choness

Introduction

Earlier this 12 months, I offered the one utility inventory in my dividend development portfolio, Duke Power (DUK). I did not do it as a result of I disliked the corporate however due to my view on rates of interest and inflation.

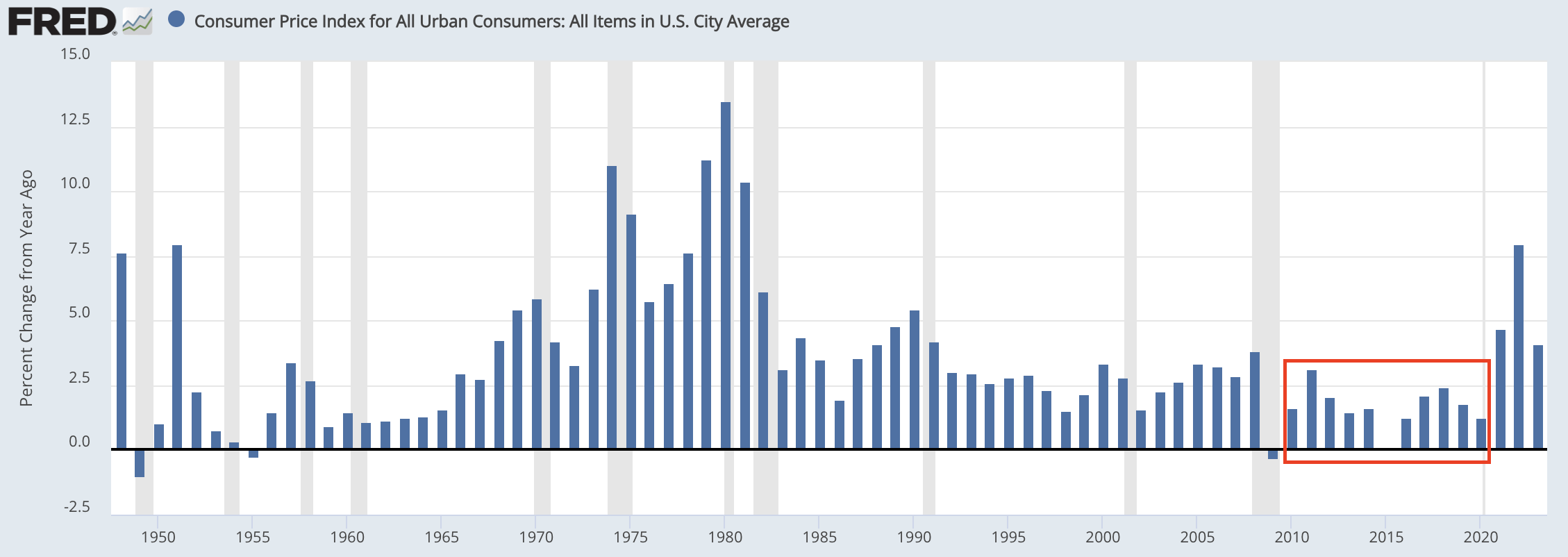

I am within the camp that believes in extended elevated inflation and rates of interest – at the very least in comparison with the favorable danger atmosphere between the Nice Monetary Disaster and 2021.

Throughout this era, inflation was subdued, supported by secular tailwinds, together with low cost vitality costs, robust globalization, and favorable labor market dynamics – amongst different elements.

Federal Reserve Financial institution of St. Louis

Now, lots of these elements are reversing, together with the availability tailwinds from the fossil gas trade.

Therefore, after the market anticipated the Fed to chop charges six instances this 12 months, we’re now in a scenario the place market contributors need to re-evaluate the scenario, as new indicators level at continued headwinds for the battle in opposition to inflation.

