MicroStockHub/iStock through Getty Pictures

Introduction

It is time to do two issues:

- Speak about cardboard and what it tells us in regards to the economic system.

- Focus on how engaging the 5%-yielding Worldwide Paper Firm (NYSE:IP) shares are for dividend buyers.

On Could 22, I wrote my most up-to-date article on Worldwide Paper, titled “How Attractive Is International Paper’s 6% Yield?”

Since then, the inventory is up greater than 20%, pushing the yield down to five%.

Now, we have to re-assess the chance/reward in mild of financial challenges and alternatives.

So, with out additional ado, let’s get to it!

Cardboard As A Main Indicator

Cardboard is not only a low-cost materials for packaging functions but in addition an ideal financial indicator. In any case, greater financial progress means extra demand for packaging supplies. A slower economic system signifies the precise reverse.

Earlier this month, the Wall Avenue Journal wrote an article titled What Cardboard Costs Inform Us About The State Of The Financial system.”

Wall Street Journal

According to the article, cardboard prices are on the rise, indicating a positive shift in the economy.

This marks the first increase in prices for cardboard since the Federal Reserve began raising interest rates early last year.

The uptick in cardboard prices suggests the end of the inventory hoarding trend observed during the post-pandemic recovery.

Historically, pricier cardboard has been associated with an accelerating economy, which is also good news for my personal consumer-focused investments like Norfolk Southern (NSC), the largest intermodal railroad in the East.

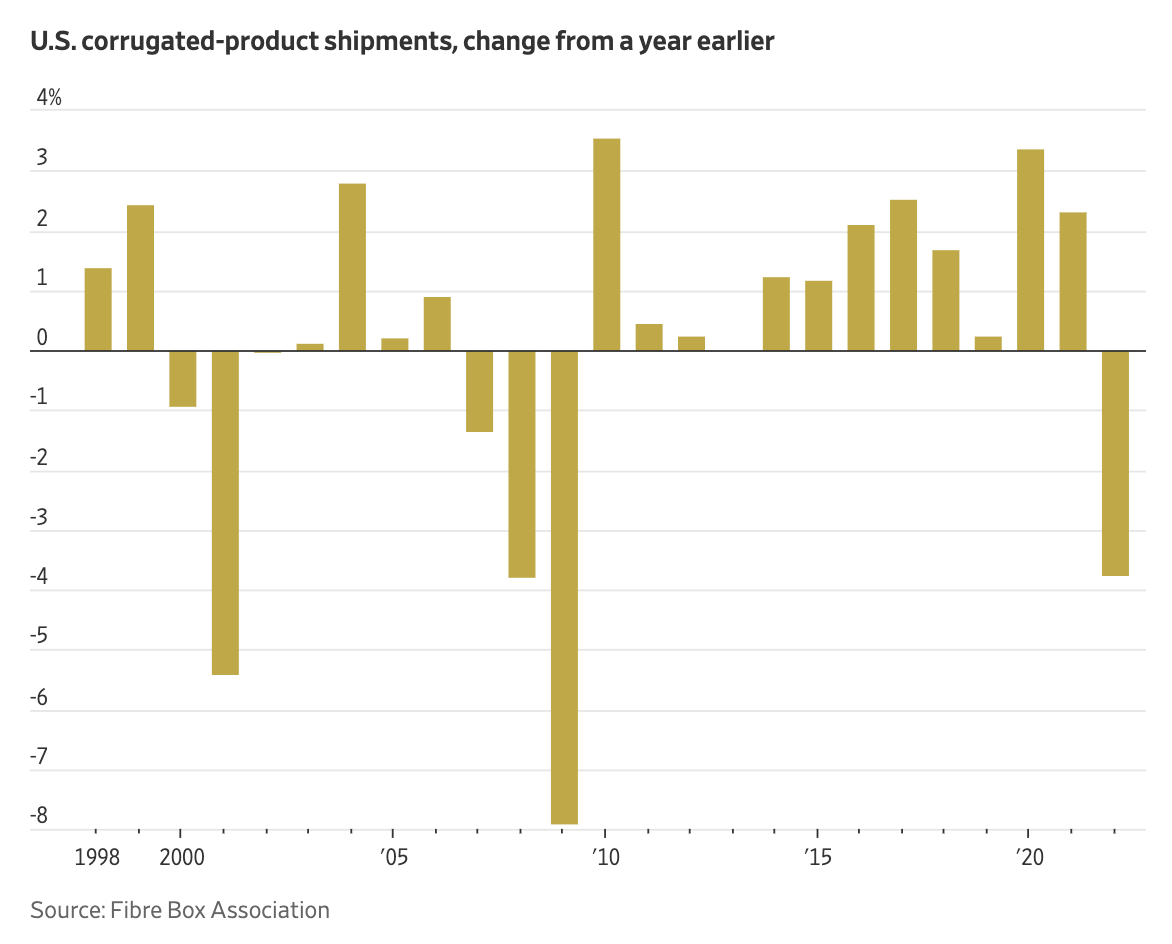

The chart below shows what cardboard shipments have looked like. Note the massive decline caused by inventory de-stocking and poor consumer health.

