Nongnuch Pitakkorn/iStock by way of Getty Pictures

The concepts of debtor and creditor as to what constitutes a very good time by no means coincide.” – P.G. Wodehouse.

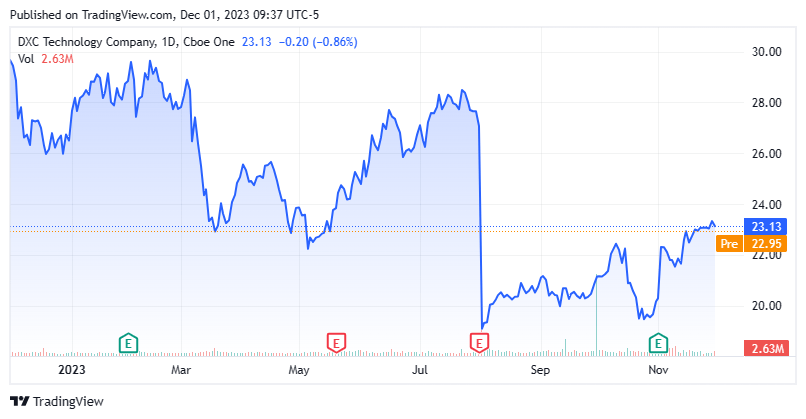

Today, we put DXC Technology Company (NYSE:DXC) within the highlight for the primary time. The inventory dropped sharply following disappointing fiscal Q1 results in August however has been on the mend recently, and fiscal second quarter numbers met expectations early in November. The shares appear cheap on a P/E basis. Where does the stock go from here? An analysis follows below.

Seeking Alpha

Company Overview:

The company is headquartered just outside of Washington, D.C. in Ashburn, VA. DXT Technology operates within two primary business divisions: Global Business Services or GBS and Global Infrastructure Services or GIS. The GIS segment provides security services, such as IT security, operations and culture for the cloud while GBS offers a portfolio of analytics services and extensive partner ecosystem that help its customers to gain rapid insights and automate operations. The stock currently trades just above $23.00 a share and sports an approximate market capitalization of $4.5 billion.

Fiscal Second Quarter Results:

November Company Presentation

The company posted its fiscal Q2 numbers on November 1st. DXC Technology had a non-GAAP profit of 70 cents a share, two pennies above expectations. Sales fell 3.6% on a year-over-year basis to $3.44 billion, in line with the consensus. The book to bill ratio for the quarter was only .81 compared to 1.02 on a trailing 12-month basis.

November Company Presentation

GIS is the current problem child for DXC Technology as far as declining revenues. The company is in the process of moving more of its and its client business to the cloud and plans to sell at $200 million worth of facilities in 2024 to improve margins and cash flow. Its GBS unit saw organic growth of 2.4% on a year-over-year basis and is now nearly half (49.7%) of overall sales.

November Company Presentation

DXC Technology had capital expenditures of $157 million during the quarter against $248 million in operational cash flow resulting in free cash flow of $91 million for the quarter.

Management’s FY2024 guidance is uninspiring except for its free cash flow goals.

November Company Presentation

Analyst Commentary & Balance Sheet:

The analyst community is not sanguine on DXC Technology’s prospects at the moment. Since the most recent quarterly earnings came out, five analyst firms including RBC Capital, Stifel Nicolaus and Citigroup have all reissued Hold/Neutral ratings on the stock. Three of these ratings contained minor downward price target revisions. Price targets proffered range from $21 to $24 a share.

Approximately six percent of the outstanding float in the shares are currently held short. The company’s General Counsel sold just over $1.5 million worth of shares on August 24th. That has been the only insider activity in the stock so far in 2023.

November Company Presentation

According to DXC Technology’s third quarter 10-Q, the company ended the quarter with just over $1.4 billion in cash and marketable securities on its balance sheet. The company ended the quarter with $3.791 billion in long-term debt, down from $3.9 billion at the end of the first quarter it should be noted. However, thanks to rising rates, interest expense was $78 million in the quarter compared to $44 million in the same period a year ago.

November Company Presentation

The company has retired over 10% of its outstanding shares so far in 2023 and just over 25% since the beginning of 2022. DXC Technology still has $500 million left on a current stock repurchase authorization as well. The company spent $214 million on stock buybacks during the quarter.

Verdict:

DXC Technology made $3.47 a share on just over $14.3 billion in revenue in FY2022. The current analyst firm consensus has sales dropping to just $13.7 billion in FY2023 and sees profits declining to $3.17 a share. They project earnings to rebound to $3.95 a share in FY2024 even as sales continue to slide to $13.44 billion.

DXC Technology Company stock is cheap by many metrics. The shares trade around seven times trailing earnings and just over 30% of annual revenues. Based on the fiscal second run rate, DXC has a free cash flow yield in the high single digits. That said, both earnings and revenues are expected to decline in FY2023, and the shares have no support in the analyst community.

I believe DXC Technology would be better served if it focused on paying down more debt instead of stock buybacks as well. The company pays no dividends. If interest rates continue to fall, this should be a nice tailwind to DXC given its debt levels.

That said, there seems little downside to DXC Technology Company shares here given valuations. The most likely scenario for DXC is the stock is likely to be rangebound in the low $20s through year end and early 2024. If it becomes more apparent the company can deliver its free cash flow guidance of $800 million in FY2024, the shares merit more consideration at that point.

There are three kinds of people: the haves, the have-nots, and the have-not-paid-for-what-they-haves.” – Earl Wilson.