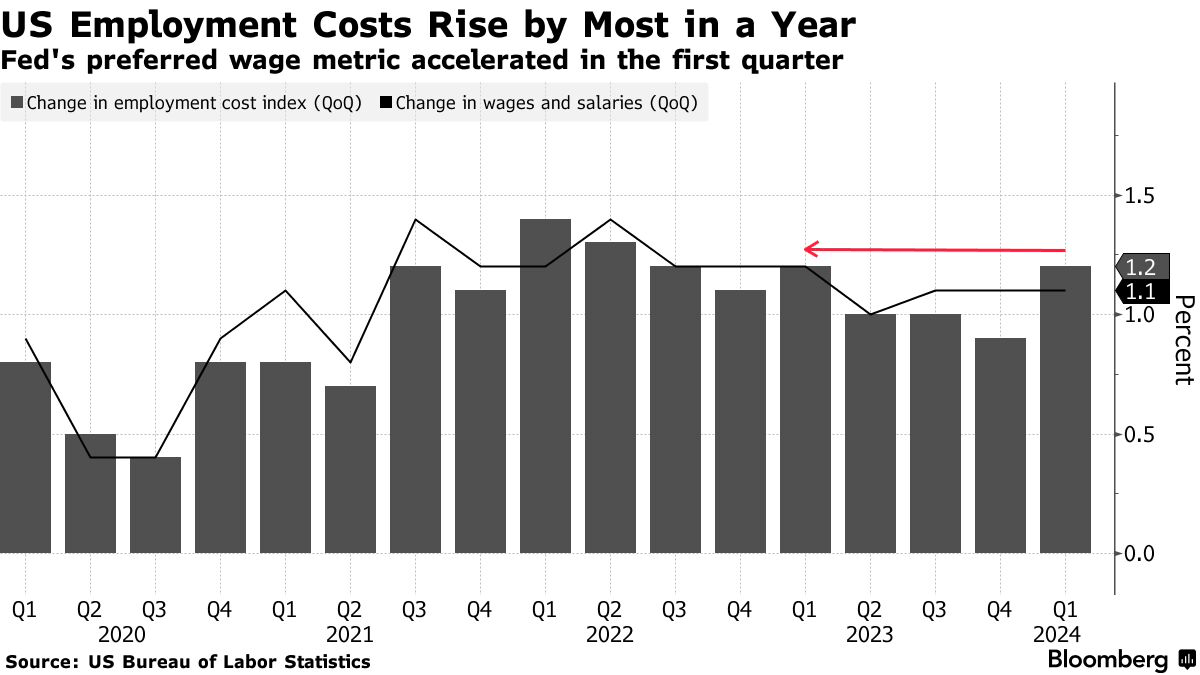

For instance, minutes earlier than I began writing this text, Bloomberg reported that the employment price index, which is a broad gauge of U.S. labor prices, had are available greater than anticipated. It is up 1.2%, essentially the most in a 12 months after rising by 0.9% on the finish of 2023.

Bloomberg

Therefore, I consider this gentleman is hitting the nail on the pinnacle:

“This is a challenging print for the Fed,” Robert Sockin, senior world economist at Citigroup Inc., stated on Bloomberg Tv. “Coming in at 1.2 is just evidence that the inflation data, the wage growth data, is moving in the wrong direction to be consistent with their target.” – Bloomberg

Typically talking, that is dangerous information for utilities, which is why I opted for yield performs in different areas, together with the rather more cyclical vitality sector.

Utilities carry out higher when inflation is low.

- They’ve restricted pricing energy attributable to oversight from Public Service Commissions, which generally observe a cost-based strategy.

- Most regulated utilities are investing billions within the vitality transition and are, typically talking, usually sitting on lots of debt. Decrease charges make it simpler to take care of a wholesome steadiness sheet.

Nonetheless, this text is a couple of utility firm I’ve began to love lots. Actually, I owned it in 2020 earlier than I restructured my dividend development portfolio. Not holding it again then was a mistake.

That firm is the American Electrical Energy Firm (NASDAQ:AEP), an enormous with a $45 billion market cap.

My most up-to-date article on this firm was written in November once I went with the title “A Path To Over 11% Annual Returns – Why 4.5%-Yielding American Electric Power Is Attractive.”

Since then, shares have been up 12.6%, barely beating the 12.0% return of the S&P 500.

Whereas I am not extraordinarily optimistic concerning the utility sector, AEP has discovered how one can constantly generate elevated returns, backed by robust EPS development, a strong steadiness sheet, and a well-covered 4% dividend yield.

On this article, I will stroll you thru the main points utilizing its just-released quarterly earnings.

So, let’s get to it!