Wall Street Journal

Unfortunately, while the price hikes may signal economic revival, analysts caution that it’s too early to determine if these increases are sustainable or a one-time adjustment due to the unique circumstances of the pandemic.

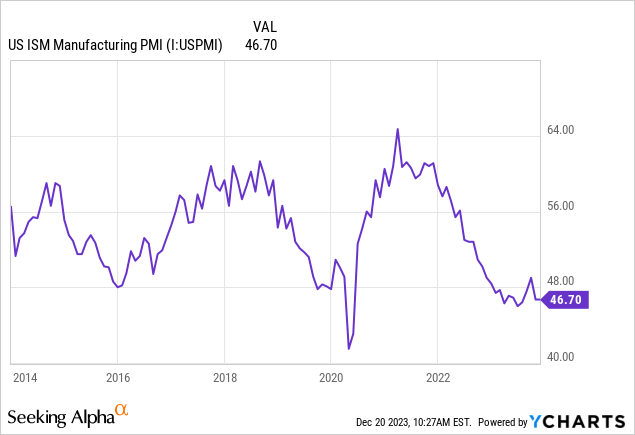

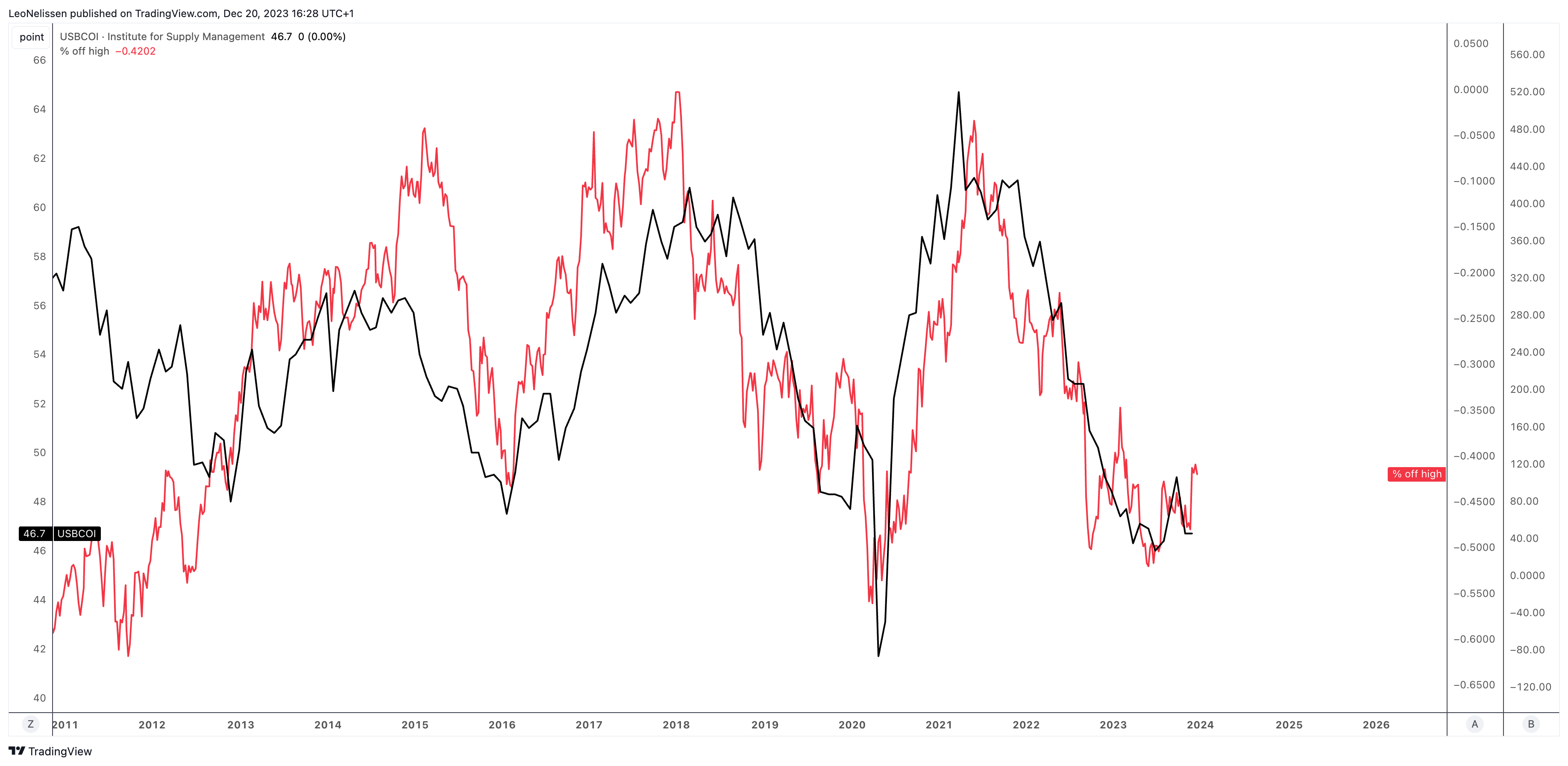

After all, this is what the ISM Manufacturing Index looks like, which is not bullish at all for demand expectations:

According to the article, major producers, including International Paper, WestRock (WRK), and Packaging Corp. of America (PKG), have announced price hikes effective January 1 for both types of containerboard used in making corrugated cardboard.

