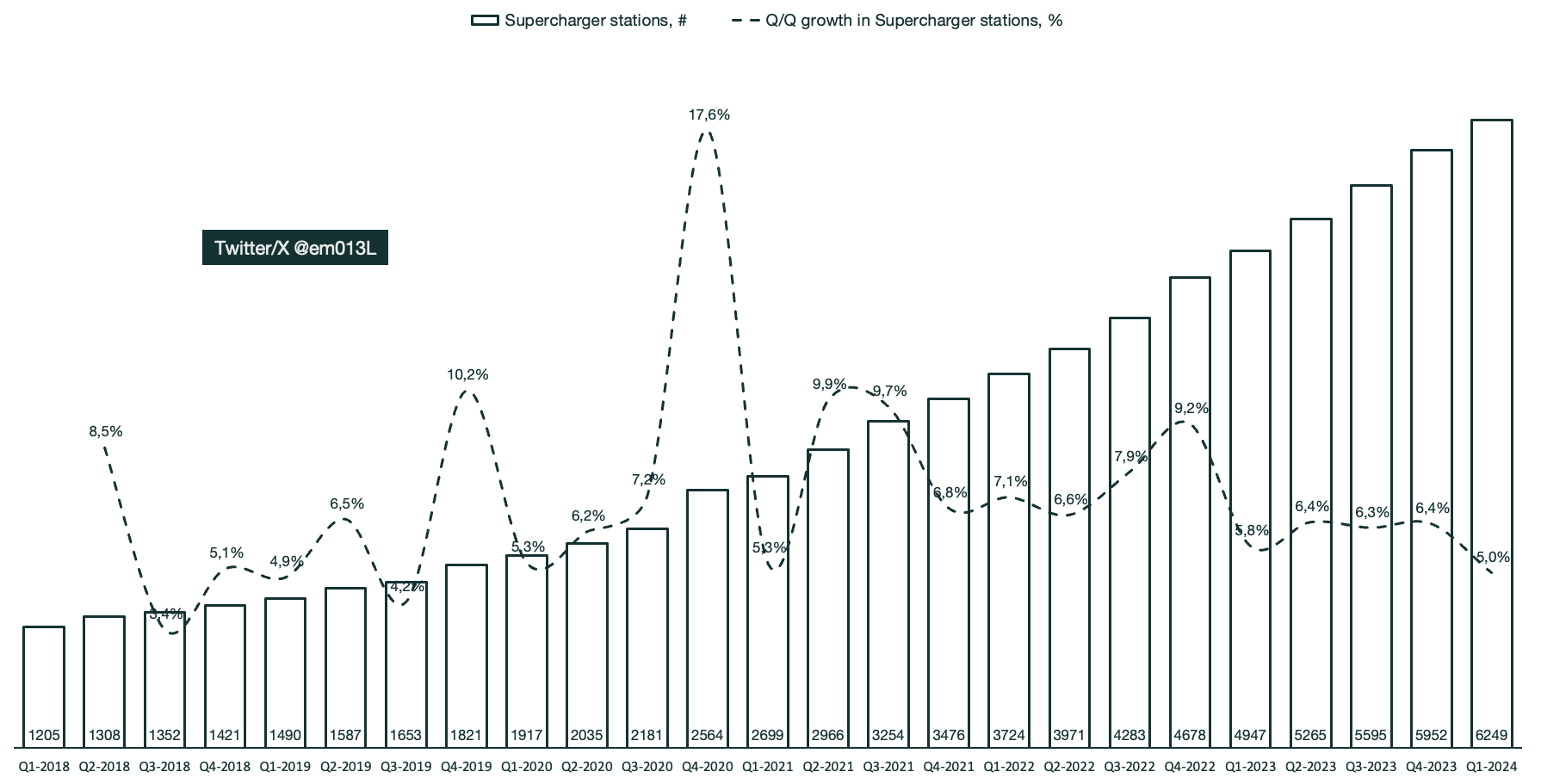

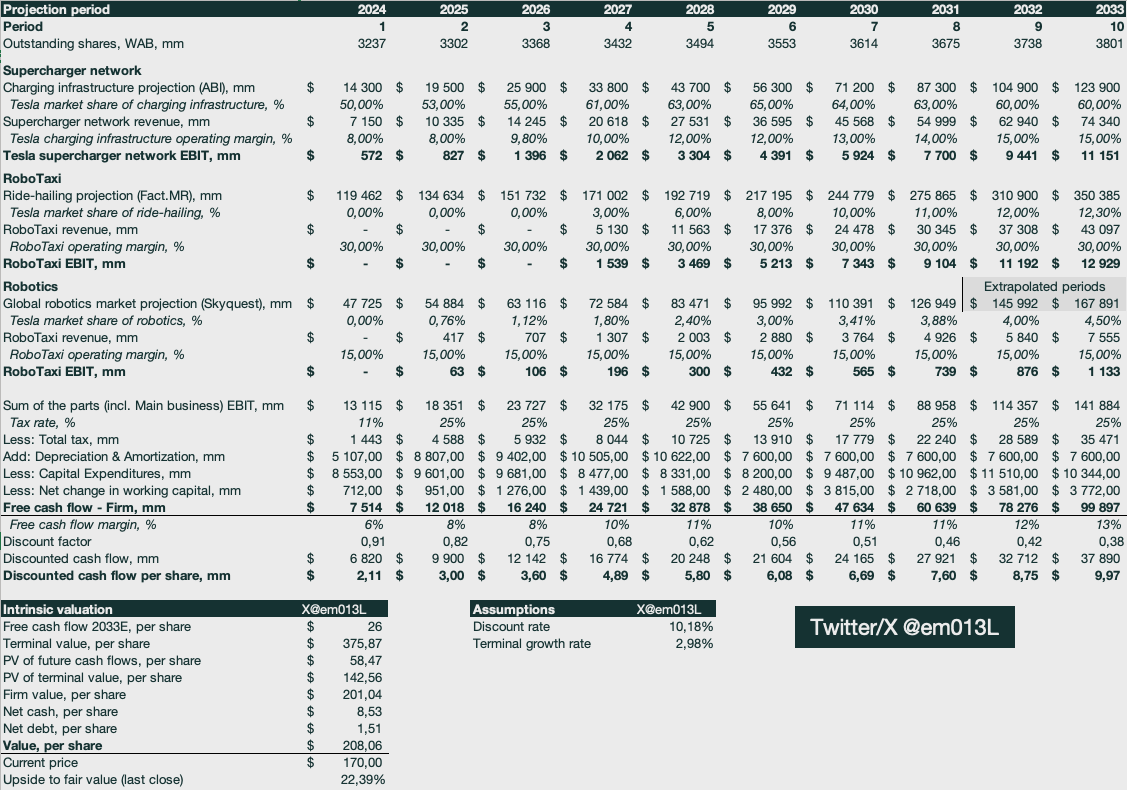

I selected to exclude the supercharger community for a similar causes I selected to not worth Robotaxi and robotics, particularly the shortage of readability and the added optionality. The supercharger community is positioned to be monopolistic, with an increasing number of producers vying to companion with Tesla for entry. The expansion and construct out of the supercharger stations have been spectacular, contemplating that they span world markets. If electrical automobiles as an entire are to develop, fixing vary anxiousness will likely be key. Excluding the supercharger community from my valuation will present a significant optionality: getting it totally free.

