marrio31

Overview

As a basic precept, we are inclined to suppose an economic system’s recession threat is decrease when it has spare capability and better when it’s overheated. The explanations for this are twofold:

- 1. Overheated economies generate extra inflation. Inflation forces authorities to implement restrictive insurance policies to decelerate mixture demand. Recessions is usually a desired or unintended results of this adjustment course of.

- 2. Overheated economies are inclined to have extra imbalances and vulnerabilities (e.g., overinvestment in 2000 created a capital overhang, client and banking system leverage in 2007 created well-known market failures and saddled the economic system with years of deleveraging). Imbalances enhance fragility and amplify the slowdown in financial progress.

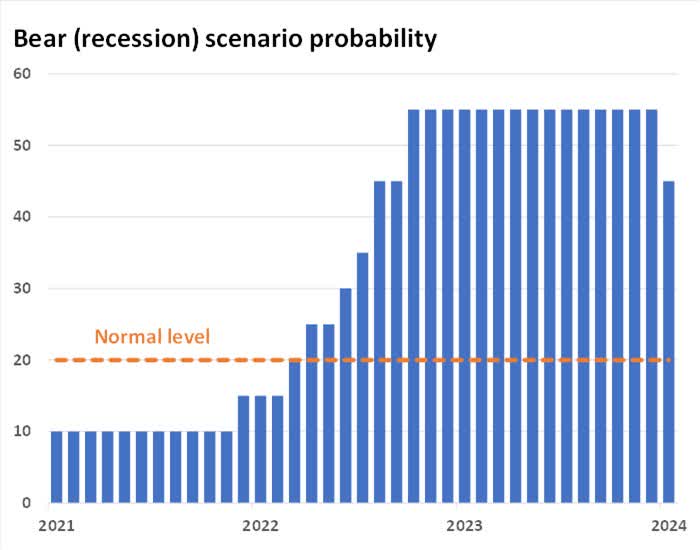

As proof of an overheated labor market and speedy Fed tightening cycle collected within the spring of 2022, we quickly lower our U.S. cycle outlook and raised our recession possibilities to mirror these customary macro threat channels.

A recession has, after all, not but materialized. The economic system is not as overheated, inflation pressures have eased, and—with this progress—policymakers are pivoting to contemplate charge cuts. Collectively, these developments lower the recession risk from 55% to 45% in our view.

Supply: Russell Investments. January 2024.

We proceed to suppose that, ought to a recession materialize, it could be a light or reasonable downturn given the dearth of main imbalances within the economic system.

Inflation continues to say no

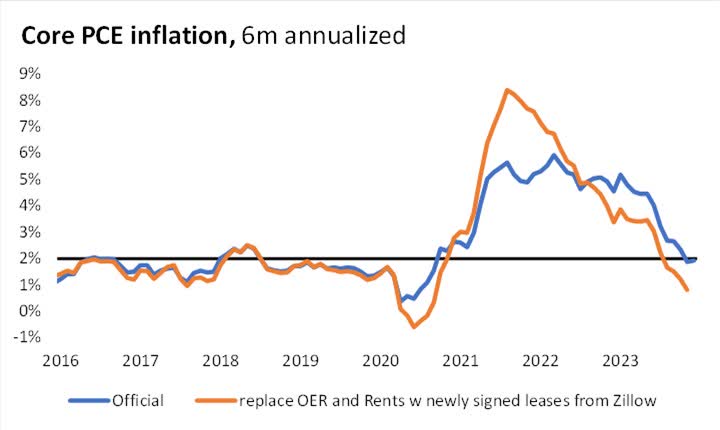

Inflation has come down quickly in current months. Core PCE (private consumption expenditures) inflation on a six-month annualized foundation was already working at 2% as of November and the CPI (client worth index) knowledge for December means that progress is more likely to maintain (see the blue line within the chart under). Moreover, it’s well-known that the shelter element of U.S. inflation indices lags developments in dwelling costs and rents. Timelier measures of rents have normalized again to pre-COVID ranges and recommend additional disinflationary progress is within the pipeline (orange).

Supply: BEA, Zillow, Russell Investments. December 2023 is estimated.

Fed outlook

The Fed’s precondition for returning rates of interest to a impartial setting (i.e., charge cuts again to a federal funds charge of two.5% to three%) is when inflation is “clearly moving down sustainably toward the Committee’s objective”. As flagged above, we’re already approaching that situation on some measures. This opens the door for a primary lower as early as March.