If the price increases hold, manufacturers stand to regain much of the pricing power they relinquished over the past two years.

Having that said, using the aforementioned ISM Manufacturing Index, we see that International paper investors have priced in a very poor economy, which is great news for the valuation (buy low, sell high).

The chart below compares the distance International Paper shares are trading below their high (in %, excluding dividends) compared to the ISM index (the black line).

TradingView (ISM Index, IP)

In general, the chart above perfectly shows how cyclical IP shares are.

With that said, before we can comment on the company’s risk/reward (which seems to be good, given how much weakness has been priced in), we need to take a closer look at its financials.

International Paper Is Improving Its Business

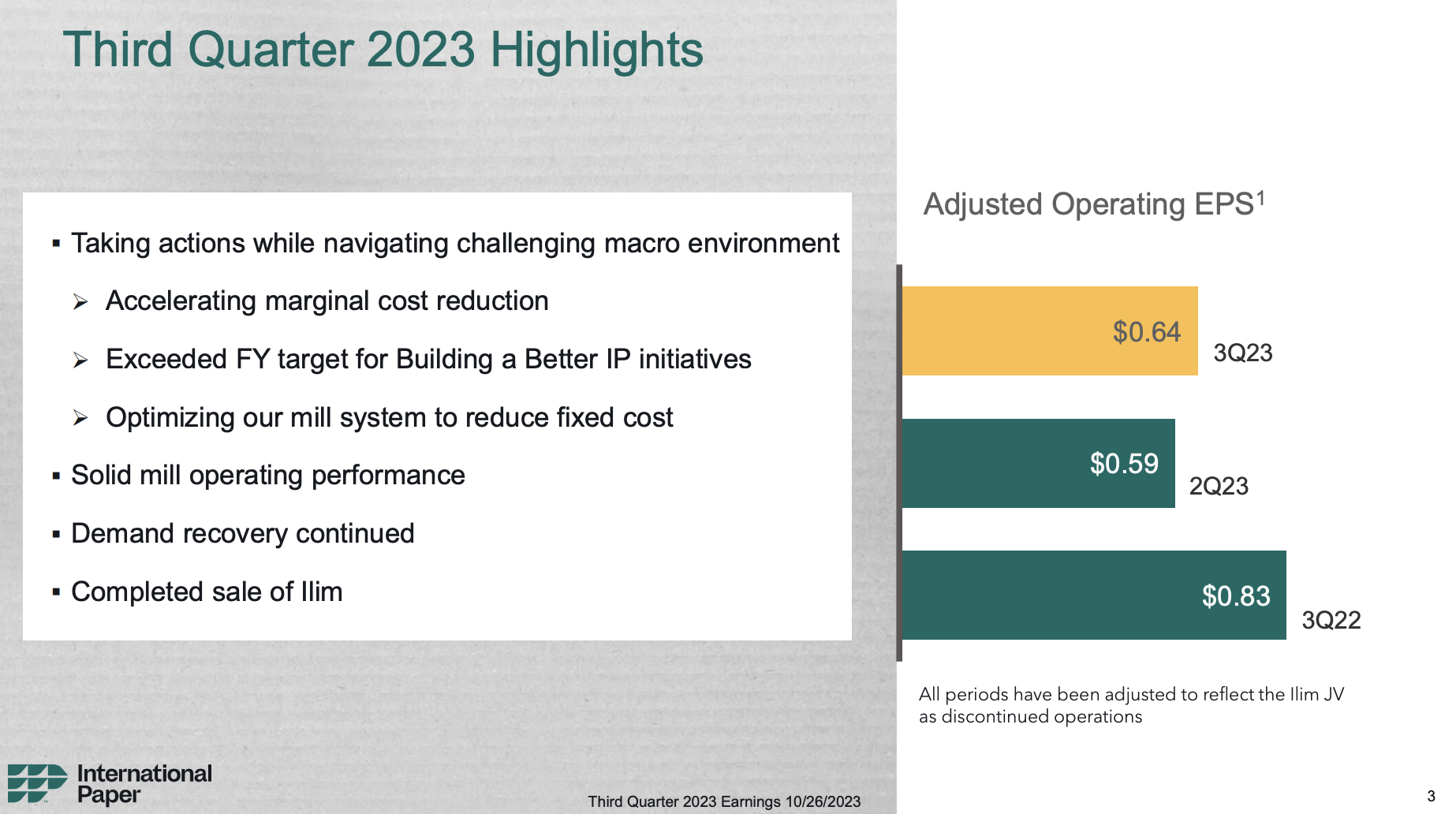

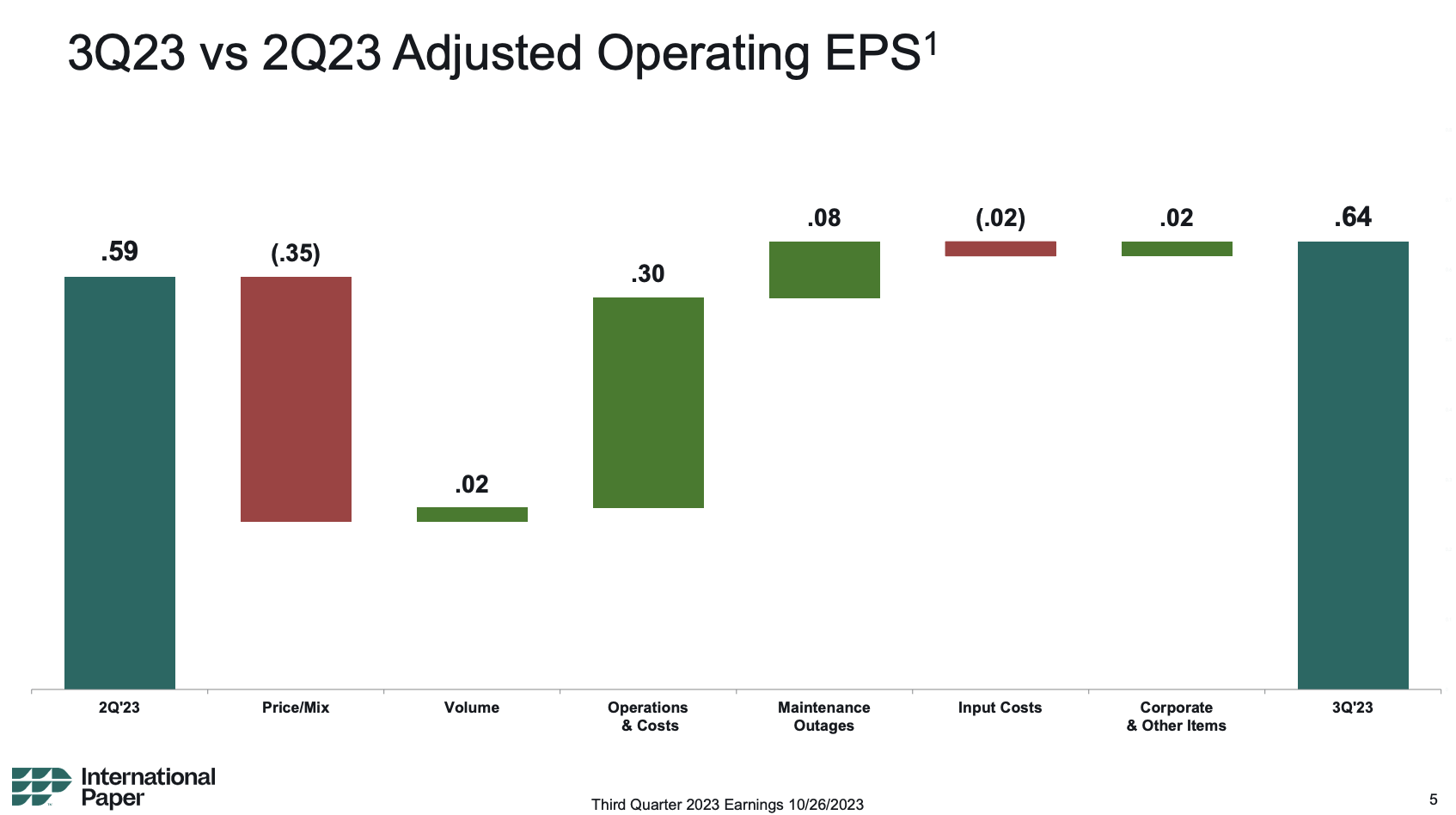

In the third quarter of 2023, International Paper showed a strong financial performance driven by strategic initiatives and a recovering demand environment, which aligns with the findings from the Wall Street Journal we discussed in the first part of this article.

Nonetheless, adjusted EPS fell from $0.83 in the prior-year quarter to $0.64.

International Paper

With that said, as one can imagine, International Paper cannot really do anything about the demand environment.

What it can do is improve its business, which I already briefly mentioned.