Why 1Q24 Was Such A Success For AEP

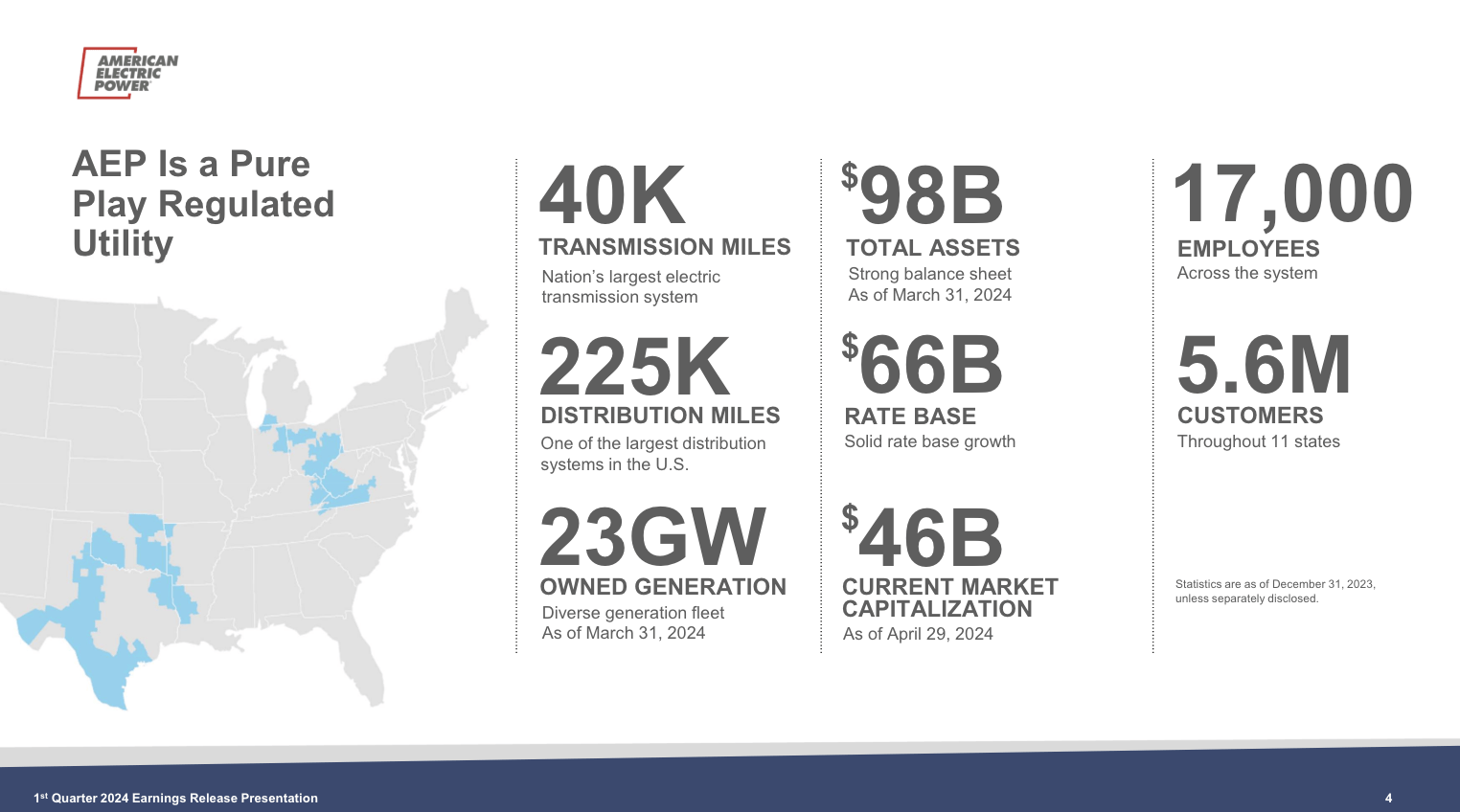

American Electrical Energy is a huge. The corporate has the biggest distribution system in the US, together with 225 thousand distribution miles. It additionally has the biggest community of transmission traces and near $100 billion in complete belongings.

This asset base supplies providers for five.6 million prospects in 11 states, together with Texas, Oklahoma, West Virginia, Virginia, and Ohio.