Moreover, the Fed’s threat administration has pivoted in current months. As lately as September 2023, the Fed and market had embraced a higher-for-longer narrative. However simply three months later, Powell mentioned the central financial institution is concentrated on attempting to not make the error of staying excessive for too lengthy, stating that, “We’re aware of the risk that we would hang on too long. We know that’s a risk, and we’re very focused on not making that mistake … we’ve come back into a better balance between the risk of overdoing it and the risk of underdoing it.”

Labor market is cooling

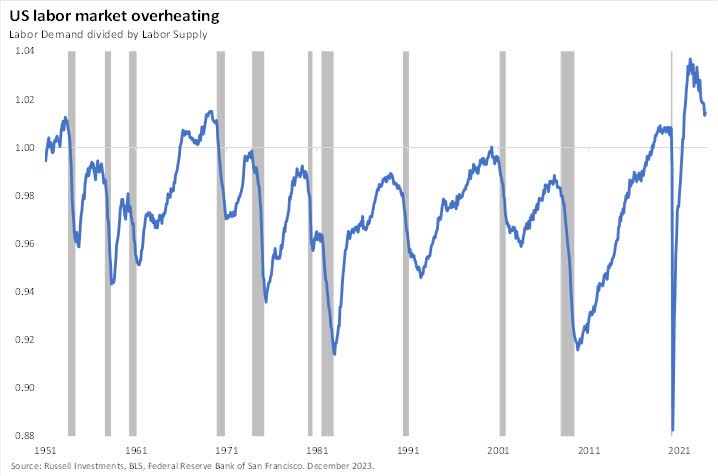

A 12 months in the past, famed economist Larry Summers mentioned that “soft landings are like second marriages…they are the triumph of hope over experience”. The requisite labor market rebalancing he was involved about and that I’ve been involved about has turned out to be painless up to now. Job openings have declined considerably with no commensurate rise in layoffs. That is exceptional within the post-war historical past of america and is welcome information. The chart under reveals that about 60% of the overheating from 2022 has gone away.

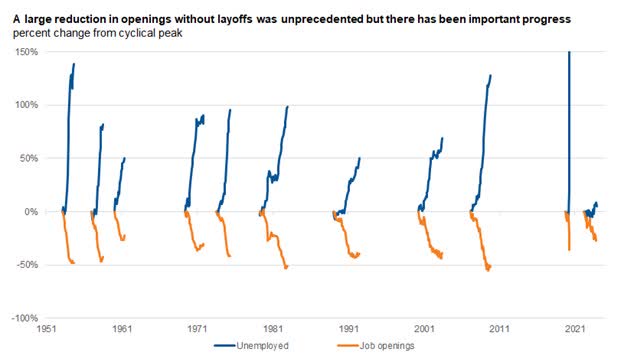

The following chart decomposes the demand facet of this labor market adjustment and reveals how uncommon the present expertise is in a historic context. At every labor market peak, we observe the following strikes in job openings and unemployment. There isn’t any precedent for a big decline in job openings (orange) with out a big rise in unemployment (blue). However up to now, so good.

Supply: BLS, Russell Investments. December 2023

Immigration and a rise in labor drive participation have additionally supported the labor market adjustment from the provision facet.

The dangers of slicing an excessive amount of and too little

Given the U.S. economic system remains to be working at a sub-4% unemployment charge, there’s a threat that too many charge cuts and an easing of monetary situations might enhance financial progress on the expense of a stickier—and even reaccelerating—inflation drawback.

There’s additionally a threat that any Fed easing in 2024 may very well be too little, too late. Lags from financial coverage onto the economic system, weak main financial indicators, slower and narrowing employment progress, and a variety of different elements recommend draw back dangers haven’t utterly gone away.