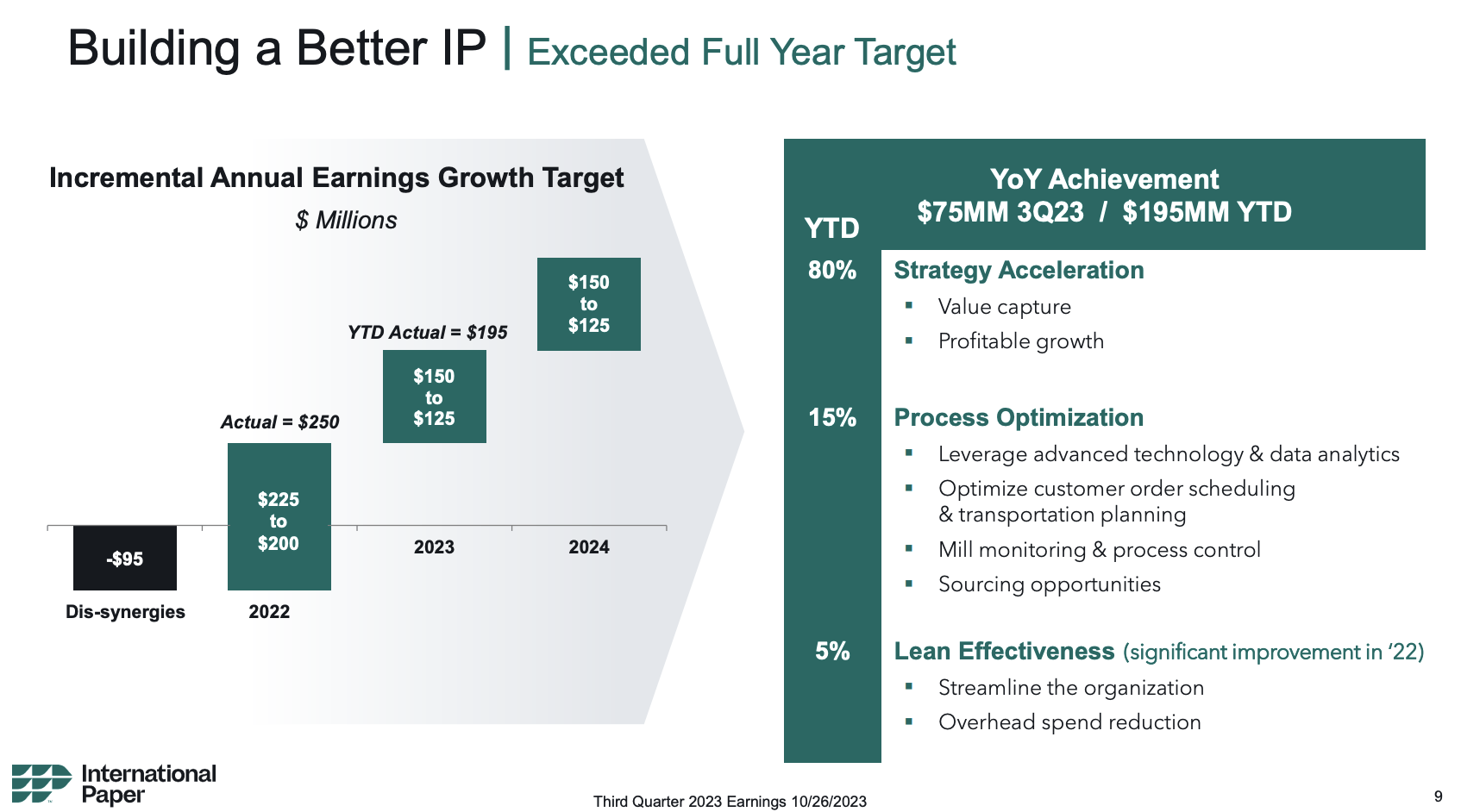

The company has a “Constructing a Higher IP” program, which played a major role in the better-than-expected financial results.

The program emphasizes strategy acceleration initiatives, focusing on creating value for customers, improving the profitability of products and services, and growing in attractive segments and regions.

The program also includes process optimization initiatives, leveraging advanced technologies and big data to identify new ways to enhance productivity and reduce costs across the large system.

International Paper

International Paper exceeded expectations by delivering $75 million in year-over-year incremental earnings benefits during the third quarter. This program, focused on commercial and process improvements, has proven effective, contributing a total of $195 million year-to-date, surpassing the full-year target for the second consecutive year.

