Douglas Rissing/iStock via Getty Images

The Axon Enterprise Investment Thesis

Almost a year ago, in late May 2023, I wrote my first article about Axon Enterprise, Inc. (NASDAQ:AXON). Then, as now, I was enthusiastic about the business model, which binds perfectly customers into the ecosystem through high switching costs and outstanding functionality.

Plus, I like the fact that they have a mission to save lives and make the world a better place. And in addition, Axon also has strong barriers to entry that protect its revenue, such as security certifications like FedRAMP High Classification.

My only criticism at the time was that the valuation was not cheap, but the business model, growth opportunities and management execution were excellent. Therefore, my rating at that time was “Hold,” which turned out to be too low as the S&P 500 (SPY) returned only 19% over that period and Axon returned an outstanding 61%.

Axon was the classic case of a company that turned out to be worth its seemingly high price tag. Since I believe that the quality of the company and its growth opportunities have continued to improve since last year, I am upgrading my rating this time and will explain in the following paragraphs why I believe that there will be an earnings beat next week.

Axon’s Earnings Surprises

Seeking Alpha Earnings Tab

Over the past 2 years, Axon has beaten revenue estimates 8 times and EPS estimates 7 out of 8 times. And on year-end EPS, Axon has only missed three times in the past 12 years, as you can see in the chart above, and has beaten every time since December 2019.

Therefore, it can be assumed that the estimates tend to be conservative, and therefore the probability of a beat is higher than the probability of a miss. However, you do not want to rely solely on these statistics if you are expecting an earnings beat.

Another reason is that Taser gross margins were down last quarter due to what, we hope, was a one-time warranty cost for the Taser 7. But they should return to their former strength this quarter.

Axon Investor Presentation

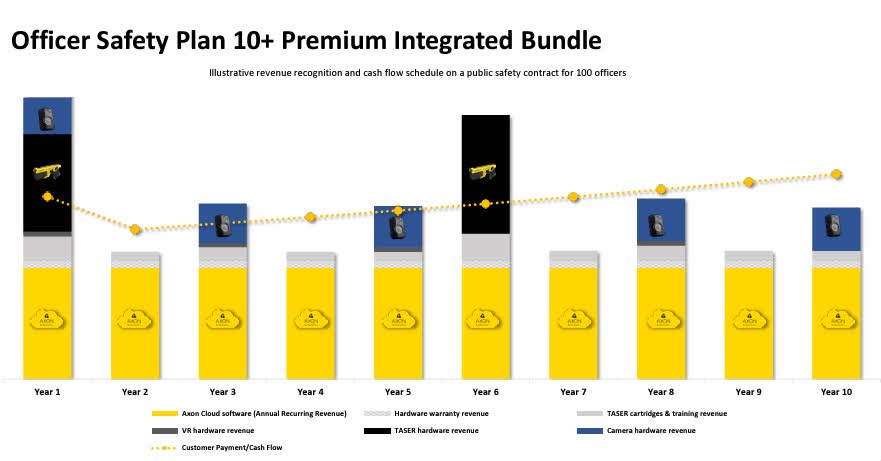

I also believe that revenue recognition of future contracted revenue will be closer to the upper end of the 15% to 25% range. Because even though the replacement intervals are supposed to be a little longer, customers seem to be switching to the Taser 10. And more hardware sales usually means that you are getting closer to the 25% mark of the range. Normally, a 5-year interval as shown above seems to be the norm for Taser, but the Taser 10 seems to be so good that customers want to upgrade sooner.

Axon Investor Presentation

And the proportion of subscription revenue continues to grow, which is good for margins because it is more cost effective. In fact, the 44% CAGR in ARR since 2019 has undoubtedly been a big part of Axon’s success over the past few years.

Axon Investor Presentation

The decision to offer real-time monitoring, digital evidence management, and faster, partially automated reporting was a great move by the management team, perfectly anticipating the future and the possibilities of AI, big data, and the cloud. And all of this has increased security and saved time and money. A huge win-win for customers and for Axon.

What makes Axon’s suite of products so attractive is the way they work together. Both the cameras and the Tasers capture evidence and data that is then analyzed and evaluated, some automatically and in real time. In addition, the Watch Me button provides a second set of eyes to help analyze dangerous and unclear situations.

