David Peperkamp

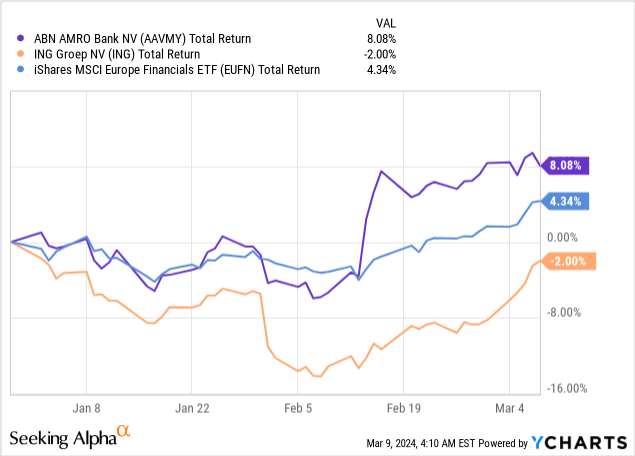

Shares of Dutch financial institution ABN AMRO (OTCPK:AAVMY)(OTC:ABMRF) have gotten off to a stable begin in 2024, returning round 8% year-to-date in USD phrases and outperforming each nationwide peer ING Groep (ING) as properly as the broader European monetary house (EUFN).

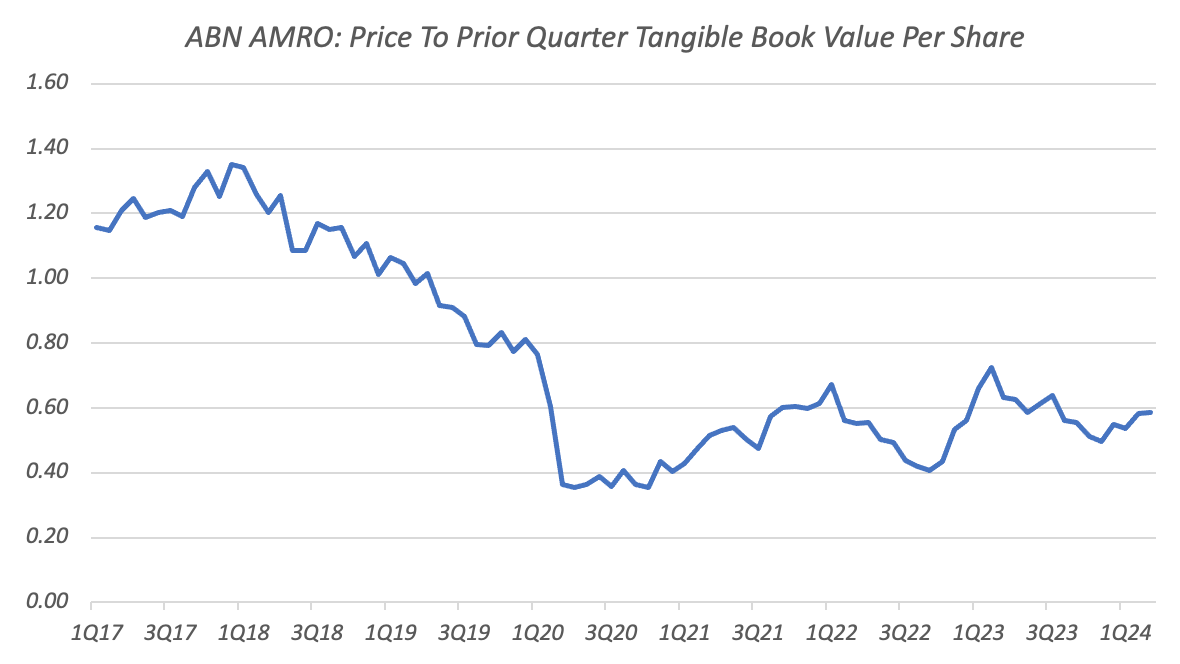

Covering the financial institution at first of the yr, I stated {that a} lack of readability concerning capital return plans and working bills was maybe holding the inventory again, with a then-valuation of simply 0.55x tangible e book worth per share (“TBVPS”) wanting too low cost relative to the financial institution’s earnings energy.

Although arguably a drag on the inventory, administration was at the least attributable to replace the market on each factors following This fall outcomes launched a number of weeks in the past, offering a possible catalyst ought to the outlook turn into a bit clearer for traders. That has certainly come to move, with the market reacting properly to extra element on capital returns, in addition to affordable This fall outcomes and ahead steerage. With the inventory nonetheless low cost and a few issues from final time addressed, I hold my Sturdy Purchase ranking in place.