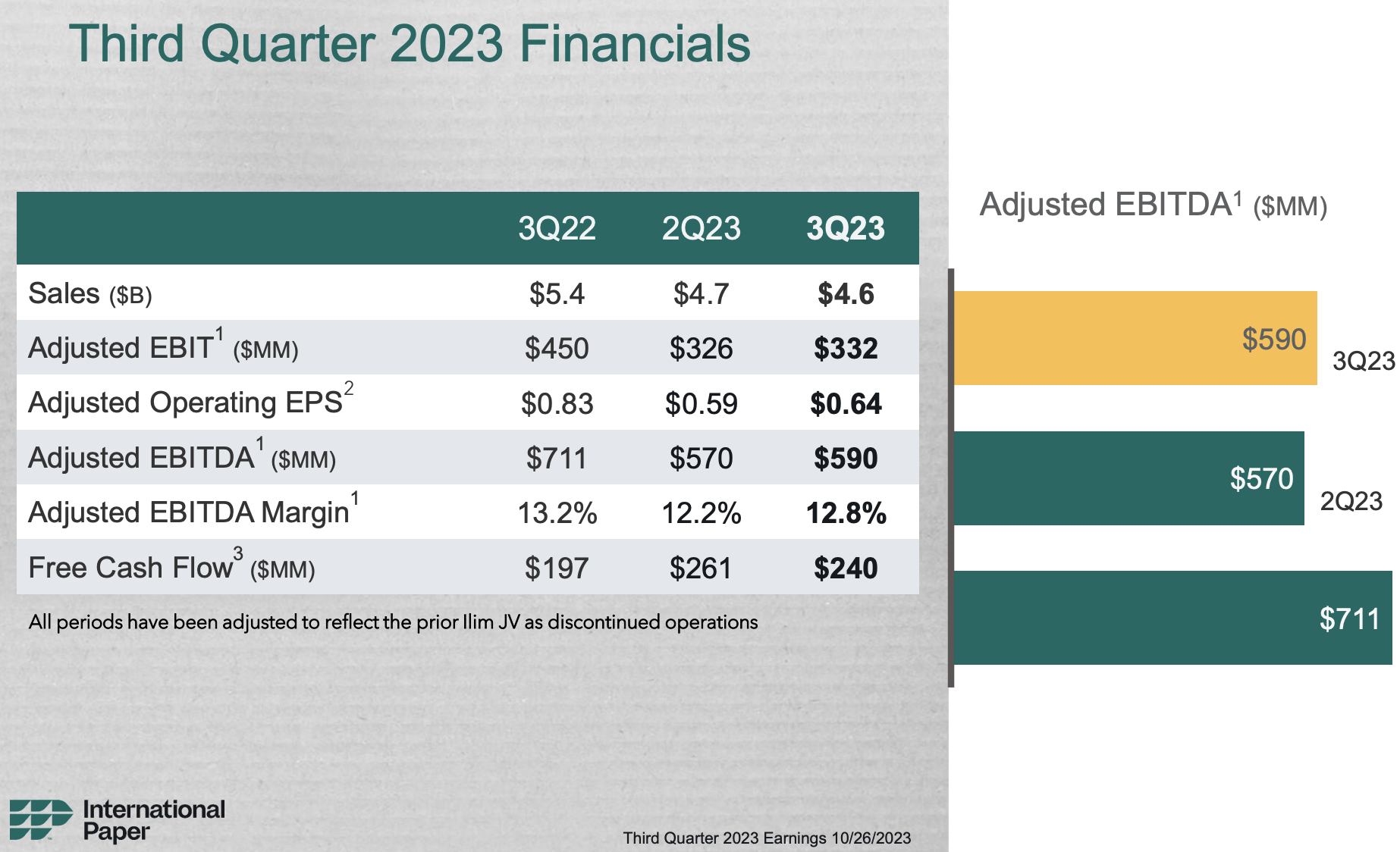

As we can see below, it helped to stabilize adjusted EBITDA and margins. Year-over-year, it also saw higher free cash flow.

International Paper

The overview below shows that benefits in the operations and cost segment almost erased the entire decline caused by price/mix headwinds.

International Paper

As one can imagine, despite the overall positive results, during the earnings call, the company acknowledged the need for additional actions to strengthen its business and improve profitability.

The strategic decisions, such as the permanent closure of the containerboard mill in Orange, Texas, and two pulp machines, demonstrate a commitment to optimizing the business portfolio and reducing fixed costs. These decisions, while challenging, are essential for achieving long-term objectives.

Moreover, International Paper successfully completed a strategic action by selling its ownership interest in the Ilim joint venture in Russia. The $508 million in proceeds from this sale align with the company’s focus on optimizing its global footprint and divesting non-core assets. With this move, International Paper no longer maintains any investment in Russia.