Emir Mulahalilovic X@em013L, Tesla SEC filings

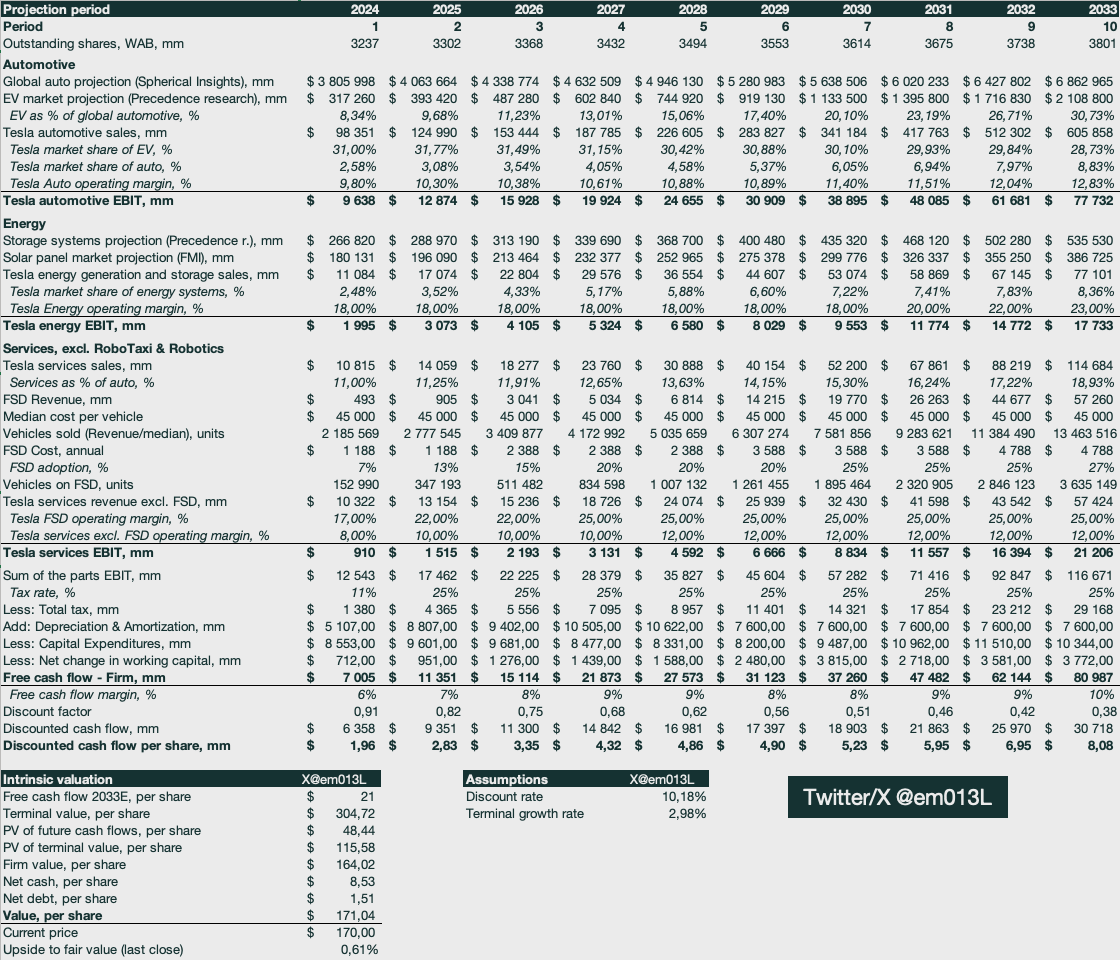

Valuation

Utilizing the figures mentioned beforehand within the article because the spine of a reduced money stream mannequin, we will begin deriving intrinsic worth.

For corporations that problem shares, I discover it vital to issue within the dilutive impact within the valuation mannequin. To attain this, every projection interval has a reduced money stream output on a per-share foundation for that interval, which is in flip used to reach at intrinsic worth. Buybacks are usually not modeled as a result of doing so would imply double-counting the free money stream used for buybacks. A extra widespread strategy is to take away stock-based compensation bills from the free money stream. Nevertheless, that may assume that the money is just not out there for leverage and, as such, is a much less correct strategy.