Affordable Outcomes And Steerage

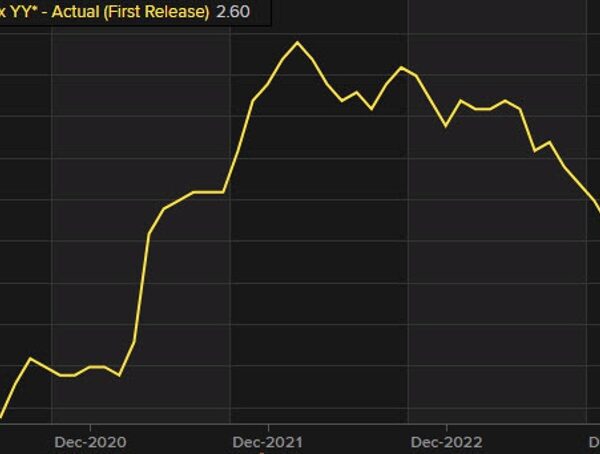

In distinction to recently-covered peer ING, ABN AMRO delivered a barely extra upbeat set of This fall outcomes and steerage, with web curiosity revenue (“NII”) touchdown somewhat larger than consensus on each counts. As NII accounts for round 70% of the financial institution’s income, developments on this line are key for general earnings.

With that, This fall NII of €1.504 billion was down round 2% sequentially however marginally forward of consensus, higher than at ING which missed consensus with a circa 4% quarter-on-quarter fall. Equally, This fall web curiosity margin of 152bps was a few factors forward of estimates. Whereas deposit migration from cheaper present and financial savings accounts to costlier time accounts continues to be a headwind, this has slowed down considerably, according to administration.