Axon’s Growth Opportunities

In February 2024, Axon acquired Fusus, a live video, data and sensor company, which is expected to be accretive to TAM and earnings in a relatively short period of time. Much more interesting, but less talked about at the moment, is the acquisition of Sky Hero. Sky Hero is probably one of the best drone manufacturers right now, and this could be a very strong addition to the drone and robotics space in the long term.

Axon Investor Presentation

Using drones and robots to make initial contact and inspect crime scenes is likely to significantly reduce casualties. And this is also one of the plans in the technology area that they want to advance robotics.

In addition, further growth is expected in VR training and data-driven learning, which are likely to be well served by generative AI. But also outside of law enforcement, there are numerous development possibilities in the commercial area. Even hospitals or normal shops can benefit from the use of bodycams to optimize operations or increase security.

Axon Investor Presentation

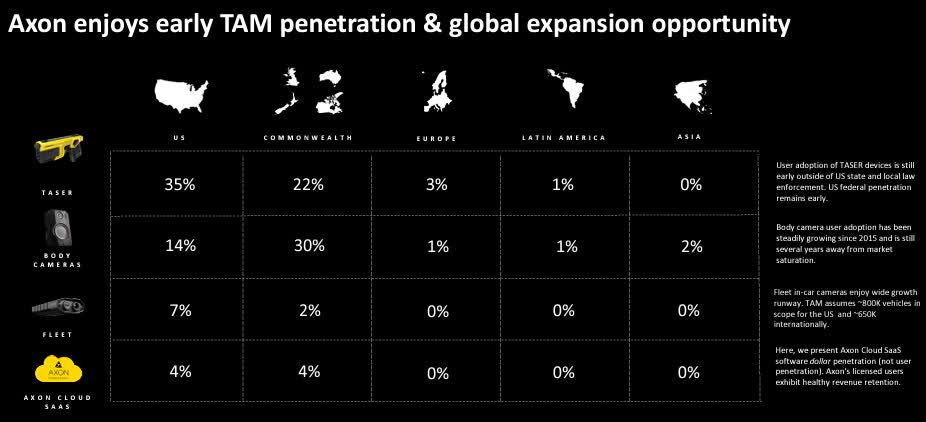

And if you look at the penetration of TAM in Europe, Latin America and Asia, there is still a large untapped market. Asia will probably be difficult because Chinese companies will probably prefer Chinese solutions, but I definitely see Europe and Latin America as markets of the future.

It is also interesting to note that the nearly 17,000 customers in the subscription model not only have contracts of 5+ years, but as mentioned in the last earnings call, many have contracts of 10 years and longer. I think that speaks volumes about Axon’s tremendous competitive advantage.

In addition, there are strong cross-selling and up-selling opportunities, as well as drones and robotics products that will be of interest to existing customers in the future.

But the biggest driver for the Americas will probably be the digital evidence services, and overseas probably the Tasers at the beginning to get customers into the ecosystem. For example, Cloud + Services revenue grew 52% in the last quarter.

Risks

One risk that was mentioned on the last earnings call that could have a big impact is the possible relocation of the headquarters. Smith & Wesson (SWBI), for example, also decided to move, and this, among other reasons, caused the stock to initially take a hit due to the associated costs, which temporarily hurt earnings.

Therefore, a move could make Axon’s stock even more volatile than it already is. But volatility also brings opportunity, as long as the costs are temporary.

Reverse DCF

Author

In my opinion, a reverse or inverse DCF is always a good way to find out what the market has priced in. And with FY23 diluted EPS of $2.31, the market is currently pricing in EPS growth of 26% per year.

The EPS growth rate over the last 5 years was 35.81% and over the last 10 years was 21.12%. Therefore, it is probably fair to say that the stock is fairly valued right now, as it is right in between these two values. Although the 75x P/E multiple seems incredibly high, what the market is pricing in is relatively realistic.

Conclusion

Axon is not as overvalued as many people think when you look at the quality of the business and the future growth opportunities. Therefore, I think it is relatively fairly valued.

I think the ecosystem with its bundles, the barriers to entry, the high switching costs, and the high switching effort, all protect sales. And Europe and the UK still offer many opportunities for growth with existing products and services. Now add in drones and robotics, and the current TAM is probably conservative.