JHVEPhoto

I’ve underestimated biopharma firm AbbVie Inc.’s (NYSE:ABBV) means to beat the near- and medium-term headwinds from Humira’s LOE. I assessed that the chance/reward of ABBV was well-balanced in my earlier replace in late November 2023. Nevertheless, that Maintain/Impartial thesis has proved to be too cautious. I had anticipated promoting stress to accentuate, probably resulting in a drop to the $130 help stage earlier than bottoming out.

Nevertheless, the market has spoken. ABBV patrons returned with conviction, serving to the inventory stage a resilient backside near the $130 zone in November. AbbVie’s fourth-quarter earnings launch in February 2024 possible justified the market’s optimism, as AbbVie demonstrated its means to forge forward with its ex-Humira progress portfolio.

Accordingly, AbbVie posted an 8% income progress for FY23 for its ex-Humira portfolio. In This fall, AbbVie posted a 15% progress. Because of this, I assessed that AbbVie has corroborated its long-term outlook as buyers look previous the headwinds from Humira’s LOE. Administration underscored that AbbVie’s “diversified growth platform efficiently absorbed” the “largest loss of exclusivity event in the industry.”

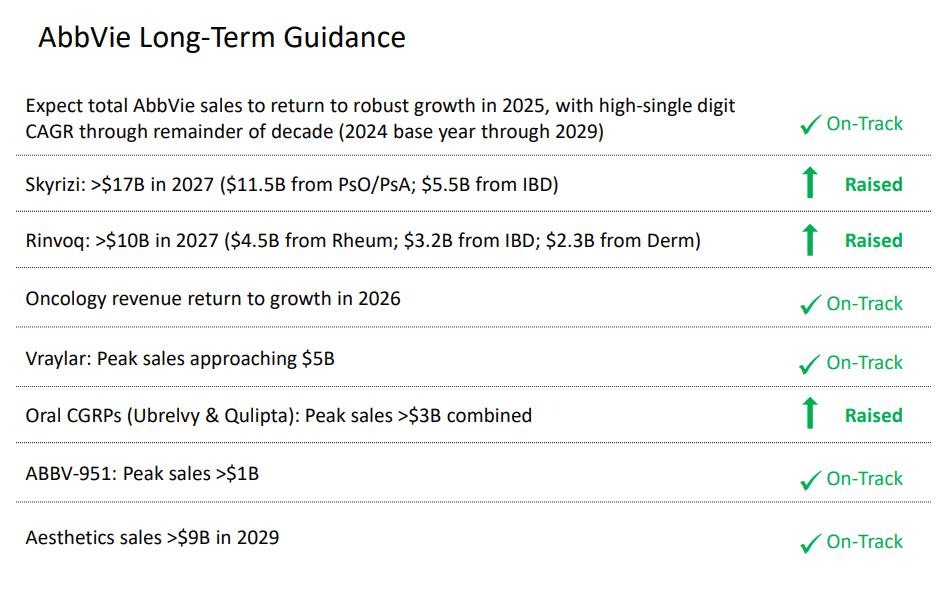

AbbVie delivered outstanding metrics in Skyrizi and Rinvoq, notching income progress of 52% and 63% in FY23, respectively. Moreover, AbbVie additionally lifted its long-term outlook for each the blockbusters, probably reaching a excessive of $27B in mixed annualized gross sales by 2027, up $6B from AbbVie’s earlier steering. Because of this, it is anticipated to blow previous Humira’s peak sales of $21B notched in 2022, showcasing AbbVie’s functionality to handle Humira’s LOE competently.

AbbVie long-term steering (AbbVie filings)

Moreover, administration assured buyers of AbbVie’s upgraded long-term steering. Its current acquisitions of ImmunoGen and Cerevel have additionally contributed to the corporate’s income trajectory, decreasing execution dangers. Administration highlighted that its long-term outlook has contemplated its current acquisition. Accordingly, AbbVie telegraphed a midpoint adjusted EPS of $11.15 for FY24. Analysts’ estimates recommend AbbVie’s outlook could possibly be conservative, as they penciled in an adjusted EPS forecast of $11.21.

Moreover, AbbVie maintained its long-term income steering of attaining a excessive single-digit income CAGR by means of 2029. AbbVie hasn’t materially upgraded its long-term outlook. Nevertheless, I consider the market has diminished its evaluation of AbbVie’s execution dangers, given its strong efficiency and robust steering of its ex-Humira portfolio. Because of this, I assessed it was justified for the market to re-rate ABBV’s earnings multiples, contemplating the upper income visibility attributed to its progress portfolio.

ABBV is valued at a ahead adjusted EBITDA a number of of 14x, effectively above its 10Y common of 10.6x. In different phrases, the market has quickly mirrored its optimism over its long-term potential, repricing it increased. In my earlier replace, I ought to have been extra optimistic about AbbVie’s means to beat Humira’s LOE dangers. Regardless of that, I will not all of the sudden go FOMO and begin chasing ABBV’s surging momentum. ABBV ought to stay a core play for healthcare buyers in a diversified portfolio. Nevertheless, buyers should be cautious about chasing its current surge, as ABBV seems more and more expensive.

ABBV value chart (weekly, medium-term, dividend adjusted) (TradingView)

Earnings buyers may level to ABBV’s comparatively enticing ahead dividend yield of three.4%. Nevertheless, ABBV’s 5Y complete return CAGR of 23.8% ought to inform buyers that ABBV is primarily a capital appreciation play. There’s little doubt that AbbVie is a high-quality and essentially sturdy healthcare inventory with a best-in-class “A+” profitability grade. Additionally, with ABBV recovering its long-term uptrend because it surged to a brand new excessive, I did not glean pink flags suggesting buyers ought to contemplate slicing their publicity.

In different phrases, buyers who missed including on AbbVie Inc.’s vital dips ought to contemplate assessing its subsequent pullback whereas ready patiently for an additional alternative so as to add to their positions.

Ranking: Preserve Maintain.

Necessary notice: Traders are reminded to do their due diligence and never depend on the data supplied as monetary recommendation. Please all the time apply unbiased pondering. Word that the score isn’t supposed to time a particular entry/exit on the level of writing, until in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a important hole in our view? Noticed one thing necessary that we didn’t? Agree or disagree? Remark under with the goal of serving to everybody in the neighborhood to study higher!