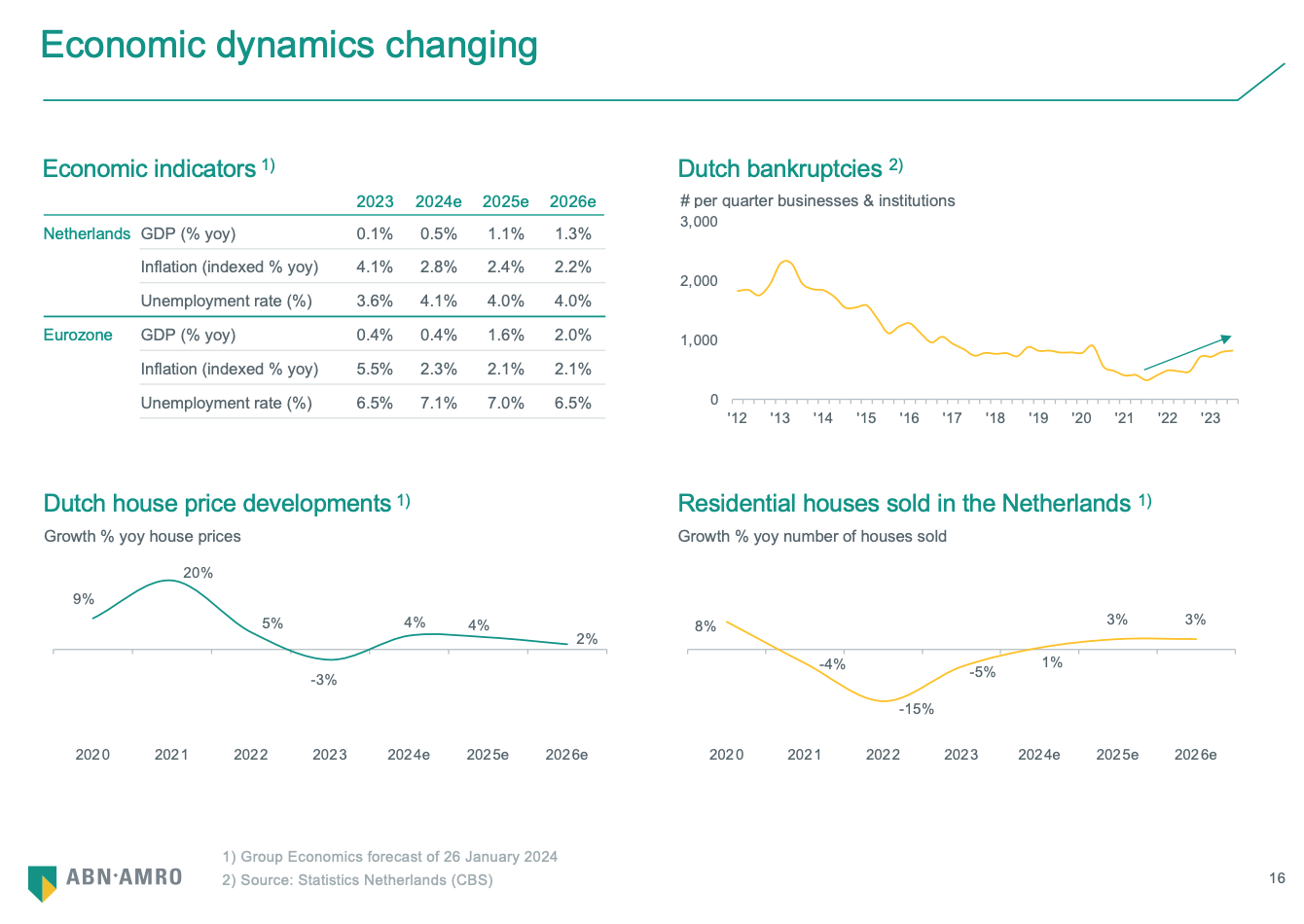

Mortgage progress additionally stays a problem, with shopper loans down somewhat over 1% sequentially to €240 billion as larger rates of interest proceed to sap demand for credit score. Mortgage loans (~64% of the e book) had been principally flat quarter-on-quarter at €151 billion, with some tentative constructive indicators wanting ahead as home value progress and transaction numbers are tentatively rebounding.

Supply: ABN AMRO This fall 2023 Outcomes Presentation

Positively, administration steerage for flat NII was higher than anticipated, with pre-results steerage pointing to a low single-digit year-on-year decline in 2024. That is additionally extra upbeat than at ING, the place administration expects NII to fall round 5% this yr.