American Electrical Energy

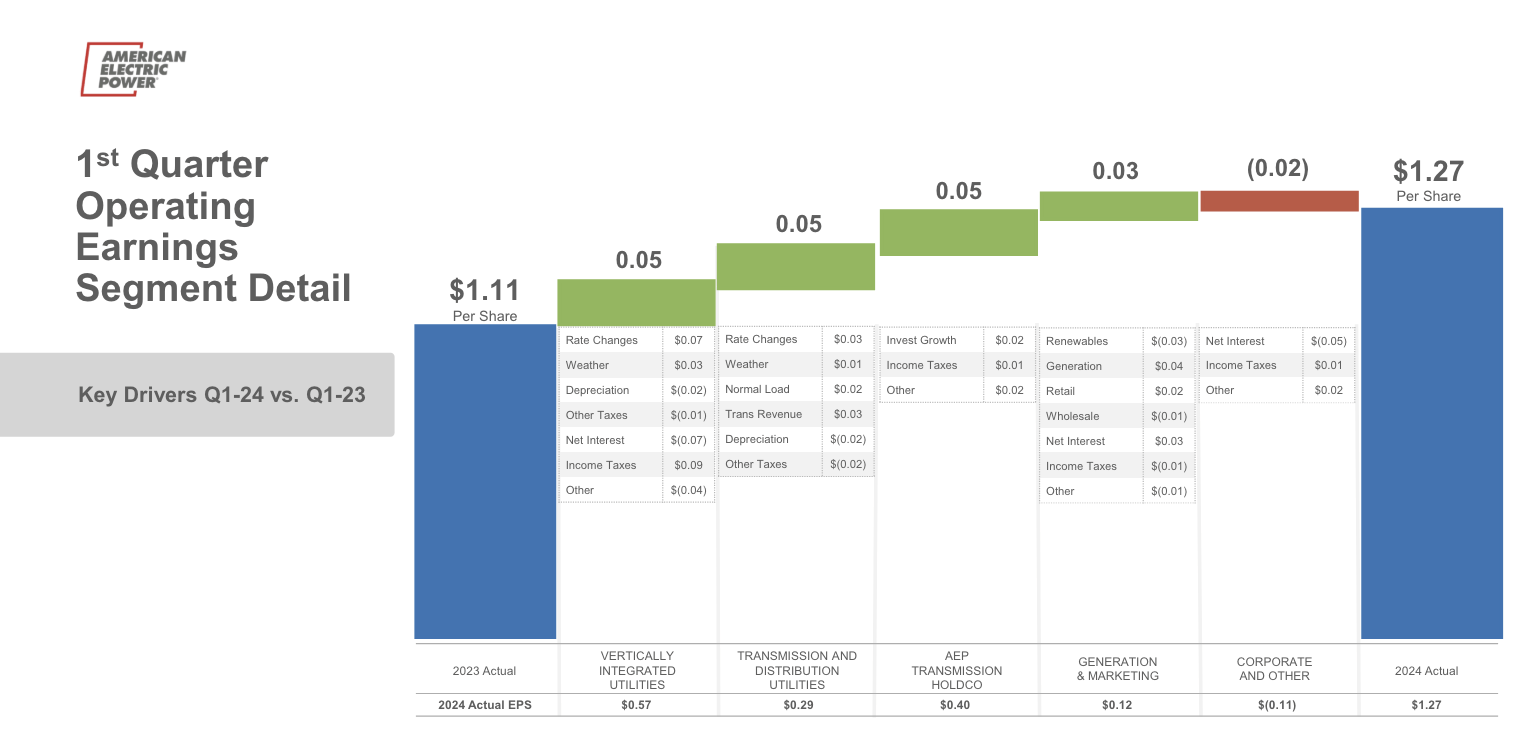

In its just-released quarter, the corporate generated working earnings of $1.27 per share, which represents a $0.16 improve in comparison with the prior-year quarter.

As we are able to see beneath, this improve was pushed by a variety of elements, together with a one-time constructive adjustment associated to the remeasurement of a regulatory legal responsibility for extra deferred taxes, as suggested by the IRS.

Furthermore, working earnings had been impacted by fee modifications and favorable climate (a $0.57 affect).

American Electrical Energy

Including to that, the corporate famous a notable acceleration in general retail load, particularly within the industrial sector, boosted by elevated demand from information facilities.

I’ve heard these feedback from numerous utilities and vitality suppliers. I added emphasis to the quote beneath.

A few nice examples of latest industrial commitments could be evidenced by final week’s bulletins from each Amazon Internet Companies and Google to construct massive information facilities in I&M’s Northern Indiana service territory.

At AEP, we now have the largest transmission system in the US with a high-voltage spine within the Midwest. We anticipate extra transmission funding prospects pushed by this information middle development, particularly in substations and buyer connections. – AEP 1Q24 Earnings Name

So as to add some colour, the industrial load noticed a ten.5% improve, pushed by the expansion of AI and different applied sciences.

In the meantime, the economic load remained secure regardless of nationwide manufacturing softness, with elevated exercise witnessed in particular manufacturing sectors akin to plastics, tires, and paper.