Emir Mulahalilovic X@em013L

An attention-grabbing issue to notice is that the mannequin utilizing my assumptions exhibits us that two-thirds of the worth of the corporate is throughout the terminal interval. This primarily implies that Tesla continues to be an organization in its early phases by way of revenues, profitability, and free money stream technology.

On the time of writing, Tesla is buying and selling across the $170 mark, which means that Tesla is at the moment pretty valued based on my projections. Nevertheless, we now have not valued the next enterprise segments, every of which could possibly be thought of a significant section for Tesla’s future:

- Robotaxi

- Robotics

- Supercharger community.

That is as an alternative thought of optionality, a possible upside to our mannequin that’s not thought of within the valuation mannequin. The query is, how a lot added worth would the optionality present? I’ve modeled estimates for these largely unproven enterprise segments utilizing market forecasts for the associated industries.

The supercharger community is probably the most tangible as a result of we now have some kind of quantity to extrapolate from. Nevertheless, the numbers are solely the entire variety of supercharger stations and connectors, with none financial metrics tied to them. Which means that we’re largely in the dead of night by way of margins and revenues for this a part of the enterprise.

Emir Mulahalilovic X@em013L, Tesla SEC Filings

The variety of stations is rising steadily, prone to match demand. We do know that Tesla is vying to create a monopoly of charging stations, already having many main automotive producers consign themselves to utilizing the Tesla normal for charging. I might not be shocked to see accelerated progress as we strategy bigger electrical automobile adoption.

There are some publicly traded charging community corporations, however these are both unprofitable, inefficient in comparison with Tesla, or on a unique scale. Because of this, I’ve gone with an working margin of 8%, rising to fifteen% by 2033. The margin additionally displays the licensing of the expertise.

As for the Robotaxi section, I went with an strategy that likens it to the ride-hailing trade. I’ve used world ride-hailing market projections as the premise of my income assumptions. From there, I’ve initiated Tesla absorbing market share by providing their very own ride-hailing companies in addition to partnering with different main gamers. I count on the margins to be excessive because of licensing and partnering, in addition to the corporate receiving the complete fare price excluding working prices. As well as, Tesla is not going to have to personal the automobiles exterior their very own ride-hailing service. I venture Tesla to have 12.3% market share of ride-hailing revenues in 2033 with a 30% working margin. Additionally word that I don’t begin Robotaxi revenues till 2027, which is my guess at regulatory approval.

Robotics is an attention-grabbing and deep section with many rivals, primarily from Japan. I can not at the moment see Tesla reaching something past 5% market share of this area by 2033, because the market as an entire encompasses far more than solely humanoid robotics. Surprisingly, the Tesla robotic seems to be operational in inner testing and anticipated to roll out to clients in 2025, based on Elon Musk throughout the Q4 2024 earnings call:

we do suppose we can have Optimus in restricted manufacturing within the pure manufacturing unit itself, doing helpful duties earlier than the top of this yr. After which I feel we might be able to promote it externally by the top of subsequent yr. These are simply guesses.

Emir Mulahalilovic X@em013L

I’ve not touched on reinvestment whereas including these segments, because the numbers are already extrapolating historic figures that embrace Tesla spending capital in the direction of these objectives. Combining these estimates within the sum-of-the-parts valuation mannequin raises the honest worth from ~$170 to ~$210 per share, or ~22.5%.

Abstract

Breaking down the totally different enterprise segments inside Tesla permits for a greater understanding of the place the worth comes from. Intrinsic worth from my sum-of-the-parts DCF mannequin exhibits that Tesla is at the moment buying and selling at honest worth, regardless of intentionally not together with Robotaxi, robotics, or the supercharger community in my mannequin.

By not together with the segments in my valuation, I open up the likelihood for optionality. Which means that the efficiency of the aforementioned segments is actually free after I buy Tesla inventory at present buying and selling ranges. With this in thoughts, I assign Tesla, Inc. inventory a purchase ranking.