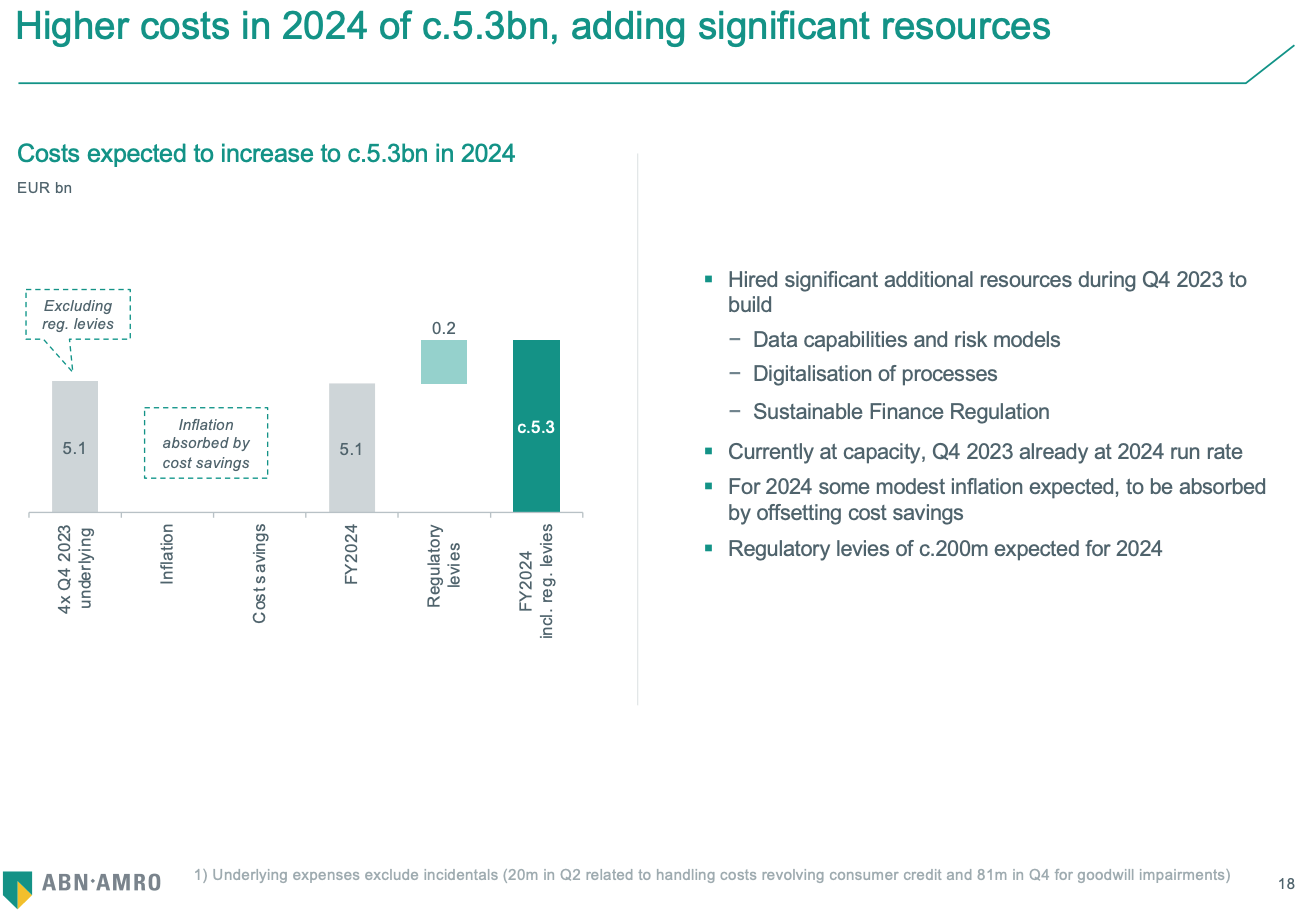

Bills had been a little bit of a combined bag. At €1.46 billion, working prices in This fall had been round 6% larger than consensus, whereas 2024 steerage of €5.3 billion was likewise heavier than anticipated pre-results. Nonetheless, readability on OpEx is welcome even when it does land on the upper facet, as this was unsure in earlier protection provided that administration had ditched prior targets attributable to inflation.

Supply: ABN AMRO This fall 2023 Outcomes Presentation

Extra positively, credit score prices continued to be a boon for the underside line final quarter, with the financial institution reserving an €83 million launch versus expectations of a ~€100 million cost. That in the end drove a big beat on web revenue, which at €523 million was round 30% forward of consensus. Whereas this is not a sustainable supply of earnings progress, administration did barely decrease through-the-cycle credit score value steerage, with this now seen at 15-20bps versus 20bps beforehand. This appears affordable given the now-completed wind down of non-core loans in its company e book (~32% of complete loans). Credit score high quality usually stays wonderful, with the late ratio bettering sequentially and nonetheless under ranges seen pre-COVID regardless of the considerably larger rate of interest surroundings.

Extra Coloration On Capital Returns Welcome

Wanting forward, administration offered a lot of the shifting elements essential to supply a tough earnings estimate for 2024. NII and OpEx steerage have already been talked about above, whereas payment revenue is seen up 3-5% and credit score prices seen “at the lower end” of administration’s 15-20bps through-the-cycle vary. All advised, that ought to get us to 2024 web revenue of round €2 billion after non-controlling pursuits and capital securities (i.e. AT1), which might map to a return on tangible fairness of roughly 9%.

Now, that is by-and-large consistent with pre-results consensus, with higher than anticipated strains like NII and credit score value offsetting larger than anticipated working prices. The extra welcome growth is that administration additionally offered extra colour on capital returns, partially eradicating a key overhang from earlier protection.

Beforehand, ABN AMRO was pretty constant on this entrance, delivering €500 million in annual buybacks over the previous three years alongside a tough dividend payout ratio equating to 50% of web revenue. Nevertheless, with this equating to a ~75% shareholder payout ratio general, it was unclear what was stopping administration from going even more durable on capital returns given the financial institution’s excessive capital ratio and comparatively minimal reinvestment wants.

Administration has now offered extra element on its intention to return surplus capital to shareholders, guiding for a 2026% CET1 ratio of 13.5% versus round 15% on the finish of 2023. Given 2024 buybacks have already been set at €500 million, this suggests a major step-up in 2025 and 2026. Maybe extra importantly, this transfer additionally de-links capital returns potential from earnings to an extent, and as such, I view it’s a welcome growth for traders.

Valuation Solely Marginally Extra Costly

At €14.95 in Amsterdam buying and selling ($16.39 per ADS), ABN AMRO has gained round 8% in share value appreciation since earlier protection. Nevertheless, this solely makes the inventory marginally costlier, as TBVPS has additionally elevated in that point, ending 2023 at roughly €25.50 per share (~$27.90 per ADS).

This a number of continues to look a lot too low cost relative to the financial institution’s earnings energy. At slightly below 0.6x TBVPS, ABN AMRO might theoretically return 13-15% to shareholders, assuming an 8-9% return on tangible fairness as per above. As a result of administration additionally intends to return extra capital to shareholders, traders could be moderately assured that the payout ratio right here will certainly be pretty near 100% of web revenue over the subsequent few years. Or stated otherwise, on the present share value traders might see larger than 10% every year returned by way of dividends and share buybacks.

Knowledge Supply: Yahoo Finance, ABN AMRO Quarterly Outcomes, Creator Calculation

With the inventory’s P/TBVPS a number of nonetheless under its latest historic common and providing upside to across the 0.8-0.9x space, ABN AMRO shares stay engaging, and I retain my Sturdy Purchase ranking.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.