The corporate additionally used “my” higher-for-longer phrase (emphasis added):

We’re holding a detailed eye on our industrial prospects, given the upper rates of interest for longer atmosphere. Nevertheless, the variety of massive new masses anticipated to return on-line within the subsequent 2 years, supplies us with confidence that demand will stay regular within the face of any financial challenges for our present prospects. – AEP 1Q24 Earnings Name

So, what does this imply for shareholders?

American Electrical Energy’s Path To +10% Annual Returns

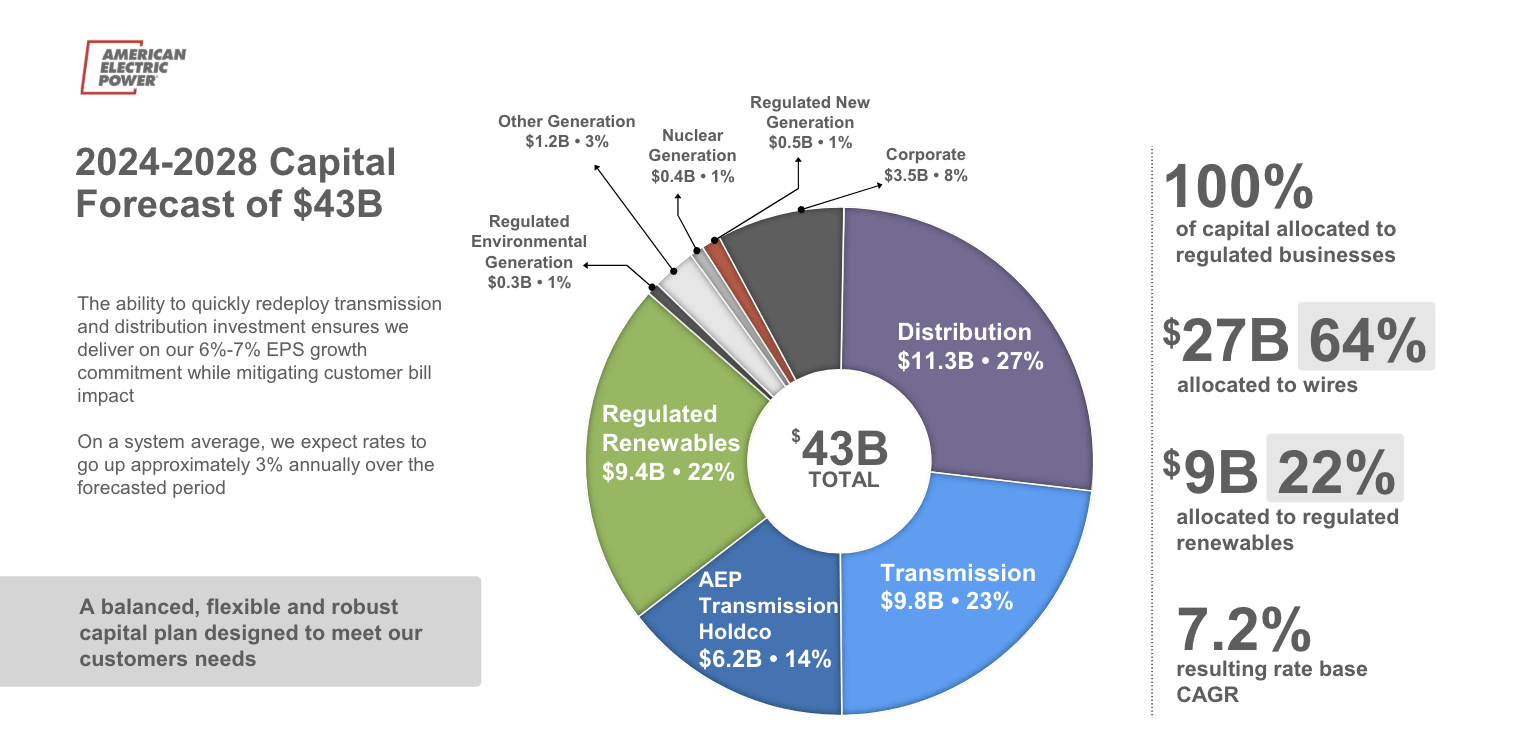

Along with investing within the capability for secular development, AEP is transitioning to web zero, which comes with billions in required capital.

Throughout its 1Q24 name, the corporate famous it’s advancing its 5-year, $9.4 billion regulated renewable capital plan, with $6.6 billion already accredited by state commissions.

These investments are a part of a $43 billion five-year plan, which consists of even greater investments in distribution and transmission capabilities.