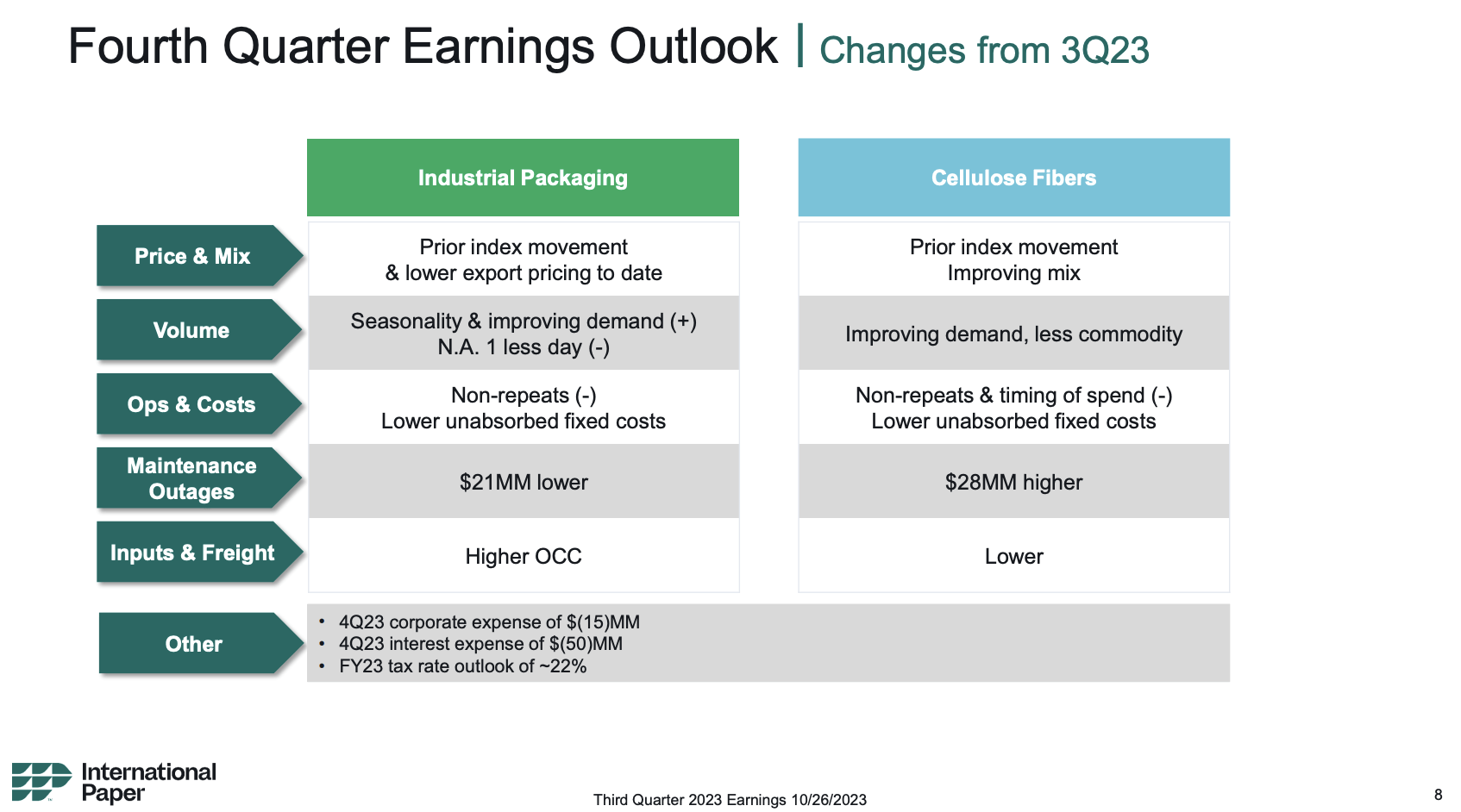

Looking ahead, International Paper sees business opportunities amid the improving demand environment.

The company is optimistic about the continued recovery across its portfolio and expects this positive trend to persist in the future.

International Paper

So, what does this imply for shareholders?

Shareholder Worth

Analysts do not believe that IP will see bottoming earnings in 2023.

Using the data in the overview below:

- EPS is expected to decline by 46% this year. Next year is expected to see a 14% EPS decline. This is not unusual, as industry declines often take two years. It also happened in 2009/2009 and 2019/2020. The stock, more often than not, bottoms during the first year.

- In 2025, EPS is expected to grow by 33%.

FAST Graphs

Needless to say, these numbers are subject to adjustments. If we were to see a bottom in the ISM index next year, we could see a meaningful increase in EPS expectations.

However, even using these numbers, the risk/reward is quite good.