Market implications

Equities

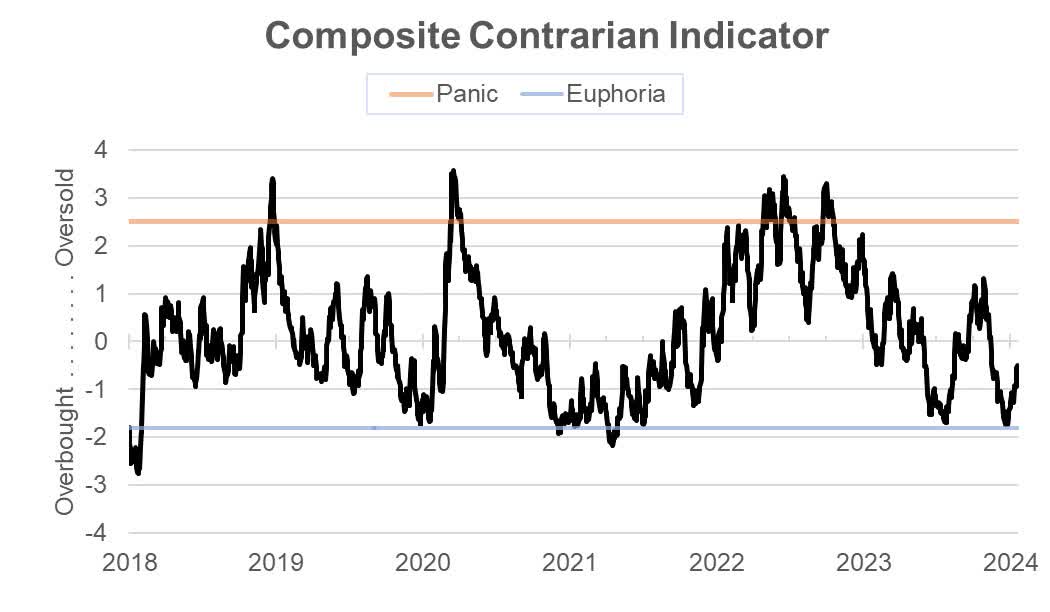

Equities already seem like pricing in a sanguine outlook. Valuations look costly, sentiment is directionally overbought (see chart under), and consensus earnings expectations seem very optimistic. At Russell Investments, we proceed to advise purchasers to maintain fairness allocations close to long-term strategic targets and don’t suppose it’s prudent to vary that based mostly on this modification in our financial eventualities.

Supply: Russell Investments, as of Jan. 22, 2024.

Charges

The decline in Treasury yields within the fourth quarter, coupled with our decrease recession possibilities, does recommend the worth in Treasuries has narrowed considerably. Valuations nonetheless seem low-cost, however much less so.

The underside line

We imagine that the painless labor market rebalancing, disinflation, and Fed pivot make it extra seemingly the U.S. economic system will keep away from recession in 2024. In mild of this, we have now lowered our U.S. recession likelihood from 55% to 45%. Nonetheless, it’s essential to grasp that recession dangers stay greater than regular even after this modification. From our vantage level, buyers could be best-served sticking to their strategic asset allocations.

Disclosures

These views are topic to vary at any time based mostly upon market or different situations and are present as of the date on the prime of the web page. The knowledge, evaluation, and opinions expressed herein are for basic info solely and should not supposed to offer particular recommendation or suggestions for any particular person or entity.

This materials just isn’t a proposal, solicitation or suggestion to buy any safety.

Forecasting represents predictions of market costs and/or quantity patterns using various analytical knowledge. It isn’t consultant of a projection of the inventory market, or of any particular funding.

Nothing contained on this materials is meant to represent authorized, tax, securities or funding recommendation, nor an opinion relating to the appropriateness of any funding. The final info contained on this publication shouldn’t be acted upon with out acquiring particular authorized, tax and funding recommendation from a licensed skilled.

Please do not forget that all investments carry some stage of threat, together with the potential lack of principal invested. They don’t sometimes develop at an excellent charge of return and will expertise damaging progress. As with every kind of portfolio structuring, making an attempt to cut back threat and enhance return might, at sure occasions, unintentionally scale back returns.

The knowledge, evaluation and opinions expressed herein are for basic info solely and should not supposed to offer particular recommendation or suggestions for any particular person entity.

Frank Russell Firm is the proprietor of the Russell logos contained on this materials and all trademark rights associated to the Russell logos, which the members of the Russell Investments group of firms are permitted to make use of below license from Frank Russell Firm. The members of the Russell Investments group of firms should not affiliated in any method with Frank Russell Firm or any entity working below the “FTSE RUSSELL” model.

The Russell brand is a trademark and repair mark of Russell Investments.

This materials is proprietary and is probably not reproduced, transferred, or distributed in any type with out prior written permission from Russell Investments. It’s delivered on an “as is” foundation with out guarantee.

CORP-12397