American Electrical Energy

The excellent news is that the corporate isn’t anticipated to run into any steadiness sheet points – not even on this atmosphere.

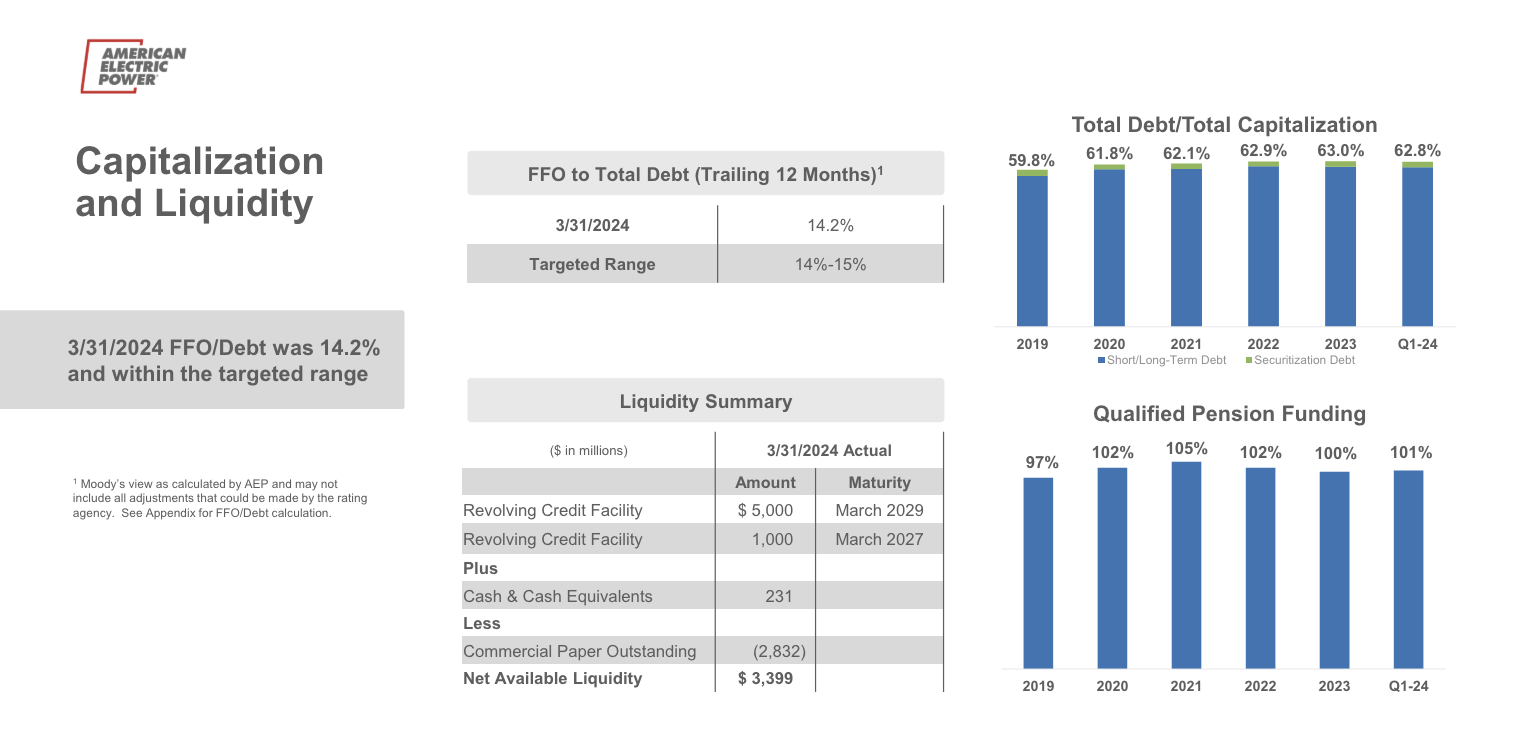

- The corporate has an FFO-to-debt ratio of 14.2%, which is 100 foundation factors greater in comparison with the top of 2023. The upper the higher, because it means it has extra funds from operations to cowl its debt. It is also properly inside the firm’s 14-15% goal vary. The corporate believes it might preserve the ratio in its goal vary within the years forward.

- The corporate has well-covered pension funding and $3.4 billion in liquidity, together with a $6 billion credit score facility that was just lately boosted by $1 billion.

Even higher information is that these investments are anticipated to end in a 7.2% annual base fee development, a part of the corporate’s plan to develop its earnings per share by 6-7% per 12 months throughout this era.