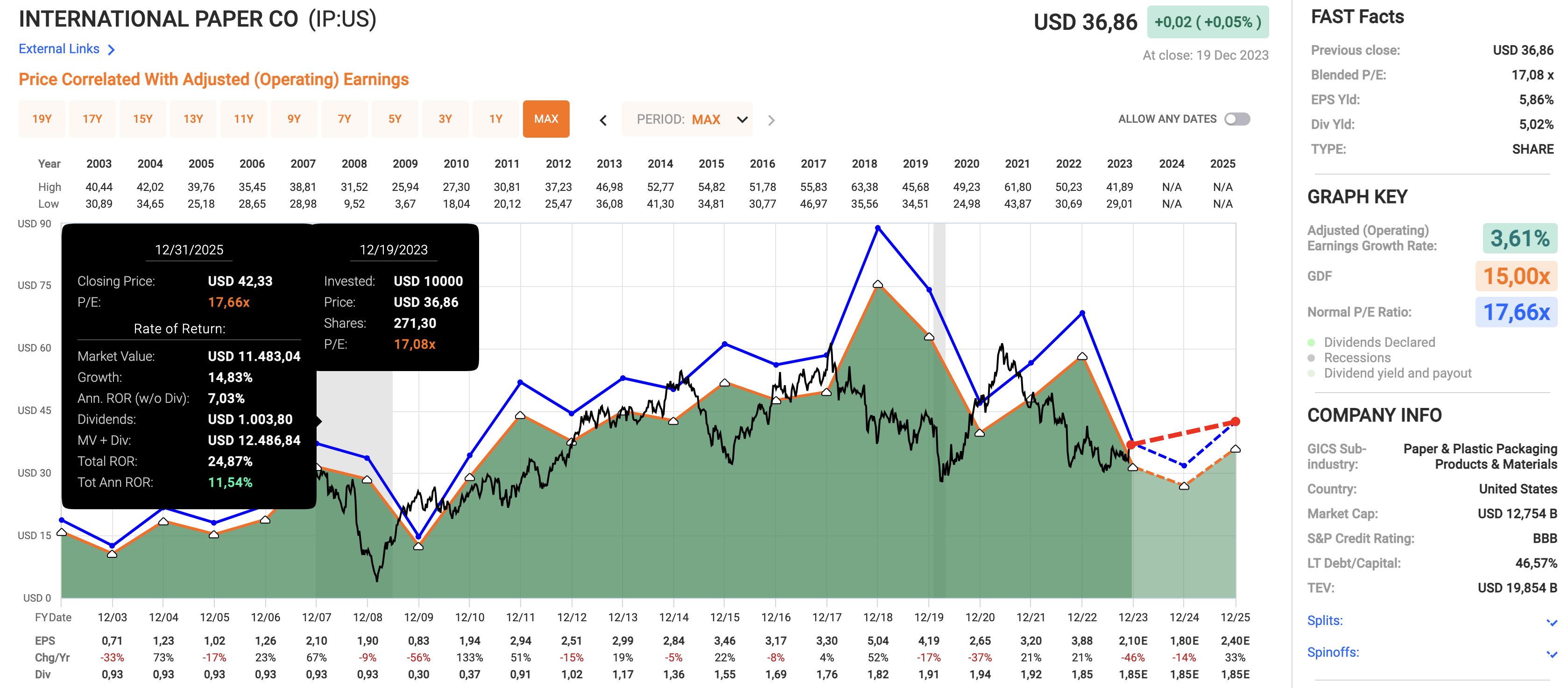

Again, using the data in the chart above, the company is trading at a blended P/E ratio of 17.1x. This is slightly below its long-term normalized multiple of 17.7x.

A return to that valuation by incorporation of the expected earnings growth numbers indicates a fair price target of $42, which is 13% above the current price.

I believe that is a fair number, with more upside if the economy were to bottom next year. In such a scenario, I see room to rise to $60-$65.

It also has a juicy yield.

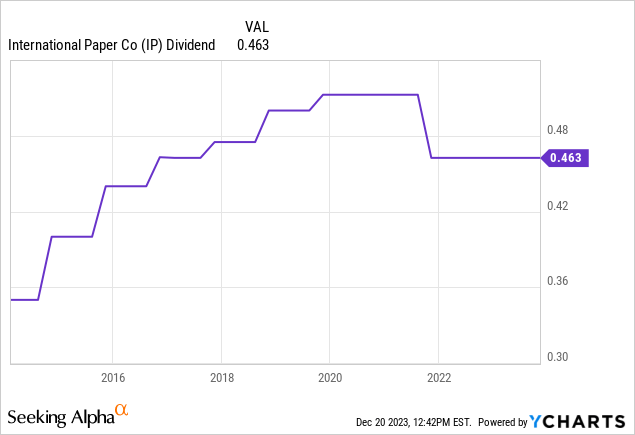

IP shares currently pay $0.4625 per share per quarter. This translates to a yield of 5.0%.

This dividend is protected by a 100% cash payout ratio. In this case, I’m using this year’s free cash flow estimates ($630 million), which are just enough to cover the dividend.

Next year, free cash flow is expected to rise to roughly $700 million before potentially surging beyond $1.0 billion. In other words, the dividend is safe unless we enter a deep recession. Even in such a scenario, a dividend cut would not be guaranteed, as one driver of higher expected free cash flow is lower capital expenses.

In 2021, the corporate cut its dividend by 10% on account of its printing paper spin-off.

“We’re dedicated to a aggressive and sustainable dividend of 40 to 50% of free money movement. The dividend adjustment we’re making is in line with our dividend coverage and is nicely under the 15 to twenty% adjustment we anticipated once we introduced the spin-off of our printing papers enterprise late final yr,” chairman & CEO Mark Sutton commented.

It also helps that the company maintains a healthy balance sheet.

It has an expected 2023E net leverage ratio of 2.1x EBITDA and an investment-grade BBB credit rating.

Overall, I believe that IP shares offer a good risk/reward for long-term investors. They have priced in a lot of economic weakness and are likely to see meaningful EPS adjustments once the U.S. economy starts a recovery.

However, the company is highly cyclical. This may not be a suitable dividend income stock for every type of investor.

For a 5.0% yield, investors can also opt for safer income plays like certain utilities (even if they yield a bit lower) or certain consumer staple stocks like 4.4%-yielding Kraft Heinz (KHC), just to give you a few examples of alternatives with (likely) lower risks.

That said, I like IP at these prices and believe it will trade much higher over the next 12 to 24 months.

But then again, it’s cyclical, and its long-term risk/reward is poor, which means it may not be the right stock for you.

Takeaway

Despite a projected short-term dip in earnings, International Paper’s attractive valuation, a 5.0% dividend yield, and a commitment to sustainability make it a compelling long-term investment.

With an optimistic outlook amid economic recovery, International Paper presents a promising opportunity for those eyeing long-term value in the paper and packaging sector.

Nonetheless, potential buyers ought to contemplate its cyclical nature and discover alternate options primarily based on danger tolerance.