American Electrical Energy

Going again to the corporate’s outlook, it’s assured in its potential to develop EPS by 6-7% on a long-term foundation.

We stay dedicated to our long-term development fee of 6% to 7% and FFO to debt solidly within the 14% to fifteen% vary. – AEP 1Q24 Earnings Name

This bodes properly for shareholders. In any case, assuming its valuation doesn’t change, we are able to anticipate at the very least 6% annual returns.

Keep in mind that annual returns come from a mixture of EPS development, valuation modifications, and dividends. The inventory value is EPS X the P/E a number of. These two numbers affect capital good points. Dividends are revenue, which completes the whole return image (capital good points + revenue).

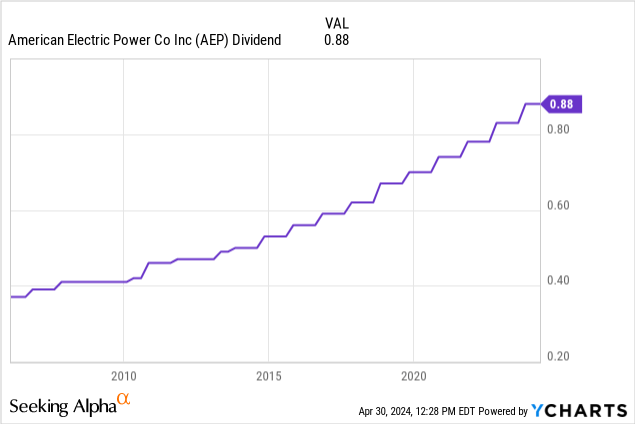

Within the case of AEP, we’re coping with a $0.88 per share per quarter dividend. This interprets to a yield of 4.0%.

This dividend comes with a low-60% payout ratio, a 5.8% five-year CAGR, and 14 consecutive annual hikes.

Assuming the corporate achieves the decrease certain of its EPS development fee, we get a ten% annual return primarily based on an unchanged valuation (6% EPS development + 4% dividends).

That might be a fantastic end result, as producing 10% with any anti-cyclical funding permits traders to construct lots of wealth with out shedding sleep.

It will even be higher than the 7.3% annual return traders have loved since January 2004.

Furthermore, it helps that analysts agree.

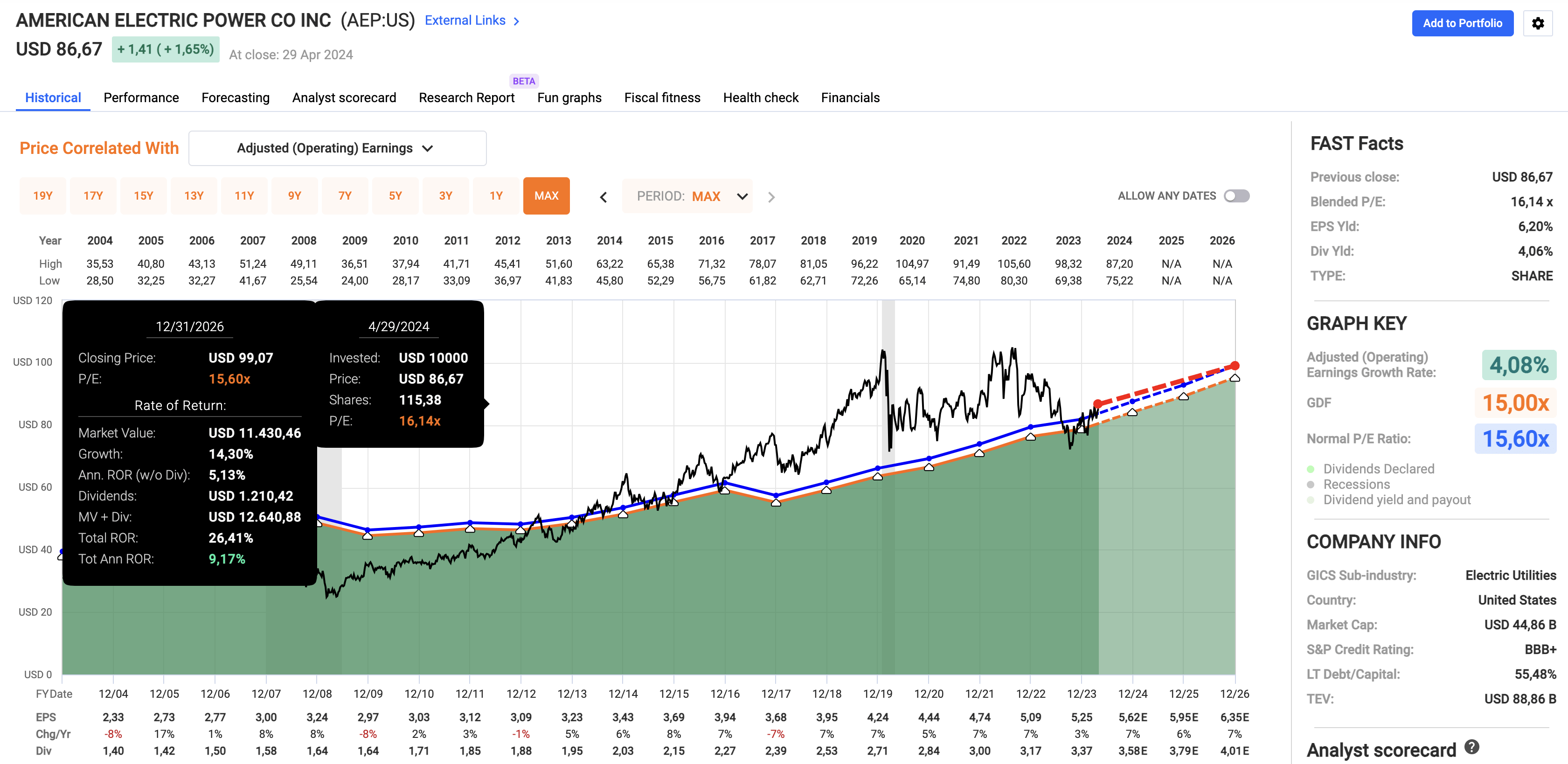

Utilizing the FactSet information within the chart beneath, we see that analysts anticipate between 6-7% annual EPS development by way of at the very least 2026.

Furthermore, AEP presently trades at a blended P/E ratio of 16.2x, which is simply barely above its long-term normalized P/E ratio of 15.6x (the blue line).

FAST Graphs

Therefore, combining EPS development expectations, its 4% yield, and its normalized valuation, we get a base case of 9% annual EPS development.

Evidently, this return could be impacted by market fluctuations, surprising fee modifications, and financial elements.

Nonetheless, and all issues thought-about, I consider AEP stays top-of-the-line utilities in the marketplace, because of its potential to take care of elevated capital necessities and financial challenges whereas capturing development in secular tendencies like information middle electrical energy demand.

If I had a extra conservative funding profile, I’d be a gradual purchaser of AEP shares.

Takeaway

American Electrical Energy presents a compelling case for traders looking for secure returns amidst financial uncertainties.

With a strong infrastructure, strategic investments in renewable vitality, and a strong steadiness sheet, AEP is positioned for regular development.

Regardless of market fluctuations, AEP’s constant earnings per share development, supported by a wholesome dividend yield, presents the potential for over 10% annual returns.

In the meantime, analysts undertaking continued EPS development, reinforcing AEP’s long-term outlook of 6-7% annual EPS development.

Professionals & Cons

Professionals:

- Regular Development: AEP’s constant EPS development, backed by strategic investments in renewable vitality, presents traders secure returns even in unsure financial climates.

- Stable Infrastructure: With the biggest distribution system within the U.S. and substantial belongings, AEP is well-positioned to satisfy rising vitality calls for.

- Wholesome Steadiness Sheet: AEP’s robust FFO-to-debt ratio and powerful liquidity profile present confidence in its potential to fund future development initiatives with out compromising monetary stability.

- Enticing Dividend: AEP’s 4% dividend yield, supported by a low payout ratio and a historical past of consecutive annual hikes, supplies traders with a gradual revenue stream.

- Favorable Outlook: Analysts undertaking continued EPS development and AEP’s present valuation suggests potential for enticing returns in the long run.

Cons:

- Market Fluctuations: Like all funding, AEP’s inventory value could be affected by market volatility, probably impacting short-term returns.

- Regulatory Oversight: As a regulated utility, AEP faces oversight from public service commissions, which can restrict pricing energy and require adherence to cost-based approaches.

- Financial Components: Financial downturns or surprising fee modifications might affect AEP’s efficiency and shareholder returns.

- Sector Sensitivity: The utility sector’s efficiency is commonly tied to rates of interest and inflation ranges, which can have an effect on investor sentiment in direction of AEP.